Download as pdf or txt

You might also like

- Gucci: Staying Relevant in Luxury Over A CenturyDocument4 pagesGucci: Staying Relevant in Luxury Over A CenturyAmrit KocharNo ratings yet

- Group Ariel S.A. Parity Conditions and Cross Border ValuationDocument13 pagesGroup Ariel S.A. Parity Conditions and Cross Border Valuationmatt100% (1)

- Turkish Leasing MarketDocument16 pagesTurkish Leasing Marketlévai_gáborNo ratings yet

- Women at The Peace Table - Making A DifferenceDocument71 pagesWomen at The Peace Table - Making A DifferenceMyleikaFernandezNo ratings yet

- FPT Powertrain Technologies: Alfredo AltavillaDocument28 pagesFPT Powertrain Technologies: Alfredo AltavillaKadirOzturkNo ratings yet

- Ideocon: Experience Change - The Indian Multinational WayDocument131 pagesIdeocon: Experience Change - The Indian Multinational WayAmitvikram ToraskarNo ratings yet

- Fundamental Analysis SeminarDocument51 pagesFundamental Analysis SeminarEugene DalanginNo ratings yet

- Monthly Economic Bulletin: January 2011Document15 pagesMonthly Economic Bulletin: January 2011lrochekellyNo ratings yet

- TeleGeography PTC 2007Document60 pagesTeleGeography PTC 2007Bobby WeeNo ratings yet

- 2.1 Macroeconomic Indicators GDP 10 11 Nov PDFDocument56 pages2.1 Macroeconomic Indicators GDP 10 11 Nov PDFIvan MedićNo ratings yet

- Used Car Exports From JapanDocument9 pagesUsed Car Exports From JapanacmunarNo ratings yet

- AMERCO Finance Slides 2021Document24 pagesAMERCO Finance Slides 2021Daniel KwanNo ratings yet

- Indian Healthcare and Pharma Industry Full Report 1624655688Document11 pagesIndian Healthcare and Pharma Industry Full Report 1624655688saurav_kumar_32No ratings yet

- The Great RecessionDocument10 pagesThe Great RecessionZorawar SinghNo ratings yet

- A Presentation On Special Economic Zones (SEZDocument29 pagesA Presentation On Special Economic Zones (SEZsvjiwaji96% (23)

- South Africa Latin America and The Caribbean Trading Relationship Synopsis October 2016Document9 pagesSouth Africa Latin America and The Caribbean Trading Relationship Synopsis October 2016JuanIgnacioPascualNo ratings yet

- 07032011195741auto Monthly UpdateDocument17 pages07032011195741auto Monthly UpdateCA Suvendu Kumar DasNo ratings yet

- Period 0 ReportsDocument24 pagesPeriod 0 ReportsrahulNo ratings yet

- Valuation - DCF+LBO - Master - VS - 09-01-2012 EB CommentsDocument89 pagesValuation - DCF+LBO - Master - VS - 09-01-2012 EB CommentsJames MitchellNo ratings yet

- Indian Auto SectorDocument14 pagesIndian Auto SectorAnkur Sharda100% (19)

- NH Corporate Presentation 9m 2017Document42 pagesNH Corporate Presentation 9m 2017Nicu ClaudiuNo ratings yet

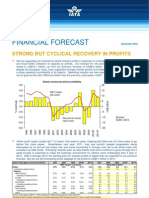

- Financial Forecast: Strong But Cyclical Recovery in ProfitsDocument4 pagesFinancial Forecast: Strong But Cyclical Recovery in ProfitsDaniel WongNo ratings yet

- Kirby Market SegmentationDocument1 pageKirby Market Segmentationsuk1234No ratings yet

- Macroeconomic PopulismDocument37 pagesMacroeconomic PopulismIván CarrinoNo ratings yet

- Confronting Economic SlowdownDocument26 pagesConfronting Economic Slowdownepra100% (1)

- Key Indicators: Analysis of EFSA Report FYE 30 June 2014Document16 pagesKey Indicators: Analysis of EFSA Report FYE 30 June 2014mostafaNo ratings yet

- Q307data SumDocument1 pageQ307data SumdiazromeriNo ratings yet

- Q1 2009-10 Performance Update GCPLDocument31 pagesQ1 2009-10 Performance Update GCPLArks_Dawn_5956No ratings yet

- 50 AAPL Buyside PitchbookDocument22 pages50 AAPL Buyside PitchbookkamranNo ratings yet

- Real Estate PPT (Final)Document63 pagesReal Estate PPT (Final)9920163728100% (1)

- 8 Emerging Nations (2020 - 08 - 15 14 - 09 - 52 UTC)Document19 pages8 Emerging Nations (2020 - 08 - 15 14 - 09 - 52 UTC)Robert TirtawigoenaNo ratings yet

- Kingdom of MoroccoDocument53 pagesKingdom of MoroccoHafiz Kamran AhmedNo ratings yet

- Indian ReetailDocument23 pagesIndian ReetailscribdranijNo ratings yet

- 25 Inflation Rate: Exports, Imports and Trade BalanceDocument4 pages25 Inflation Rate: Exports, Imports and Trade BalanceKenjin SaiNo ratings yet

- 50 AAPL Buyside PitchbookDocument22 pages50 AAPL Buyside PitchbookAkshay ShaikhNo ratings yet

- International BusinessDocument10 pagesInternational BusinessGauravTiwariNo ratings yet

- Request-Jefferies Nantucket FINAL v3Document39 pagesRequest-Jefferies Nantucket FINAL v3guillermoNo ratings yet

- Simon Lim, Director - Listings 26 March 2008: Singapore ExchangeDocument40 pagesSimon Lim, Director - Listings 26 March 2008: Singapore ExchangenetworkedNo ratings yet

- Maruti Suzuki India LTDDocument40 pagesMaruti Suzuki India LTDnishantNo ratings yet

- Boeing Current Market Outlook 2009 To 2028Document30 pagesBoeing Current Market Outlook 2009 To 2028Jijoo Jacob VargheseNo ratings yet

- Slides SwapDocument23 pagesSlides Swapqwsx098No ratings yet

- About FINN For CandidatesDocument26 pagesAbout FINN For CandidatesChinmay SHAHNo ratings yet

- Maruti Suzuki CLSA ConfDocument26 pagesMaruti Suzuki CLSA ConfnishantNo ratings yet

- Vietnam Coffee Sector Review and PerspectiveDocument19 pagesVietnam Coffee Sector Review and PerspectivepabonmcNo ratings yet

- LBO Modeling PE Firm Case StudyDocument6 pagesLBO Modeling PE Firm Case StudybasanisujithkumarNo ratings yet

- Asset Management Companies: Date: 20 February, 2020Document34 pagesAsset Management Companies: Date: 20 February, 2020Ikp IkpNo ratings yet

- Q2 FY10 Results Review: 26 October, 2009Document17 pagesQ2 FY10 Results Review: 26 October, 2009rayhan7No ratings yet

- Oati 30 enDocument48 pagesOati 30 enerereredssdfsfdsfNo ratings yet

- 2008 J D Power Automotive Online Marketing ReviewDocument28 pages2008 J D Power Automotive Online Marketing ReviewTxScoutNo ratings yet

- Industry Growth OutlookDocument1 pageIndustry Growth OutlookPalo Alto SoftwareNo ratings yet

- Nokia Results 2023 q2Document31 pagesNokia Results 2023 q2yalemorgan69No ratings yet

- Maple Leaf Cement Factory LimitedDocument70 pagesMaple Leaf Cement Factory LimitedMubasharNo ratings yet

- Financial Analysis of ACC LimitedDocument9 pagesFinancial Analysis of ACC LimitedJasjeet SinghNo ratings yet

- Secondary Pres On MULDocument23 pagesSecondary Pres On MULnishantNo ratings yet

- Dupont DPC LBO AssignmentDocument3 pagesDupont DPC LBO Assignmentw_fibNo ratings yet

- Q1 2020-21 Fact Sheet PDFDocument27 pagesQ1 2020-21 Fact Sheet PDFJose CANo ratings yet

- 3-Belobaba Fares and Competition AirlineDocument30 pages3-Belobaba Fares and Competition AirlineGonzaloAlarconNo ratings yet

- Alternators, Generators & Parts (C.V. OE & Aftermarket) World Summary: Market Values & Financials by CountryFrom EverandAlternators, Generators & Parts (C.V. OE & Aftermarket) World Summary: Market Values & Financials by CountryNo ratings yet

- OEM Paints & Finishes World Summary: Market Sector Values & Financials by CountryFrom EverandOEM Paints & Finishes World Summary: Market Sector Values & Financials by CountryNo ratings yet

- Batteries (Commercial Vehicle OE & Aftermarket) World Summary: Market Values & Financials by CountryFrom EverandBatteries (Commercial Vehicle OE & Aftermarket) World Summary: Market Values & Financials by CountryNo ratings yet

- Steering & Steering Parts (C.V. OE & Aftermarket) World Summary: Market Values & Financials by CountryFrom EverandSteering & Steering Parts (C.V. OE & Aftermarket) World Summary: Market Values & Financials by CountryNo ratings yet

- Intellectual Property: Valuation, Exploitation, and Infringement Damages, 2017 Cumulative SupplementFrom EverandIntellectual Property: Valuation, Exploitation, and Infringement Damages, 2017 Cumulative SupplementNo ratings yet

- Wheels & Parts (C.V. OE & Aftermarket) World Summary: Market Values & Financials by CountryFrom EverandWheels & Parts (C.V. OE & Aftermarket) World Summary: Market Values & Financials by CountryNo ratings yet

- Japan StudyDocument52 pagesJapan Studylévai_gáborNo ratings yet

- Credit Bureau - ACCIS-Survey Final ReportDocument37 pagesCredit Bureau - ACCIS-Survey Final Reportlévai_gáborNo ratings yet

- Challenges & Opportunities in The Automotive Leasing IndustryDocument25 pagesChallenges & Opportunities in The Automotive Leasing Industrylévai_gáborNo ratings yet

- Leasing Yearbook 2010Document115 pagesLeasing Yearbook 2010lévai_gáborNo ratings yet

- Unidroit - Doc. 13 - Summary ReportDocument95 pagesUnidroit - Doc. 13 - Summary Reportlévai_gáborNo ratings yet

- Subcont - PT Tigenco Graha PersadaDocument9 pagesSubcont - PT Tigenco Graha PersadaxoxxNo ratings yet

- (Anonymous :josman) Buttboy in A Blindfold (Eng) - My Reading MangaDocument14 pages(Anonymous :josman) Buttboy in A Blindfold (Eng) - My Reading MangaPedro Costa50% (4)

- WHO Tobacco Global Report 2000-2025Document150 pagesWHO Tobacco Global Report 2000-2025ANo ratings yet

- Mohammed Anwar CVDocument2 pagesMohammed Anwar CVDebananda SuarNo ratings yet

- Oranjestad The CapitalDocument4 pagesOranjestad The CapitalJAYSONN GARCIANo ratings yet

- Para PrefecturaDocument2 pagesPara PrefecturaAngelo CopettiNo ratings yet

- Fidic IV Conditions of Contract - OverviewDocument8 pagesFidic IV Conditions of Contract - Overviewlittledragon0110100% (2)

- Bristol, Virginia ResolutionDocument2 pagesBristol, Virginia ResolutionNews 5 WCYBNo ratings yet

- People v. PerezDocument1 pagePeople v. PerezNoreenesse SantosNo ratings yet

- Food AdulterationDocument3 pagesFood AdulterationFarhan KarimNo ratings yet

- PEB Foundation Certificate Trade Mark Law FC5 (P7)Document13 pagesPEB Foundation Certificate Trade Mark Law FC5 (P7)Pradeep KumarNo ratings yet

- MmpiDocument25 pagesMmpiMardans Whaisman100% (1)

- VMP E16 E01 V00Document36 pagesVMP E16 E01 V00Marian StatacheNo ratings yet

- The Psychic BeingDocument15 pagesThe Psychic Beingbibilal vijayadevNo ratings yet

- Court DiaryDocument29 pagesCourt DiarySwati KishoreNo ratings yet

- Study NoteDocument3 pagesStudy NoteBezalel OwusuNo ratings yet

- Modul Bhs. InggrisDocument35 pagesModul Bhs. InggrisayodyaNo ratings yet

- Industrial Relations and PolicyDocument3 pagesIndustrial Relations and Policyshikher027598No ratings yet

- If Only U Sleep-Walking Americans Have A Thousand Men Like This Joe CortinaDocument19 pagesIf Only U Sleep-Walking Americans Have A Thousand Men Like This Joe CortinaYusuf (Joe) Jussac, Jr. a.k.a unclejoeNo ratings yet

- Usaid Adr Mechanics in Coop SectorDocument94 pagesUsaid Adr Mechanics in Coop SectorArnel Mondejar100% (1)

- American Cinematographer 1922 Vol 2 No 27 PDFDocument16 pagesAmerican Cinematographer 1922 Vol 2 No 27 PDFbrad_rushingNo ratings yet

- 22nd Recitation Summary ProceedingDocument14 pages22nd Recitation Summary ProceedingSumpt LatogNo ratings yet

- Fall 2024 Seasonal CatalogDocument48 pagesFall 2024 Seasonal CatalogStanford University PressNo ratings yet

- Running A Lottery Quick Guide PDFDocument2 pagesRunning A Lottery Quick Guide PDFsyeddilNo ratings yet

- AWH Catalogue DIN 11864-11853 1.1Document70 pagesAWH Catalogue DIN 11864-11853 1.1dingobk1No ratings yet

- 2 Jose Ang V Estate of Sy SoDocument2 pages2 Jose Ang V Estate of Sy SoDarkSlumberNo ratings yet

- Habeas Corpus, Amparo, Habeas DataDocument32 pagesHabeas Corpus, Amparo, Habeas DataLeila De SilvaNo ratings yet

- OSINT TikTokDocument21 pagesOSINT TikTokEduardoNo ratings yet