Download as pdf or txt

You might also like

- Performance Management: Time Allowed 3 HoursDocument9 pagesPerformance Management: Time Allowed 3 HourschimbanguraNo ratings yet

- Problems: 2-58. Cost ConceptsDocument16 pagesProblems: 2-58. Cost ConceptsChristy HabelNo ratings yet

- Cortez Practice Set JanuaryDocument5 pagesCortez Practice Set JanuaryChristian LapidNo ratings yet

- Job Order Costing TheoryDocument3 pagesJob Order Costing TheoryMiscaCruzNo ratings yet

- P2 09Document8 pagesP2 09Mark Levi CorpuzNo ratings yet

- For DiscussionDocument41 pagesFor DiscussionKianah Shanelle MAGNAYENo ratings yet

- Chapter 3 Material Procurement, Use and ControlDocument3 pagesChapter 3 Material Procurement, Use and ControlKaren CaelNo ratings yet

- Garcia, Phoebe Stephane C. Cost Accounting BS Accountancy 1-A CHAPTER 10: Process Costing True or FalseDocument26 pagesGarcia, Phoebe Stephane C. Cost Accounting BS Accountancy 1-A CHAPTER 10: Process Costing True or FalsePeabeeNo ratings yet

- Cost Mock Compre With AnsDocument15 pagesCost Mock Compre With Anssky dela cruzNo ratings yet

- Abc StratDocument8 pagesAbc StratapremsNo ratings yet

- Chapter 8 Acctng For FOHDocument3 pagesChapter 8 Acctng For FOHGwyneth Hannah Sator RupacNo ratings yet

- This Study Resource Was: Award: 1.00 PointDocument2 pagesThis Study Resource Was: Award: 1.00 PointAaron Jan FelicildaNo ratings yet

- C13 Standard CostingDocument12 pagesC13 Standard CostingPaula BautistaNo ratings yet

- Process Costing - FIFODocument5 pagesProcess Costing - FIFODerick FigueroaNo ratings yet

- 2.1.1 Assignment - Cost According To Cost Behavior - Answers and SolutionsDocument7 pages2.1.1 Assignment - Cost According To Cost Behavior - Answers and SolutionsRoselyn LumbaoNo ratings yet

- Cost AccountingDocument4 pagesCost AccountingRoselyn LumbaoNo ratings yet

- Practical AccountingDocument25 pagesPractical AccountingWed CornelNo ratings yet

- Cost of Production Report Sample Problem:: SolutionDocument2 pagesCost of Production Report Sample Problem:: SolutionDaryl Joeh SagabaenNo ratings yet

- COST ACCTG Semi Final Exam 2020Document9 pagesCOST ACCTG Semi Final Exam 2020TyrsonNo ratings yet

- Strategic Cost Management Exercises 12369Document2 pagesStrategic Cost Management Exercises 12369Arlene Diane OrozcoNo ratings yet

- Cost Accounting QuestionsDocument14 pagesCost Accounting QuestionsMhico MateoNo ratings yet

- Cost ReviewerDocument130 pagesCost ReviewerMarjorie Nepomuceno100% (1)

- Bsa 2103-Cost Accounting and Control Midterm Departmental Exam Reviewer Multiple ChoiceDocument17 pagesBsa 2103-Cost Accounting and Control Midterm Departmental Exam Reviewer Multiple ChoiceFerb CruzadaNo ratings yet

- Cost Chapter 15 (1-13)Document5 pagesCost Chapter 15 (1-13)Ericka Hazel Osorio0% (1)

- Irish CorporationDocument3 pagesIrish CorporationAngeline RamirezNo ratings yet

- Job Order CostingDocument10 pagesJob Order CostingGennelyn Grace Penaredondo100% (1)

- Chapter 15Document10 pagesChapter 15Jess SiazonNo ratings yet

- Cost Accounting Cycle (Multiple Choice)Document3 pagesCost Accounting Cycle (Multiple Choice)Rosselle Manoriña100% (1)

- 2nd Grading Exams Key AnswersDocument19 pages2nd Grading Exams Key AnswersUnknown WandererNo ratings yet

- Activity 5 Accounting For Overhead: Problem 1Document3 pagesActivity 5 Accounting For Overhead: Problem 1itik meowmeowNo ratings yet

- 06 Process CostingDocument16 pages06 Process CostingChristian Blanza LlevaNo ratings yet

- Notes Receivable - Ia 1Document4 pagesNotes Receivable - Ia 1Aldrin CabangbangNo ratings yet

- Finals - QuizzesDocument10 pagesFinals - QuizzesXyne FernandezNo ratings yet

- Comprehensive Exam in Cost Accounting and Control 2022Document8 pagesComprehensive Exam in Cost Accounting and Control 2022Maui EquizaNo ratings yet

- Answer Q1 Job Order CostingDocument5 pagesAnswer Q1 Job Order CostingDiane Cris Duque100% (1)

- 8.1 Cost HWDocument3 pages8.1 Cost HWJune Maylyn MarzoNo ratings yet

- Discussion of Assignment - Just in Time and Backflush CostingDocument4 pagesDiscussion of Assignment - Just in Time and Backflush CostingRoselyn Lumbao100% (1)

- Investments AssignmentDocument3 pagesInvestments AssignmentKhai Supleo PabelicoNo ratings yet

- Finished Goods Inventory: Exercise 1-1 (True or False)Document16 pagesFinished Goods Inventory: Exercise 1-1 (True or False)Isaiah BatucanNo ratings yet

- Accounting For Labor ProblemsDocument2 pagesAccounting For Labor ProblemsRyan Maliwat0% (1)

- Q3 Part 2 Problem On Job Order CostingDocument9 pagesQ3 Part 2 Problem On Job Order CostingLadybellereyann A TeguihanonNo ratings yet

- Joint Products and By-Products: de Leon/ de Leon/ de LeonDocument17 pagesJoint Products and By-Products: de Leon/ de Leon/ de LeonMay Grethel Joy PeranteNo ratings yet

- Cost Accounting Chapter 10Document66 pagesCost Accounting Chapter 10Reshyl HicaleNo ratings yet

- Cost Accounting ProblemsDocument3 pagesCost Accounting ProblemsRowena TamboongNo ratings yet

- Operational and Financial Budgeting: Multiple ChoiceDocument16 pagesOperational and Financial Budgeting: Multiple ChoiceNaddieNo ratings yet

- The University of Manila College of Business Administration and Accountacy Integrated CPA Review and Refresher Program Pre-Final Examination AE 16Document5 pagesThe University of Manila College of Business Administration and Accountacy Integrated CPA Review and Refresher Program Pre-Final Examination AE 16ana rosemarie enaoNo ratings yet

- Reviewer+ +Midterm+ExaminationCOSTDocument7 pagesReviewer+ +Midterm+ExaminationCOSTMelka BelmonteNo ratings yet

- Preliminary Examination MC (Q)Document9 pagesPreliminary Examination MC (Q)Vanessa HaliliNo ratings yet

- Afar CostDocument9 pagesAfar CostDiana Faye CaduadaNo ratings yet

- DocDocument6 pagesDocBanana QNo ratings yet

- Simulated Midterm Exam - Cost Accounting PDFDocument13 pagesSimulated Midterm Exam - Cost Accounting PDFMarcus MonocayNo ratings yet

- Test Bank For Cornerstones of Cost Management 2nd Edition by Hansen PDFDocument23 pagesTest Bank For Cornerstones of Cost Management 2nd Edition by Hansen PDFJyasmine Aura V. AgustinNo ratings yet

- AE 22 M TEST 3 With AnswersDocument6 pagesAE 22 M TEST 3 With AnswersJerome MonserratNo ratings yet

- MidtermS2 InventoriesDocument11 pagesMidtermS2 InventoriesQueenie Dayagro0% (2)

- Standard Costing - Answer KeyDocument6 pagesStandard Costing - Answer KeyRoselyn LumbaoNo ratings yet

- BACOSTMX Module 3 Self-ReviewerDocument5 pagesBACOSTMX Module 3 Self-ReviewerlcNo ratings yet

- Module 9 Part 3 - Joint Cost and By-Products Sample ProblemsDocument28 pagesModule 9 Part 3 - Joint Cost and By-Products Sample ProblemsMarjorie NepomucenoNo ratings yet

- Acmas 2137 Final SADocument5 pagesAcmas 2137 Final SAkakaoNo ratings yet

- Job Order Costing HandoutsDocument8 pagesJob Order Costing HandoutsHannah Jane Arevalo LafuenteNo ratings yet

- Pinnacle First Preboards May 2023 SECUREDDocument109 pagesPinnacle First Preboards May 2023 SECUREDhotdoughhuhuhuNo ratings yet

- Acctg11B Quiz 2Document5 pagesAcctg11B Quiz 2faithfagalasNo ratings yet

- Product Pricing Strategy and Costing Template For Food RecipesDocument3 pagesProduct Pricing Strategy and Costing Template For Food RecipesKïtëł GägüïNo ratings yet

- CHAPTER 5 Cost Analysis and Pricing DecisionsDocument47 pagesCHAPTER 5 Cost Analysis and Pricing DecisionsTewodros TafereNo ratings yet

- Costacc HWDocument2 pagesCostacc HWRikka Takanashi100% (1)

- Test Bank For Managerial Accounting 16th Edition Garrison Noreen Brewer 1260153134 9781260153132Document36 pagesTest Bank For Managerial Accounting 16th Edition Garrison Noreen Brewer 1260153134 9781260153132jordanwyattgiosqackyn100% (25)

- Schedule of Cost of Goods Manufactured V13Document10 pagesSchedule of Cost of Goods Manufactured V13bagirNo ratings yet

- Introduction To Cost Accounting PDFDocument262 pagesIntroduction To Cost Accounting PDFFahmida AkhterNo ratings yet

- ch04 SM RankinDocument23 pagesch04 SM RankinSTU DOC100% (2)

- Customs Valuation RulesDocument16 pagesCustoms Valuation RulespramodpadhyeNo ratings yet

- Adv - IT Project Cost - FinalDocument10 pagesAdv - IT Project Cost - FinalAdamNo ratings yet

- Design Build Proposal FormDocument10 pagesDesign Build Proposal FormLouie MirandaNo ratings yet

- Presentation On MCSDocument20 pagesPresentation On MCSMAHENDRA SHIVAJI DHENAKNo ratings yet

- Module No. 2 Construction ContractsDocument18 pagesModule No. 2 Construction ContractsPrincess SagreNo ratings yet

- Educational Material On Ind AS 115Document15 pagesEducational Material On Ind AS 115IJAZ AHAMED S 2212053No ratings yet

- Dwnload Full Accounting Understanding and Practice 4th Edition Leiwy Test Bank PDFDocument35 pagesDwnload Full Accounting Understanding and Practice 4th Edition Leiwy Test Bank PDFsynomocyeducable6pyb8k100% (23)

- Chapter 2 - Investment Property (MFRS 140)Document35 pagesChapter 2 - Investment Property (MFRS 140)SITI NUR WARDINA WAFI ROMLINo ratings yet

- CORMINAL - 06 Activity 01Document1 pageCORMINAL - 06 Activity 01Betchang AquinoNo ratings yet

- CA in 5873 of 2019 GreenfieldDocument60 pagesCA in 5873 of 2019 GreenfieldGurdev SinghNo ratings yet

- BS 6143-1 - 1992 Guide To The Economics of Quality - Part 1 Process Cost Model PDFDocument22 pagesBS 6143-1 - 1992 Guide To The Economics of Quality - Part 1 Process Cost Model PDFVCNo ratings yet

- Financial Accounting and Analysis MaterialDocument132 pagesFinancial Accounting and Analysis MaterialkarthikreddyNo ratings yet

- THEORY26PROBLEMSDocument10 pagesTHEORY26PROBLEMSIryne Kim PalatanNo ratings yet

- 40 Facilities Location and SupportDocument54 pages40 Facilities Location and Supportwisang residataNo ratings yet

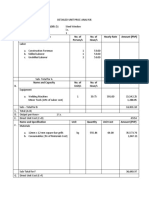

- DETAILED UNIT PRICE ANALYSIS CadDocument7 pagesDETAILED UNIT PRICE ANALYSIS CadIan Kirby RedondoNo ratings yet

- P KumaresanDocument13 pagesP KumaresanJohn Luis Nebreja Ferrera100% (1)

- Solution Far560 - Jul 2017Document8 pagesSolution Far560 - Jul 2017MUHAMAD MUKHAIRI MUHAMAD HANIFAHNo ratings yet

- Standard Costing and Flexible Budget 10Document5 pagesStandard Costing and Flexible Budget 10Lhorene Hope DueñasNo ratings yet

- TSCM52 65Document17 pagesTSCM52 65Chirag SolankiNo ratings yet

- Ma-Module 1 Organizational Planning N BudgetingDocument45 pagesMa-Module 1 Organizational Planning N BudgetingTaaraniyaal Thirumurugu ArivanandanNo ratings yet

- TAX PROJECT - doSAIDOJASOIJDOINASDcxDocument25 pagesTAX PROJECT - doSAIDOJASOIJDOINASDcxadarsh kumarNo ratings yet

- MSC PSCM SOB Mayani, Stephen 2019Document112 pagesMSC PSCM SOB Mayani, Stephen 2019Ismail A IsmailNo ratings yet