Download as pdf or txt

You might also like

- Question Bank AuditingiDocument51 pagesQuestion Bank AuditingiNever Gonondo0% (1)

- CMA Srilanka PDFDocument7 pagesCMA Srilanka PDFFerry SihalohoNo ratings yet

- Contractor's Ledger 1Document4 pagesContractor's Ledger 1Fareha RiazNo ratings yet

- Alcatraz Analysis (With Explanations)Document16 pagesAlcatraz Analysis (With Explanations)Raul Dolo Quinones100% (1)

- Summer Exam-2018 Pakistan Institute of Public Finance AccountantsDocument2 pagesSummer Exam-2018 Pakistan Institute of Public Finance Accountantssaqib shahzadNo ratings yet

- PMAD RulesDocument7 pagesPMAD RulesMasood Ahmed MakaNo ratings yet

- PMADDocument7 pagesPMADDanish RehmanNo ratings yet

- Part-I: Pakistan Institute of Public Finance Accountants Summer Exam-2019Document1 pagePart-I: Pakistan Institute of Public Finance Accountants Summer Exam-2019Chand SoorajNo ratings yet

- Audit Assurance S-23Document2 pagesAudit Assurance S-23Rana Sunny KhokharNo ratings yet

- Summer 13Document28 pagesSummer 13Adnan SethiNo ratings yet

- 21s CgaDocument2 pages21s CgaALISA ASIFNo ratings yet

- 22s CgaDocument2 pages22s CgaALISA ASIFNo ratings yet

- FAM Papers Upto 2008Document34 pagesFAM Papers Upto 2008danishrehman2011No ratings yet

- Audit Questions 5Document5 pagesAudit Questions 5Humayun KhanNo ratings yet

- B8af108 Audit Summer 2018 Exam PaperDocument6 pagesB8af108 Audit Summer 2018 Exam PaperEizam Ben JetteyNo ratings yet

- PFM S-22Document2 pagesPFM S-22Rana Sunny KhokharNo ratings yet

- Summer Exam-2019 Pakistan Institute of Public Finance AccountantsDocument2 pagesSummer Exam-2019 Pakistan Institute of Public Finance AccountantsChand SoorajNo ratings yet

- SpecimenPaper MADocument14 pagesSpecimenPaper MANatalie Andria WeeramanthriNo ratings yet

- Winter Exam-2018 Pakistan Institute of Public Finance AccountantsDocument2 pagesWinter Exam-2018 Pakistan Institute of Public Finance AccountantsArifNo ratings yet

- University of ZimbabweDocument3 pagesUniversity of ZimbabweZvikomborero Lisah KamupiraNo ratings yet

- Federal Public Service Commission: Roll NumberDocument1 pageFederal Public Service Commission: Roll NumberSyed Ali NaqiNo ratings yet

- PFM W-21 Already PrintedDocument1 pagePFM W-21 Already PrintedRana Sunny KhokharNo ratings yet

- ACC302 THEFinal A 2021 SpringDocument5 pagesACC302 THEFinal A 2021 Springayushi kNo ratings yet

- Audit Updated Past PapersDocument265 pagesAudit Updated Past PapershamizNo ratings yet

- 0102 Managerial Economics and Financial AnalysisDocument7 pages0102 Managerial Economics and Financial AnalysisFozia PanhwerNo ratings yet

- Practice Manual: © The Institute of Chartered Accountants of IndiaDocument4 pagesPractice Manual: © The Institute of Chartered Accountants of IndiaBhagwat ThakkerNo ratings yet

- 2013 PatternDocument232 pages2013 PatternPrayank RajeNo ratings yet

- (2013 Pattern) PDFDocument230 pages(2013 Pattern) PDFSanket SonawaneNo ratings yet

- Lecture 55 AssignmentDocument3 pagesLecture 55 AssignmentMuneeb UllahNo ratings yet

- Faculty of Business Management BAC 215: Auditing: TH THDocument2 pagesFaculty of Business Management BAC 215: Auditing: TH THMichael AronNo ratings yet

- CPT Model Test Paper 1Document150 pagesCPT Model Test Paper 1Tanya Hughes100% (1)

- Ininstitute of Management Technology: Centre For Distance LearningDocument2 pagesIninstitute of Management Technology: Centre For Distance Learningabhimani5472No ratings yet

- CA Inter Audit MTP 1 May 24Document16 pagesCA Inter Audit MTP 1 May 24Sans RecourseNo ratings yet

- Industrial Engineering Question Bank Vishal Shinde Kbtcoe NashikDocument4 pagesIndustrial Engineering Question Bank Vishal Shinde Kbtcoe NashikAashishNo ratings yet

- PART A - Performance of Audit and ReportingDocument9 pagesPART A - Performance of Audit and Reportingsidra awanNo ratings yet

- Audit and Internal ReviewDocument3 pagesAudit and Internal ReviewChristen Castillo100% (1)

- (2019 Pattern) - April 2022Document237 pages(2019 Pattern) - April 2022Kadam RohitNo ratings yet

- Group: Departmental Examination For Auditors, March-2014Document6 pagesGroup: Departmental Examination For Auditors, March-2014maxNo ratings yet

- Punjab Finance Sector: Attempt All QuestionsDocument1 pagePunjab Finance Sector: Attempt All Questionslost_battalion10No ratings yet

- Auditing: Professional 1 Examination - April 2015Document17 pagesAuditing: Professional 1 Examination - April 2015Issa BoyNo ratings yet

- Auditing June 2011 ExamDocument8 pagesAuditing June 2011 ExammohedNo ratings yet

- Audit MCQDocument299 pagesAudit MCQVamseenath N RNo ratings yet

- Operations MGMT - PG A - B - II 13-15 - Pramod S.Document3 pagesOperations MGMT - PG A - B - II 13-15 - Pramod S.Abhishek RaghavNo ratings yet

- Audit Test 7 QP Ch#14 (ISA 705,706)Document1 pageAudit Test 7 QP Ch#14 (ISA 705,706)HussainNo ratings yet

- Appendix III (Irem) Examination For Indian Railway Accounts Staff - Ldce Question Papers - SC Rly. - Papers One & Two - 2012 YearDocument8 pagesAppendix III (Irem) Examination For Indian Railway Accounts Staff - Ldce Question Papers - SC Rly. - Papers One & Two - 2012 Yearceportal100% (1)

- Mba851 2020Document2 pagesMba851 2020DORNU SIMEON NGBAANo ratings yet

- AA133.AUDIL II Question CMA May 2022 ExaminationDocument7 pagesAA133.AUDIL II Question CMA May 2022 Examinationkm nafizNo ratings yet

- Module 2Document2 pagesModule 2Rajveer SaeNo ratings yet

- UntitledDocument69 pagesUntitledAhiaanNo ratings yet

- Exemption Scoring 60 Questions CA CMA CS INTER MAY NOV 2023 1Document68 pagesExemption Scoring 60 Questions CA CMA CS INTER MAY NOV 2023 1pvvpnx5djvNo ratings yet

- MMPC 014Document6 pagesMMPC 014Pawan ShokeenNo ratings yet

- Qms-Exam-Paper IADocument9 pagesQms-Exam-Paper IAALOKE GANGULYNo ratings yet

- Capital BudgetingDocument75 pagesCapital Budgetingsubroshakar gamerNo ratings yet

- All Mcqs Are Compulsory Question No. 1 Is Compulsory. Attempt Any Four Questions From The RestDocument10 pagesAll Mcqs Are Compulsory Question No. 1 Is Compulsory. Attempt Any Four Questions From The Restritz meshNo ratings yet

- 3.2 Advanced Audit Assurance PDFDocument24 pages3.2 Advanced Audit Assurance PDFmohedNo ratings yet

- Department of Automobile Engineering: Question Bank Bam8E4-Bme009-Total Quality ManagementDocument5 pagesDepartment of Automobile Engineering: Question Bank Bam8E4-Bme009-Total Quality ManagementLeon MathaiosNo ratings yet

- BUSN7054 Take Home Final Exam S1 2020Document14 pagesBUSN7054 Take Home Final Exam S1 2020Li XiangNo ratings yet

- Oscm QPDocument8 pagesOscm QPjpkassociates2019No ratings yet

- Set No. 1: Code No: R4203ADocument4 pagesSet No. 1: Code No: R4203AsivaenotesNo ratings yet

- End Term Examination: From Each UnitDocument2 pagesEnd Term Examination: From Each UnitAbhishek MittalNo ratings yet

- The Court For A Warrant For His Custody Pending TrialDocument1 pageThe Court For A Warrant For His Custody Pending TrialFareha RiazNo ratings yet

- VIIIDocument1 pageVIIIFareha RiazNo ratings yet

- Financial ControlDocument1 pageFinancial ControlFareha RiazNo ratings yet

- Acts Relating To Prisons and Prisoners Rule1Document1 pageActs Relating To Prisons and Prisoners Rule1Fareha RiazNo ratings yet

- HR CodesDocument51 pagesHR CodesFareha RiazNo ratings yet

- Job Description of MInes DepartmentDocument3 pagesJob Description of MInes DepartmentFareha RiazNo ratings yet

- Factories ActDocument1 pageFactories ActFareha RiazNo ratings yet

- Chapter - XV: Fund ElementDocument223 pagesChapter - XV: Fund ElementFareha RiazNo ratings yet

- Wage TypeDocument4 pagesWage TypeFareha RiazNo ratings yet

- GFR CH 2Document6 pagesGFR CH 2Fareha RiazNo ratings yet

- Section 14: Substantially Financed From Union or State RevenuesDocument5 pagesSection 14: Substantially Financed From Union or State RevenuesFareha RiazNo ratings yet

- IMSP 06 6-2-1 Part Running Bill PaymentsDocument6 pagesIMSP 06 6-2-1 Part Running Bill PaymentsFareha RiazNo ratings yet

- 2011LHC4023Document6 pages2011LHC4023Fareha RiazNo ratings yet

- Appropriations & Re-AppropriationDocument6 pagesAppropriations & Re-AppropriationFareha RiazNo ratings yet

- GFR ch1Document4 pagesGFR ch1Fareha RiazNo ratings yet

- Chapter - 6 Rules Relating To Classification of Losses in Government AccountsDocument2 pagesChapter - 6 Rules Relating To Classification of Losses in Government AccountsFareha RiazNo ratings yet

- Chapter - 5 Classification of Recoveries of Expenditure in Government AccountsDocument2 pagesChapter - 5 Classification of Recoveries of Expenditure in Government AccountsFareha RiazNo ratings yet

- 1534 - 2015 11 02 11 49 00 - 1446445141 PDFDocument134 pages1534 - 2015 11 02 11 49 00 - 1446445141 PDFFareha RiazNo ratings yet

- Chapter - 8 Important General Orders Governing ClassificationDocument4 pagesChapter - 8 Important General Orders Governing ClassificationFareha RiazNo ratings yet

- Chapter 7 - Miscellaneous RulesDocument2 pagesChapter 7 - Miscellaneous RulesFareha RiazNo ratings yet

- Stores: Fictitious Stock Adjustments Are Strictly Prohibited, For E.GDocument6 pagesStores: Fictitious Stock Adjustments Are Strictly Prohibited, For E.GFareha RiazNo ratings yet

- Stores Part 2Document3 pagesStores Part 2Fareha RiazNo ratings yet

- Overview of Running Account Bill (Form 26)Document4 pagesOverview of Running Account Bill (Form 26)Fareha RiazNo ratings yet

- 2017 Summer Question PaperDocument3 pages2017 Summer Question PaperFareha RiazNo ratings yet

- Work Accounts 2Document5 pagesWork Accounts 2Fareha RiazNo ratings yet

- RollDocument5 pagesRollFareha RiazNo ratings yet

- SolutionDocument4 pagesSolutionFareha RiazNo ratings yet

- P5-4, 6 Dan 8Document18 pagesP5-4, 6 Dan 8ramaNo ratings yet

- Avtar Singh NetworthDocument2 pagesAvtar Singh Networthprince.gill07No ratings yet

- Basic Concepts in Management AccountingDocument9 pagesBasic Concepts in Management AccountingKeach Harrel CabagayNo ratings yet

- Financing Resources - Valuation of Stocks L4AEDocument57 pagesFinancing Resources - Valuation of Stocks L4AETacitus KilgoreNo ratings yet

- LeverageDocument7 pagesLeverageChiranjeev RoutrayNo ratings yet

- Solution Manual Managerial Accounting Hansen Mowen 8th Editions CH 6Document44 pagesSolution Manual Managerial Accounting Hansen Mowen 8th Editions CH 6Riki HalimNo ratings yet

- Sample Learning Module BTECH Business 2Document17 pagesSample Learning Module BTECH Business 2jaydaman08No ratings yet

- Free Cash Flows FCFF & FcfeDocument56 pagesFree Cash Flows FCFF & FcfeYagyaaGoyalNo ratings yet

- W5 - AS2 - Deferred TaxesDocument2 pagesW5 - AS2 - Deferred TaxesJere Mae MarananNo ratings yet

- Disclosure Statement Pursuant To The Pink Basic Disclosure GuidelinesDocument24 pagesDisclosure Statement Pursuant To The Pink Basic Disclosure GuidelinesRenato GoncalvesNo ratings yet

- PFRS SGV PDFDocument18 pagesPFRS SGV PDFJonathan Javier GajeNo ratings yet

- Announcement of Interim Results For The Six Months Ended 30 June 2020Document45 pagesAnnouncement of Interim Results For The Six Months Ended 30 June 2020in resNo ratings yet

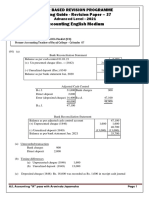

- Accounting English Medium: Paper Based Revision Programme Marking Guide - Revision Paper - 37Document6 pagesAccounting English Medium: Paper Based Revision Programme Marking Guide - Revision Paper - 37Malar SrirengarajahNo ratings yet

- Performance Evaluation of Uttara Bank LTDDocument49 pagesPerformance Evaluation of Uttara Bank LTDConnorLokmanNo ratings yet

- ACCT4011 - Lecture 2 - Business Combinations II (Revised) (Class)Document12 pagesACCT4011 - Lecture 2 - Business Combinations II (Revised) (Class)DaveKwokNo ratings yet

- AFIN210 Midterm Exam 2017Document5 pagesAFIN210 Midterm Exam 2017William C ManelaNo ratings yet

- Asset Liability Management at HDFC BankDocument31 pagesAsset Liability Management at HDFC BankwebstdsnrNo ratings yet

- AccountingDocument8 pagesAccountingLaurio, Genebabe TagubarasNo ratings yet

- Cost of CapitalDocument2 pagesCost of Capitalkomal100% (1)

- Comparative Financial Statements: Heritage Antiquing Services Comparative Balance Sheet (Dollars in Thousands)Document2 pagesComparative Financial Statements: Heritage Antiquing Services Comparative Balance Sheet (Dollars in Thousands)Rose BaynaNo ratings yet

- Additional Funds Needed - Exercises - QuestionsDocument2 pagesAdditional Funds Needed - Exercises - QuestionsDANE MATTHEW PILAPILNo ratings yet

- Aspire Global Q2-21-ReportDocument25 pagesAspire Global Q2-21-Reportl chanNo ratings yet

- Mind Map of Accounting ElementsDocument4 pagesMind Map of Accounting ElementsSapphire Au MartinNo ratings yet

- Day 1 - Overview of The SAP FI-CO Module PDFDocument13 pagesDay 1 - Overview of The SAP FI-CO Module PDFkyushineNo ratings yet

- Financial Accounting: Belverd E. Needles, Jr. Marian PowersDocument64 pagesFinancial Accounting: Belverd E. Needles, Jr. Marian PowersTugara AmosNo ratings yet

- Pricing Quiz With SolutionDocument4 pagesPricing Quiz With SolutionShieryl-Joy Postrero PorrasNo ratings yet

- Sports Bar Business PlanDocument35 pagesSports Bar Business PlanMarco Gómez Caballero100% (2)

- Automotive Axles Result UpdatedDocument10 pagesAutomotive Axles Result UpdatedAngel BrokingNo ratings yet

- Fsa 2011 15 PDFDocument253 pagesFsa 2011 15 PDFalizaNo ratings yet