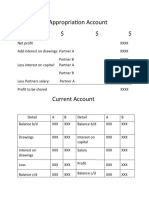

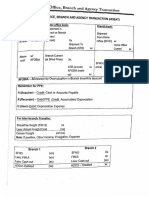

Home Office and Branch Accounting: Investment in BR (IIB) / Branch Current Account (BCA)

Home Office and Branch Accounting: Investment in BR (IIB) / Branch Current Account (BCA)

You might also like

- Accounting-Formats For Cambridge IGCSEDocument11 pagesAccounting-Formats For Cambridge IGCSEmuhtasim kabir100% (9)

- Mini Case of Cost of CapitalDocument13 pagesMini Case of Cost of Capitalpoooja2850% (4)

- Management Accounting Chapter 1Document4 pagesManagement Accounting Chapter 1Ieda ShaharNo ratings yet

- Opre 3310 Final Exam Study Guide 2020Document2 pagesOpre 3310 Final Exam Study Guide 2020An KouNo ratings yet

- MBA - OM Lesson PlanDocument4 pagesMBA - OM Lesson PlannvijayNo ratings yet

- Chapter - 01 LogisticsDocument13 pagesChapter - 01 LogisticsTracy Van Tangonan100% (1)

- Module 2 Home Office and Branch Accounting - Interbranch AccountingDocument5 pagesModule 2 Home Office and Branch Accounting - Interbranch Accountingpajarillagavincent15No ratings yet

- Home Office and Branch AccountingDocument14 pagesHome Office and Branch AccountingRujean Salar AltejarNo ratings yet

- (PAS 1 Par. 66) : Prepared By: Joseph R. Mendoza CPA, MBADocument3 pages(PAS 1 Par. 66) : Prepared By: Joseph R. Mendoza CPA, MBAJoshua LokinoNo ratings yet

- 4 InventoryDocument1 page4 InventoryCharisse AbordoNo ratings yet

- Proforma Journal Entries - Merchandising TransactionsDocument4 pagesProforma Journal Entries - Merchandising TransactionsJames Christian AvesNo ratings yet

- Local Media-1751823765Document33 pagesLocal Media-1751823765Anonymous CuUAaRSNNo ratings yet

- ACYAVA 2 Formula SheetDocument13 pagesACYAVA 2 Formula SheetN SNo ratings yet

- Chapter 10Document12 pagesChapter 10Villanueva, Jane G.No ratings yet

- Cash Base VS Accrual BaseDocument8 pagesCash Base VS Accrual BaseCheryl FuentesNo ratings yet

- FAR 04: Trade Accounts Receivable: J. CayetanoDocument58 pagesFAR 04: Trade Accounts Receivable: J. CayetanoCherrylane EdicaNo ratings yet

- 4 Branch AccountsDocument18 pages4 Branch AccountsBAZINGA100% (1)

- HOBAT NotesDocument2 pagesHOBAT NotesYazieeNo ratings yet

- 6 Branch AccountingDocument48 pages6 Branch AccountingsmartshivenduNo ratings yet

- Financial Statements - Format#3 (GR10)Document3 pagesFinancial Statements - Format#3 (GR10)Nathefa LayneNo ratings yet

- AST HO BR AccountingDocument12 pagesAST HO BR AccountingeiraNo ratings yet

- Home Office and Branch AccountingDocument7 pagesHome Office and Branch AccountingRujean Salar AltejarNo ratings yet

- 2 Assignment For Midterm - Merchandising Business: (Periodic System)Document4 pages2 Assignment For Midterm - Merchandising Business: (Periodic System)Lisa PalermoNo ratings yet

- Format of Financial StatementDocument4 pagesFormat of Financial Statementmardhiahnajihah17No ratings yet

- Accounts Rec. XXX Cash XXX Cash XXXDocument2 pagesAccounts Rec. XXX Cash XXX Cash XXXMikaella LamadoraNo ratings yet

- Balance Sheet (LIST)Document6 pagesBalance Sheet (LIST)Apryl TaiNo ratings yet

- Advanced Financial AccountingDocument102 pagesAdvanced Financial AccountingYash WanthNo ratings yet

- A. Adjusted Balance Method: Reconciling ItemsDocument9 pagesA. Adjusted Balance Method: Reconciling ItemsVirnal R. PaulinoNo ratings yet

- C7 Problem 13Document2 pagesC7 Problem 13Erica CastroNo ratings yet

- Far1 NotesDocument10 pagesFar1 NotesAROCENA, Rosemary ReignNo ratings yet

- Integration: Organization StructureDocument39 pagesIntegration: Organization StructureSantosh TripathiNo ratings yet

- INCOTERMS - Class ExerciseDocument7 pagesINCOTERMS - Class ExerciseEmilio SantaNo ratings yet

- Assets Page 1 4Document12 pagesAssets Page 1 4RELLYSA MARIE ONGNo ratings yet

- قوانين محاسبه اداريهDocument4 pagesقوانين محاسبه اداريهEhab hobaNo ratings yet

- Merchandising Concern 09-26-2022Document8 pagesMerchandising Concern 09-26-2022Rhandy OyaoNo ratings yet

- 2 - Bank ReconciliationDocument1 page2 - Bank ReconciliationCharisse AbordoNo ratings yet

- FAR 215 Inventory EstimationDocument8 pagesFAR 215 Inventory EstimationJai BacalsoNo ratings yet

- AP 001 A.1 Bank Reconciliation LECTUREDocument9 pagesAP 001 A.1 Bank Reconciliation LECTUREJomar Carlo CasupangNo ratings yet

- ABC Text BookDocument115 pagesABC Text BookNaing linnNo ratings yet

- BLACK HT (HT50210) Stock ManagementDocument181 pagesBLACK HT (HT50210) Stock ManagementLULB RFID KR6No ratings yet

- Transfer and Business Taxation Accounting Methods and PeriodsDocument5 pagesTransfer and Business Taxation Accounting Methods and PeriodsApril Joy Padua SimonNo ratings yet

- Accounting Formats For Cambridge Igcse CompressDocument11 pagesAccounting Formats For Cambridge Igcse Compresslegendza010No ratings yet

- Working Papers in InventoriesDocument17 pagesWorking Papers in InventoriesTrisha VillegasNo ratings yet

- Merchandising Formula CardDocument8 pagesMerchandising Formula CardANGELICA ROSE GARCIANo ratings yet

- Debtor Creditor FormatsDocument1 pageDebtor Creditor FormatsFaizan MahmoodNo ratings yet

- Financial Statements Part A&bDocument6 pagesFinancial Statements Part A&b16115dxbpNo ratings yet

- 08 Inventories EstimationsDocument8 pages08 Inventories EstimationsKhen HannaNo ratings yet

- AE221 - Single Entry, Cash, Accrual, CashflowDocument34 pagesAE221 - Single Entry, Cash, Accrual, Cashflow2216391No ratings yet

- Incomplete Record 2019Document3 pagesIncomplete Record 2019Parvatee Ramessur100% (1)

- Container TriangulationDocument14 pagesContainer TriangulationKumudNo ratings yet

- Accounting For PartershipDocument7 pagesAccounting For Partershipwairimuesther506No ratings yet

- Inventories&Inventoryestimation GAPASINAODocument25 pagesInventories&Inventoryestimation GAPASINAOGerly GapasinaoNo ratings yet

- Audit On ReceivablesDocument19 pagesAudit On ReceivablesPaupauNo ratings yet

- Topic 6 Partnership: 6.1 FormationDocument5 pagesTopic 6 Partnership: 6.1 FormationxxpjulxxNo ratings yet

- Cash Flows StatementsDocument4 pagesCash Flows StatementsMae-shane SagayoNo ratings yet

- Pships 2023 VIPDocument17 pagesPships 2023 VIPora mashaNo ratings yet

- Problem XDocument30 pagesProblem XLove FreddyNo ratings yet

- Branch Account Problems & AnswerDocument11 pagesBranch Account Problems & Answeranand dpi0% (1)

- FABM - SCI Quiz 4Document4 pagesFABM - SCI Quiz 4Raidenhile mae VicenteNo ratings yet

- Daily Position For Wagon Condemnation: SN ActivityDocument4 pagesDaily Position For Wagon Condemnation: SN ActivityCWMJMPCELLNo ratings yet

- Tax Incidence, Deadweight Loss, Government Income: Elastic and Inelastic Demand Curves Inelastic Demand Elastic DemandDocument2 pagesTax Incidence, Deadweight Loss, Government Income: Elastic and Inelastic Demand Curves Inelastic Demand Elastic DemandOlebogengPNo ratings yet

- FAR Freight ChargesDocument2 pagesFAR Freight ChargesJaybie John Palco Eralino100% (1)

- 2 PGPM-MPW 2023 Acctg Exerc Sol SH 1Document1 page2 PGPM-MPW 2023 Acctg Exerc Sol SH 1somechnitjNo ratings yet

- Financial Report Merchandising Buisness CorporationDocument4 pagesFinancial Report Merchandising Buisness Corporationcheldulceconstan28No ratings yet

- Managerial Economics ReviewerDocument9 pagesManagerial Economics ReviewerMerrie Rainelle Delos ReyesNo ratings yet

- Chapter 4 Question ReviewDocument11 pagesChapter 4 Question ReviewUyenNo ratings yet

- AbuegDocument10 pagesAbuegswit_kamoteNo ratings yet

- Impact of Digital Marketing On Revenue GenerationDocument75 pagesImpact of Digital Marketing On Revenue GenerationAjay Chopra67% (6)

- China's Foreign Exchange Market AnalysisDocument27 pagesChina's Foreign Exchange Market AnalysisMilanNo ratings yet

- Sampling and MaterialityDocument25 pagesSampling and MaterialityYuliana PriscillaNo ratings yet

- AFAR Quiz 4 and 5Document5 pagesAFAR Quiz 4 and 5Kyla DabalmatNo ratings yet

- Christ University, Bangalore Department of Commerce Certificate Course Course Plan - November 2014 - March 2015Document3 pagesChrist University, Bangalore Department of Commerce Certificate Course Course Plan - November 2014 - March 2015BasappaSarkarNo ratings yet

- ASP Lec 02Document22 pagesASP Lec 02drew quanosNo ratings yet

- Fusion Inventory QuestionDocument10 pagesFusion Inventory QuestionArpit KhandelwalNo ratings yet

- Integrating Marketing Communications To Build Brand EquityDocument37 pagesIntegrating Marketing Communications To Build Brand EquityJITHA JOHNNY 22No ratings yet

- Honda SWOT Analysis 2013 Strengths Weaknesses: Opportunities ThreatsDocument2 pagesHonda SWOT Analysis 2013 Strengths Weaknesses: Opportunities ThreatsPrateek ChaudharyNo ratings yet

- Also, TTDocument11 pagesAlso, TTNUR FARAH ALIAH RAMLANNo ratings yet

- Backing Our Customers: Annual Financial ReportDocument388 pagesBacking Our Customers: Annual Financial ReportKiran NaiduNo ratings yet

- Managerial Accounting Tools For Business Decision Making Canadian 4th Edition Weygandt Test BankDocument35 pagesManagerial Accounting Tools For Business Decision Making Canadian 4th Edition Weygandt Test BankKerriGonzalesgjtkz100% (14)

- Presentation IDocument9 pagesPresentation IVanshika Srivastava 17IFT017No ratings yet

- A Framework For The Analysis of Financial FlexibilityDocument9 pagesA Framework For The Analysis of Financial FlexibilityEdwin GunawanNo ratings yet

- Interest CalculationDocument4 pagesInterest CalculationprasadzNo ratings yet

- Chapter 10-MarketingDocument18 pagesChapter 10-MarketingTrúc Lê Thảo GiaNo ratings yet

- Uds Business Plan Presentation FinalDocument21 pagesUds Business Plan Presentation FinalAdams Yussif KwajaNo ratings yet

- Jam Althea O. Agner Prelec Output 1Document3 pagesJam Althea O. Agner Prelec Output 1JAM ALTHEA AGNERNo ratings yet

- Assignment - B.com 3rd YearDocument6 pagesAssignment - B.com 3rd Yearprakash gangwarNo ratings yet

- PR-2331-Vinamilk- Nguyễn Trần Thiên PhúcDocument6 pagesPR-2331-Vinamilk- Nguyễn Trần Thiên Phúcphuc.ntt06260No ratings yet

- Advacc Final Exam Answer KeyDocument7 pagesAdvacc Final Exam Answer KeyRIZLE SOGRADIELNo ratings yet

- MNO Chapter 06 - Strategic Management - How Exceptional Managers Realise A Grand DesignDocument14 pagesMNO Chapter 06 - Strategic Management - How Exceptional Managers Realise A Grand DesignDouglas FongNo ratings yet

Download as pdf or txt

You might also like

- Accounting-Formats For Cambridge IGCSEDocument11 pagesAccounting-Formats For Cambridge IGCSEmuhtasim kabir100% (9)

- Mini Case of Cost of CapitalDocument13 pagesMini Case of Cost of Capitalpoooja2850% (4)

- Management Accounting Chapter 1Document4 pagesManagement Accounting Chapter 1Ieda ShaharNo ratings yet

- Opre 3310 Final Exam Study Guide 2020Document2 pagesOpre 3310 Final Exam Study Guide 2020An KouNo ratings yet

- MBA - OM Lesson PlanDocument4 pagesMBA - OM Lesson PlannvijayNo ratings yet

- Chapter - 01 LogisticsDocument13 pagesChapter - 01 LogisticsTracy Van Tangonan100% (1)

- Module 2 Home Office and Branch Accounting - Interbranch AccountingDocument5 pagesModule 2 Home Office and Branch Accounting - Interbranch Accountingpajarillagavincent15No ratings yet

- Home Office and Branch AccountingDocument14 pagesHome Office and Branch AccountingRujean Salar AltejarNo ratings yet

- (PAS 1 Par. 66) : Prepared By: Joseph R. Mendoza CPA, MBADocument3 pages(PAS 1 Par. 66) : Prepared By: Joseph R. Mendoza CPA, MBAJoshua LokinoNo ratings yet

- 4 InventoryDocument1 page4 InventoryCharisse AbordoNo ratings yet

- Proforma Journal Entries - Merchandising TransactionsDocument4 pagesProforma Journal Entries - Merchandising TransactionsJames Christian AvesNo ratings yet

- Local Media-1751823765Document33 pagesLocal Media-1751823765Anonymous CuUAaRSNNo ratings yet

- ACYAVA 2 Formula SheetDocument13 pagesACYAVA 2 Formula SheetN SNo ratings yet

- Chapter 10Document12 pagesChapter 10Villanueva, Jane G.No ratings yet

- Cash Base VS Accrual BaseDocument8 pagesCash Base VS Accrual BaseCheryl FuentesNo ratings yet

- FAR 04: Trade Accounts Receivable: J. CayetanoDocument58 pagesFAR 04: Trade Accounts Receivable: J. CayetanoCherrylane EdicaNo ratings yet

- 4 Branch AccountsDocument18 pages4 Branch AccountsBAZINGA100% (1)

- HOBAT NotesDocument2 pagesHOBAT NotesYazieeNo ratings yet

- 6 Branch AccountingDocument48 pages6 Branch AccountingsmartshivenduNo ratings yet

- Financial Statements - Format#3 (GR10)Document3 pagesFinancial Statements - Format#3 (GR10)Nathefa LayneNo ratings yet

- AST HO BR AccountingDocument12 pagesAST HO BR AccountingeiraNo ratings yet

- Home Office and Branch AccountingDocument7 pagesHome Office and Branch AccountingRujean Salar AltejarNo ratings yet

- 2 Assignment For Midterm - Merchandising Business: (Periodic System)Document4 pages2 Assignment For Midterm - Merchandising Business: (Periodic System)Lisa PalermoNo ratings yet

- Format of Financial StatementDocument4 pagesFormat of Financial Statementmardhiahnajihah17No ratings yet

- Accounts Rec. XXX Cash XXX Cash XXXDocument2 pagesAccounts Rec. XXX Cash XXX Cash XXXMikaella LamadoraNo ratings yet

- Balance Sheet (LIST)Document6 pagesBalance Sheet (LIST)Apryl TaiNo ratings yet

- Advanced Financial AccountingDocument102 pagesAdvanced Financial AccountingYash WanthNo ratings yet

- A. Adjusted Balance Method: Reconciling ItemsDocument9 pagesA. Adjusted Balance Method: Reconciling ItemsVirnal R. PaulinoNo ratings yet

- C7 Problem 13Document2 pagesC7 Problem 13Erica CastroNo ratings yet

- Far1 NotesDocument10 pagesFar1 NotesAROCENA, Rosemary ReignNo ratings yet

- Integration: Organization StructureDocument39 pagesIntegration: Organization StructureSantosh TripathiNo ratings yet

- INCOTERMS - Class ExerciseDocument7 pagesINCOTERMS - Class ExerciseEmilio SantaNo ratings yet

- Assets Page 1 4Document12 pagesAssets Page 1 4RELLYSA MARIE ONGNo ratings yet

- قوانين محاسبه اداريهDocument4 pagesقوانين محاسبه اداريهEhab hobaNo ratings yet

- Merchandising Concern 09-26-2022Document8 pagesMerchandising Concern 09-26-2022Rhandy OyaoNo ratings yet

- 2 - Bank ReconciliationDocument1 page2 - Bank ReconciliationCharisse AbordoNo ratings yet

- FAR 215 Inventory EstimationDocument8 pagesFAR 215 Inventory EstimationJai BacalsoNo ratings yet

- AP 001 A.1 Bank Reconciliation LECTUREDocument9 pagesAP 001 A.1 Bank Reconciliation LECTUREJomar Carlo CasupangNo ratings yet

- ABC Text BookDocument115 pagesABC Text BookNaing linnNo ratings yet

- BLACK HT (HT50210) Stock ManagementDocument181 pagesBLACK HT (HT50210) Stock ManagementLULB RFID KR6No ratings yet

- Transfer and Business Taxation Accounting Methods and PeriodsDocument5 pagesTransfer and Business Taxation Accounting Methods and PeriodsApril Joy Padua SimonNo ratings yet

- Accounting Formats For Cambridge Igcse CompressDocument11 pagesAccounting Formats For Cambridge Igcse Compresslegendza010No ratings yet

- Working Papers in InventoriesDocument17 pagesWorking Papers in InventoriesTrisha VillegasNo ratings yet

- Merchandising Formula CardDocument8 pagesMerchandising Formula CardANGELICA ROSE GARCIANo ratings yet

- Debtor Creditor FormatsDocument1 pageDebtor Creditor FormatsFaizan MahmoodNo ratings yet

- Financial Statements Part A&bDocument6 pagesFinancial Statements Part A&b16115dxbpNo ratings yet

- 08 Inventories EstimationsDocument8 pages08 Inventories EstimationsKhen HannaNo ratings yet

- AE221 - Single Entry, Cash, Accrual, CashflowDocument34 pagesAE221 - Single Entry, Cash, Accrual, Cashflow2216391No ratings yet

- Incomplete Record 2019Document3 pagesIncomplete Record 2019Parvatee Ramessur100% (1)

- Container TriangulationDocument14 pagesContainer TriangulationKumudNo ratings yet

- Accounting For PartershipDocument7 pagesAccounting For Partershipwairimuesther506No ratings yet

- Inventories&Inventoryestimation GAPASINAODocument25 pagesInventories&Inventoryestimation GAPASINAOGerly GapasinaoNo ratings yet

- Audit On ReceivablesDocument19 pagesAudit On ReceivablesPaupauNo ratings yet

- Topic 6 Partnership: 6.1 FormationDocument5 pagesTopic 6 Partnership: 6.1 FormationxxpjulxxNo ratings yet

- Cash Flows StatementsDocument4 pagesCash Flows StatementsMae-shane SagayoNo ratings yet

- Pships 2023 VIPDocument17 pagesPships 2023 VIPora mashaNo ratings yet

- Problem XDocument30 pagesProblem XLove FreddyNo ratings yet

- Branch Account Problems & AnswerDocument11 pagesBranch Account Problems & Answeranand dpi0% (1)

- FABM - SCI Quiz 4Document4 pagesFABM - SCI Quiz 4Raidenhile mae VicenteNo ratings yet

- Daily Position For Wagon Condemnation: SN ActivityDocument4 pagesDaily Position For Wagon Condemnation: SN ActivityCWMJMPCELLNo ratings yet

- Tax Incidence, Deadweight Loss, Government Income: Elastic and Inelastic Demand Curves Inelastic Demand Elastic DemandDocument2 pagesTax Incidence, Deadweight Loss, Government Income: Elastic and Inelastic Demand Curves Inelastic Demand Elastic DemandOlebogengPNo ratings yet

- FAR Freight ChargesDocument2 pagesFAR Freight ChargesJaybie John Palco Eralino100% (1)

- 2 PGPM-MPW 2023 Acctg Exerc Sol SH 1Document1 page2 PGPM-MPW 2023 Acctg Exerc Sol SH 1somechnitjNo ratings yet

- Financial Report Merchandising Buisness CorporationDocument4 pagesFinancial Report Merchandising Buisness Corporationcheldulceconstan28No ratings yet

- Managerial Economics ReviewerDocument9 pagesManagerial Economics ReviewerMerrie Rainelle Delos ReyesNo ratings yet

- Chapter 4 Question ReviewDocument11 pagesChapter 4 Question ReviewUyenNo ratings yet

- AbuegDocument10 pagesAbuegswit_kamoteNo ratings yet

- Impact of Digital Marketing On Revenue GenerationDocument75 pagesImpact of Digital Marketing On Revenue GenerationAjay Chopra67% (6)

- China's Foreign Exchange Market AnalysisDocument27 pagesChina's Foreign Exchange Market AnalysisMilanNo ratings yet

- Sampling and MaterialityDocument25 pagesSampling and MaterialityYuliana PriscillaNo ratings yet

- AFAR Quiz 4 and 5Document5 pagesAFAR Quiz 4 and 5Kyla DabalmatNo ratings yet

- Christ University, Bangalore Department of Commerce Certificate Course Course Plan - November 2014 - March 2015Document3 pagesChrist University, Bangalore Department of Commerce Certificate Course Course Plan - November 2014 - March 2015BasappaSarkarNo ratings yet

- ASP Lec 02Document22 pagesASP Lec 02drew quanosNo ratings yet

- Fusion Inventory QuestionDocument10 pagesFusion Inventory QuestionArpit KhandelwalNo ratings yet

- Integrating Marketing Communications To Build Brand EquityDocument37 pagesIntegrating Marketing Communications To Build Brand EquityJITHA JOHNNY 22No ratings yet

- Honda SWOT Analysis 2013 Strengths Weaknesses: Opportunities ThreatsDocument2 pagesHonda SWOT Analysis 2013 Strengths Weaknesses: Opportunities ThreatsPrateek ChaudharyNo ratings yet

- Also, TTDocument11 pagesAlso, TTNUR FARAH ALIAH RAMLANNo ratings yet

- Backing Our Customers: Annual Financial ReportDocument388 pagesBacking Our Customers: Annual Financial ReportKiran NaiduNo ratings yet

- Managerial Accounting Tools For Business Decision Making Canadian 4th Edition Weygandt Test BankDocument35 pagesManagerial Accounting Tools For Business Decision Making Canadian 4th Edition Weygandt Test BankKerriGonzalesgjtkz100% (14)

- Presentation IDocument9 pagesPresentation IVanshika Srivastava 17IFT017No ratings yet

- A Framework For The Analysis of Financial FlexibilityDocument9 pagesA Framework For The Analysis of Financial FlexibilityEdwin GunawanNo ratings yet

- Interest CalculationDocument4 pagesInterest CalculationprasadzNo ratings yet

- Chapter 10-MarketingDocument18 pagesChapter 10-MarketingTrúc Lê Thảo GiaNo ratings yet

- Uds Business Plan Presentation FinalDocument21 pagesUds Business Plan Presentation FinalAdams Yussif KwajaNo ratings yet

- Jam Althea O. Agner Prelec Output 1Document3 pagesJam Althea O. Agner Prelec Output 1JAM ALTHEA AGNERNo ratings yet

- Assignment - B.com 3rd YearDocument6 pagesAssignment - B.com 3rd Yearprakash gangwarNo ratings yet

- PR-2331-Vinamilk- Nguyễn Trần Thiên PhúcDocument6 pagesPR-2331-Vinamilk- Nguyễn Trần Thiên Phúcphuc.ntt06260No ratings yet

- Advacc Final Exam Answer KeyDocument7 pagesAdvacc Final Exam Answer KeyRIZLE SOGRADIELNo ratings yet

- MNO Chapter 06 - Strategic Management - How Exceptional Managers Realise A Grand DesignDocument14 pagesMNO Chapter 06 - Strategic Management - How Exceptional Managers Realise A Grand DesignDouglas FongNo ratings yet