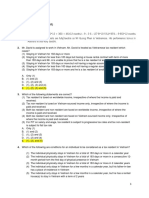

BE4-1. The Adjusted Trial Balance of Pacific Scientific Corporation On

BE4-1. The Adjusted Trial Balance of Pacific Scientific Corporation On

You might also like

- Key Chapter 7 Ms - TrangDocument6 pagesKey Chapter 7 Ms - TrangHoàng Việt VũNo ratings yet

- Bookkeeping ActivitesDocument23 pagesBookkeeping ActivitesRose Darnayla55% (11)

- Managerial AccoutingDocument33 pagesManagerial AccoutingLan TrinhNo ratings yet

- Bài kiểm tra trắc nghiệm tổng hợp các chủ đề - Xem lại bài làmDocument22 pagesBài kiểm tra trắc nghiệm tổng hợp các chủ đề - Xem lại bài làmAh TuanNo ratings yet

- Bài tập chương 4cDocument10 pagesBài tập chương 4cHậu MinNgôNo ratings yet

- Kansas City Property Management AgreementDocument23 pagesKansas City Property Management AgreementJustin ScerboNo ratings yet

- 2.1. For Process A What Is The Scrap Value of The Normal Loss?Document19 pages2.1. For Process A What Is The Scrap Value of The Normal Loss?Yến Nguyễn100% (1)

- Topic 11 - Revenue From Contract With Customers (IFRS 15) - SVDocument56 pagesTopic 11 - Revenue From Contract With Customers (IFRS 15) - SVHONG NGUYEN THI KIMNo ratings yet

- Section 1Document12 pagesSection 1Uyên Ỉn50% (2)

- F6 PIT-AnswersDocument21 pagesF6 PIT-AnswersChippu Anh100% (1)

- Dap An Ke Toan Quoc Te 2 UehDocument165 pagesDap An Ke Toan Quoc Te 2 UehLoki Luke100% (1)

- ACC564 Week 8 Homework 2Document2 pagesACC564 Week 8 Homework 2fombyfNo ratings yet

- Senior High School S.Y. 2019-2020Document4 pagesSenior High School S.Y. 2019-2020Cy Dollete-Suarez100% (1)

- Kế toán quản trị 17 - 4Document8 pagesKế toán quản trị 17 - 4Ly BùiNo ratings yet

- Bài kiểm tra KTQTDocument10 pagesBài kiểm tra KTQTDUYÊN LÊ NGUYỄN MỸNo ratings yet

- Managerial Accounting II - Exam: Problem 1Document3 pagesManagerial Accounting II - Exam: Problem 1NGOC HOANG PHAM YENNo ratings yet

- Ifrs Test 2Document6 pagesIfrs Test 2Ngọc LêNo ratings yet

- Chương 4Document3 pagesChương 4Trần Khánh VyNo ratings yet

- Tổng Hợp Trắc Nghiệm (252 Trang)Document252 pagesTổng Hợp Trắc Nghiệm (252 Trang)Thương TrầnNo ratings yet

- On Tap Ke Toan Quan Tri 1 Quiz Ke Toan Quan TriDocument45 pagesOn Tap Ke Toan Quan Tri 1 Quiz Ke Toan Quan TriPhan HieuNo ratings yet

- Case - MCSDocument3 pagesCase - MCSQUY VO TRONGNo ratings yet

- Managerial AccountingDocument9 pagesManagerial AccountingTrang NguyênNo ratings yet

- CẦN LÀM THEO 2 PHƯƠNG PHÁP vì đề không yêu cầu làm theo phương pháp nàoDocument4 pagesCẦN LÀM THEO 2 PHƯƠNG PHÁP vì đề không yêu cầu làm theo phương pháp nàotrangdoan.31221023445100% (1)

- Quizzes - Topic 2 - Attempt ReviewDocument11 pagesQuizzes - Topic 2 - Attempt ReviewHà Mai VõNo ratings yet

- BaitapnhomF2 Phan2 Chapter2 Nhom4 K24KT2Document9 pagesBaitapnhomF2 Phan2 Chapter2 Nhom4 K24KT2Lúa PhạmNo ratings yet

- Topic 3 - Impairment - SVDocument4 pagesTopic 3 - Impairment - SVHuỳnh Minh Gia Hào100% (2)

- Kế Toán Quốc Tế: Select oneDocument8 pagesKế Toán Quốc Tế: Select oneLoki Luke100% (1)

- VD - IAS 36 (Gui SV) - Chua Co Dap AnDocument5 pagesVD - IAS 36 (Gui SV) - Chua Co Dap AnThiện PhátNo ratings yet

- Midterm 1+ 2 (T NG H P)Document13 pagesMidterm 1+ 2 (T NG H P)Shen NPTDNo ratings yet

- Câu H i ạ ể: Hoàn thành t i m 1,00 trên 1,00Document4 pagesCâu H i ạ ể: Hoàn thành t i m 1,00 trên 1,00Tram NguyenNo ratings yet

- Bài tập nhóm chương 3 - nhóm 4-k24kt02Document18 pagesBài tập nhóm chương 3 - nhóm 4-k24kt02Lúa PhạmNo ratings yet

- Quiz 1 2Document9 pagesQuiz 1 2Hồng ThơmNo ratings yet

- De Thi Giua Hoc Ki Mon Thanh Toan Quoc TeDocument5 pagesDe Thi Giua Hoc Ki Mon Thanh Toan Quoc TeTÚ HOÀNG ANHNo ratings yet

- Bài kiểm tra trắc nghiệm chủ đề - Thanh toán bằng cổ phiếu - - Xem lại bài làmDocument13 pagesBài kiểm tra trắc nghiệm chủ đề - Thanh toán bằng cổ phiếu - - Xem lại bài làmAh TuanNo ratings yet

- Bài kiểm tra tự luận Lợi nhuận mỗi cổ phiếu - Xem lại bài làmDocument8 pagesBài kiểm tra tự luận Lợi nhuận mỗi cổ phiếu - Xem lại bài làmAh TuanNo ratings yet

- PDF - Revenue From Contract With Customers (IFRS 15)Document27 pagesPDF - Revenue From Contract With Customers (IFRS 15)Tram NguyenNo ratings yet

- Quizzes Ias 37 Ke Toan Quoc Te1Document12 pagesQuizzes Ias 37 Ke Toan Quoc Te1Mỹ Ngọc Trần ThịNo ratings yet

- Baitap C3 HVDocument27 pagesBaitap C3 HVThanh ThảoNo ratings yet

- - Mai Thị Hoàng My: Câu HỏiDocument13 pages- Mai Thị Hoàng My: Câu HỏiPhạm Ngọc ÁnhNo ratings yet

- Kế toán quản trị ngày 9 - 5Document6 pagesKế toán quản trị ngày 9 - 5Ly BùiNo ratings yet

- Quizzes - Topic 5 - Impairment of Asset - Attempt ReviewDocument11 pagesQuizzes - Topic 5 - Impairment of Asset - Attempt ReviewThiện Phát100% (1)

- Quizz C3Document10 pagesQuizz C3Thanh NgânNo ratings yet

- - Huỳnh Thị Thiên Nhi: Câu HỏiDocument9 pages- Huỳnh Thị Thiên Nhi: Câu HỏiBông GấuNo ratings yet

- CHƯƠNG 5 -NHÓM 7 - HTTTKT - BÀI TẬPDocument19 pagesCHƯƠNG 5 -NHÓM 7 - HTTTKT - BÀI TẬPVy Ngô100% (1)

- PaDocument9 pagesPaGotta Patti HouseNo ratings yet

- De Thi 2020Document5 pagesDe Thi 2020Kim HồngNo ratings yet

- Corporate Income Tax: Section A - Multiple Choice QuestionsDocument36 pagesCorporate Income Tax: Section A - Multiple Choice QuestionsWanda NguyenNo ratings yet

- Problem 13.1 13.7Document8 pagesProblem 13.1 13.7Le UyenNo ratings yet

- This Study Resource Was: Multiple Choice QuestionsDocument8 pagesThis Study Resource Was: Multiple Choice QuestionsPamela SantosNo ratings yet

- Thực Hành 2020Document17 pagesThực Hành 2020Sún HítNo ratings yet

- Lợi Nhuận Trên Mỗi Cổ PhiếuDocument6 pagesLợi Nhuận Trên Mỗi Cổ PhiếuLoki Luke100% (1)

- MQ - Ifrs 9Document11 pagesMQ - Ifrs 9Huỳnh Minh Gia HàoNo ratings yet

- Quiz Chương Btap - HTRDocument7 pagesQuiz Chương Btap - HTRDOAN NGUYEN TRAN THUCNo ratings yet

- Quizzes - Topic 4 - Xem L I Bài LàmDocument4 pagesQuizzes - Topic 4 - Xem L I Bài LàmHải YếnNo ratings yet

- c20 KTTC 3Document34 pagesc20 KTTC 3Trần Nguyễn Tuệ MinhNo ratings yet

- tổng hợp đề KTQT 2Document43 pagestổng hợp đề KTQT 2Ly BùiNo ratings yet

- Bai Tap CF 2018 Solution PDFDocument11 pagesBai Tap CF 2018 Solution PDFXuân Huỳnh100% (2)

- 21 Problems For CB NewDocument31 pages21 Problems For CB NewNguyễn Thảo MyNo ratings yet

- Kiểm Tra Giữa Kì Hệ Thống Thông Tin Kế Toán Kiểm Tra Giữa Kì Hệ Thống Thông Tin Kế ToánDocument14 pagesKiểm Tra Giữa Kì Hệ Thống Thông Tin Kế Toán Kiểm Tra Giữa Kì Hệ Thống Thông Tin Kế ToánLOC TRUONG TANNo ratings yet

- - Đặng Hương Giang: Câu HỏiDocument4 pages- Đặng Hương Giang: Câu HỏiHANG NGUYEN THI THANHNo ratings yet

- Topic 1: Conceptual FrameworkDocument16 pagesTopic 1: Conceptual FrameworkHuỳnh Như PhạmNo ratings yet

- Financial StatementsDocument3 pagesFinancial StatementsMahibabaNo ratings yet

- SPM Example 3Document8 pagesSPM Example 3inderNo ratings yet

- Income TaxDocument98 pagesIncome TaxGunjan Maheshwari50% (2)

- Tax 2 NotesDocument57 pagesTax 2 NotesMelissa MarinduqueNo ratings yet

- "Azvirt" Limited Liability Company: 25. Construction RevenueDocument1 page"Azvirt" Limited Liability Company: 25. Construction RevenueŞeyxəli ŞəliyevNo ratings yet

- Government AccountingDocument2 pagesGovernment AccountingJoody CatacutanNo ratings yet

- Accounting Notes PDFDocument13 pagesAccounting Notes PDFStellaNo ratings yet

- Jhurzel Anne S. Aguilar BSBA MM-2105: Personal Income/expenses of The HeirsDocument4 pagesJhurzel Anne S. Aguilar BSBA MM-2105: Personal Income/expenses of The HeirsJESTONI RAMOSNo ratings yet

- Chapter 5 Accounting EquationDocument8 pagesChapter 5 Accounting EquationDevam junejaNo ratings yet

- 677261-Foundations of Financial Management Ch04Document28 pages677261-Foundations of Financial Management Ch04pcman92No ratings yet

- Solution Manual For Cfin 5Th Edition by Besley and Brigham Isbn 1305661656 9781305661653 Full Chapter PDFDocument36 pagesSolution Manual For Cfin 5Th Edition by Besley and Brigham Isbn 1305661656 9781305661653 Full Chapter PDFtiffany.kunst387100% (12)

- Acca f6 Taxation Vietnam 2012 Dec QuestionDocument13 pagesAcca f6 Taxation Vietnam 2012 Dec QuestionNguyễn GiangNo ratings yet

- Budgetry ControlDocument61 pagesBudgetry ControlPranav Shandil100% (1)

- Lecture 3 Business IncomeDocument47 pagesLecture 3 Business IncomeVeenesha MuralidharanNo ratings yet

- CRM-M 36522 2019 06 01 2020 Final OrderDocument32 pagesCRM-M 36522 2019 06 01 2020 Final OrderLatest Laws Team67% (3)

- m20 ATX MYS QPDocument13 pagesm20 ATX MYS QPizzahderhamNo ratings yet

- Accounting Standard 34Document34 pagesAccounting Standard 34Kisi Ka Dar NahiNo ratings yet

- AFA WorksheetDocument3 pagesAFA WorksheetanasfinkileNo ratings yet

- National Municipal Accounting Manual PDFDocument722 pagesNational Municipal Accounting Manual PDFpravin100% (1)

- 2014 - UOL Management Accounting ReportDocument46 pages2014 - UOL Management Accounting ReportAbdulAzeemNo ratings yet

- Allowe Training ResourcesDocument29 pagesAllowe Training ResourcesIon Logofătu AlbertNo ratings yet

- A Sample Organic (Vegetarian) Restaurant Business Plan Template - ProfitableVentureDocument18 pagesA Sample Organic (Vegetarian) Restaurant Business Plan Template - ProfitableVentureYashna BeeharryNo ratings yet

- Page 1 of 20 Chapter 6 - Accounting For PartnershipsDocument20 pagesPage 1 of 20 Chapter 6 - Accounting For PartnershipsELLAINE MA EBLACASNo ratings yet

- Best Way Cement........Document13 pagesBest Way Cement........veer2020No ratings yet

- Prospective Analysis 1Document5 pagesProspective Analysis 1MAYANK JAINNo ratings yet

- PayslipDocument1 pagePaysliplove entertainmentNo ratings yet

- IAS 12 Solutions PDFDocument74 pagesIAS 12 Solutions PDFrafid aliNo ratings yet

- Entrep12 Q2 M7 Forecasting-Revenues-And-CostsDocument36 pagesEntrep12 Q2 M7 Forecasting-Revenues-And-CostsThea Iris EscanillaNo ratings yet

- May 2016 Ques & Answers Taxation-&-Fiscal-policy May 2016Document14 pagesMay 2016 Ques & Answers Taxation-&-Fiscal-policy May 2016Timore FrancisNo ratings yet

Download as docx, pdf, or txt

You might also like

- Key Chapter 7 Ms - TrangDocument6 pagesKey Chapter 7 Ms - TrangHoàng Việt VũNo ratings yet

- Bookkeeping ActivitesDocument23 pagesBookkeeping ActivitesRose Darnayla55% (11)

- Managerial AccoutingDocument33 pagesManagerial AccoutingLan TrinhNo ratings yet

- Bài kiểm tra trắc nghiệm tổng hợp các chủ đề - Xem lại bài làmDocument22 pagesBài kiểm tra trắc nghiệm tổng hợp các chủ đề - Xem lại bài làmAh TuanNo ratings yet

- Bài tập chương 4cDocument10 pagesBài tập chương 4cHậu MinNgôNo ratings yet

- Kansas City Property Management AgreementDocument23 pagesKansas City Property Management AgreementJustin ScerboNo ratings yet

- 2.1. For Process A What Is The Scrap Value of The Normal Loss?Document19 pages2.1. For Process A What Is The Scrap Value of The Normal Loss?Yến Nguyễn100% (1)

- Topic 11 - Revenue From Contract With Customers (IFRS 15) - SVDocument56 pagesTopic 11 - Revenue From Contract With Customers (IFRS 15) - SVHONG NGUYEN THI KIMNo ratings yet

- Section 1Document12 pagesSection 1Uyên Ỉn50% (2)

- F6 PIT-AnswersDocument21 pagesF6 PIT-AnswersChippu Anh100% (1)

- Dap An Ke Toan Quoc Te 2 UehDocument165 pagesDap An Ke Toan Quoc Te 2 UehLoki Luke100% (1)

- ACC564 Week 8 Homework 2Document2 pagesACC564 Week 8 Homework 2fombyfNo ratings yet

- Senior High School S.Y. 2019-2020Document4 pagesSenior High School S.Y. 2019-2020Cy Dollete-Suarez100% (1)

- Kế toán quản trị 17 - 4Document8 pagesKế toán quản trị 17 - 4Ly BùiNo ratings yet

- Bài kiểm tra KTQTDocument10 pagesBài kiểm tra KTQTDUYÊN LÊ NGUYỄN MỸNo ratings yet

- Managerial Accounting II - Exam: Problem 1Document3 pagesManagerial Accounting II - Exam: Problem 1NGOC HOANG PHAM YENNo ratings yet

- Ifrs Test 2Document6 pagesIfrs Test 2Ngọc LêNo ratings yet

- Chương 4Document3 pagesChương 4Trần Khánh VyNo ratings yet

- Tổng Hợp Trắc Nghiệm (252 Trang)Document252 pagesTổng Hợp Trắc Nghiệm (252 Trang)Thương TrầnNo ratings yet

- On Tap Ke Toan Quan Tri 1 Quiz Ke Toan Quan TriDocument45 pagesOn Tap Ke Toan Quan Tri 1 Quiz Ke Toan Quan TriPhan HieuNo ratings yet

- Case - MCSDocument3 pagesCase - MCSQUY VO TRONGNo ratings yet

- Managerial AccountingDocument9 pagesManagerial AccountingTrang NguyênNo ratings yet

- CẦN LÀM THEO 2 PHƯƠNG PHÁP vì đề không yêu cầu làm theo phương pháp nàoDocument4 pagesCẦN LÀM THEO 2 PHƯƠNG PHÁP vì đề không yêu cầu làm theo phương pháp nàotrangdoan.31221023445100% (1)

- Quizzes - Topic 2 - Attempt ReviewDocument11 pagesQuizzes - Topic 2 - Attempt ReviewHà Mai VõNo ratings yet

- BaitapnhomF2 Phan2 Chapter2 Nhom4 K24KT2Document9 pagesBaitapnhomF2 Phan2 Chapter2 Nhom4 K24KT2Lúa PhạmNo ratings yet

- Topic 3 - Impairment - SVDocument4 pagesTopic 3 - Impairment - SVHuỳnh Minh Gia Hào100% (2)

- Kế Toán Quốc Tế: Select oneDocument8 pagesKế Toán Quốc Tế: Select oneLoki Luke100% (1)

- VD - IAS 36 (Gui SV) - Chua Co Dap AnDocument5 pagesVD - IAS 36 (Gui SV) - Chua Co Dap AnThiện PhátNo ratings yet

- Midterm 1+ 2 (T NG H P)Document13 pagesMidterm 1+ 2 (T NG H P)Shen NPTDNo ratings yet

- Câu H i ạ ể: Hoàn thành t i m 1,00 trên 1,00Document4 pagesCâu H i ạ ể: Hoàn thành t i m 1,00 trên 1,00Tram NguyenNo ratings yet

- Bài tập nhóm chương 3 - nhóm 4-k24kt02Document18 pagesBài tập nhóm chương 3 - nhóm 4-k24kt02Lúa PhạmNo ratings yet

- Quiz 1 2Document9 pagesQuiz 1 2Hồng ThơmNo ratings yet

- De Thi Giua Hoc Ki Mon Thanh Toan Quoc TeDocument5 pagesDe Thi Giua Hoc Ki Mon Thanh Toan Quoc TeTÚ HOÀNG ANHNo ratings yet

- Bài kiểm tra trắc nghiệm chủ đề - Thanh toán bằng cổ phiếu - - Xem lại bài làmDocument13 pagesBài kiểm tra trắc nghiệm chủ đề - Thanh toán bằng cổ phiếu - - Xem lại bài làmAh TuanNo ratings yet

- Bài kiểm tra tự luận Lợi nhuận mỗi cổ phiếu - Xem lại bài làmDocument8 pagesBài kiểm tra tự luận Lợi nhuận mỗi cổ phiếu - Xem lại bài làmAh TuanNo ratings yet

- PDF - Revenue From Contract With Customers (IFRS 15)Document27 pagesPDF - Revenue From Contract With Customers (IFRS 15)Tram NguyenNo ratings yet

- Quizzes Ias 37 Ke Toan Quoc Te1Document12 pagesQuizzes Ias 37 Ke Toan Quoc Te1Mỹ Ngọc Trần ThịNo ratings yet

- Baitap C3 HVDocument27 pagesBaitap C3 HVThanh ThảoNo ratings yet

- - Mai Thị Hoàng My: Câu HỏiDocument13 pages- Mai Thị Hoàng My: Câu HỏiPhạm Ngọc ÁnhNo ratings yet

- Kế toán quản trị ngày 9 - 5Document6 pagesKế toán quản trị ngày 9 - 5Ly BùiNo ratings yet

- Quizzes - Topic 5 - Impairment of Asset - Attempt ReviewDocument11 pagesQuizzes - Topic 5 - Impairment of Asset - Attempt ReviewThiện Phát100% (1)

- Quizz C3Document10 pagesQuizz C3Thanh NgânNo ratings yet

- - Huỳnh Thị Thiên Nhi: Câu HỏiDocument9 pages- Huỳnh Thị Thiên Nhi: Câu HỏiBông GấuNo ratings yet

- CHƯƠNG 5 -NHÓM 7 - HTTTKT - BÀI TẬPDocument19 pagesCHƯƠNG 5 -NHÓM 7 - HTTTKT - BÀI TẬPVy Ngô100% (1)

- PaDocument9 pagesPaGotta Patti HouseNo ratings yet

- De Thi 2020Document5 pagesDe Thi 2020Kim HồngNo ratings yet

- Corporate Income Tax: Section A - Multiple Choice QuestionsDocument36 pagesCorporate Income Tax: Section A - Multiple Choice QuestionsWanda NguyenNo ratings yet

- Problem 13.1 13.7Document8 pagesProblem 13.1 13.7Le UyenNo ratings yet

- This Study Resource Was: Multiple Choice QuestionsDocument8 pagesThis Study Resource Was: Multiple Choice QuestionsPamela SantosNo ratings yet

- Thực Hành 2020Document17 pagesThực Hành 2020Sún HítNo ratings yet

- Lợi Nhuận Trên Mỗi Cổ PhiếuDocument6 pagesLợi Nhuận Trên Mỗi Cổ PhiếuLoki Luke100% (1)

- MQ - Ifrs 9Document11 pagesMQ - Ifrs 9Huỳnh Minh Gia HàoNo ratings yet

- Quiz Chương Btap - HTRDocument7 pagesQuiz Chương Btap - HTRDOAN NGUYEN TRAN THUCNo ratings yet

- Quizzes - Topic 4 - Xem L I Bài LàmDocument4 pagesQuizzes - Topic 4 - Xem L I Bài LàmHải YếnNo ratings yet

- c20 KTTC 3Document34 pagesc20 KTTC 3Trần Nguyễn Tuệ MinhNo ratings yet

- tổng hợp đề KTQT 2Document43 pagestổng hợp đề KTQT 2Ly BùiNo ratings yet

- Bai Tap CF 2018 Solution PDFDocument11 pagesBai Tap CF 2018 Solution PDFXuân Huỳnh100% (2)

- 21 Problems For CB NewDocument31 pages21 Problems For CB NewNguyễn Thảo MyNo ratings yet

- Kiểm Tra Giữa Kì Hệ Thống Thông Tin Kế Toán Kiểm Tra Giữa Kì Hệ Thống Thông Tin Kế ToánDocument14 pagesKiểm Tra Giữa Kì Hệ Thống Thông Tin Kế Toán Kiểm Tra Giữa Kì Hệ Thống Thông Tin Kế ToánLOC TRUONG TANNo ratings yet

- - Đặng Hương Giang: Câu HỏiDocument4 pages- Đặng Hương Giang: Câu HỏiHANG NGUYEN THI THANHNo ratings yet

- Topic 1: Conceptual FrameworkDocument16 pagesTopic 1: Conceptual FrameworkHuỳnh Như PhạmNo ratings yet

- Financial StatementsDocument3 pagesFinancial StatementsMahibabaNo ratings yet

- SPM Example 3Document8 pagesSPM Example 3inderNo ratings yet

- Income TaxDocument98 pagesIncome TaxGunjan Maheshwari50% (2)

- Tax 2 NotesDocument57 pagesTax 2 NotesMelissa MarinduqueNo ratings yet

- "Azvirt" Limited Liability Company: 25. Construction RevenueDocument1 page"Azvirt" Limited Liability Company: 25. Construction RevenueŞeyxəli ŞəliyevNo ratings yet

- Government AccountingDocument2 pagesGovernment AccountingJoody CatacutanNo ratings yet

- Accounting Notes PDFDocument13 pagesAccounting Notes PDFStellaNo ratings yet

- Jhurzel Anne S. Aguilar BSBA MM-2105: Personal Income/expenses of The HeirsDocument4 pagesJhurzel Anne S. Aguilar BSBA MM-2105: Personal Income/expenses of The HeirsJESTONI RAMOSNo ratings yet

- Chapter 5 Accounting EquationDocument8 pagesChapter 5 Accounting EquationDevam junejaNo ratings yet

- 677261-Foundations of Financial Management Ch04Document28 pages677261-Foundations of Financial Management Ch04pcman92No ratings yet

- Solution Manual For Cfin 5Th Edition by Besley and Brigham Isbn 1305661656 9781305661653 Full Chapter PDFDocument36 pagesSolution Manual For Cfin 5Th Edition by Besley and Brigham Isbn 1305661656 9781305661653 Full Chapter PDFtiffany.kunst387100% (12)

- Acca f6 Taxation Vietnam 2012 Dec QuestionDocument13 pagesAcca f6 Taxation Vietnam 2012 Dec QuestionNguyễn GiangNo ratings yet

- Budgetry ControlDocument61 pagesBudgetry ControlPranav Shandil100% (1)

- Lecture 3 Business IncomeDocument47 pagesLecture 3 Business IncomeVeenesha MuralidharanNo ratings yet

- CRM-M 36522 2019 06 01 2020 Final OrderDocument32 pagesCRM-M 36522 2019 06 01 2020 Final OrderLatest Laws Team67% (3)

- m20 ATX MYS QPDocument13 pagesm20 ATX MYS QPizzahderhamNo ratings yet

- Accounting Standard 34Document34 pagesAccounting Standard 34Kisi Ka Dar NahiNo ratings yet

- AFA WorksheetDocument3 pagesAFA WorksheetanasfinkileNo ratings yet

- National Municipal Accounting Manual PDFDocument722 pagesNational Municipal Accounting Manual PDFpravin100% (1)

- 2014 - UOL Management Accounting ReportDocument46 pages2014 - UOL Management Accounting ReportAbdulAzeemNo ratings yet

- Allowe Training ResourcesDocument29 pagesAllowe Training ResourcesIon Logofătu AlbertNo ratings yet

- A Sample Organic (Vegetarian) Restaurant Business Plan Template - ProfitableVentureDocument18 pagesA Sample Organic (Vegetarian) Restaurant Business Plan Template - ProfitableVentureYashna BeeharryNo ratings yet

- Page 1 of 20 Chapter 6 - Accounting For PartnershipsDocument20 pagesPage 1 of 20 Chapter 6 - Accounting For PartnershipsELLAINE MA EBLACASNo ratings yet

- Best Way Cement........Document13 pagesBest Way Cement........veer2020No ratings yet

- Prospective Analysis 1Document5 pagesProspective Analysis 1MAYANK JAINNo ratings yet

- PayslipDocument1 pagePaysliplove entertainmentNo ratings yet

- IAS 12 Solutions PDFDocument74 pagesIAS 12 Solutions PDFrafid aliNo ratings yet

- Entrep12 Q2 M7 Forecasting-Revenues-And-CostsDocument36 pagesEntrep12 Q2 M7 Forecasting-Revenues-And-CostsThea Iris EscanillaNo ratings yet

- May 2016 Ques & Answers Taxation-&-Fiscal-policy May 2016Document14 pagesMay 2016 Ques & Answers Taxation-&-Fiscal-policy May 2016Timore FrancisNo ratings yet