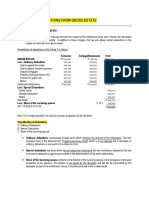

Gross Estate: Resident Citizen, Non-Resident Citizen, and Resident Alien Decedents

Gross Estate: Resident Citizen, Non-Resident Citizen, and Resident Alien Decedents

You might also like

- Module 1 - Deductions From Gross EstateDocument68 pagesModule 1 - Deductions From Gross EstateKat Miranda100% (1)

- Feasibility StudyDocument5 pagesFeasibility StudyKath Garcia50% (4)

- Encyclopedia of Chemical Processing - S Lee (Taylor and Francis, 2006) WW PDFDocument3,338 pagesEncyclopedia of Chemical Processing - S Lee (Taylor and Francis, 2006) WW PDFMahfuzur Rahman SiddikyNo ratings yet

- Chapter Exercises DeductionsDocument11 pagesChapter Exercises DeductionsShaine KeefeNo ratings yet

- KH-HO - NG-MAI-CH - NH - 1.xlsx Filename UTF-8''KH-HOÀNG-MAI-CH - NHÀ-1Document549 pagesKH-HO - NG-MAI-CH - NH - 1.xlsx Filename UTF-8''KH-HOÀNG-MAI-CH - NHÀ-1Lê Minh TuânNo ratings yet

- Deductions From Gross EstateDocument34 pagesDeductions From Gross Estatesmosaldana.cvtNo ratings yet

- Chapter 9 Estate Tax DeductionsDocument7 pagesChapter 9 Estate Tax DeductionsEthel Joy Tolentino GamboaNo ratings yet

- Lesson 3Document4 pagesLesson 3Iris Lavigne RojoNo ratings yet

- ACAE 18 - Deduction From Gross EstateDocument4 pagesACAE 18 - Deduction From Gross Estatechen dalitNo ratings yet

- TAX 2 Deductions From The Gross Estate 1PPT.Document24 pagesTAX 2 Deductions From The Gross Estate 1PPT.Franz Ana Marie CuaNo ratings yet

- Deductions: Philippines Gross Estate World Gross Estate Deductible LITDocument3 pagesDeductions: Philippines Gross Estate World Gross Estate Deductible LITMaria LopezNo ratings yet

- Chapter 6 Deductions From The Gross Estate PDFDocument7 pagesChapter 6 Deductions From The Gross Estate PDFDudz MatienzoNo ratings yet

- M5 - Deductions From Gross Estate - Students'Document33 pagesM5 - Deductions From Gross Estate - Students'micaella pasionNo ratings yet

- BusTax - Chapter 3 MODULEDocument8 pagesBusTax - Chapter 3 MODULETimon CarandangNo ratings yet

- Tax 2 4Document9 pagesTax 2 4amlecdeyojNo ratings yet

- X DeductionsDocument11 pagesX Deductionsmariyha PalangganaNo ratings yet

- Estate Tax: Taxation 1Document22 pagesEstate Tax: Taxation 1Jess Guiang CasamorinNo ratings yet

- TAX 2 Deductions From The Gross Estate 1PPTDocument24 pagesTAX 2 Deductions From The Gross Estate 1PPTMichael AquinoNo ratings yet

- Estate Tax 3Document50 pagesEstate Tax 3Lea JoaquinNo ratings yet

- Chapter 2 - Deductions From The Gross EstateDocument9 pagesChapter 2 - Deductions From The Gross EstateElla Marie WicoNo ratings yet

- Estate Tax (Exercises)Document3 pagesEstate Tax (Exercises)dimpy dNo ratings yet

- Ordinary DeductionDocument6 pagesOrdinary Deductionar calasangNo ratings yet

- Allowable Deductions in The Gross Estate Under TRADocument7 pagesAllowable Deductions in The Gross Estate Under TRASantiago Joanna MarieNo ratings yet

- ReSA B42 TAX First PB Exam - Questions, Answers - SolutionsDocument18 pagesReSA B42 TAX First PB Exam - Questions, Answers - SolutionsPearl Mae De VeasNo ratings yet

- TRAIN LAW - Estate TAX - SUMMARY OF CHANGESDocument10 pagesTRAIN LAW - Estate TAX - SUMMARY OF CHANGESBon BonsNo ratings yet

- Deductions From Gross EstateDocument46 pagesDeductions From Gross EstateARC SVIORNo ratings yet

- Deductions From Gross EstateDocument112 pagesDeductions From Gross EstateLuna CakesNo ratings yet

- Jessa B. Regalario Ms. Tabernilla V-Bsa F. Schedule and Computation of The Tax Estate Tax Imposed On Net EstateDocument8 pagesJessa B. Regalario Ms. Tabernilla V-Bsa F. Schedule and Computation of The Tax Estate Tax Imposed On Net EstatejessaNo ratings yet

- Activity No. 1: Estate Tax (Pages 440-461) : Multiple Choice QuestionsDocument5 pagesActivity No. 1: Estate Tax (Pages 440-461) : Multiple Choice QuestionsSara Andrea SantiagoNo ratings yet

- Tax 02-Lesson 05 - Estate Tax Credit, Distributable Estate, and Estate Tax ReturnsDocument31 pagesTax 02-Lesson 05 - Estate Tax Credit, Distributable Estate, and Estate Tax ReturnsMama MiyaNo ratings yet

- Vanishing DeductionsDocument3 pagesVanishing DeductionsCyrell AsidNo ratings yet

- Estate Tax PDFDocument35 pagesEstate Tax PDFRhea Mae Sa-onoyNo ratings yet

- Tax 2 Module1 Estate TaxationDocument28 pagesTax 2 Module1 Estate TaxationXyza JabiliNo ratings yet

- 03 Deductions From Gross EstateDocument4 pages03 Deductions From Gross Estatelemvin121003No ratings yet

- Shall File A Return Under OathDocument17 pagesShall File A Return Under OathMixx MineNo ratings yet

- Deductions On Gross Estate Part 1Document19 pagesDeductions On Gross Estate Part 1Angel Clarisse JariolNo ratings yet

- Taxation Report - Valuation of Properties - Vanishing DeductionDocument49 pagesTaxation Report - Valuation of Properties - Vanishing DeductionAnonymous S6CQnxuJcINo ratings yet

- TRAIN LAW - Estate TAxSUMMARY OF CHANGESDocument11 pagesTRAIN LAW - Estate TAxSUMMARY OF CHANGESBon BonsNo ratings yet

- Deduction From The Gross EstateDocument6 pagesDeduction From The Gross EstateEmma Mariz GarciaNo ratings yet

- Estate TaxDocument7 pagesEstate TaxMarie MAy MagtibayNo ratings yet

- Taxation Atty. Macmod, C.P.A. Estate Tax 2020 EditionDocument7 pagesTaxation Atty. Macmod, C.P.A. Estate Tax 2020 EditionKira Lim100% (1)

- ACT26 - Ch04 - Deduction From The Gross EstateDocument7 pagesACT26 - Ch04 - Deduction From The Gross EstateMark BajacanNo ratings yet

- Taxation On Estates and TrustsDocument31 pagesTaxation On Estates and TrustsAndrea Renice S. FerriolNo ratings yet

- Deductions From Gross EstateDocument3 pagesDeductions From Gross EstateMark Lawrence YusiNo ratings yet

- Taxation 1 Mod 3Document45 pagesTaxation 1 Mod 3Harui Hani-31No ratings yet

- Transfer Estate Tax Chapter 1Document33 pagesTransfer Estate Tax Chapter 1cmaepitoc21No ratings yet

- Transfer TaxesDocument101 pagesTransfer TaxesAngelo IvanNo ratings yet

- HQ11 - Estate TaxationDocument18 pagesHQ11 - Estate TaxationJane Oblena100% (1)

- Estate Tax Payable - 1625701751Document17 pagesEstate Tax Payable - 1625701751T-121-Gutierrez, GwynethNo ratings yet

- Prelim Tax 2Document13 pagesPrelim Tax 2Joseph Mangahas50% (2)

- Chapter 7 Deduction For Gross EstatesDocument19 pagesChapter 7 Deduction For Gross Estatesmendonesmariza2No ratings yet

- Estate TaxDocument5 pagesEstate Taxericamaecarpila0520No ratings yet

- ARTICLE - Death, Real Estate, and Estate TaxesDocument10 pagesARTICLE - Death, Real Estate, and Estate TaxestemporiariNo ratings yet

- TAX With TRAIN LAW - Transfer and Business TaxDocument61 pagesTAX With TRAIN LAW - Transfer and Business TaxRamon AngelesNo ratings yet

- Put A Mark On The Letter of Your ChoiceDocument5 pagesPut A Mark On The Letter of Your Choicejhell dela cruzNo ratings yet

- Deduction From Gross EstateDocument41 pagesDeduction From Gross EstateDianne Pearl DelfinNo ratings yet

- Deductions From Gross EstateDocument20 pagesDeductions From Gross EstateJamaica David100% (2)

- Module 2 DEDUCTION FROM GROSS ESTATE AND ESTATE TAX - Part 1Document35 pagesModule 2 DEDUCTION FROM GROSS ESTATE AND ESTATE TAX - Part 1Venice Marie ArroyoNo ratings yet

- Module 2 - Estate TaxDocument14 pagesModule 2 - Estate TaxHaidee Flavier SabidoNo ratings yet

- 3 - Estate TaxDocument10 pages3 - Estate TaxVernnNo ratings yet

- Estate Tax - A Tax Levied On The Transmission of Properties From A To His Lawful Heirs andDocument6 pagesEstate Tax - A Tax Levied On The Transmission of Properties From A To His Lawful Heirs andAngelyn SamandeNo ratings yet

- Lesson Handouts ARGDocument26 pagesLesson Handouts ARGsamantha sisonNo ratings yet

- MPT Staff Rules of Service - Latest XXXYDocument126 pagesMPT Staff Rules of Service - Latest XXXYwaheedNo ratings yet

- Associated Labor Union v. BorromeoDocument2 pagesAssociated Labor Union v. BorromeoJaneen ZamudioNo ratings yet

- Wandering Heroes of Ogre Gate - House of Paper ShadowsDocument97 pagesWandering Heroes of Ogre Gate - House of Paper ShadowsSamuel Smallman75% (4)

- Controller Job DescriptionDocument1 pageController Job Descriptionmarco thompson100% (2)

- Lavon 2004Document7 pagesLavon 2004Tazkiyatul Asma'iNo ratings yet

- Abubakar 2014Document13 pagesAbubakar 2014tommy maulanaNo ratings yet

- SF Hose Cat 2017Document40 pagesSF Hose Cat 2017Ahmed Abdelaty100% (1)

- Role Based Training - Managing Work (Projects) in PlanviewDocument89 pagesRole Based Training - Managing Work (Projects) in PlanviewMark StrolenbergNo ratings yet

- Geotechnical Properties of Dublin Boulder ClayDocument18 pagesGeotechnical Properties of Dublin Boulder ClayBLPgalwayNo ratings yet

- Sisymposiumharrisburgpaworkshoptraceyvincent PDFDocument76 pagesSisymposiumharrisburgpaworkshoptraceyvincent PDFNancyNo ratings yet

- Eskom, ABB Reach R1.5bn Settlement For Kusile Cost OverrunDocument3 pagesEskom, ABB Reach R1.5bn Settlement For Kusile Cost OverrunNokukhanya MntamboNo ratings yet

- BVM L230Document156 pagesBVM L230JFrink333No ratings yet

- 3.3.2.3 Lab - Configuring Rapid PVST, PortFast, and BPDU GuardDocument9 pages3.3.2.3 Lab - Configuring Rapid PVST, PortFast, and BPDU Guardsebastian ruiz100% (1)

- 3.03 Lab ClassificationDocument3 pages3.03 Lab ClassificationISWABiologyNo ratings yet

- Bunya Pine: Araucaria BidwilliiDocument10 pagesBunya Pine: Araucaria BidwilliiLinda CarroliNo ratings yet

- Luciano ActivitiesDocument5 pagesLuciano ActivitiesCandela MoretaNo ratings yet

- NSTP Lesson 1Document4 pagesNSTP Lesson 1LACANARIA, ELLE BEA N.No ratings yet

- Terms and Conditions On The Issuance and Use of RCBC Credit CardsDocument15 pagesTerms and Conditions On The Issuance and Use of RCBC Credit CardsGillian Alexis ColegadoNo ratings yet

- UK Terms Shell Collection Granny Square Pattern by Shelley Husband 2014Document5 pagesUK Terms Shell Collection Granny Square Pattern by Shelley Husband 2014Liz MatzNo ratings yet

- AnycubicSlicer - Usage Instructions - V1.0 - ENDocument16 pagesAnycubicSlicer - Usage Instructions - V1.0 - ENkokiNo ratings yet

- Health Education & Behaviour Change CommunicationDocument50 pagesHealth Education & Behaviour Change CommunicationAarya MathewNo ratings yet

- 2018 Trial 1 Biology Questions and Marking SchemeDocument11 pages2018 Trial 1 Biology Questions and Marking SchemeKodhekNo ratings yet

- Primus Overview Catalogue ANGDocument8 pagesPrimus Overview Catalogue ANGpesumasinad0% (1)

- Science 7 q3 Module 3 Week3Document23 pagesScience 7 q3 Module 3 Week3Mary Cila TingalNo ratings yet

- Lacerte Jennifer ResumeDocument1 pageLacerte Jennifer Resumejennifer_lacerteNo ratings yet

- Feynman ParadoxDocument3 pagesFeynman ParadoxBabai KunduNo ratings yet

Download as docx, pdf, or txt

You might also like

- Module 1 - Deductions From Gross EstateDocument68 pagesModule 1 - Deductions From Gross EstateKat Miranda100% (1)

- Feasibility StudyDocument5 pagesFeasibility StudyKath Garcia50% (4)

- Encyclopedia of Chemical Processing - S Lee (Taylor and Francis, 2006) WW PDFDocument3,338 pagesEncyclopedia of Chemical Processing - S Lee (Taylor and Francis, 2006) WW PDFMahfuzur Rahman SiddikyNo ratings yet

- Chapter Exercises DeductionsDocument11 pagesChapter Exercises DeductionsShaine KeefeNo ratings yet

- KH-HO - NG-MAI-CH - NH - 1.xlsx Filename UTF-8''KH-HOÀNG-MAI-CH - NHÀ-1Document549 pagesKH-HO - NG-MAI-CH - NH - 1.xlsx Filename UTF-8''KH-HOÀNG-MAI-CH - NHÀ-1Lê Minh TuânNo ratings yet

- Deductions From Gross EstateDocument34 pagesDeductions From Gross Estatesmosaldana.cvtNo ratings yet

- Chapter 9 Estate Tax DeductionsDocument7 pagesChapter 9 Estate Tax DeductionsEthel Joy Tolentino GamboaNo ratings yet

- Lesson 3Document4 pagesLesson 3Iris Lavigne RojoNo ratings yet

- ACAE 18 - Deduction From Gross EstateDocument4 pagesACAE 18 - Deduction From Gross Estatechen dalitNo ratings yet

- TAX 2 Deductions From The Gross Estate 1PPT.Document24 pagesTAX 2 Deductions From The Gross Estate 1PPT.Franz Ana Marie CuaNo ratings yet

- Deductions: Philippines Gross Estate World Gross Estate Deductible LITDocument3 pagesDeductions: Philippines Gross Estate World Gross Estate Deductible LITMaria LopezNo ratings yet

- Chapter 6 Deductions From The Gross Estate PDFDocument7 pagesChapter 6 Deductions From The Gross Estate PDFDudz MatienzoNo ratings yet

- M5 - Deductions From Gross Estate - Students'Document33 pagesM5 - Deductions From Gross Estate - Students'micaella pasionNo ratings yet

- BusTax - Chapter 3 MODULEDocument8 pagesBusTax - Chapter 3 MODULETimon CarandangNo ratings yet

- Tax 2 4Document9 pagesTax 2 4amlecdeyojNo ratings yet

- X DeductionsDocument11 pagesX Deductionsmariyha PalangganaNo ratings yet

- Estate Tax: Taxation 1Document22 pagesEstate Tax: Taxation 1Jess Guiang CasamorinNo ratings yet

- TAX 2 Deductions From The Gross Estate 1PPTDocument24 pagesTAX 2 Deductions From The Gross Estate 1PPTMichael AquinoNo ratings yet

- Estate Tax 3Document50 pagesEstate Tax 3Lea JoaquinNo ratings yet

- Chapter 2 - Deductions From The Gross EstateDocument9 pagesChapter 2 - Deductions From The Gross EstateElla Marie WicoNo ratings yet

- Estate Tax (Exercises)Document3 pagesEstate Tax (Exercises)dimpy dNo ratings yet

- Ordinary DeductionDocument6 pagesOrdinary Deductionar calasangNo ratings yet

- Allowable Deductions in The Gross Estate Under TRADocument7 pagesAllowable Deductions in The Gross Estate Under TRASantiago Joanna MarieNo ratings yet

- ReSA B42 TAX First PB Exam - Questions, Answers - SolutionsDocument18 pagesReSA B42 TAX First PB Exam - Questions, Answers - SolutionsPearl Mae De VeasNo ratings yet

- TRAIN LAW - Estate TAX - SUMMARY OF CHANGESDocument10 pagesTRAIN LAW - Estate TAX - SUMMARY OF CHANGESBon BonsNo ratings yet

- Deductions From Gross EstateDocument46 pagesDeductions From Gross EstateARC SVIORNo ratings yet

- Deductions From Gross EstateDocument112 pagesDeductions From Gross EstateLuna CakesNo ratings yet

- Jessa B. Regalario Ms. Tabernilla V-Bsa F. Schedule and Computation of The Tax Estate Tax Imposed On Net EstateDocument8 pagesJessa B. Regalario Ms. Tabernilla V-Bsa F. Schedule and Computation of The Tax Estate Tax Imposed On Net EstatejessaNo ratings yet

- Activity No. 1: Estate Tax (Pages 440-461) : Multiple Choice QuestionsDocument5 pagesActivity No. 1: Estate Tax (Pages 440-461) : Multiple Choice QuestionsSara Andrea SantiagoNo ratings yet

- Tax 02-Lesson 05 - Estate Tax Credit, Distributable Estate, and Estate Tax ReturnsDocument31 pagesTax 02-Lesson 05 - Estate Tax Credit, Distributable Estate, and Estate Tax ReturnsMama MiyaNo ratings yet

- Vanishing DeductionsDocument3 pagesVanishing DeductionsCyrell AsidNo ratings yet

- Estate Tax PDFDocument35 pagesEstate Tax PDFRhea Mae Sa-onoyNo ratings yet

- Tax 2 Module1 Estate TaxationDocument28 pagesTax 2 Module1 Estate TaxationXyza JabiliNo ratings yet

- 03 Deductions From Gross EstateDocument4 pages03 Deductions From Gross Estatelemvin121003No ratings yet

- Shall File A Return Under OathDocument17 pagesShall File A Return Under OathMixx MineNo ratings yet

- Deductions On Gross Estate Part 1Document19 pagesDeductions On Gross Estate Part 1Angel Clarisse JariolNo ratings yet

- Taxation Report - Valuation of Properties - Vanishing DeductionDocument49 pagesTaxation Report - Valuation of Properties - Vanishing DeductionAnonymous S6CQnxuJcINo ratings yet

- TRAIN LAW - Estate TAxSUMMARY OF CHANGESDocument11 pagesTRAIN LAW - Estate TAxSUMMARY OF CHANGESBon BonsNo ratings yet

- Deduction From The Gross EstateDocument6 pagesDeduction From The Gross EstateEmma Mariz GarciaNo ratings yet

- Estate TaxDocument7 pagesEstate TaxMarie MAy MagtibayNo ratings yet

- Taxation Atty. Macmod, C.P.A. Estate Tax 2020 EditionDocument7 pagesTaxation Atty. Macmod, C.P.A. Estate Tax 2020 EditionKira Lim100% (1)

- ACT26 - Ch04 - Deduction From The Gross EstateDocument7 pagesACT26 - Ch04 - Deduction From The Gross EstateMark BajacanNo ratings yet

- Taxation On Estates and TrustsDocument31 pagesTaxation On Estates and TrustsAndrea Renice S. FerriolNo ratings yet

- Deductions From Gross EstateDocument3 pagesDeductions From Gross EstateMark Lawrence YusiNo ratings yet

- Taxation 1 Mod 3Document45 pagesTaxation 1 Mod 3Harui Hani-31No ratings yet

- Transfer Estate Tax Chapter 1Document33 pagesTransfer Estate Tax Chapter 1cmaepitoc21No ratings yet

- Transfer TaxesDocument101 pagesTransfer TaxesAngelo IvanNo ratings yet

- HQ11 - Estate TaxationDocument18 pagesHQ11 - Estate TaxationJane Oblena100% (1)

- Estate Tax Payable - 1625701751Document17 pagesEstate Tax Payable - 1625701751T-121-Gutierrez, GwynethNo ratings yet

- Prelim Tax 2Document13 pagesPrelim Tax 2Joseph Mangahas50% (2)

- Chapter 7 Deduction For Gross EstatesDocument19 pagesChapter 7 Deduction For Gross Estatesmendonesmariza2No ratings yet

- Estate TaxDocument5 pagesEstate Taxericamaecarpila0520No ratings yet

- ARTICLE - Death, Real Estate, and Estate TaxesDocument10 pagesARTICLE - Death, Real Estate, and Estate TaxestemporiariNo ratings yet

- TAX With TRAIN LAW - Transfer and Business TaxDocument61 pagesTAX With TRAIN LAW - Transfer and Business TaxRamon AngelesNo ratings yet

- Put A Mark On The Letter of Your ChoiceDocument5 pagesPut A Mark On The Letter of Your Choicejhell dela cruzNo ratings yet

- Deduction From Gross EstateDocument41 pagesDeduction From Gross EstateDianne Pearl DelfinNo ratings yet

- Deductions From Gross EstateDocument20 pagesDeductions From Gross EstateJamaica David100% (2)

- Module 2 DEDUCTION FROM GROSS ESTATE AND ESTATE TAX - Part 1Document35 pagesModule 2 DEDUCTION FROM GROSS ESTATE AND ESTATE TAX - Part 1Venice Marie ArroyoNo ratings yet

- Module 2 - Estate TaxDocument14 pagesModule 2 - Estate TaxHaidee Flavier SabidoNo ratings yet

- 3 - Estate TaxDocument10 pages3 - Estate TaxVernnNo ratings yet

- Estate Tax - A Tax Levied On The Transmission of Properties From A To His Lawful Heirs andDocument6 pagesEstate Tax - A Tax Levied On The Transmission of Properties From A To His Lawful Heirs andAngelyn SamandeNo ratings yet

- Lesson Handouts ARGDocument26 pagesLesson Handouts ARGsamantha sisonNo ratings yet

- MPT Staff Rules of Service - Latest XXXYDocument126 pagesMPT Staff Rules of Service - Latest XXXYwaheedNo ratings yet

- Associated Labor Union v. BorromeoDocument2 pagesAssociated Labor Union v. BorromeoJaneen ZamudioNo ratings yet

- Wandering Heroes of Ogre Gate - House of Paper ShadowsDocument97 pagesWandering Heroes of Ogre Gate - House of Paper ShadowsSamuel Smallman75% (4)

- Controller Job DescriptionDocument1 pageController Job Descriptionmarco thompson100% (2)

- Lavon 2004Document7 pagesLavon 2004Tazkiyatul Asma'iNo ratings yet

- Abubakar 2014Document13 pagesAbubakar 2014tommy maulanaNo ratings yet

- SF Hose Cat 2017Document40 pagesSF Hose Cat 2017Ahmed Abdelaty100% (1)

- Role Based Training - Managing Work (Projects) in PlanviewDocument89 pagesRole Based Training - Managing Work (Projects) in PlanviewMark StrolenbergNo ratings yet

- Geotechnical Properties of Dublin Boulder ClayDocument18 pagesGeotechnical Properties of Dublin Boulder ClayBLPgalwayNo ratings yet

- Sisymposiumharrisburgpaworkshoptraceyvincent PDFDocument76 pagesSisymposiumharrisburgpaworkshoptraceyvincent PDFNancyNo ratings yet

- Eskom, ABB Reach R1.5bn Settlement For Kusile Cost OverrunDocument3 pagesEskom, ABB Reach R1.5bn Settlement For Kusile Cost OverrunNokukhanya MntamboNo ratings yet

- BVM L230Document156 pagesBVM L230JFrink333No ratings yet

- 3.3.2.3 Lab - Configuring Rapid PVST, PortFast, and BPDU GuardDocument9 pages3.3.2.3 Lab - Configuring Rapid PVST, PortFast, and BPDU Guardsebastian ruiz100% (1)

- 3.03 Lab ClassificationDocument3 pages3.03 Lab ClassificationISWABiologyNo ratings yet

- Bunya Pine: Araucaria BidwilliiDocument10 pagesBunya Pine: Araucaria BidwilliiLinda CarroliNo ratings yet

- Luciano ActivitiesDocument5 pagesLuciano ActivitiesCandela MoretaNo ratings yet

- NSTP Lesson 1Document4 pagesNSTP Lesson 1LACANARIA, ELLE BEA N.No ratings yet

- Terms and Conditions On The Issuance and Use of RCBC Credit CardsDocument15 pagesTerms and Conditions On The Issuance and Use of RCBC Credit CardsGillian Alexis ColegadoNo ratings yet

- UK Terms Shell Collection Granny Square Pattern by Shelley Husband 2014Document5 pagesUK Terms Shell Collection Granny Square Pattern by Shelley Husband 2014Liz MatzNo ratings yet

- AnycubicSlicer - Usage Instructions - V1.0 - ENDocument16 pagesAnycubicSlicer - Usage Instructions - V1.0 - ENkokiNo ratings yet

- Health Education & Behaviour Change CommunicationDocument50 pagesHealth Education & Behaviour Change CommunicationAarya MathewNo ratings yet

- 2018 Trial 1 Biology Questions and Marking SchemeDocument11 pages2018 Trial 1 Biology Questions and Marking SchemeKodhekNo ratings yet

- Primus Overview Catalogue ANGDocument8 pagesPrimus Overview Catalogue ANGpesumasinad0% (1)

- Science 7 q3 Module 3 Week3Document23 pagesScience 7 q3 Module 3 Week3Mary Cila TingalNo ratings yet

- Lacerte Jennifer ResumeDocument1 pageLacerte Jennifer Resumejennifer_lacerteNo ratings yet

- Feynman ParadoxDocument3 pagesFeynman ParadoxBabai KunduNo ratings yet