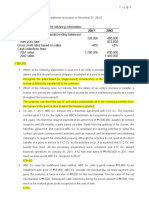

Use The Following Information For The Next Two Questions

Use The Following Information For The Next Two Questions

You might also like

- Answers - Activity 2.4 2.5 and 3.1Document38 pagesAnswers - Activity 2.4 2.5 and 3.1Tine Vasiana Duerme83% (6)

- Afar QuestionsDocument16 pagesAfar QuestionsJessarene Fauni Depante50% (18)

- Questions SsDocument7 pagesQuestions SsAngelli Lamique100% (2)

- AFAR Questions With AnswersDocument11 pagesAFAR Questions With AnswersAngelica CerioNo ratings yet

- OrDocument10 pagesOrasdf100% (1)

- LTCC and Franchise Long Exam PDFDocument9 pagesLTCC and Franchise Long Exam PDFChristine Joy Original50% (2)

- ACC110 P3Quiz2 AnswersDocument12 pagesACC110 P3Quiz2 AnswersTricia Mae FernandezNo ratings yet

- Chapter 10 - Teacher's Manual - Afar Part 1Document20 pagesChapter 10 - Teacher's Manual - Afar Part 1Angelic67% (3)

- Buss. Combi PrelimDocument8 pagesBuss. Combi PrelimPhia TeoNo ratings yet

- Module 8 - Home Office, Branch and Agency AccountingDocument8 pagesModule 8 - Home Office, Branch and Agency AccountingSunshine Khuletz67% (3)

- Chapter 11 - Home Agency, Branch and Agency AccountingDocument14 pagesChapter 11 - Home Agency, Branch and Agency Accountingmonica ocureza100% (1)

- This Study Resource WasDocument3 pagesThis Study Resource WasQueeny Mae Cantre ReutaNo ratings yet

- Consolidated Financial Statements: XYZ, Inc. Carrying Amounts Fair Values Fair Value Adjustments (FVA)Document3 pagesConsolidated Financial Statements: XYZ, Inc. Carrying Amounts Fair Values Fair Value Adjustments (FVA)mhar lon100% (2)

- QUIZ - CHAPTER 8 - ACCOUNTING FOR FRANCHISE OPERATIONS FRANCHISOR NoaDocument3 pagesQUIZ - CHAPTER 8 - ACCOUNTING FOR FRANCHISE OPERATIONS FRANCHISOR NoaNeirish fainsan43% (7)

- Joint Arrangement Quiz AnswersDocument7 pagesJoint Arrangement Quiz AnswersAlexandrite100% (1)

- Excercises On Branch and Home Office Chapter TwoDocument3 pagesExcercises On Branch and Home Office Chapter Twoሔርሞን ይድነቃቸው50% (4)

- Entendiendo El Estado de ResultadoDocument105 pagesEntendiendo El Estado de ResultadodidioserNo ratings yet

- MODULE 3 - Installment SalesDocument8 pagesMODULE 3 - Installment SalesEdison Salgado Castigador50% (2)

- ACC110 P3Quiz2 AnswersDocument12 pagesACC110 P3Quiz2 AnswersTricia Mae FernandezNo ratings yet

- Home Office and Branch AccountingDocument5 pagesHome Office and Branch AccountingMaryjoy Sarzadilla JuanataNo ratings yet

- Activity 1Document4 pagesActivity 1Fernando III PerezNo ratings yet

- p1 Quiz With TheoryDocument15 pagesp1 Quiz With TheoryGrace CorpoNo ratings yet

- PDF Valle Quiz ABC CompressDocument6 pagesPDF Valle Quiz ABC CompressPotie RhymeszNo ratings yet

- Chapter 9 Teachers Manual Afar Part 1Document9 pagesChapter 9 Teachers Manual Afar Part 1Aimee Diaz100% (3)

- Notes For Advanced AccountingDocument5 pagesNotes For Advanced AccountingSoleil Sierra0% (1)

- Name: Date: Professor: Section: Score: Assynchronous Activity-Final TermDocument14 pagesName: Date: Professor: Section: Score: Assynchronous Activity-Final TermkmarisseeNo ratings yet

- LTCCDocument7 pagesLTCCgenevieve sicatNo ratings yet

- 07 Installment SalesDocument1 page07 Installment SalesGem Yiel33% (3)

- 13 Business Combination Pt3Document1 page13 Business Combination Pt3Riselle Ann Sanchez50% (2)

- Home Office, Branch and Agency Accounting: Problem 11-1: True or FalseDocument13 pagesHome Office, Branch and Agency Accounting: Problem 11-1: True or FalseVenz Lacre100% (1)

- LTCCDocument7 pagesLTCCGenesis Dizon67% (6)

- AFAR - Revenue Recognition 2019Document4 pagesAFAR - Revenue Recognition 2019Joanna Rose DeciarNo ratings yet

- Sample ProblemsDocument3 pagesSample ProblemsGracias100% (1)

- Buss. Combi PrelimDocument8 pagesBuss. Combi PrelimPhia TeoNo ratings yet

- Special Tansaction Quiz 1 and 2Document4 pagesSpecial Tansaction Quiz 1 and 2Helen Fiedalan Falcutila MondiaNo ratings yet

- Enabling Assessment: (Note: Several Ted Suavillo Cases)Document2 pagesEnabling Assessment: (Note: Several Ted Suavillo Cases)Von Andrei MedinaNo ratings yet

- Chapter 7 Accounting For Franchise Operations FranchisorDocument15 pagesChapter 7 Accounting For Franchise Operations FranchisorKaren BalibalosNo ratings yet

- Business Combination ExerciseDocument5 pagesBusiness Combination Exercise수지No ratings yet

- Accounting ResearchDocument28 pagesAccounting ResearchRhanel Joy Cayube100% (2)

- FL AfarDocument20 pagesFL AfarKenneth Robledo50% (2)

- Corporate Liquidation Quiz 5docxDocument5 pagesCorporate Liquidation Quiz 5docxAngelica Duarte33% (6)

- AFAR - Installment, Customer, ConsignmentDocument3 pagesAFAR - Installment, Customer, ConsignmentJoanna Rose DeciarNo ratings yet

- Chapter 4 Teachers Manual Afar Part 1Document13 pagesChapter 4 Teachers Manual Afar Part 1cezyyyyyyNo ratings yet

- Afar1-Exercises 2Document17 pagesAfar1-Exercises 2aleachon100% (1)

- Activity-Chapter 7: Ans. None of These SolutionDocument1 pageActivity-Chapter 7: Ans. None of These SolutionRandelle James FiestaNo ratings yet

- Ast - 3B - Quiz No. 1Document10 pagesAst - 3B - Quiz No. 1Renalyn Paras0% (1)

- Illustration Problem & SolutionDocument4 pagesIllustration Problem & SolutionClauie BarsNo ratings yet

- Cebu Institute of Technology - University: Use The Following Information For The Next Two QuestionsDocument13 pagesCebu Institute of Technology - University: Use The Following Information For The Next Two QuestionsPrima Facie50% (2)

- AuditingDocument14 pagesAuditingedrick LouiseNo ratings yet

- Chapter 7 - Teacher's Manual - Afar Part 1Document24 pagesChapter 7 - Teacher's Manual - Afar Part 1Angelic100% (3)

- Grace-AST Module 10Document5 pagesGrace-AST Module 10Devine Grace A. MaghinayNo ratings yet

- Consignment Sales: Name: Date: Professor: Section: Score: QuizDocument3 pagesConsignment Sales: Name: Date: Professor: Section: Score: QuizAndrea Florence Guy VidalNo ratings yet

- Prelim Exam - Doc2Document16 pagesPrelim Exam - Doc2alellie100% (1)

- Quiz 2 Joint ArrangementsDocument4 pagesQuiz 2 Joint ArrangementsJane Gavino100% (2)

- Chapter 10 SolMan Special Accounting 1 Millan 2018Document20 pagesChapter 10 SolMan Special Accounting 1 Millan 2018Alvin Jheii Sioco Alfonso100% (1)

- HO, B & A AcctgDocument15 pagesHO, B & A AcctgCarolina Fortez Dacanay71% (7)

- Construction IllustrationDocument54 pagesConstruction IllustrationCatherine Joy Vasaya100% (3)

- ExerciseDocument4 pagesExerciseMae RxNo ratings yet

- Home and Branch Part 1Document4 pagesHome and Branch Part 1Jessica Libunao100% (1)

- Quiz#3 CompleteDocument2 pagesQuiz#3 CompleteGio SantosNo ratings yet

- Agency and Branch Accounting - General Procedures - v.2.0Document3 pagesAgency and Branch Accounting - General Procedures - v.2.0Catherine SelladoNo ratings yet

- Branches and Agencies - OdtDocument9 pagesBranches and Agencies - OdtEunice BernalNo ratings yet

- Home Office and Branch AccountingDocument4 pagesHome Office and Branch AccountingMaurice AgbayaniNo ratings yet

- LUCHANA Narrative ExperienceDocument2 pagesLUCHANA Narrative ExperienceAllecks Juel LuchanaNo ratings yet

- IRC 1 - P1 Final Exam (Second Sem 2013 - 2014)Document13 pagesIRC 1 - P1 Final Exam (Second Sem 2013 - 2014)Allecks Juel LuchanaNo ratings yet

- Act3 StatDocument33 pagesAct3 StatAllecks Juel Luchana0% (1)

- Himarios Company Worksheet To Prepare Financial Statements DECEMBER 31, 20X9Document3 pagesHimarios Company Worksheet To Prepare Financial Statements DECEMBER 31, 20X9Allecks Juel LuchanaNo ratings yet

- Amber Nestor Art Gallery Trial Balance As of December 31, 20X4Document10 pagesAmber Nestor Art Gallery Trial Balance As of December 31, 20X4Allecks Juel LuchanaNo ratings yet

- Auditing in A Cis EnvironmentDocument23 pagesAuditing in A Cis EnvironmentAllecks Juel LuchanaNo ratings yet

- Unit Summary D-7&8Document5 pagesUnit Summary D-7&8Allecks Juel LuchanaNo ratings yet

- RPH First Cry of Phil RevDocument6 pagesRPH First Cry of Phil RevAllecks Juel LuchanaNo ratings yet

- RPH SourcesDocument2 pagesRPH SourcesAllecks Juel LuchanaNo ratings yet

- Luchana, A. - Cbmec Case Study 2 (Chapter 4)Document5 pagesLuchana, A. - Cbmec Case Study 2 (Chapter 4)Allecks Juel LuchanaNo ratings yet

- Cbmec QuizDocument2 pagesCbmec QuizAllecks Juel LuchanaNo ratings yet

- Cbmec FinalDocument9 pagesCbmec FinalAllecks Juel LuchanaNo ratings yet

- ACC 110 - Day 19 - 20 - SASDocument15 pagesACC 110 - Day 19 - 20 - SASFeedback Or BawiNo ratings yet

- Installment SalesDocument14 pagesInstallment SalesAlexandriteNo ratings yet

- AFAR Review Midterm ExamDocument10 pagesAFAR Review Midterm ExamZyrah Mae SaezNo ratings yet

- Installment and LTCCDocument9 pagesInstallment and LTCCAngelica RubiosNo ratings yet

- Summary Notes Installment Sales and Consignment SalesDocument11 pagesSummary Notes Installment Sales and Consignment SalesJaycel OngyNo ratings yet

- Welcome Aboard 3 Year Bsa!!Document61 pagesWelcome Aboard 3 Year Bsa!!Riza Mae AlceNo ratings yet

- Installment Sales ConceptsDocument61 pagesInstallment Sales ConceptsRanne BalanaNo ratings yet

- IFRS 15 & Installment Sales - QUIZDocument5 pagesIFRS 15 & Installment Sales - QUIZArieza MontañoNo ratings yet

- Template - Acctg. Major 3 Module 5 PDFDocument16 pagesTemplate - Acctg. Major 3 Module 5 PDFRia Mendez100% (2)

- Module 7 InstallmentDocument12 pagesModule 7 InstallmentNiki DimaanoNo ratings yet

- Chapter 09Document16 pagesChapter 09FireBNo ratings yet

- Acct 557 Week 1 HomeworkDocument16 pagesAcct 557 Week 1 HomeworkMichelle Porter-Price0% (1)

- 2 - FSA1 Handout (Topic 3) - Standard&incomeDocument73 pages2 - FSA1 Handout (Topic 3) - Standard&incomeGuyu PanNo ratings yet

- Solution Manual Chapter 9Document16 pagesSolution Manual Chapter 9Shealalyn1100% (2)

- Solution Chapter 9Document15 pagesSolution Chapter 9BobslaneLlenos0% (2)

- Accsptr - ReviewerDocument10 pagesAccsptr - ReviewerDanna VargasNo ratings yet

- Installment Sales Multiple QuestionsDocument36 pagesInstallment Sales Multiple QuestionsTrixie CapisosNo ratings yet

- Installment Sales AccountingDocument9 pagesInstallment Sales AccountingCillian ReevesNo ratings yet

- Loss On Repossession 3,800Document2 pagesLoss On Repossession 3,800Future CPANo ratings yet

- Installment Sales Method Cost Recovery Method (Traditional)Document23 pagesInstallment Sales Method Cost Recovery Method (Traditional)yhygyugNo ratings yet

- Advanced-Accounting-Part 1-Dayag-2015-Chapter-9Document19 pagesAdvanced-Accounting-Part 1-Dayag-2015-Chapter-9trisha sacramento100% (4)

- Installment Sales-: Loss On Repossession XXX Gain On Repossession XXXDocument5 pagesInstallment Sales-: Loss On Repossession XXX Gain On Repossession XXXJoyce Ann Agdippa BarcelonaNo ratings yet

- Accounting For Special Transaction Final ReviewerDocument73 pagesAccounting For Special Transaction Final ReviewerLunaNo ratings yet

- Illustration Problem & SolutionDocument4 pagesIllustration Problem & SolutionClauie BarsNo ratings yet

- Advacc1 Installment SalesDocument21 pagesAdvacc1 Installment SalesAlex OngNo ratings yet

- Advance Chapter 3Document12 pagesAdvance Chapter 3abel habtamuNo ratings yet

- Topic 2 Installment Sales Module Part 1Document5 pagesTopic 2 Installment Sales Module Part 1Maricel Ann BaccayNo ratings yet

Download as docx, pdf, or txt

You might also like

- Answers - Activity 2.4 2.5 and 3.1Document38 pagesAnswers - Activity 2.4 2.5 and 3.1Tine Vasiana Duerme83% (6)

- Afar QuestionsDocument16 pagesAfar QuestionsJessarene Fauni Depante50% (18)

- Questions SsDocument7 pagesQuestions SsAngelli Lamique100% (2)

- AFAR Questions With AnswersDocument11 pagesAFAR Questions With AnswersAngelica CerioNo ratings yet

- OrDocument10 pagesOrasdf100% (1)

- LTCC and Franchise Long Exam PDFDocument9 pagesLTCC and Franchise Long Exam PDFChristine Joy Original50% (2)

- ACC110 P3Quiz2 AnswersDocument12 pagesACC110 P3Quiz2 AnswersTricia Mae FernandezNo ratings yet

- Chapter 10 - Teacher's Manual - Afar Part 1Document20 pagesChapter 10 - Teacher's Manual - Afar Part 1Angelic67% (3)

- Buss. Combi PrelimDocument8 pagesBuss. Combi PrelimPhia TeoNo ratings yet

- Module 8 - Home Office, Branch and Agency AccountingDocument8 pagesModule 8 - Home Office, Branch and Agency AccountingSunshine Khuletz67% (3)

- Chapter 11 - Home Agency, Branch and Agency AccountingDocument14 pagesChapter 11 - Home Agency, Branch and Agency Accountingmonica ocureza100% (1)

- This Study Resource WasDocument3 pagesThis Study Resource WasQueeny Mae Cantre ReutaNo ratings yet

- Consolidated Financial Statements: XYZ, Inc. Carrying Amounts Fair Values Fair Value Adjustments (FVA)Document3 pagesConsolidated Financial Statements: XYZ, Inc. Carrying Amounts Fair Values Fair Value Adjustments (FVA)mhar lon100% (2)

- QUIZ - CHAPTER 8 - ACCOUNTING FOR FRANCHISE OPERATIONS FRANCHISOR NoaDocument3 pagesQUIZ - CHAPTER 8 - ACCOUNTING FOR FRANCHISE OPERATIONS FRANCHISOR NoaNeirish fainsan43% (7)

- Joint Arrangement Quiz AnswersDocument7 pagesJoint Arrangement Quiz AnswersAlexandrite100% (1)

- Excercises On Branch and Home Office Chapter TwoDocument3 pagesExcercises On Branch and Home Office Chapter Twoሔርሞን ይድነቃቸው50% (4)

- Entendiendo El Estado de ResultadoDocument105 pagesEntendiendo El Estado de ResultadodidioserNo ratings yet

- MODULE 3 - Installment SalesDocument8 pagesMODULE 3 - Installment SalesEdison Salgado Castigador50% (2)

- ACC110 P3Quiz2 AnswersDocument12 pagesACC110 P3Quiz2 AnswersTricia Mae FernandezNo ratings yet

- Home Office and Branch AccountingDocument5 pagesHome Office and Branch AccountingMaryjoy Sarzadilla JuanataNo ratings yet

- Activity 1Document4 pagesActivity 1Fernando III PerezNo ratings yet

- p1 Quiz With TheoryDocument15 pagesp1 Quiz With TheoryGrace CorpoNo ratings yet

- PDF Valle Quiz ABC CompressDocument6 pagesPDF Valle Quiz ABC CompressPotie RhymeszNo ratings yet

- Chapter 9 Teachers Manual Afar Part 1Document9 pagesChapter 9 Teachers Manual Afar Part 1Aimee Diaz100% (3)

- Notes For Advanced AccountingDocument5 pagesNotes For Advanced AccountingSoleil Sierra0% (1)

- Name: Date: Professor: Section: Score: Assynchronous Activity-Final TermDocument14 pagesName: Date: Professor: Section: Score: Assynchronous Activity-Final TermkmarisseeNo ratings yet

- LTCCDocument7 pagesLTCCgenevieve sicatNo ratings yet

- 07 Installment SalesDocument1 page07 Installment SalesGem Yiel33% (3)

- 13 Business Combination Pt3Document1 page13 Business Combination Pt3Riselle Ann Sanchez50% (2)

- Home Office, Branch and Agency Accounting: Problem 11-1: True or FalseDocument13 pagesHome Office, Branch and Agency Accounting: Problem 11-1: True or FalseVenz Lacre100% (1)

- LTCCDocument7 pagesLTCCGenesis Dizon67% (6)

- AFAR - Revenue Recognition 2019Document4 pagesAFAR - Revenue Recognition 2019Joanna Rose DeciarNo ratings yet

- Sample ProblemsDocument3 pagesSample ProblemsGracias100% (1)

- Buss. Combi PrelimDocument8 pagesBuss. Combi PrelimPhia TeoNo ratings yet

- Special Tansaction Quiz 1 and 2Document4 pagesSpecial Tansaction Quiz 1 and 2Helen Fiedalan Falcutila MondiaNo ratings yet

- Enabling Assessment: (Note: Several Ted Suavillo Cases)Document2 pagesEnabling Assessment: (Note: Several Ted Suavillo Cases)Von Andrei MedinaNo ratings yet

- Chapter 7 Accounting For Franchise Operations FranchisorDocument15 pagesChapter 7 Accounting For Franchise Operations FranchisorKaren BalibalosNo ratings yet

- Business Combination ExerciseDocument5 pagesBusiness Combination Exercise수지No ratings yet

- Accounting ResearchDocument28 pagesAccounting ResearchRhanel Joy Cayube100% (2)

- FL AfarDocument20 pagesFL AfarKenneth Robledo50% (2)

- Corporate Liquidation Quiz 5docxDocument5 pagesCorporate Liquidation Quiz 5docxAngelica Duarte33% (6)

- AFAR - Installment, Customer, ConsignmentDocument3 pagesAFAR - Installment, Customer, ConsignmentJoanna Rose DeciarNo ratings yet

- Chapter 4 Teachers Manual Afar Part 1Document13 pagesChapter 4 Teachers Manual Afar Part 1cezyyyyyyNo ratings yet

- Afar1-Exercises 2Document17 pagesAfar1-Exercises 2aleachon100% (1)

- Activity-Chapter 7: Ans. None of These SolutionDocument1 pageActivity-Chapter 7: Ans. None of These SolutionRandelle James FiestaNo ratings yet

- Ast - 3B - Quiz No. 1Document10 pagesAst - 3B - Quiz No. 1Renalyn Paras0% (1)

- Illustration Problem & SolutionDocument4 pagesIllustration Problem & SolutionClauie BarsNo ratings yet

- Cebu Institute of Technology - University: Use The Following Information For The Next Two QuestionsDocument13 pagesCebu Institute of Technology - University: Use The Following Information For The Next Two QuestionsPrima Facie50% (2)

- AuditingDocument14 pagesAuditingedrick LouiseNo ratings yet

- Chapter 7 - Teacher's Manual - Afar Part 1Document24 pagesChapter 7 - Teacher's Manual - Afar Part 1Angelic100% (3)

- Grace-AST Module 10Document5 pagesGrace-AST Module 10Devine Grace A. MaghinayNo ratings yet

- Consignment Sales: Name: Date: Professor: Section: Score: QuizDocument3 pagesConsignment Sales: Name: Date: Professor: Section: Score: QuizAndrea Florence Guy VidalNo ratings yet

- Prelim Exam - Doc2Document16 pagesPrelim Exam - Doc2alellie100% (1)

- Quiz 2 Joint ArrangementsDocument4 pagesQuiz 2 Joint ArrangementsJane Gavino100% (2)

- Chapter 10 SolMan Special Accounting 1 Millan 2018Document20 pagesChapter 10 SolMan Special Accounting 1 Millan 2018Alvin Jheii Sioco Alfonso100% (1)

- HO, B & A AcctgDocument15 pagesHO, B & A AcctgCarolina Fortez Dacanay71% (7)

- Construction IllustrationDocument54 pagesConstruction IllustrationCatherine Joy Vasaya100% (3)

- ExerciseDocument4 pagesExerciseMae RxNo ratings yet

- Home and Branch Part 1Document4 pagesHome and Branch Part 1Jessica Libunao100% (1)

- Quiz#3 CompleteDocument2 pagesQuiz#3 CompleteGio SantosNo ratings yet

- Agency and Branch Accounting - General Procedures - v.2.0Document3 pagesAgency and Branch Accounting - General Procedures - v.2.0Catherine SelladoNo ratings yet

- Branches and Agencies - OdtDocument9 pagesBranches and Agencies - OdtEunice BernalNo ratings yet

- Home Office and Branch AccountingDocument4 pagesHome Office and Branch AccountingMaurice AgbayaniNo ratings yet

- LUCHANA Narrative ExperienceDocument2 pagesLUCHANA Narrative ExperienceAllecks Juel LuchanaNo ratings yet

- IRC 1 - P1 Final Exam (Second Sem 2013 - 2014)Document13 pagesIRC 1 - P1 Final Exam (Second Sem 2013 - 2014)Allecks Juel LuchanaNo ratings yet

- Act3 StatDocument33 pagesAct3 StatAllecks Juel Luchana0% (1)

- Himarios Company Worksheet To Prepare Financial Statements DECEMBER 31, 20X9Document3 pagesHimarios Company Worksheet To Prepare Financial Statements DECEMBER 31, 20X9Allecks Juel LuchanaNo ratings yet

- Amber Nestor Art Gallery Trial Balance As of December 31, 20X4Document10 pagesAmber Nestor Art Gallery Trial Balance As of December 31, 20X4Allecks Juel LuchanaNo ratings yet

- Auditing in A Cis EnvironmentDocument23 pagesAuditing in A Cis EnvironmentAllecks Juel LuchanaNo ratings yet

- Unit Summary D-7&8Document5 pagesUnit Summary D-7&8Allecks Juel LuchanaNo ratings yet

- RPH First Cry of Phil RevDocument6 pagesRPH First Cry of Phil RevAllecks Juel LuchanaNo ratings yet

- RPH SourcesDocument2 pagesRPH SourcesAllecks Juel LuchanaNo ratings yet

- Luchana, A. - Cbmec Case Study 2 (Chapter 4)Document5 pagesLuchana, A. - Cbmec Case Study 2 (Chapter 4)Allecks Juel LuchanaNo ratings yet

- Cbmec QuizDocument2 pagesCbmec QuizAllecks Juel LuchanaNo ratings yet

- Cbmec FinalDocument9 pagesCbmec FinalAllecks Juel LuchanaNo ratings yet

- ACC 110 - Day 19 - 20 - SASDocument15 pagesACC 110 - Day 19 - 20 - SASFeedback Or BawiNo ratings yet

- Installment SalesDocument14 pagesInstallment SalesAlexandriteNo ratings yet

- AFAR Review Midterm ExamDocument10 pagesAFAR Review Midterm ExamZyrah Mae SaezNo ratings yet

- Installment and LTCCDocument9 pagesInstallment and LTCCAngelica RubiosNo ratings yet

- Summary Notes Installment Sales and Consignment SalesDocument11 pagesSummary Notes Installment Sales and Consignment SalesJaycel OngyNo ratings yet

- Welcome Aboard 3 Year Bsa!!Document61 pagesWelcome Aboard 3 Year Bsa!!Riza Mae AlceNo ratings yet

- Installment Sales ConceptsDocument61 pagesInstallment Sales ConceptsRanne BalanaNo ratings yet

- IFRS 15 & Installment Sales - QUIZDocument5 pagesIFRS 15 & Installment Sales - QUIZArieza MontañoNo ratings yet

- Template - Acctg. Major 3 Module 5 PDFDocument16 pagesTemplate - Acctg. Major 3 Module 5 PDFRia Mendez100% (2)

- Module 7 InstallmentDocument12 pagesModule 7 InstallmentNiki DimaanoNo ratings yet

- Chapter 09Document16 pagesChapter 09FireBNo ratings yet

- Acct 557 Week 1 HomeworkDocument16 pagesAcct 557 Week 1 HomeworkMichelle Porter-Price0% (1)

- 2 - FSA1 Handout (Topic 3) - Standard&incomeDocument73 pages2 - FSA1 Handout (Topic 3) - Standard&incomeGuyu PanNo ratings yet

- Solution Manual Chapter 9Document16 pagesSolution Manual Chapter 9Shealalyn1100% (2)

- Solution Chapter 9Document15 pagesSolution Chapter 9BobslaneLlenos0% (2)

- Accsptr - ReviewerDocument10 pagesAccsptr - ReviewerDanna VargasNo ratings yet

- Installment Sales Multiple QuestionsDocument36 pagesInstallment Sales Multiple QuestionsTrixie CapisosNo ratings yet

- Installment Sales AccountingDocument9 pagesInstallment Sales AccountingCillian ReevesNo ratings yet

- Loss On Repossession 3,800Document2 pagesLoss On Repossession 3,800Future CPANo ratings yet

- Installment Sales Method Cost Recovery Method (Traditional)Document23 pagesInstallment Sales Method Cost Recovery Method (Traditional)yhygyugNo ratings yet

- Advanced-Accounting-Part 1-Dayag-2015-Chapter-9Document19 pagesAdvanced-Accounting-Part 1-Dayag-2015-Chapter-9trisha sacramento100% (4)

- Installment Sales-: Loss On Repossession XXX Gain On Repossession XXXDocument5 pagesInstallment Sales-: Loss On Repossession XXX Gain On Repossession XXXJoyce Ann Agdippa BarcelonaNo ratings yet

- Accounting For Special Transaction Final ReviewerDocument73 pagesAccounting For Special Transaction Final ReviewerLunaNo ratings yet

- Illustration Problem & SolutionDocument4 pagesIllustration Problem & SolutionClauie BarsNo ratings yet

- Advacc1 Installment SalesDocument21 pagesAdvacc1 Installment SalesAlex OngNo ratings yet

- Advance Chapter 3Document12 pagesAdvance Chapter 3abel habtamuNo ratings yet

- Topic 2 Installment Sales Module Part 1Document5 pagesTopic 2 Installment Sales Module Part 1Maricel Ann BaccayNo ratings yet