Download as docx, pdf, or txt

You might also like

- Payment Due Dates - Billing & Payments - CricketDocument9 pagesPayment Due Dates - Billing & Payments - CricketJohn Michael AntonioNo ratings yet

- Working Capital Management Exercise 3Document2 pagesWorking Capital Management Exercise 3Nikki San GabrielNo ratings yet

- S.No. Period of Delay Rate of Simple Interest Per AnnumDocument1 pageS.No. Period of Delay Rate of Simple Interest Per AnnumOmkar MauryaNo ratings yet

- Important T&CsDocument18 pagesImportant T&CsKrishna KishoreNo ratings yet

- 00001914-Payment Term ScenarioDocument6 pages00001914-Payment Term Scenariobikash dasNo ratings yet

- Mitc 8271022000045Document6 pagesMitc 8271022000045Kumar KumarNo ratings yet

- IMP TDS Return Due Dates For FY 2023-24 - Penalty ForDocument5 pagesIMP TDS Return Due Dates For FY 2023-24 - Penalty Forsukantabera215No ratings yet

- Mitc For Amazon Pay Credit CardDocument7 pagesMitc For Amazon Pay Credit CardBlain Santhosh FernandesNo ratings yet

- Demand & Recovery and Offences & PenaltiesDocument8 pagesDemand & Recovery and Offences & PenaltiesKedarnath GajewarNo ratings yet

- Sosc Ver 210313Document3 pagesSosc Ver 210313Shashank AgarwalNo ratings yet

- Federal Budget: June 2012Document2 pagesFederal Budget: June 2012api-140871676No ratings yet

- Tax Deducted at SourceDocument5 pagesTax Deducted at SourceRajinder KaurNo ratings yet

- Explanation of The Medical Tax CreditsDocument2 pagesExplanation of The Medical Tax CreditspttaNo ratings yet

- How 2 Fillforn 280Document6 pagesHow 2 Fillforn 280anon_639359071No ratings yet

- It's Time To Estimate Advance TaxDocument4 pagesIt's Time To Estimate Advance TaxRavi KtNo ratings yet

- EY-Indonesia Tax Insight 20012013Document6 pagesEY-Indonesia Tax Insight 20012013davidwijaya1986No ratings yet

- CA. Pavan GoyalDocument15 pagesCA. Pavan Goyalshruti2024No ratings yet

- English MITC PDFDocument15 pagesEnglish MITC PDFAmit ShuklaNo ratings yet

- TF Case StudyDocument11 pagesTF Case StudyNavin ChoudharyNo ratings yet

- FK Reward System Revision TNCDocument4 pagesFK Reward System Revision TNCvarunchopNo ratings yet

- TAX REFORM: Local Sales Tax Proposal: Counties and Transit Authorities: Revenue Will GrowDocument4 pagesTAX REFORM: Local Sales Tax Proposal: Counties and Transit Authorities: Revenue Will GrowTimNo ratings yet

- Federal Inland Revenue Service: Information CircularDocument10 pagesFederal Inland Revenue Service: Information CircularJesseNo ratings yet

- Intcert - 20220927 - 01 04 2021 31 03 2022 - 35138734Document2 pagesIntcert - 20220927 - 01 04 2021 31 03 2022 - 35138734Mohan KumarNo ratings yet

- Citibank - CREDITCARD CONDITIONSDocument8 pagesCitibank - CREDITCARD CONDITIONSkrishna_1238No ratings yet

- Tax Calender: San Corporate Advisors PVT LTD in Association With A N GAWADE & CO, Chartered AccountantsDocument6 pagesTax Calender: San Corporate Advisors PVT LTD in Association With A N GAWADE & CO, Chartered AccountantsvruaklNo ratings yet

- GST Payments - GST Refund Online & OfflineDocument6 pagesGST Payments - GST Refund Online & Offlineajayprajapti828No ratings yet

- 27 Useful Charts of Service Tax 2016 17 PDFDocument24 pages27 Useful Charts of Service Tax 2016 17 PDFJosef AnthonyNo ratings yet

- Perpajakan Nomor 1Document14 pagesPerpajakan Nomor 1jarilegendarisNo ratings yet

- TCS On Sales of GoodsDocument11 pagesTCS On Sales of GoodsAnsari NaeemuddinNo ratings yet

- Tax Management: Assignment-1Document6 pagesTax Management: Assignment-1Rida ZahidNo ratings yet

- Tax Alert Buletin Fiscal: No. 4 January 2013 Nr. 4 Ianuarie 2013Document6 pagesTax Alert Buletin Fiscal: No. 4 January 2013 Nr. 4 Ianuarie 2013ponorelNo ratings yet

- R13 - 07.09.20 PDFDocument42 pagesR13 - 07.09.20 PDFअहा मधुमक्खीपालनNo ratings yet

- How To Convert Black Money in White Money??Document7 pagesHow To Convert Black Money in White Money??Yani UlyNo ratings yet

- Should You Choose Cash or Accruals Accounting?: Your Farm Business and The GST - A Detailed GuideDocument10 pagesShould You Choose Cash or Accruals Accounting?: Your Farm Business and The GST - A Detailed GuidePrince McGershonNo ratings yet

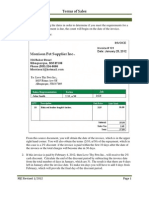

- Terms of SaleDocument6 pagesTerms of SaleMary100% (1)

- Advance Tax PaymentDocument4 pagesAdvance Tax PaymentJaneesNo ratings yet

- 1.filing Tax For 2020 - PostDocument2 pages1.filing Tax For 2020 - PostShahu PawarNo ratings yet

- IDBI Bank MITC ConditionsDocument14 pagesIDBI Bank MITC Conditionswestm4248No ratings yet

- Premium Paid Certificate: Date: 09-JAN-2014Document2 pagesPremium Paid Certificate: Date: 09-JAN-2014kumber_singh5069No ratings yet

- BudgetDocument21 pagesBudgetshweta_narkhede01No ratings yet

- Cps ClarificationDocument4 pagesCps ClarificationgcrajasekaranNo ratings yet

- Tax - Questio AnswersDocument7 pagesTax - Questio AnswersAnamika VatsaNo ratings yet

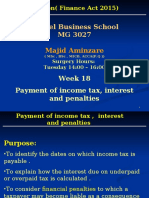

- MG 3027 TAXATION - Week 18 Payment of Income Tax, Interest and PenaltiesDocument27 pagesMG 3027 TAXATION - Week 18 Payment of Income Tax, Interest and PenaltiesSyed SafdarNo ratings yet

- Mitc For Amazon Pay Credit CardDocument7 pagesMitc For Amazon Pay Credit Cardsomeonestupid19690% (1)

- When To File GST ReturnsDocument4 pagesWhen To File GST ReturnsNikita BaliNo ratings yet

- Employment Income TaxDocument10 pagesEmployment Income TaxHarsh Nahar100% (1)

- Communique: Information To EmployersDocument1 pageCommunique: Information To EmployersVassen MootooNo ratings yet

- Citibank Credit CardDocument6 pagesCitibank Credit CardgjvoraNo ratings yet

- DTC 2012 ProjectDocument10 pagesDTC 2012 ProjectSandeep SharmaNo ratings yet

- The Need For GSTDocument6 pagesThe Need For GSTrvanithakumarNo ratings yet

- S 234A, 234B and 234CDocument5 pagesS 234A, 234B and 234CMahaveer DhelariyaNo ratings yet

- TDS PresentationDocument16 pagesTDS Presentationgamers SatisfactionNo ratings yet

- Direct and Indirect TaxesDocument47 pagesDirect and Indirect TaxesThomasGetye67% (3)

- FAQs - IncomeTaxRegime - FY23-24 Tax RegimeDocument8 pagesFAQs - IncomeTaxRegime - FY23-24 Tax RegimeGokul KrishNo ratings yet

- Remittance Tax Guide: MIRA R833Document14 pagesRemittance Tax Guide: MIRA R833SODDEYNo ratings yet

- Citi Rewards Domestic MITC FinalDocument8 pagesCiti Rewards Domestic MITC FinalGauravkNo ratings yet

- MSD 2012 48 enDocument2 pagesMSD 2012 48 enAnushka AbeysingheNo ratings yet

- Unit 5 TaxDocument15 pagesUnit 5 TaxVijay GiriNo ratings yet

- Invoicing Under GSTDocument5 pagesInvoicing Under GSTpuru1292No ratings yet

- c2 Fundamentals in Lodging OperationsDocument10 pagesc2 Fundamentals in Lodging OperationsJUN GERONANo ratings yet

- Nonprofit Executive Director ResumeDocument6 pagesNonprofit Executive Director Resumef5dpebax100% (2)

- Impact of The Iberian Overseas ExpansionDocument3 pagesImpact of The Iberian Overseas ExpansionNavisha BaidNo ratings yet

- Audit of Receivables PSPDocument6 pagesAudit of Receivables PSPMarriel Fate CullanoNo ratings yet

- Wintershall DeaDocument11 pagesWintershall Dearadoslav micicNo ratings yet

- Receipt - Booking - Ems 2Document2 pagesReceipt - Booking - Ems 2Zabar RudinNo ratings yet

- Term Report On One Potato Two PotatoDocument20 pagesTerm Report On One Potato Two Potatojawwadakhtar100% (4)

- Qualified Contestable Customers - April 2021 DataDocument61 pagesQualified Contestable Customers - April 2021 DataelsanpedroiiNo ratings yet

- Soce2023bskeforms Form2Document1 pageSoce2023bskeforms Form2lavariasmarjorieanne211100% (2)

- International Marketing PlanDocument4 pagesInternational Marketing PlanUsaiwevhu McmillanNo ratings yet

- 5CI022 Task 02 (2057112)Document8 pages5CI022 Task 02 (2057112)Dulmi MendisNo ratings yet

- Training Calendar 2024Document28 pagesTraining Calendar 2024Puteri Allysa rosliNo ratings yet

- Concept Notes On Uganda Network of Businesses (Unb) 1.0Document6 pagesConcept Notes On Uganda Network of Businesses (Unb) 1.0SundayNo ratings yet

- Blades Plc. Case I: Decision To Expand InternationallyDocument4 pagesBlades Plc. Case I: Decision To Expand InternationallyАлинаNo ratings yet

- Formal& Informal InstitutionsDocument7 pagesFormal& Informal InstitutionsKaif KhanNo ratings yet

- Interview Questions of Production PlanningDocument7 pagesInterview Questions of Production PlanningPriyank Patel0% (1)

- Profiles: Prospects For Coal and Clean Coal Technologies in IndonesiaDocument2 pagesProfiles: Prospects For Coal and Clean Coal Technologies in IndonesiayansenbarusNo ratings yet

- 4.1.data Analysis & Findings: Print Vs Digital Media Print in IndiaDocument16 pages4.1.data Analysis & Findings: Print Vs Digital Media Print in IndiaSidNo ratings yet

- E-Payslip Admin. - 1561198Document2 pagesE-Payslip Admin. - 1561198xkr5f7wyt2No ratings yet

- Business Communication Process and Product Brief Canadian Canadian 4th Edition Guffey Test BankDocument26 pagesBusiness Communication Process and Product Brief Canadian Canadian 4th Edition Guffey Test BankJenniferLeexdte100% (59)

- Bill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total AmountDocument1 pageBill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total AmountSHAIK AJEESNo ratings yet

- The Impact of Supply Chain Management Practices On Performance of OrganizationDocument10 pagesThe Impact of Supply Chain Management Practices On Performance of OrganizationSmart TirmiziNo ratings yet

- All About BpoDocument10 pagesAll About BpoLadimer SabidaNo ratings yet

- 2018 - Kuldeep Bishnoi - NLU NagpurDocument2 pages2018 - Kuldeep Bishnoi - NLU NagpurLife Hacks Stunt PerfectNo ratings yet

- Duka - LectureDocument5 pagesDuka - LectureNicole Blanche BorcesNo ratings yet

- Shop Leave and License AgreementDocument4 pagesShop Leave and License AgreementDonald Gonsalves60% (10)

- Finance For Everyone Assignment 2 ROHAN 1099Document10 pagesFinance For Everyone Assignment 2 ROHAN 1099NathoNo ratings yet

- Sdnlist PDFDocument2,088 pagesSdnlist PDFInducciones SACSANo ratings yet

- Ladder Risk AssessmentDocument3 pagesLadder Risk AssessmentPearl TeresaNo ratings yet