Download as docx, pdf, or txt

You might also like

- ACC 406 Module Guide 2018 - SatandeDocument240 pagesACC 406 Module Guide 2018 - SatandeTATENDA GANDIWA100% (1)

- EY Share-Based Payment GuideDocument404 pagesEY Share-Based Payment GuidemichellermailNo ratings yet

- A Comparison of IFRS, US GAAP and Belgian GAAPDocument100 pagesA Comparison of IFRS, US GAAP and Belgian GAAPVoicu Dragomir67% (3)

- Financial Statement Preparation and AnalysisDocument40 pagesFinancial Statement Preparation and AnalysisMD SAIFUL ISLAMNo ratings yet

- Ipsas 1 PDFDocument59 pagesIpsas 1 PDFWinnie Ann Daquil Lomosad100% (1)

- PWC Vietnam Ifrs Vas PDFDocument99 pagesPWC Vietnam Ifrs Vas PDFminhNo ratings yet

- Interim Financial Statements (June 2023) FinalDocument74 pagesInterim Financial Statements (June 2023) FinalKatarina GojkovicNo ratings yet

- Government Financial Reporting: Ifac Public Sector CommitteeDocument286 pagesGovernment Financial Reporting: Ifac Public Sector CommitteeYalew Wondmnew100% (1)

- Ey Ifrs Us Gaap Rap 2014 EngDocument52 pagesEy Ifrs Us Gaap Rap 2014 EngNasir AliyevNo ratings yet

- GRANT THORNTON - 2016.09 - Comparison Between U.S. GAAP and IFRSDocument228 pagesGRANT THORNTON - 2016.09 - Comparison Between U.S. GAAP and IFRSricardo.j.cruzNo ratings yet

- IPSASB IPSAS 33 First Time Adoption of Accrual Basis IPSASsDocument114 pagesIPSASB IPSAS 33 First Time Adoption of Accrual Basis IPSASskajaleNo ratings yet

- Interim Financial Statements: IAS 34 Explained (30 June 2017)Document68 pagesInterim Financial Statements: IAS 34 Explained (30 June 2017)Abu AzlanNo ratings yet

- ABM312 Financial Accounting 2015 ModuleDocument77 pagesABM312 Financial Accounting 2015 ModuleDAVY SIMONGANo ratings yet

- Joint Ventures: Financial Reporting DevelopmentsDocument54 pagesJoint Ventures: Financial Reporting DevelopmentsRaphael MarquezNo ratings yet

- Cooperative BookkeepingDocument41 pagesCooperative Bookkeepingjaydeeado50% (4)

- Ap Faisal 001Document19 pagesAp Faisal 001Jashim UddinNo ratings yet

- Illustrative Financial StatementsDocument42 pagesIllustrative Financial StatementsMulinya MulinyaNo ratings yet

- About Financial Account V2 PDFDocument465 pagesAbout Financial Account V2 PDFStar69 Stay schemin2100% (1)

- How To Read A Financial Report by Merrill LynchDocument0 pagesHow To Read A Financial Report by Merrill Lynchjunaid_256No ratings yet

- FIN 301 hoàn chỉnh.vi.enDocument29 pagesFIN 301 hoàn chỉnh.vi.enNguyễn Trần Trung ThịnhNo ratings yet

- Ipsas 2 Cash Flow StatementsDocument22 pagesIpsas 2 Cash Flow StatementsJAMAN SOUTH MUNICIPAL HEALTH DIRECTORATENo ratings yet

- ED Revised FAS 1 F2 2020 31 December 2020 For Issuance UpdatedDocument51 pagesED Revised FAS 1 F2 2020 31 December 2020 For Issuance Updatedhebaalhomidi2025No ratings yet

- Fores PDFDocument167 pagesFores PDFAriunbolor BayraaNo ratings yet

- Ipsas 1 Presentation of FDocument57 pagesIpsas 1 Presentation of FGi VieiraNo ratings yet

- Manage Finance - EditedDocument30 pagesManage Finance - EditedPupunBiswalNo ratings yet

- Dai23 Yuho EDocument275 pagesDai23 Yuho ERayhan AlfansaNo ratings yet

- Eyu ProjectDocument38 pagesEyu ProjectTEWODROS ASFAWNo ratings yet

- Financial Management - Rev - 04 19 19Document35 pagesFinancial Management - Rev - 04 19 19Zebib DestaNo ratings yet

- Annual Report 2014 PDFDocument294 pagesAnnual Report 2014 PDFJeisson ReyesNo ratings yet

- MousamDas Interim-Report IFGLDocument67 pagesMousamDas Interim-Report IFGLMousam89No ratings yet

- 04-Sap Mda2023 AngDocument102 pages04-Sap Mda2023 AngAlexandra De BianchiNo ratings yet

- IFRS SummaryDocument97 pagesIFRS SummaryMOHIT AGRAWALNo ratings yet

- Risk Based Internal Auditing in BanksDocument55 pagesRisk Based Internal Auditing in BanksAKSHAT RAJESH SHAH100% (1)

- Understanding Business CyclesDocument29 pagesUnderstanding Business CyclesAnshumanNo ratings yet

- Bank Accounting Traning Material 2017Document138 pagesBank Accounting Traning Material 2017mintefikreNo ratings yet

- Uw eMBA Wikibook-Managerial-Accounting PDFDocument103 pagesUw eMBA Wikibook-Managerial-Accounting PDFEswari Gk100% (1)

- ABS Guidelines On AML and Countering The Financing of TerrorismDocument72 pagesABS Guidelines On AML and Countering The Financing of TerrorismOlivia XNo ratings yet

- Financial Analysis Final Report General TyresDocument36 pagesFinancial Analysis Final Report General TyresBurhan AhmadNo ratings yet

- Financial Statement Analiysis of Bangladesh Krishibank LTDDocument40 pagesFinancial Statement Analiysis of Bangladesh Krishibank LTDEdu WriterNo ratings yet

- EY - A Comprehensive Guide - Share-Based PaymentDocument417 pagesEY - A Comprehensive Guide - Share-Based PaymentAmiNo ratings yet

- Short Guide To IFRSDocument35 pagesShort Guide To IFRSAdekanye Adetayo100% (1)

- TextbookDocument465 pagesTextbookVishnu PillayNo ratings yet

- Modern Business Administration-2020Document252 pagesModern Business Administration-2020OmarNo ratings yet

- Issai 200Document41 pagesIssai 200ateam4984No ratings yet

- Ey frd02856 161us 05 27 2020 PDFDocument538 pagesEy frd02856 161us 05 27 2020 PDFSarwar GolamNo ratings yet

- Financial Trend Monitoring System: Prepared by The Finance DepartmentDocument52 pagesFinancial Trend Monitoring System: Prepared by The Finance DepartmentkokiNo ratings yet

- MDP231Document36 pagesMDP231May FadlNo ratings yet

- Iaasb Isa 810 RevisedDocument31 pagesIaasb Isa 810 RevisedGlenn TaduranNo ratings yet

- PISA 2021 Financial Literacy FrameworkDocument50 pagesPISA 2021 Financial Literacy FrameworkKiko HuitNo ratings yet

- Basic Accounting and Financial ManagementDocument163 pagesBasic Accounting and Financial ManagementBernard Owusu100% (1)

- AFARDocument107 pagesAFARmisonim.eNo ratings yet

- Ifrs 10Document160 pagesIfrs 10fauziahezzyNo ratings yet

- US GAAP X IFRSDocument220 pagesUS GAAP X IFRSTharsis BaldinottiNo ratings yet

- Ipsas 6 Consolidated and 3Document36 pagesIpsas 6 Consolidated and 3EmmaNo ratings yet

- ED FAS On Presentation and Disclsoure in The FS of Takaful Institutions FinalDocument30 pagesED FAS On Presentation and Disclsoure in The FS of Takaful Institutions FinalIstiaqueNo ratings yet

- Grace Corporati On: Financial Statements For The Year Ended December 31, 2017Document3 pagesGrace Corporati On: Financial Statements For The Year Ended December 31, 2017Nesuui MontejoNo ratings yet

- Financial Accounting and Management CourDocument256 pagesFinancial Accounting and Management CourAdanechNo ratings yet

- f-504 FinalDocument83 pagesf-504 FinalSamiul21No ratings yet

- Finance Dossier 2023-24Document141 pagesFinance Dossier 2023-24kanikabhateja7No ratings yet

- The Boston Institute of Finance Mutual Fund Advisor Course: Series 6 and Series 63 Test PrepFrom EverandThe Boston Institute of Finance Mutual Fund Advisor Course: Series 6 and Series 63 Test PrepNo ratings yet

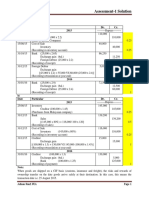

- CAF-07 Assessment-1 Solution: Answer-1 A) Date Particular Dr. Cr. 2015Document5 pagesCAF-07 Assessment-1 Solution: Answer-1 A) Date Particular Dr. Cr. 2015Ali OptimisticNo ratings yet

- Chapter 4Document9 pagesChapter 4limenih100% (1)

- AN To Debt Policy and ValueDocument7 pagesAN To Debt Policy and ValueMochamad Arief RahmanNo ratings yet

- BPM-SMA 13-Best Practice Model Example 2Document27 pagesBPM-SMA 13-Best Practice Model Example 2Ahmad DeebNo ratings yet

- Coca Cola - With Notes On Discount Factor CalculationDocument20 pagesCoca Cola - With Notes On Discount Factor CalculationJared HerberNo ratings yet

- Corporate Accounting: AssignmentDocument7 pagesCorporate Accounting: AssignmentRajni KumariNo ratings yet

- Consolidated Balance SheetDocument2 pagesConsolidated Balance SheetSEHWAG MATHAVANNo ratings yet

- MCQ in Engineering EconomicsDocument318 pagesMCQ in Engineering EconomicsKen Joshua ManaloNo ratings yet

- A Project Report OnDocument21 pagesA Project Report Onsuresh kumar sainiNo ratings yet

- Managerial Accounting Vs Financial AccouDocument11 pagesManagerial Accounting Vs Financial AccouJermaine Joselle FranciscoNo ratings yet

- Accounting Standard 28 CA Prajakta SangoramDocument43 pagesAccounting Standard 28 CA Prajakta SangoramASHIMA GUPTANo ratings yet

- Exercise 22Document8 pagesExercise 22Elisa Dwi LestariNo ratings yet

- p1b2 Key To CorrectionDocument14 pagesp1b2 Key To CorrectionReynaldo Alarde Goce Jr.No ratings yet

- PAS 2 InventoriesDocument3 pagesPAS 2 InventoriesLary Lou Ventura100% (4)

- BonusDocument5 pagesBonusbustillos_edwinjrNo ratings yet

- Corporate Liquidation & Reorganization: Problem 1: True or FalseDocument20 pagesCorporate Liquidation & Reorganization: Problem 1: True or FalseRicalyn Bugarin0% (2)

- Introduction To Accounting Practice Exercises: Exercise 1: The Accounting Equation Problem 1.1Document10 pagesIntroduction To Accounting Practice Exercises: Exercise 1: The Accounting Equation Problem 1.1Arbie Joy Olofernes SibilNo ratings yet

- Responsibility AcctngDocument5 pagesResponsibility AcctngKatherine EderosasNo ratings yet

- Term Paper On Business Analysis On Agrani BankDocument11 pagesTerm Paper On Business Analysis On Agrani BankMd. Atiqul Hoque NiloyNo ratings yet

- SMEsDocument3 pagesSMEsLayJohn LacadenNo ratings yet

- Foreign OperationsDocument2 pagesForeign OperationsrathaNo ratings yet

- Jamb Principles-Of-Accounts Past Question 1994 - 2004Document38 pagesJamb Principles-Of-Accounts Past Question 1994 - 2004Chukwudinma IkechukwuNo ratings yet

- Chapter 16Document53 pagesChapter 16V ChandriaNo ratings yet

- Mercury Athletic Footwear - Valuing The Opportunity: FINS 3625 - Case Study Written ComponentDocument9 pagesMercury Athletic Footwear - Valuing The Opportunity: FINS 3625 - Case Study Written ComponentBharat KoiralaNo ratings yet

- NobleCorporation 10Q 20101109Document118 pagesNobleCorporation 10Q 20101109msim10No ratings yet

- Investment Property ProblemsDocument3 pagesInvestment Property ProblemsAbigail TalusanNo ratings yet

- Midterm Exam Analysis of Financial StatementsDocument4 pagesMidterm Exam Analysis of Financial StatementsAlyssa TordesillasNo ratings yet

- Pc102 w05 Document Applicationactivity BreakevenDocument5 pagesPc102 w05 Document Applicationactivity Breakevenmanamadu11No ratings yet

- Bad DebtDocument4 pagesBad DebtTran Minh KhoiNo ratings yet

- 5 6255862442081910859Document29 pages5 6255862442081910859Christine PedronanNo ratings yet