Download as pdf

You might also like

- JDE Document Type DescriptionDocument7 pagesJDE Document Type DescriptionKelvin Tai Wei LimNo ratings yet

- Final Report Industrial Training For Accounting StudentDocument34 pagesFinal Report Industrial Training For Accounting StudentLau King Lieng65% (20)

- Accounting Problem Book 2011Document103 pagesAccounting Problem Book 2011Sveta Chernica100% (1)

- Chap 8Document63 pagesChap 8Jose Martin Castillo PatiñoNo ratings yet

- Accountancy For Dummies PDFDocument6 pagesAccountancy For Dummies PDFsritesh00% (1)

- Chap008 A SOLDocument13 pagesChap008 A SOLKaif Mohammad HussainNo ratings yet

- Combinations: Advocates & Solicitors Delhi - Gurgaon - Mumbai - Bangalore - HyderabadDocument23 pagesCombinations: Advocates & Solicitors Delhi - Gurgaon - Mumbai - Bangalore - HyderabadMishika PanditaNo ratings yet

- Taxguru - In-Compliances Based On Threshold Limits Under The Companies Act 2013Document16 pagesTaxguru - In-Compliances Based On Threshold Limits Under The Companies Act 2013starNo ratings yet

- Regulatory Framework of M&ADocument5 pagesRegulatory Framework of M&ARaghuramNo ratings yet

- Cross Broder MergersDocument5 pagesCross Broder MergersAnanya UpadhyeNo ratings yet

- Introduction and Roadmap of Ind As For 1st 2nd August Pune Branch Programme CA. Zaware SirDocument51 pagesIntroduction and Roadmap of Ind As For 1st 2nd August Pune Branch Programme CA. Zaware SirAnonymous ffGTtPfhdNo ratings yet

- Session 1 and 2 Competition Law Merger RegimeDocument6 pagesSession 1 and 2 Competition Law Merger RegimeDHRUV CHOPRANo ratings yet

- Carve-Outs From IFRS & Key Clarifications Brought in by ITFGDocument20 pagesCarve-Outs From IFRS & Key Clarifications Brought in by ITFGSrNo ratings yet

- Case Study DocumentDocument30 pagesCase Study Documentbbtqwrws78No ratings yet

- 08 MF NBFC - UnlockedDocument23 pages08 MF NBFC - UnlockedBittu SharmaNo ratings yet

- Key Terms of The Merger Control Regime 1639647849Document12 pagesKey Terms of The Merger Control Regime 1639647849ishaankc1510No ratings yet

- COMBINATIONSDocument25 pagesCOMBINATIONSjlu04870No ratings yet

- Trends in Mergers and Acquisitions in Past Five Years in Indian Corporate SectorDocument21 pagesTrends in Mergers and Acquisitions in Past Five Years in Indian Corporate SectorsecondtononeNo ratings yet

- Companies Act 2017 Significant Amendments, May 2020: Smart Decisions. Lasting ValueDocument24 pagesCompanies Act 2017 Significant Amendments, May 2020: Smart Decisions. Lasting ValueMuhammad IrshadNo ratings yet

- Mergers and Acquisitions in The Indian Pharmaceutical Sector: Trends, Sample Study, and Financial Analysis of Pre and Post MergeDocument14 pagesMergers and Acquisitions in The Indian Pharmaceutical Sector: Trends, Sample Study, and Financial Analysis of Pre and Post MergeDrx Mehazabeen KachchawalaNo ratings yet

- EY Step Up To Ind AsDocument35 pagesEY Step Up To Ind AsRakeshkargwalNo ratings yet

- Trigger 5 - Big Ranch ConsolidationDocument26 pagesTrigger 5 - Big Ranch ConsolidationALBERTNo ratings yet

- Legal and Regulatory Frameworks For M&A in India: Domestic Mergers and AcquisitionsDocument5 pagesLegal and Regulatory Frameworks For M&A in India: Domestic Mergers and AcquisitionsShivam TomarNo ratings yet

- Ifrs 22 Aug 09 - VC - 4Document32 pagesIfrs 22 Aug 09 - VC - 4Darshan ToreNo ratings yet

- KPMG Flash News Draft Guidelines For Core Investment CompaniesDocument5 pagesKPMG Flash News Draft Guidelines For Core Investment CompaniesmurthyeNo ratings yet

- Recent Developments On Participatory Notes: IndiaDocument3 pagesRecent Developments On Participatory Notes: IndiapulkitaquarianNo ratings yet

- CCI, 'Provisions Relating To Combinations', Accessed 15 MAY 2020. IbidDocument7 pagesCCI, 'Provisions Relating To Combinations', Accessed 15 MAY 2020. IbidAyushNo ratings yet

- Role of Sebi - Cross Border Merger, Takeover CodeDocument7 pagesRole of Sebi - Cross Border Merger, Takeover Codeshivangidubey9415No ratings yet

- Provisions Under Mergers and Acquisitions Laws in IndiaDocument2 pagesProvisions Under Mergers and Acquisitions Laws in IndiabhavanshujNo ratings yet

- Convergence With International Financial Reporting Standards ('IFRS') - Impact On Fundamental Accounting Practices and Regulatory Framework in IndiaDocument4 pagesConvergence With International Financial Reporting Standards ('IFRS') - Impact On Fundamental Accounting Practices and Regulatory Framework in IndiaVinodh RathnamNo ratings yet

- Indian Accounting Standards: 2 Marks Question and AnswersDocument5 pagesIndian Accounting Standards: 2 Marks Question and Answersharsha100% (2)

- Indian Accounting Standards (Ind AS) : Basic ConceptsDocument18 pagesIndian Accounting Standards (Ind AS) : Basic ConceptsSivasankariNo ratings yet

- ACMA Unit 2Document47 pagesACMA Unit 2Subhodeep Roy ChowdhuryNo ratings yet

- Summary of Changes of New IFRS As of 123117Document6 pagesSummary of Changes of New IFRS As of 123117Jedy Ann PamorNo ratings yet

- FCCBDocument17 pagesFCCBcoffytoffyNo ratings yet

- Ifrs vs. Indian GaapDocument4 pagesIfrs vs. Indian GaapPankaj100% (1)

- Vodafone Tax Saga: Group 4Document17 pagesVodafone Tax Saga: Group 4Saharsh SaraogiNo ratings yet

- Session-2 - Consolidated Financial StatementDocument61 pagesSession-2 - Consolidated Financial StatementamanNo ratings yet

- Course Code: COM-405 Course Title: Credit Hours: 3 (3-0) : Introduction To Business FinanceDocument15 pagesCourse Code: COM-405 Course Title: Credit Hours: 3 (3-0) : Introduction To Business FinanceSajjad AhmadNo ratings yet

- Competition ActDocument43 pagesCompetition ActDurgesh 136No ratings yet

- Corporate Funding and Listing Short NotesDocument141 pagesCorporate Funding and Listing Short NotesVineela Srinidhi DantuNo ratings yet

- IFRS 3 Identifying A Business CombinationDocument8 pagesIFRS 3 Identifying A Business CombinationNicole CorderoNo ratings yet

- Business Accounting Assignment: Submitted By: Akash Yadav Course: Bms 1 Year ROLL No.: 6538Document9 pagesBusiness Accounting Assignment: Submitted By: Akash Yadav Course: Bms 1 Year ROLL No.: 6538akash yadavNo ratings yet

- Missive Volume IV - July 2011: Transaction AdvisorsDocument11 pagesMissive Volume IV - July 2011: Transaction AdvisorsAkhil BansalNo ratings yet

- Mergers & Acquisitions: in 60 Jurisdictions WorldwideDocument8 pagesMergers & Acquisitions: in 60 Jurisdictions WorldwideVivveck NayuduNo ratings yet

- Amended Schedule IIIDocument23 pagesAmended Schedule IIIpadiNo ratings yet

- Audit of Non Banking Financial Companies: HapterDocument6 pagesAudit of Non Banking Financial Companies: HapterAditya Jayseelan KNo ratings yet

- Guide On Taxation of Equity and F&O Segment IncomeDocument11 pagesGuide On Taxation of Equity and F&O Segment IncomenikhilkhemkaNo ratings yet

- M&a NotesDocument23 pagesM&a NotesAribba SiddiqueNo ratings yet

- Chapter 2. Mergers and Amalgamation, Corporate Demerger and Reverse MergerDocument32 pagesChapter 2. Mergers and Amalgamation, Corporate Demerger and Reverse MergerAbhishek SinghNo ratings yet

- CA Final Course Paper 2 Strategic Financial Management Chapter 13 CA. Biharilal DeoraDocument79 pagesCA Final Course Paper 2 Strategic Financial Management Chapter 13 CA. Biharilal DeoraPiyush KulkarniNo ratings yet

- Economy CADocument149 pagesEconomy CAnaimishrajverdhanNo ratings yet

- 8 IFRS 3 Business CombinationDocument21 pages8 IFRS 3 Business Combinationmae acuestaNo ratings yet

- Legal Aspects of M&ADocument48 pagesLegal Aspects of M&AkarunakaranNo ratings yet

- AA PPT 3rd Criteria 215Document11 pagesAA PPT 3rd Criteria 215Vignesh IyerNo ratings yet

- Redemption of Debenture NotesDocument18 pagesRedemption of Debenture Notesfriendsforever3405No ratings yet

- Reliance SIP Insure Application FormDocument24 pagesReliance SIP Insure Application FormDrashti Investments100% (6)

- Cross Border Mergers - Rbi Seminar dt22062019 - RajendraDocument12 pagesCross Border Mergers - Rbi Seminar dt22062019 - RajendraRishika GautamNo ratings yet

- Cross-Border Mergers and Acquisition and Related LawsDocument5 pagesCross-Border Mergers and Acquisition and Related Lawsdevendra bankarNo ratings yet

- Corporate RestructuringDocument3 pagesCorporate Restructuringcerab67850No ratings yet

- Startup Series 7 - Exchange Control Provisions For StartupsDocument12 pagesStartup Series 7 - Exchange Control Provisions For StartupsRavi PatelNo ratings yet

- Qatar Companies Commercial Law Update: Know The Rules, Know Your Way AheadDocument22 pagesQatar Companies Commercial Law Update: Know The Rules, Know Your Way AheadmuzammilshaikhNo ratings yet

- Ind AS at A GlanceDocument100 pagesInd AS at A GlanceSanjayNo ratings yet

- MSME IBC2 FootDocument26 pagesMSME IBC2 FootPriyadarshan NairNo ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- IAS 35 Discontinuing Operations: International Accounting StandardsDocument19 pagesIAS 35 Discontinuing Operations: International Accounting Standardsrio1603No ratings yet

- Auditor Appointment Letter FormatDocument2 pagesAuditor Appointment Letter Formateva100% (3)

- CH 5 QuizDocument11 pagesCH 5 QuizCha Chi BossNo ratings yet

- Rules of Debits and CreditsDocument2 pagesRules of Debits and CreditsRadhika PatkeNo ratings yet

- SAP Application AreasDocument100 pagesSAP Application AreasLodewijk BorsboomNo ratings yet

- UOL 2017 EbrcohureDocument20 pagesUOL 2017 EbrcohureZhess BugNo ratings yet

- AC3091 - Vle Financial ReportingDocument295 pagesAC3091 - Vle Financial Reportingletuan2212100% (3)

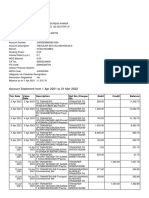

- Account Statement From 1 Apr 2021 To 31 Mar 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument12 pagesAccount Statement From 1 Apr 2021 To 31 Mar 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balancesanket enterprisesNo ratings yet

- The Basis For Business Decisions: Financial & Managerial AccountingDocument75 pagesThe Basis For Business Decisions: Financial & Managerial AccountingAdil AliNo ratings yet

- Financial Accounting and Reporting - QUIZ 7Document4 pagesFinancial Accounting and Reporting - QUIZ 7JINGLE FULGENCIONo ratings yet

- Introduction To Financial Statements: Wirecard ScandalDocument22 pagesIntroduction To Financial Statements: Wirecard ScandalNilesh Kumar GuptaNo ratings yet

- Discount Berlaku Bagi Setiap Menit Late Submission: Problem 1Document6 pagesDiscount Berlaku Bagi Setiap Menit Late Submission: Problem 1sherinaNo ratings yet

- Unity University College School of Distance and Continuing Education Worksheet For Auditing (Acct 252) Diploma ProgrammeDocument3 pagesUnity University College School of Distance and Continuing Education Worksheet For Auditing (Acct 252) Diploma ProgrammeAkkamaNo ratings yet

- Ethical Issues Facing Tax ProfessionDocument25 pagesEthical Issues Facing Tax ProfessionNur AsniNo ratings yet

- Performance Task 1Document3 pagesPerformance Task 1Diana CortezNo ratings yet

- Masira VastaDocument2 pagesMasira VastaAakashNo ratings yet

- CVP Analysis - Jan18Document23 pagesCVP Analysis - Jan18Jobert DiliNo ratings yet

- Roadmap To FRK 705Document61 pagesRoadmap To FRK 705RaychelNo ratings yet

- Dygnonise of FusionDocument17 pagesDygnonise of Fusionyramesh77No ratings yet

- Balance Sheet Template PDFDocument2 pagesBalance Sheet Template PDFSubha ManNo ratings yet

- 4 HTMLDocument4 pages4 HTMLOrafuJamesNo ratings yet

- 01 Dan SimunicDocument25 pages01 Dan SimunicVincent LeungNo ratings yet

- Internship Taxation ReportDocument57 pagesInternship Taxation ReportEmmanuel franksteinNo ratings yet

- Accounting For Managers: Dr.R.Vasanthagopal University of KeralaDocument22 pagesAccounting For Managers: Dr.R.Vasanthagopal University of KeralaSmitha K BNo ratings yet