Earnings Update Q1FY22

Earnings Update Q1FY22

You might also like

- How To Set Up A Suspension (Time) Histogram v2Document13 pagesHow To Set Up A Suspension (Time) Histogram v2Julian Morcillo100% (2)

- Kantar Worldpanel Division FMCG Monitor Full Year 2020 EN FinalDocument10 pagesKantar Worldpanel Division FMCG Monitor Full Year 2020 EN FinalvinhtamledangNo ratings yet

- Support For A Two-Dimensional Model of Conflict BehaviorDocument13 pagesSupport For A Two-Dimensional Model of Conflict BehaviorMariaIoanaTelecanNo ratings yet

- Pcem 06 Swot Analysis Kaha FinalDocument23 pagesPcem 06 Swot Analysis Kaha FinalziadNo ratings yet

- David Blueford Gaines - Racial Possibilities As Indicated by The Negroes of Arkansas (1898)Document198 pagesDavid Blueford Gaines - Racial Possibilities As Indicated by The Negroes of Arkansas (1898)chyoungNo ratings yet

- Sub: Raymond Limited - Investor Presentation: Rakesh Muljibh Ai DarjiDocument64 pagesSub: Raymond Limited - Investor Presentation: Rakesh Muljibh Ai DarjiSathwik PadamNo ratings yet

- Phiroze Jeejeebhoy Towers Dalal Street Mumbai - 400 001Document5 pagesPhiroze Jeejeebhoy Towers Dalal Street Mumbai - 400 001Namrata ShahNo ratings yet

- 91 Full Year Results Presentation May 2022Document41 pages91 Full Year Results Presentation May 2022floferNo ratings yet

- Overweight: Going Through Steep PathsDocument6 pagesOverweight: Going Through Steep PathsPutu Chantika Putri DhammayantiNo ratings yet

- YES Bank Presentation Q42018Document32 pagesYES Bank Presentation Q42018sanjeev7777No ratings yet

- Dilip Buildcon Q3FY18 - Result Update - Axis Direct - 20022018 - 20!02!2018 - 16Document6 pagesDilip Buildcon Q3FY18 - Result Update - Axis Direct - 20022018 - 20!02!2018 - 16MiteshNo ratings yet

- BritanniaDocument3 pagesBritanniaDhritiman DuttaNo ratings yet

- Realigning Estimate On Stronger Than Expected Mass Market: Bloomberry Resorts CorporationDocument8 pagesRealigning Estimate On Stronger Than Expected Mass Market: Bloomberry Resorts CorporationJajahinaNo ratings yet

- ITC - Deep Value Significant Opportunities To Unlock Value For ShareholdersDocument13 pagesITC - Deep Value Significant Opportunities To Unlock Value For ShareholdersYogeshNo ratings yet

- Nse: Itc PRICE: INR 203.10Document7 pagesNse: Itc PRICE: INR 203.10Shresth GuptaNo ratings yet

- Africa Day Presentation VDefDocument30 pagesAfrica Day Presentation VDefBernard BiboumNo ratings yet

- 91 Interim Results Presentation November 2021Document34 pages91 Interim Results Presentation November 2021floferNo ratings yet

- Nickel StudyDocument7 pagesNickel StudyILSEN N. DAETNo ratings yet

- FMCG Industry: $110 Billion 14% CAGR $110 Billion 14% CAGRDocument9 pagesFMCG Industry: $110 Billion 14% CAGR $110 Billion 14% CAGRShresth GuptaNo ratings yet

- Asian Paints: Volume Led Growth ContinuesDocument9 pagesAsian Paints: Volume Led Growth ContinuesanjugaduNo ratings yet

- SOK 2020 Annual ReportDocument158 pagesSOK 2020 Annual Reporttarikerkut44No ratings yet

- Group 1 - TBSL PDFDocument18 pagesGroup 1 - TBSL PDFAnkit BansalNo ratings yet

- Radico Khaitan Ltd. Earnings Presentation: Q4 and Full Year FY2020Document23 pagesRadico Khaitan Ltd. Earnings Presentation: Q4 and Full Year FY2020UmangNo ratings yet

- Ambev Presentation Dec.19Document22 pagesAmbev Presentation Dec.19arthurNo ratings yet

- Company Overview: Source: Investor Presentation Q4 2019Document10 pagesCompany Overview: Source: Investor Presentation Q4 2019Radhika IyerNo ratings yet

- Avenue Supermarts Sell: Result UpdateDocument6 pagesAvenue Supermarts Sell: Result UpdateAshokNo ratings yet

- Acrysil Investor Presentation 31102018Document34 pagesAcrysil Investor Presentation 31102018Sajid FlexwalaNo ratings yet

- PWC Vietnam Outlook enDocument10 pagesPWC Vietnam Outlook enPham Thi Phuong Anh (K16 HCM)No ratings yet

- PWC Vietnam Outlook enDocument10 pagesPWC Vietnam Outlook enQuynh VoNo ratings yet

- Vodafone Group PLC: DisclaimerDocument17 pagesVodafone Group PLC: DisclaimerTawfiq4444No ratings yet

- Sub: Investor Presentation On Financial Results For The Quarter and Nine Months Ended 31 December, 2021Document39 pagesSub: Investor Presentation On Financial Results For The Quarter and Nine Months Ended 31 December, 2021Dasari PrabodhNo ratings yet

- Chapter-06 Eng Eng-21Document16 pagesChapter-06 Eng Eng-21Riyad HossainNo ratings yet

- TCS Financial Results: Quarter III FY 2021-22Document25 pagesTCS Financial Results: Quarter III FY 2021-22Arindam MukhopadhyayNo ratings yet

- Union Budget 2022: #ConfidentindiaDocument31 pagesUnion Budget 2022: #ConfidentindiaRavi AgarwalNo ratings yet

- Investor Presentation Q1 FY21 July 2020Document55 pagesInvestor Presentation Q1 FY21 July 2020vvpvarunNo ratings yet

- DownloadDocument3 pagesDownloadVenkatesh VenkateshNo ratings yet

- BDO Unibank 2019-Annual-Report-Financial-Supplements PDFDocument228 pagesBDO Unibank 2019-Annual-Report-Financial-Supplements PDFCristine AquinoNo ratings yet

- Challenges On Debt Management in Developing CountriesDocument18 pagesChallenges On Debt Management in Developing CountriesAsian Development Bank - Event DocumentsNo ratings yet

- Cyient LTD.: Q1FY20: Weak Quarter, Lack VisibilityDocument7 pagesCyient LTD.: Q1FY20: Weak Quarter, Lack VisibilityADNo ratings yet

- MRSGI Books Net Loss of Php126Mil, Below Estimates: Metro Retail Stores Group, IncDocument7 pagesMRSGI Books Net Loss of Php126Mil, Below Estimates: Metro Retail Stores Group, IncJajahinaNo ratings yet

- Fin Analysis of SpicejetDocument9 pagesFin Analysis of SpicejetRadhika IyerNo ratings yet

- HCL Tech Q4 FY22 Investor ReleaseDocument25 pagesHCL Tech Q4 FY22 Investor ReleaseNddd NnbNo ratings yet

- 2019 Q2 2019.07.31 Vingroup Earnings Presentation 2Q2019Document44 pages2019 Q2 2019.07.31 Vingroup Earnings Presentation 2Q2019MNo ratings yet

- BP Case StudyDocument12 pagesBP Case Studypyush0786No ratings yet

- JK Cement: Valuations Factor in Positive Downgrade To HOLDDocument9 pagesJK Cement: Valuations Factor in Positive Downgrade To HOLDShubham BawkarNo ratings yet

- Arrow - Dry Bulk Outlook - Apr-20Document22 pagesArrow - Dry Bulk Outlook - Apr-20Sahil FarazNo ratings yet

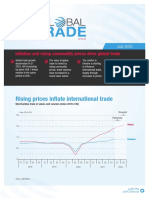

- GL Bal: Rising Prices Inflate International TradeDocument11 pagesGL Bal: Rising Prices Inflate International TradeBekele Guta GemeneNo ratings yet

- Golden Stocks PortfolioDocument6 pagesGolden Stocks PortfoliocompangelNo ratings yet

- Vietnam Market Trend Q3 - 2020Document22 pagesVietnam Market Trend Q3 - 2020cosmosmediavnNo ratings yet

- Vinati Organics LTD: Growth To Pick-Up..Document5 pagesVinati Organics LTD: Growth To Pick-Up..Bhaveek OstwalNo ratings yet

- Gabriel India Limited: AJINKYA YADAV - 19020348002 - MBA FINANCE (EXECUTIVE) 2019-22Document22 pagesGabriel India Limited: AJINKYA YADAV - 19020348002 - MBA FINANCE (EXECUTIVE) 2019-22Ajinkya YadavNo ratings yet

- Presentacion 2019 PDFDocument9 pagesPresentacion 2019 PDFWilsonNo ratings yet

- InvestorResentation Q4 FY18 19Document40 pagesInvestorResentation Q4 FY18 19Saksham SinhaNo ratings yet

- BVSC+-+Update+Report+DRC+10 2019Document12 pagesBVSC+-+Update+Report+DRC+10 2019acc1qhuyNo ratings yet

- Britannia - Q4FY19 - Result Update - 130520191 - 14-05-2019 - 16Document9 pagesBritannia - Q4FY19 - Result Update - 130520191 - 14-05-2019 - 16sps fetrNo ratings yet

- BigTech Analysis - Example AnswerDocument22 pagesBigTech Analysis - Example AnswerÚdita ShNo ratings yet

- Oa NH Deutsche Bank 2022 0Document51 pagesOa NH Deutsche Bank 2022 0justineNo ratings yet

- Hampered by Tightening PPKM: Mitra Adiperkasa TBK (MAPI IJ)Document6 pagesHampered by Tightening PPKM: Mitra Adiperkasa TBK (MAPI IJ)Putu Chantika Putri DhammayantiNo ratings yet

- TCP Research ReportDocument6 pagesTCP Research ReportAyush GoelNo ratings yet

- Icici Bank LTD: Operating Performance On TrackDocument6 pagesIcici Bank LTD: Operating Performance On TrackADNo ratings yet

- DownloadDocument22 pagesDownloadAshwani KesharwaniNo ratings yet

- Investor Presentation: Jeyamurugan Ramalingam JeyapandiyanDocument23 pagesInvestor Presentation: Jeyamurugan Ramalingam JeyapandiyanAbhilashNo ratings yet

- Pidilite Industries (PIDIND) : High Raw Material Prices Hit MarginDocument10 pagesPidilite Industries (PIDIND) : High Raw Material Prices Hit MarginSiddhant SinghNo ratings yet

- Economic Indicators for East Asia: Input–Output TablesFrom EverandEconomic Indicators for East Asia: Input–Output TablesNo ratings yet

- 20170525-Guarantee Schedule For 175 Mva Power Transformers-RevisedDocument44 pages20170525-Guarantee Schedule For 175 Mva Power Transformers-RevisedAhmed Said GhonimyNo ratings yet

- LAB 6 7-ElectroMechanical PneumaticDocument9 pagesLAB 6 7-ElectroMechanical PneumaticBien MedinaNo ratings yet

- ITS 2016 Boston - Tugconomy PaperDocument6 pagesITS 2016 Boston - Tugconomy PaperPietGebruikerNo ratings yet

- Gupta R. S., Principles of Structural Design Wood, Steel, and Concrete, 2nd Ed, 2014Document58 pagesGupta R. S., Principles of Structural Design Wood, Steel, and Concrete, 2nd Ed, 2014reyNo ratings yet

- Btech Syllabus For Gndec LudhianaDocument38 pagesBtech Syllabus For Gndec Ludhianaਅਰ ਜੋਤNo ratings yet

- Laporan Bulanan Data Center CyberDocument11 pagesLaporan Bulanan Data Center CyberDeden Andri Maulana SyamsudinNo ratings yet

- Architectural Design 9 Thesis Research Writing: 3 Proposal DraftDocument7 pagesArchitectural Design 9 Thesis Research Writing: 3 Proposal DraftVANESSA DELA TORRENo ratings yet

- Entertainment QuestionnaireDocument18 pagesEntertainment QuestionnairermtadtadNo ratings yet

- APSC Mains GS5 Syllabus Topic ListDocument11 pagesAPSC Mains GS5 Syllabus Topic ListAdhish Bipul BarmanNo ratings yet

- Data Communication Concepts: Dr. Shuchita Upadhyaya Bhasin Professor Department of Computer Science & ApplicationsDocument14 pagesData Communication Concepts: Dr. Shuchita Upadhyaya Bhasin Professor Department of Computer Science & ApplicationsRaj VermaNo ratings yet

- Life Below Water: Verlin Andre Africa Simon Marquis Lumbera Rhona Mae Panopio Ais1ADocument14 pagesLife Below Water: Verlin Andre Africa Simon Marquis Lumbera Rhona Mae Panopio Ais1ASimon Marquis LUMBERANo ratings yet

- Entrega de Productos Wings Mobile 14-09-2021Document18 pagesEntrega de Productos Wings Mobile 14-09-2021claudiaNo ratings yet

- Notes MT Module I - KTUDocument47 pagesNotes MT Module I - KTURagesh Dudu100% (1)

- AIDICO ECO-STONE Sustainable System Implementation For Natural Stone Production and Use PDFDocument81 pagesAIDICO ECO-STONE Sustainable System Implementation For Natural Stone Production and Use PDFDaniNo ratings yet

- Click Chemistry For Biotechnology BDocument433 pagesClick Chemistry For Biotechnology BAnonymous GIvZJ4v100% (1)

- Architecture and Technology Components For 5G Mobile and Wireless CommunicationDocument7 pagesArchitecture and Technology Components For 5G Mobile and Wireless CommunicationGaurav VishalNo ratings yet

- GR 190080Document9 pagesGR 190080Arvi MendezNo ratings yet

- Ses11 GSLC Chap11 Supply Chain ManagementDocument27 pagesSes11 GSLC Chap11 Supply Chain ManagementRonan WisnuNo ratings yet

- 16 Bit Carry Select Adder With Low Power and AreaDocument3 pages16 Bit Carry Select Adder With Low Power and AreaSam XingxnNo ratings yet

- Labuenavida Business Summary 2023Document24 pagesLabuenavida Business Summary 2023UzoNo ratings yet

- November 2023 Timetable Zone 2Document12 pagesNovember 2023 Timetable Zone 2Horror666No ratings yet

- Consumer ReportsDocument69 pagesConsumer ReportsRamakrishna RNo ratings yet

- FactoryTalk Historian SE - PI Web Services vs. PI Web APIDocument5 pagesFactoryTalk Historian SE - PI Web Services vs. PI Web APIDiegoFonsecaNo ratings yet

- S. No. Title Primary Subject Area Journal Code Impact FactorDocument6 pagesS. No. Title Primary Subject Area Journal Code Impact FactorRohitKumarSahuNo ratings yet

- NHA - Revised GEHP Application FormDocument2 pagesNHA - Revised GEHP Application FormMuhammad Hasher AnjalinNo ratings yet

- Article - Harper's - February 2011 - Adam Hochschild Reviews Timothy Snyder's Blood LandsDocument4 pagesArticle - Harper's - February 2011 - Adam Hochschild Reviews Timothy Snyder's Blood Landsbear clawNo ratings yet

Download as pdf or txt

You might also like

- How To Set Up A Suspension (Time) Histogram v2Document13 pagesHow To Set Up A Suspension (Time) Histogram v2Julian Morcillo100% (2)

- Kantar Worldpanel Division FMCG Monitor Full Year 2020 EN FinalDocument10 pagesKantar Worldpanel Division FMCG Monitor Full Year 2020 EN FinalvinhtamledangNo ratings yet

- Support For A Two-Dimensional Model of Conflict BehaviorDocument13 pagesSupport For A Two-Dimensional Model of Conflict BehaviorMariaIoanaTelecanNo ratings yet

- Pcem 06 Swot Analysis Kaha FinalDocument23 pagesPcem 06 Swot Analysis Kaha FinalziadNo ratings yet

- David Blueford Gaines - Racial Possibilities As Indicated by The Negroes of Arkansas (1898)Document198 pagesDavid Blueford Gaines - Racial Possibilities As Indicated by The Negroes of Arkansas (1898)chyoungNo ratings yet

- Sub: Raymond Limited - Investor Presentation: Rakesh Muljibh Ai DarjiDocument64 pagesSub: Raymond Limited - Investor Presentation: Rakesh Muljibh Ai DarjiSathwik PadamNo ratings yet

- Phiroze Jeejeebhoy Towers Dalal Street Mumbai - 400 001Document5 pagesPhiroze Jeejeebhoy Towers Dalal Street Mumbai - 400 001Namrata ShahNo ratings yet

- 91 Full Year Results Presentation May 2022Document41 pages91 Full Year Results Presentation May 2022floferNo ratings yet

- Overweight: Going Through Steep PathsDocument6 pagesOverweight: Going Through Steep PathsPutu Chantika Putri DhammayantiNo ratings yet

- YES Bank Presentation Q42018Document32 pagesYES Bank Presentation Q42018sanjeev7777No ratings yet

- Dilip Buildcon Q3FY18 - Result Update - Axis Direct - 20022018 - 20!02!2018 - 16Document6 pagesDilip Buildcon Q3FY18 - Result Update - Axis Direct - 20022018 - 20!02!2018 - 16MiteshNo ratings yet

- BritanniaDocument3 pagesBritanniaDhritiman DuttaNo ratings yet

- Realigning Estimate On Stronger Than Expected Mass Market: Bloomberry Resorts CorporationDocument8 pagesRealigning Estimate On Stronger Than Expected Mass Market: Bloomberry Resorts CorporationJajahinaNo ratings yet

- ITC - Deep Value Significant Opportunities To Unlock Value For ShareholdersDocument13 pagesITC - Deep Value Significant Opportunities To Unlock Value For ShareholdersYogeshNo ratings yet

- Nse: Itc PRICE: INR 203.10Document7 pagesNse: Itc PRICE: INR 203.10Shresth GuptaNo ratings yet

- Africa Day Presentation VDefDocument30 pagesAfrica Day Presentation VDefBernard BiboumNo ratings yet

- 91 Interim Results Presentation November 2021Document34 pages91 Interim Results Presentation November 2021floferNo ratings yet

- Nickel StudyDocument7 pagesNickel StudyILSEN N. DAETNo ratings yet

- FMCG Industry: $110 Billion 14% CAGR $110 Billion 14% CAGRDocument9 pagesFMCG Industry: $110 Billion 14% CAGR $110 Billion 14% CAGRShresth GuptaNo ratings yet

- Asian Paints: Volume Led Growth ContinuesDocument9 pagesAsian Paints: Volume Led Growth ContinuesanjugaduNo ratings yet

- SOK 2020 Annual ReportDocument158 pagesSOK 2020 Annual Reporttarikerkut44No ratings yet

- Group 1 - TBSL PDFDocument18 pagesGroup 1 - TBSL PDFAnkit BansalNo ratings yet

- Radico Khaitan Ltd. Earnings Presentation: Q4 and Full Year FY2020Document23 pagesRadico Khaitan Ltd. Earnings Presentation: Q4 and Full Year FY2020UmangNo ratings yet

- Ambev Presentation Dec.19Document22 pagesAmbev Presentation Dec.19arthurNo ratings yet

- Company Overview: Source: Investor Presentation Q4 2019Document10 pagesCompany Overview: Source: Investor Presentation Q4 2019Radhika IyerNo ratings yet

- Avenue Supermarts Sell: Result UpdateDocument6 pagesAvenue Supermarts Sell: Result UpdateAshokNo ratings yet

- Acrysil Investor Presentation 31102018Document34 pagesAcrysil Investor Presentation 31102018Sajid FlexwalaNo ratings yet

- PWC Vietnam Outlook enDocument10 pagesPWC Vietnam Outlook enPham Thi Phuong Anh (K16 HCM)No ratings yet

- PWC Vietnam Outlook enDocument10 pagesPWC Vietnam Outlook enQuynh VoNo ratings yet

- Vodafone Group PLC: DisclaimerDocument17 pagesVodafone Group PLC: DisclaimerTawfiq4444No ratings yet

- Sub: Investor Presentation On Financial Results For The Quarter and Nine Months Ended 31 December, 2021Document39 pagesSub: Investor Presentation On Financial Results For The Quarter and Nine Months Ended 31 December, 2021Dasari PrabodhNo ratings yet

- Chapter-06 Eng Eng-21Document16 pagesChapter-06 Eng Eng-21Riyad HossainNo ratings yet

- TCS Financial Results: Quarter III FY 2021-22Document25 pagesTCS Financial Results: Quarter III FY 2021-22Arindam MukhopadhyayNo ratings yet

- Union Budget 2022: #ConfidentindiaDocument31 pagesUnion Budget 2022: #ConfidentindiaRavi AgarwalNo ratings yet

- Investor Presentation Q1 FY21 July 2020Document55 pagesInvestor Presentation Q1 FY21 July 2020vvpvarunNo ratings yet

- DownloadDocument3 pagesDownloadVenkatesh VenkateshNo ratings yet

- BDO Unibank 2019-Annual-Report-Financial-Supplements PDFDocument228 pagesBDO Unibank 2019-Annual-Report-Financial-Supplements PDFCristine AquinoNo ratings yet

- Challenges On Debt Management in Developing CountriesDocument18 pagesChallenges On Debt Management in Developing CountriesAsian Development Bank - Event DocumentsNo ratings yet

- Cyient LTD.: Q1FY20: Weak Quarter, Lack VisibilityDocument7 pagesCyient LTD.: Q1FY20: Weak Quarter, Lack VisibilityADNo ratings yet

- MRSGI Books Net Loss of Php126Mil, Below Estimates: Metro Retail Stores Group, IncDocument7 pagesMRSGI Books Net Loss of Php126Mil, Below Estimates: Metro Retail Stores Group, IncJajahinaNo ratings yet

- Fin Analysis of SpicejetDocument9 pagesFin Analysis of SpicejetRadhika IyerNo ratings yet

- HCL Tech Q4 FY22 Investor ReleaseDocument25 pagesHCL Tech Q4 FY22 Investor ReleaseNddd NnbNo ratings yet

- 2019 Q2 2019.07.31 Vingroup Earnings Presentation 2Q2019Document44 pages2019 Q2 2019.07.31 Vingroup Earnings Presentation 2Q2019MNo ratings yet

- BP Case StudyDocument12 pagesBP Case Studypyush0786No ratings yet

- JK Cement: Valuations Factor in Positive Downgrade To HOLDDocument9 pagesJK Cement: Valuations Factor in Positive Downgrade To HOLDShubham BawkarNo ratings yet

- Arrow - Dry Bulk Outlook - Apr-20Document22 pagesArrow - Dry Bulk Outlook - Apr-20Sahil FarazNo ratings yet

- GL Bal: Rising Prices Inflate International TradeDocument11 pagesGL Bal: Rising Prices Inflate International TradeBekele Guta GemeneNo ratings yet

- Golden Stocks PortfolioDocument6 pagesGolden Stocks PortfoliocompangelNo ratings yet

- Vietnam Market Trend Q3 - 2020Document22 pagesVietnam Market Trend Q3 - 2020cosmosmediavnNo ratings yet

- Vinati Organics LTD: Growth To Pick-Up..Document5 pagesVinati Organics LTD: Growth To Pick-Up..Bhaveek OstwalNo ratings yet

- Gabriel India Limited: AJINKYA YADAV - 19020348002 - MBA FINANCE (EXECUTIVE) 2019-22Document22 pagesGabriel India Limited: AJINKYA YADAV - 19020348002 - MBA FINANCE (EXECUTIVE) 2019-22Ajinkya YadavNo ratings yet

- Presentacion 2019 PDFDocument9 pagesPresentacion 2019 PDFWilsonNo ratings yet

- InvestorResentation Q4 FY18 19Document40 pagesInvestorResentation Q4 FY18 19Saksham SinhaNo ratings yet

- BVSC+-+Update+Report+DRC+10 2019Document12 pagesBVSC+-+Update+Report+DRC+10 2019acc1qhuyNo ratings yet

- Britannia - Q4FY19 - Result Update - 130520191 - 14-05-2019 - 16Document9 pagesBritannia - Q4FY19 - Result Update - 130520191 - 14-05-2019 - 16sps fetrNo ratings yet

- BigTech Analysis - Example AnswerDocument22 pagesBigTech Analysis - Example AnswerÚdita ShNo ratings yet

- Oa NH Deutsche Bank 2022 0Document51 pagesOa NH Deutsche Bank 2022 0justineNo ratings yet

- Hampered by Tightening PPKM: Mitra Adiperkasa TBK (MAPI IJ)Document6 pagesHampered by Tightening PPKM: Mitra Adiperkasa TBK (MAPI IJ)Putu Chantika Putri DhammayantiNo ratings yet

- TCP Research ReportDocument6 pagesTCP Research ReportAyush GoelNo ratings yet

- Icici Bank LTD: Operating Performance On TrackDocument6 pagesIcici Bank LTD: Operating Performance On TrackADNo ratings yet

- DownloadDocument22 pagesDownloadAshwani KesharwaniNo ratings yet

- Investor Presentation: Jeyamurugan Ramalingam JeyapandiyanDocument23 pagesInvestor Presentation: Jeyamurugan Ramalingam JeyapandiyanAbhilashNo ratings yet

- Pidilite Industries (PIDIND) : High Raw Material Prices Hit MarginDocument10 pagesPidilite Industries (PIDIND) : High Raw Material Prices Hit MarginSiddhant SinghNo ratings yet

- Economic Indicators for East Asia: Input–Output TablesFrom EverandEconomic Indicators for East Asia: Input–Output TablesNo ratings yet

- 20170525-Guarantee Schedule For 175 Mva Power Transformers-RevisedDocument44 pages20170525-Guarantee Schedule For 175 Mva Power Transformers-RevisedAhmed Said GhonimyNo ratings yet

- LAB 6 7-ElectroMechanical PneumaticDocument9 pagesLAB 6 7-ElectroMechanical PneumaticBien MedinaNo ratings yet

- ITS 2016 Boston - Tugconomy PaperDocument6 pagesITS 2016 Boston - Tugconomy PaperPietGebruikerNo ratings yet

- Gupta R. S., Principles of Structural Design Wood, Steel, and Concrete, 2nd Ed, 2014Document58 pagesGupta R. S., Principles of Structural Design Wood, Steel, and Concrete, 2nd Ed, 2014reyNo ratings yet

- Btech Syllabus For Gndec LudhianaDocument38 pagesBtech Syllabus For Gndec Ludhianaਅਰ ਜੋਤNo ratings yet

- Laporan Bulanan Data Center CyberDocument11 pagesLaporan Bulanan Data Center CyberDeden Andri Maulana SyamsudinNo ratings yet

- Architectural Design 9 Thesis Research Writing: 3 Proposal DraftDocument7 pagesArchitectural Design 9 Thesis Research Writing: 3 Proposal DraftVANESSA DELA TORRENo ratings yet

- Entertainment QuestionnaireDocument18 pagesEntertainment QuestionnairermtadtadNo ratings yet

- APSC Mains GS5 Syllabus Topic ListDocument11 pagesAPSC Mains GS5 Syllabus Topic ListAdhish Bipul BarmanNo ratings yet

- Data Communication Concepts: Dr. Shuchita Upadhyaya Bhasin Professor Department of Computer Science & ApplicationsDocument14 pagesData Communication Concepts: Dr. Shuchita Upadhyaya Bhasin Professor Department of Computer Science & ApplicationsRaj VermaNo ratings yet

- Life Below Water: Verlin Andre Africa Simon Marquis Lumbera Rhona Mae Panopio Ais1ADocument14 pagesLife Below Water: Verlin Andre Africa Simon Marquis Lumbera Rhona Mae Panopio Ais1ASimon Marquis LUMBERANo ratings yet

- Entrega de Productos Wings Mobile 14-09-2021Document18 pagesEntrega de Productos Wings Mobile 14-09-2021claudiaNo ratings yet

- Notes MT Module I - KTUDocument47 pagesNotes MT Module I - KTURagesh Dudu100% (1)

- AIDICO ECO-STONE Sustainable System Implementation For Natural Stone Production and Use PDFDocument81 pagesAIDICO ECO-STONE Sustainable System Implementation For Natural Stone Production and Use PDFDaniNo ratings yet

- Click Chemistry For Biotechnology BDocument433 pagesClick Chemistry For Biotechnology BAnonymous GIvZJ4v100% (1)

- Architecture and Technology Components For 5G Mobile and Wireless CommunicationDocument7 pagesArchitecture and Technology Components For 5G Mobile and Wireless CommunicationGaurav VishalNo ratings yet

- GR 190080Document9 pagesGR 190080Arvi MendezNo ratings yet

- Ses11 GSLC Chap11 Supply Chain ManagementDocument27 pagesSes11 GSLC Chap11 Supply Chain ManagementRonan WisnuNo ratings yet

- 16 Bit Carry Select Adder With Low Power and AreaDocument3 pages16 Bit Carry Select Adder With Low Power and AreaSam XingxnNo ratings yet

- Labuenavida Business Summary 2023Document24 pagesLabuenavida Business Summary 2023UzoNo ratings yet

- November 2023 Timetable Zone 2Document12 pagesNovember 2023 Timetable Zone 2Horror666No ratings yet

- Consumer ReportsDocument69 pagesConsumer ReportsRamakrishna RNo ratings yet

- FactoryTalk Historian SE - PI Web Services vs. PI Web APIDocument5 pagesFactoryTalk Historian SE - PI Web Services vs. PI Web APIDiegoFonsecaNo ratings yet

- S. No. Title Primary Subject Area Journal Code Impact FactorDocument6 pagesS. No. Title Primary Subject Area Journal Code Impact FactorRohitKumarSahuNo ratings yet

- NHA - Revised GEHP Application FormDocument2 pagesNHA - Revised GEHP Application FormMuhammad Hasher AnjalinNo ratings yet

- Article - Harper's - February 2011 - Adam Hochschild Reviews Timothy Snyder's Blood LandsDocument4 pagesArticle - Harper's - February 2011 - Adam Hochschild Reviews Timothy Snyder's Blood Landsbear clawNo ratings yet