Download as pdf or txt

You might also like

- Importance and Role of TaxationDocument7 pagesImportance and Role of TaxationZale Crud100% (2)

- Taxation As A Major Source of Govt. FundingDocument47 pagesTaxation As A Major Source of Govt. FundingPriyali Rai50% (2)

- Repeal and Revival of StatutesDocument22 pagesRepeal and Revival of Statutestwink58% (19)

- Develop Understanding of TaxationDocument31 pagesDevelop Understanding of TaxationAshenafi Abdurkadir100% (3)

- Chapter 10: Transaction C'eycle - The Expenditure Cycle True/FalseDocument13 pagesChapter 10: Transaction C'eycle - The Expenditure Cycle True/FalseHong NguyenNo ratings yet

- New Management Challenges For The New AgeDocument22 pagesNew Management Challenges For The New AgeHong Nguyen100% (1)

- In The Court of Appeal of The State of CaliforniaDocument9 pagesIn The Court of Appeal of The State of CaliforniaCalifornia Judicial Branch News Service - Investigative Reporting Source Material & Story IdeasNo ratings yet

- (Digest) Pelayo V LauronDocument1 page(Digest) Pelayo V LauronKarla Bee50% (2)

- The Importance of Taxes: What Is A "Tax"Document6 pagesThe Importance of Taxes: What Is A "Tax"Hami KhaNNo ratings yet

- 11 Advanced Taxation Aau MaterialDocument129 pages11 Advanced Taxation Aau MaterialErmi ManNo ratings yet

- © Ncert Not To Be RepublishedDocument16 pages© Ncert Not To Be Republishedguru1241987babuNo ratings yet

- TaxationDocument34 pagesTaxationShyamKumarKCNo ratings yet

- BACC3 - Antiniolos, FaieDocument21 pagesBACC3 - Antiniolos, Faiemochi antiniolosNo ratings yet

- Public Revenue 17396Document54 pagesPublic Revenue 17396sneha9988gargNo ratings yet

- Lec 10 ImaDocument13 pagesLec 10 ImaSean Muriithi PaulNo ratings yet

- As Fiscal PolicyDocument8 pagesAs Fiscal PolicyZunaira JamilNo ratings yet

- 2.1. Definition of TaxDocument15 pages2.1. Definition of TaxAyalew TayeNo ratings yet

- Public Finance CH1 - PrintDocument6 pagesPublic Finance CH1 - PrintWegene Benti UmaNo ratings yet

- Meaning and Characteristics of Taxation: Public Revenue Sources of Public RevenuesDocument19 pagesMeaning and Characteristics of Taxation: Public Revenue Sources of Public Revenuessamuel debebeNo ratings yet

- PFT Chapter 3Document16 pagesPFT Chapter 3Nati TesfayeNo ratings yet

- PFT - Chapter 2, MEANING AND CHARACTERISTICS OF TAXATIONDocument19 pagesPFT - Chapter 2, MEANING AND CHARACTERISTICS OF TAXATIONLakachew GetasewNo ratings yet

- Me 2Document11 pagesMe 2Parth SharmaNo ratings yet

- Chapter ThreeDocument25 pagesChapter ThreeEleni DrNo ratings yet

- Taxation CTDocument8 pagesTaxation CTJoy NathNo ratings yet

- 5.1 Taxes: Definition, Principles, Objectives and ClassificationsDocument12 pages5.1 Taxes: Definition, Principles, Objectives and Classificationsdr7dh8c2sdNo ratings yet

- 2Document2 pages2Md. Rasel PatwaryNo ratings yet

- Business TaxationDocument7 pagesBusiness TaxationMahes WaranNo ratings yet

- 2.1meaning of Tax: Chapter TwoDocument16 pages2.1meaning of Tax: Chapter TwoEmebet TesemaNo ratings yet

- Lecture 1Document10 pagesLecture 1Masitala PhiriNo ratings yet

- The Impact of Taxation On The Economic DevelopmentDocument3 pagesThe Impact of Taxation On The Economic DevelopmentppppNo ratings yet

- Business Taxation MaterialDocument18 pagesBusiness Taxation MaterialKhushboo ParikhNo ratings yet

- 3.1 Definition of TaxDocument27 pages3.1 Definition of TaxTerefe DubeNo ratings yet

- Tax Policies and Its Economic FluctuationsDocument14 pagesTax Policies and Its Economic FluctuationsZubairNo ratings yet

- Essay FinalDocument6 pagesEssay FinalHananNo ratings yet

- Importance of Tax in EconomyDocument7 pagesImportance of Tax in EconomyAbdul WahabNo ratings yet

- CH 1Document20 pagesCH 1tomas PenuelaNo ratings yet

- Government RevenueDocument6 pagesGovernment Revenuenihadarfin19No ratings yet

- Chapter No. 2 Theoretical Framework OftaxationDocument51 pagesChapter No. 2 Theoretical Framework OftaxationSachin KumarNo ratings yet

- Calculate Taxes Fees and Charges For 2015 EntryDocument45 pagesCalculate Taxes Fees and Charges For 2015 Entrywashoelias5100% (1)

- Tax Accounting AssignmentDocument6 pagesTax Accounting AssignmentabdulrashidNo ratings yet

- Role of Taxation in Equal Distribution of The Economic Resources in A CountryDocument5 pagesRole of Taxation in Equal Distribution of The Economic Resources in A CountryAlextro MaxonNo ratings yet

- Chapter One TaxationDocument10 pagesChapter One TaxationEmebet TesemaNo ratings yet

- Leec 105Document19 pagesLeec 105pradyu1990No ratings yet

- 12th Economics Chapter 5 & 6Document38 pages12th Economics Chapter 5 & 6anupsorenNo ratings yet

- Best Practices To Control Underground Economy in The World: JapanDocument8 pagesBest Practices To Control Underground Economy in The World: JapanAsif RahoojoNo ratings yet

- Leec 105Document19 pagesLeec 105Pradeep NairNo ratings yet

- TAXATIONDocument3 pagesTAXATIONDELA TORRE, SHENANORNo ratings yet

- Taxes at A Glance - Lec1Document17 pagesTaxes at A Glance - Lec1Furqan KhanNo ratings yet

- BBA Program Course Title: Taxation Course Code: A408 Course Outline Introduction of FacultyDocument45 pagesBBA Program Course Title: Taxation Course Code: A408 Course Outline Introduction of FacultyMunkasir MasudNo ratings yet

- Educ 612 Reaction Paper Unit 3Document2 pagesEduc 612 Reaction Paper Unit 3Cristobal RabuyaNo ratings yet

- Why Is Tax Important For The Company of A Country?: T + S + M I + X + GDocument2 pagesWhy Is Tax Important For The Company of A Country?: T + S + M I + X + GAnonymous rcCVWoM8bNo ratings yet

- Session 4 Fiscal PolicyDocument13 pagesSession 4 Fiscal PolicyThouseef AhmedNo ratings yet

- Relevance of Taxation1Document10 pagesRelevance of Taxation1einol padalNo ratings yet

- Calculate Tax Fees and Charge PDFDocument30 pagesCalculate Tax Fees and Charge PDFJamal86% (7)

- Develop and Understand TaxationDocument26 pagesDevelop and Understand TaxationNigussie BerhanuNo ratings yet

- Canons of Taxation, Shifting and IncidenceDocument16 pagesCanons of Taxation, Shifting and Incidence7ky2nz4tkyNo ratings yet

- Introduction To Taxation Lec 1 and 2 25032024 020536amDocument14 pagesIntroduction To Taxation Lec 1 and 2 25032024 020536amJhonnNo ratings yet

- TaxationDocument10 pagesTaxationVictoria PitaNo ratings yet

- Microeconomics Group Assignment (Report Writing)Document9 pagesMicroeconomics Group Assignment (Report Writing)Abdirizak AhmedNo ratings yet

- Fiscal Policy 2019Document23 pagesFiscal Policy 2019DNLNo ratings yet

- Tax Indiidual AssDocument6 pagesTax Indiidual AssdemolaojaomoNo ratings yet

- Ans Taxation 1Document23 pagesAns Taxation 1Priscilla AdebolaNo ratings yet

- Methods of Enhancing Tax Revenue.: Subitted By-Saima SultanDocument14 pagesMethods of Enhancing Tax Revenue.: Subitted By-Saima Sultansaima sultanNo ratings yet

- The Government Budget & The EconomyDocument10 pagesThe Government Budget & The EconomyNeel ChaurushiNo ratings yet

- 1 Nesta (6/13) : 49 MarksDocument2 pages1 Nesta (6/13) : 49 MarksHong NguyenNo ratings yet

- Unit 10 SpeakingDocument7 pagesUnit 10 SpeakingHong NguyenNo ratings yet

- Chapter 6: Enterprise Information Systems: True/FalseDocument7 pagesChapter 6: Enterprise Information Systems: True/FalseHong NguyenNo ratings yet

- 8-Database Concepts 1Document16 pages8-Database Concepts 1Hong NguyenNo ratings yet

- Chapter 4: Database Concepts II: True/FalseDocument10 pagesChapter 4: Database Concepts II: True/FalseHong NguyenNo ratings yet

- Chapter 9: Transaction Cycle - The Revenue Cycle: True/FalseDocument7 pagesChapter 9: Transaction Cycle - The Revenue Cycle: True/FalseHong NguyenNo ratings yet

- Personal income tax (PIT) : PGS.,TS Nguyễn Thị Thanh Hoài 1Document14 pagesPersonal income tax (PIT) : PGS.,TS Nguyễn Thị Thanh Hoài 1Hong NguyenNo ratings yet

- Net Cash Flows From Financing Activities 108,523 49,112 2,996Document11 pagesNet Cash Flows From Financing Activities 108,523 49,112 2,996Hong NguyenNo ratings yet

- Lesson 5 MNS 1052Document52 pagesLesson 5 MNS 1052Hong NguyenNo ratings yet

- Lesson 4 MNS 1052Document61 pagesLesson 4 MNS 1052Hong NguyenNo ratings yet

- Lesson 6 MNS 1052Document46 pagesLesson 6 MNS 1052Hong NguyenNo ratings yet

- Spanking The ChildrenDocument22 pagesSpanking The ChildrenHong NguyenNo ratings yet

- Lesson 2 MNS 1052Document62 pagesLesson 2 MNS 1052Hong NguyenNo ratings yet

- 1 Consumer Guide 172 2 Dealership 93 3 Word of Mouth 40 4 Internet 26 331Document2 pages1 Consumer Guide 172 2 Dealership 93 3 Word of Mouth 40 4 Internet 26 331Hong NguyenNo ratings yet

- Seminar 1 - Q - TradeDocument15 pagesSeminar 1 - Q - TradeHong NguyenNo ratings yet

- A: Introducing and Discussing B: New WordsDocument3 pagesA: Introducing and Discussing B: New WordsHong NguyenNo ratings yet

- Assignment - INS1015.July. 2020Document2 pagesAssignment - INS1015.July. 2020Hong NguyenNo ratings yet

- Tai Lieu Nghe - ML Upper - 2011 - EditedDocument9 pagesTai Lieu Nghe - ML Upper - 2011 - EditedHong NguyenNo ratings yet

- Lesson 1: MNS 1052 3-chiều thư năm. Cô Trinh. Team Code: t11m5ze doanvx@isvnu.vnDocument47 pagesLesson 1: MNS 1052 3-chiều thư năm. Cô Trinh. Team Code: t11m5ze doanvx@isvnu.vnHong NguyenNo ratings yet

- Seminar 3: QuestionDocument9 pagesSeminar 3: QuestionHong NguyenNo ratings yet

- Economics: Consumers, Producers, and The Efficiency of MarketsDocument44 pagesEconomics: Consumers, Producers, and The Efficiency of MarketsHong NguyenNo ratings yet

- The Theory of Production: Dr. Lê Thanh HàDocument86 pagesThe Theory of Production: Dr. Lê Thanh HàHong NguyenNo ratings yet

- Seminar 2Document2 pagesSeminar 2Hong NguyenNo ratings yet

- Economics: Thinking Like An EconomistDocument29 pagesEconomics: Thinking Like An EconomistHong NguyenNo ratings yet

- SGLGB Technical Notes 2022Document27 pagesSGLGB Technical Notes 2022Louie ManarpiisNo ratings yet

- DownloadDocument2 pagesDownloadgeethikaNo ratings yet

- Zamora vs. Heirs of CarmenDocument5 pagesZamora vs. Heirs of CarmenAnakataNo ratings yet

- Calamba Medical Center Inc. v. NationalDocument10 pagesCalamba Medical Center Inc. v. NationalAndrei Anne PalomarNo ratings yet

- Marubeni Is A Non-Resident Foreign Corporation With Respect To The Transaction in QuestionDocument3 pagesMarubeni Is A Non-Resident Foreign Corporation With Respect To The Transaction in Questionarden1imNo ratings yet

- Chapter 2 Oblicon ReviewerDocument7 pagesChapter 2 Oblicon ReviewerPetrelle RodrigoNo ratings yet

- AP Gov Unit 3 JeopardyDocument55 pagesAP Gov Unit 3 JeopardyMark DarketNo ratings yet

- Justice For IrelandDocument7 pagesJustice For IrelandAna GilNo ratings yet

- Media To Upload1637323538Document2 pagesMedia To Upload1637323538Sushant JadhavNo ratings yet

- TPR 001 eDocument4 pagesTPR 001 ebandara123No ratings yet

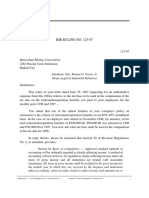

- ECONOMIC BENEFIT THEORY - BIR Ruling No. 123-97 (Retirement and Separation Benefits Paid To Employees)Document2 pagesECONOMIC BENEFIT THEORY - BIR Ruling No. 123-97 (Retirement and Separation Benefits Paid To Employees)KriszanFrancoManiponNo ratings yet

- Sharekhan NRIDocument58 pagesSharekhan NRIRaghuThimmegowdaNo ratings yet

- Corporate PersonalityDocument22 pagesCorporate PersonalitysonviNo ratings yet

- SpecializationDocument22 pagesSpecializationKervin SysingNo ratings yet

- Nigeria Current Affairs Latest Questions and Answers PDF Free Download (1960 Till Date)Document123 pagesNigeria Current Affairs Latest Questions and Answers PDF Free Download (1960 Till Date)Deborah Omobolanle OlalekanNo ratings yet

- Chanakya National Law University: Law of Contracts Beneficial Contracts and Contracts For Apprenticeship of MinorDocument4 pagesChanakya National Law University: Law of Contracts Beneficial Contracts and Contracts For Apprenticeship of MinorKaran singh RautelaNo ratings yet

- Scholarship Cssinst13Document10 pagesScholarship Cssinst13Arjun CpNo ratings yet

- State Tax FormDocument2 pagesState Tax FormRon SchingsNo ratings yet

- Cypress Bay-Laurent-Levinson-Neg-Dowling-Round2Document38 pagesCypress Bay-Laurent-Levinson-Neg-Dowling-Round2IanNo ratings yet

- PPTDocument32 pagesPPTPistaccio GiovanniNo ratings yet

- Tai Tong v. Insurance Commission, GR. 55397, 29 Feb. 1988Document6 pagesTai Tong v. Insurance Commission, GR. 55397, 29 Feb. 1988Homer SimpsonNo ratings yet

- Riap PDFDocument2 pagesRiap PDFMark AsisNo ratings yet

- Why Do We Need Political Parties?Document3 pagesWhy Do We Need Political Parties?AdyaNo ratings yet

- The American Occupation in The Philippines: Presented by LIKHADocument35 pagesThe American Occupation in The Philippines: Presented by LIKHAMarc Jiro Dalluay100% (2)

- Offer LetterDocument4 pagesOffer LetterBikramNo ratings yet

- PRELIMDocument8 pagesPRELIMSATANIS, JESIE BOY O.No ratings yet

- Construction Industry Authority of The Philippines - 34 Page PDFDocument34 pagesConstruction Industry Authority of The Philippines - 34 Page PDFWilliamNo ratings yet