Unit 2 Journal Posting Trans

Unit 2 Journal Posting Trans

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5822)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Human Resource Management: The Key FunctionsDocument10 pagesHuman Resource Management: The Key FunctionsVirginia TownzenNo ratings yet

- Normal Balances in Accounting Video TranscriptDocument2 pagesNormal Balances in Accounting Video TranscriptVirginia TownzenNo ratings yet

- November 2019 Transactions: Date Account Titles and Explanations Debit CreditDocument5 pagesNovember 2019 Transactions: Date Account Titles and Explanations Debit CreditVirginia TownzenNo ratings yet

- Unit 8 Article Review SubmitDocument4 pagesUnit 8 Article Review SubmitVirginia TownzenNo ratings yet

- Chapter 2 Accounting Principles 2-20 To 2-29Document17 pagesChapter 2 Accounting Principles 2-20 To 2-29Virginia TownzenNo ratings yet

- Unit III Study GuideDocument5 pagesUnit III Study GuideVirginia TownzenNo ratings yet

- Unit V Study GuideDocument4 pagesUnit V Study GuideVirginia TownzenNo ratings yet

- Unit 1 Accounting Equation TranscriptDocument2 pagesUnit 1 Accounting Equation TranscriptVirginia TownzenNo ratings yet

- Unit III Study GuideDocument5 pagesUnit III Study GuideVirginia TownzenNo ratings yet

- Unit II Study GuideDocument4 pagesUnit II Study GuideVirginia TownzenNo ratings yet

- Unit I Study GuideDocument5 pagesUnit I Study GuideVirginia TownzenNo ratings yet

- Savings Bank Passbook-RBI GuidelineDocument2 pagesSavings Bank Passbook-RBI GuidelineDebabrata MohantyNo ratings yet

- Homeowners Savings and Loan Bank Vs DailoDocument1 pageHomeowners Savings and Loan Bank Vs DailoCarlota Nicolas VillaromanNo ratings yet

- Goldleaf WP Making A Case For BIC at The Teller LineDocument16 pagesGoldleaf WP Making A Case For BIC at The Teller LineJyoti PatelNo ratings yet

- What To Do After Admission For Freemover StudentsDocument34 pagesWhat To Do After Admission For Freemover StudentsKunchur NarayanNo ratings yet

- Usaa Financial GuideDocument93 pagesUsaa Financial GuideDavid CloseNo ratings yet

- DB Realty Limited: Another Mumbai-Based PlayerDocument8 pagesDB Realty Limited: Another Mumbai-Based PlayerVahni SinghNo ratings yet

- A Saint in The Board Room Book Cover (Hardbound)Document1 pageA Saint in The Board Room Book Cover (Hardbound)vijay999No ratings yet

- Council Tax Bill - SampleXXXDocument4 pagesCouncil Tax Bill - SampleXXXs6286135No ratings yet

- Unit ThreeDocument19 pagesUnit Threesamiksha hamalNo ratings yet

- Islamic Banking User Manual-WAKALADocument20 pagesIslamic Banking User Manual-WAKALAPranay Kumar SahuNo ratings yet

- 19cse214: Theory of Computation: Case Study ReportDocument5 pages19cse214: Theory of Computation: Case Study ReportHarish RNo ratings yet

- Amer Shareef ResumeDocument2 pagesAmer Shareef Resumeamershareef337No ratings yet

- INV5606545Document11 pagesINV5606545mrgrayinthedarkNo ratings yet

- Inv. Mechanism by Islami Bank Bangladesh LTDDocument42 pagesInv. Mechanism by Islami Bank Bangladesh LTDshuvo100% (1)

- Eastern District New York Federal Court Complaint: Fraud Upon The CourtDocument42 pagesEastern District New York Federal Court Complaint: Fraud Upon The CourtTaylorbey American NationalNo ratings yet

- Euro Currency MarketDocument24 pagesEuro Currency MarketAlina RajputNo ratings yet

- Full Pack Pfcea New ProceduresDocument27 pagesFull Pack Pfcea New Proceduresdirector@bancofinancieroprivadoNo ratings yet

- Baft Cdcs Flyer Final 10 13 16 PDFDocument2 pagesBaft Cdcs Flyer Final 10 13 16 PDFDileep310No ratings yet

- Zeeshan 11Document861 pagesZeeshan 11Elasani Pvt LtdNo ratings yet

- OpTransactionHistory08 06 2019Document12 pagesOpTransactionHistory08 06 2019sara vananNo ratings yet

- Commercial Law Final ReviewDocument4 pagesCommercial Law Final ReviewJen ShaversNo ratings yet

- Financing Small Scale Industries Sbi Vis-À-Vis Other BanksDocument98 pagesFinancing Small Scale Industries Sbi Vis-À-Vis Other BanksAnonymous V9E1ZJtwoENo ratings yet

- Economy TermsDocument90 pagesEconomy TermsSabyasachi SahuNo ratings yet

- RA 9243 - Rationalizing The Provision of Documentary Stamp TaxDocument5 pagesRA 9243 - Rationalizing The Provision of Documentary Stamp TaxCrislene CruzNo ratings yet

- Ellery RulingDocument11 pagesEllery Rulingcorruptioncurrents100% (1)

- Contactless Smart Card Technology - GRP 4Document17 pagesContactless Smart Card Technology - GRP 4samiyaNo ratings yet

- Day Count ConventionDocument7 pagesDay Count ConventionDiego GonzálesNo ratings yet

- DigiPay v1Document18 pagesDigiPay v1KAVEEN PRASANNAMOORTHYNo ratings yet

- Removals & Storage Feb 10Document76 pagesRemovals & Storage Feb 10British Association of RemoversNo ratings yet

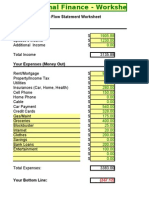

- Your Personal Cash Flow Statement Worksheet Income (Money In)Document4 pagesYour Personal Cash Flow Statement Worksheet Income (Money In)api-3831249No ratings yet

Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5822)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Human Resource Management: The Key FunctionsDocument10 pagesHuman Resource Management: The Key FunctionsVirginia TownzenNo ratings yet

- Normal Balances in Accounting Video TranscriptDocument2 pagesNormal Balances in Accounting Video TranscriptVirginia TownzenNo ratings yet

- November 2019 Transactions: Date Account Titles and Explanations Debit CreditDocument5 pagesNovember 2019 Transactions: Date Account Titles and Explanations Debit CreditVirginia TownzenNo ratings yet

- Unit 8 Article Review SubmitDocument4 pagesUnit 8 Article Review SubmitVirginia TownzenNo ratings yet

- Chapter 2 Accounting Principles 2-20 To 2-29Document17 pagesChapter 2 Accounting Principles 2-20 To 2-29Virginia TownzenNo ratings yet

- Unit III Study GuideDocument5 pagesUnit III Study GuideVirginia TownzenNo ratings yet

- Unit V Study GuideDocument4 pagesUnit V Study GuideVirginia TownzenNo ratings yet

- Unit 1 Accounting Equation TranscriptDocument2 pagesUnit 1 Accounting Equation TranscriptVirginia TownzenNo ratings yet

- Unit III Study GuideDocument5 pagesUnit III Study GuideVirginia TownzenNo ratings yet

- Unit II Study GuideDocument4 pagesUnit II Study GuideVirginia TownzenNo ratings yet

- Unit I Study GuideDocument5 pagesUnit I Study GuideVirginia TownzenNo ratings yet

- Savings Bank Passbook-RBI GuidelineDocument2 pagesSavings Bank Passbook-RBI GuidelineDebabrata MohantyNo ratings yet

- Homeowners Savings and Loan Bank Vs DailoDocument1 pageHomeowners Savings and Loan Bank Vs DailoCarlota Nicolas VillaromanNo ratings yet

- Goldleaf WP Making A Case For BIC at The Teller LineDocument16 pagesGoldleaf WP Making A Case For BIC at The Teller LineJyoti PatelNo ratings yet

- What To Do After Admission For Freemover StudentsDocument34 pagesWhat To Do After Admission For Freemover StudentsKunchur NarayanNo ratings yet

- Usaa Financial GuideDocument93 pagesUsaa Financial GuideDavid CloseNo ratings yet

- DB Realty Limited: Another Mumbai-Based PlayerDocument8 pagesDB Realty Limited: Another Mumbai-Based PlayerVahni SinghNo ratings yet

- A Saint in The Board Room Book Cover (Hardbound)Document1 pageA Saint in The Board Room Book Cover (Hardbound)vijay999No ratings yet

- Council Tax Bill - SampleXXXDocument4 pagesCouncil Tax Bill - SampleXXXs6286135No ratings yet

- Unit ThreeDocument19 pagesUnit Threesamiksha hamalNo ratings yet

- Islamic Banking User Manual-WAKALADocument20 pagesIslamic Banking User Manual-WAKALAPranay Kumar SahuNo ratings yet

- 19cse214: Theory of Computation: Case Study ReportDocument5 pages19cse214: Theory of Computation: Case Study ReportHarish RNo ratings yet

- Amer Shareef ResumeDocument2 pagesAmer Shareef Resumeamershareef337No ratings yet

- INV5606545Document11 pagesINV5606545mrgrayinthedarkNo ratings yet

- Inv. Mechanism by Islami Bank Bangladesh LTDDocument42 pagesInv. Mechanism by Islami Bank Bangladesh LTDshuvo100% (1)

- Eastern District New York Federal Court Complaint: Fraud Upon The CourtDocument42 pagesEastern District New York Federal Court Complaint: Fraud Upon The CourtTaylorbey American NationalNo ratings yet

- Euro Currency MarketDocument24 pagesEuro Currency MarketAlina RajputNo ratings yet

- Full Pack Pfcea New ProceduresDocument27 pagesFull Pack Pfcea New Proceduresdirector@bancofinancieroprivadoNo ratings yet

- Baft Cdcs Flyer Final 10 13 16 PDFDocument2 pagesBaft Cdcs Flyer Final 10 13 16 PDFDileep310No ratings yet

- Zeeshan 11Document861 pagesZeeshan 11Elasani Pvt LtdNo ratings yet

- OpTransactionHistory08 06 2019Document12 pagesOpTransactionHistory08 06 2019sara vananNo ratings yet

- Commercial Law Final ReviewDocument4 pagesCommercial Law Final ReviewJen ShaversNo ratings yet

- Financing Small Scale Industries Sbi Vis-À-Vis Other BanksDocument98 pagesFinancing Small Scale Industries Sbi Vis-À-Vis Other BanksAnonymous V9E1ZJtwoENo ratings yet

- Economy TermsDocument90 pagesEconomy TermsSabyasachi SahuNo ratings yet

- RA 9243 - Rationalizing The Provision of Documentary Stamp TaxDocument5 pagesRA 9243 - Rationalizing The Provision of Documentary Stamp TaxCrislene CruzNo ratings yet

- Ellery RulingDocument11 pagesEllery Rulingcorruptioncurrents100% (1)

- Contactless Smart Card Technology - GRP 4Document17 pagesContactless Smart Card Technology - GRP 4samiyaNo ratings yet

- Day Count ConventionDocument7 pagesDay Count ConventionDiego GonzálesNo ratings yet

- DigiPay v1Document18 pagesDigiPay v1KAVEEN PRASANNAMOORTHYNo ratings yet

- Removals & Storage Feb 10Document76 pagesRemovals & Storage Feb 10British Association of RemoversNo ratings yet

- Your Personal Cash Flow Statement Worksheet Income (Money In)Document4 pagesYour Personal Cash Flow Statement Worksheet Income (Money In)api-3831249No ratings yet