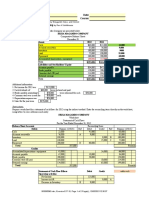

National Foods LTD FY21 Earnings Update

National Foods LTD FY21 Earnings Update

You might also like

- Financial Analysis of - Toys "R" Us, Inc.Document30 pagesFinancial Analysis of - Toys "R" Us, Inc.Arabi AsadNo ratings yet

- UAE Equity Research - Agthia Group 4Q22 - First Look NoteDocument5 pagesUAE Equity Research - Agthia Group 4Q22 - First Look Notexen101No ratings yet

- UAE Equity Research: First Look Note - 3Q22Document5 pagesUAE Equity Research: First Look Note - 3Q22xen101No ratings yet

- Top Stories:: THU 11 APR 2024Document3 pagesTop Stories:: THU 11 APR 2024philnabank1217No ratings yet

- Ceylon Cold Stores PLC: Limited Disruptions To Support CCS's Growth AvenuesDocument3 pagesCeylon Cold Stores PLC: Limited Disruptions To Support CCS's Growth AvenuesantiqurrNo ratings yet

- 536248112021255dabur India Limited - 20210806Document5 pages536248112021255dabur India Limited - 20210806Michelle CastelinoNo ratings yet

- Earnings Update DANGCEM 2021FY 1Document6 pagesEarnings Update DANGCEM 2021FY 1kazeemsheriff8No ratings yet

- Stove Kraft-1QFY22 Result Update - 01 August 2021Document7 pagesStove Kraft-1QFY22 Result Update - 01 August 2021Raghu KuchiNo ratings yet

- Granules - India BP - Wealth 151121Document7 pagesGranules - India BP - Wealth 151121Lakshay SainiNo ratings yet

- JollibeeDocument4 pagesJollibeeJoyce C.No ratings yet

- VMART Q4FY22 ResultDocument6 pagesVMART Q4FY22 ResultKhush GosraniNo ratings yet

- Coal India (COAL IN) : Q4FY19 Result UpdateDocument6 pagesCoal India (COAL IN) : Q4FY19 Result Updatesaran21No ratings yet

- Godrej Consumer Products Result Update - Q1FY23Document4 pagesGodrej Consumer Products Result Update - Q1FY23Prity KumariNo ratings yet

- Padenga Holdings FY22 Earnings UpdateDocument3 pagesPadenga Holdings FY22 Earnings UpdateMichael MatambanadzoNo ratings yet

- Bayer Cropscience (BYRCS IN) : Q1FY21 Result UpdateDocument7 pagesBayer Cropscience (BYRCS IN) : Q1FY21 Result UpdateChockalingam SundharNo ratings yet

- Motilal Oswal On Devyani InternationalDocument10 pagesMotilal Oswal On Devyani InternationalbapianshumanNo ratings yet

- q2 2021 Results AnnouncementDocument71 pagesq2 2021 Results AnnouncementmarceloNo ratings yet

- Suryoday Small Finance Bank Q1FY24 Result Update Centrum 11082023Document13 pagesSuryoday Small Finance Bank Q1FY24 Result Update Centrum 11082023yoursaaryaNo ratings yet

- Cpin 130524 PtosDocument4 pagesCpin 130524 Ptosmaradona ligaNo ratings yet

- 1Q21 Profits Jump 23.5% Y/y, in Line With Estimates: Century Pacific Food, IncDocument7 pages1Q21 Profits Jump 23.5% Y/y, in Line With Estimates: Century Pacific Food, IncJajahinaNo ratings yet

- CNPF Sustains Growth Momentum in 3Q21: Century Pacific Food, IncDocument8 pagesCNPF Sustains Growth Momentum in 3Q21: Century Pacific Food, IncJajahinaNo ratings yet

- Hold Hindustan Unilever: Strong Performance Inflation Pressure Continues To PersistDocument13 pagesHold Hindustan Unilever: Strong Performance Inflation Pressure Continues To PersistAbhishek SaxenaNo ratings yet

- Fineorg 25 5 23 PLDocument8 pagesFineorg 25 5 23 PLSubhash MsNo ratings yet

- Indofood CBP: Navigating WellDocument11 pagesIndofood CBP: Navigating WellAbimanyu LearingNo ratings yet

- Weekly Wrap: Recovery Hopes Bolster PCOMP Above 6,600Document2 pagesWeekly Wrap: Recovery Hopes Bolster PCOMP Above 6,600Romel Alvendia ValenciaNo ratings yet

- HSIE Results Daily - 04 August 21-202108040822126132901Document9 pagesHSIE Results Daily - 04 August 21-202108040822126132901Michelle CastelinoNo ratings yet

- DNL 1Q21 Earnings Grow 35% Y/y, Ahead of Estimates: D&L Industries, IncDocument9 pagesDNL 1Q21 Earnings Grow 35% Y/y, Ahead of Estimates: D&L Industries, IncJajahinaNo ratings yet

- Financial AnalysisDocument14 pagesFinancial Analysismuzaffarovh271No ratings yet

- ICICI Securities REDUCE on Adani Wilmar With 6 DOWNSIDE ProfitabilityDocument8 pagesICICI Securities REDUCE on Adani Wilmar With 6 DOWNSIDE ProfitabilityPratham IngaleNo ratings yet

- Quarterly Update Q1FY22: Krishna Institute of Medical Sciences LTDDocument10 pagesQuarterly Update Q1FY22: Krishna Institute of Medical Sciences LTDhackmaverickNo ratings yet

- Nirmal Bang PDFDocument11 pagesNirmal Bang PDFBook MonkNo ratings yet

- Varun Beverages Q1CY22 Result UpdateDocument5 pagesVarun Beverages Q1CY22 Result UpdateBaria VirenNo ratings yet

- 2Q FY22 Financial Results Presentation: 22 October 2021Document58 pages2Q FY22 Financial Results Presentation: 22 October 2021chaitanya varma ChekuriNo ratings yet

- Burger King India (BURGERKI IN) : Q2FY22 Result UpdateDocument8 pagesBurger King India (BURGERKI IN) : Q2FY22 Result UpdatebradburywillsNo ratings yet

- Asian-Paints Broker ReportDocument7 pagesAsian-Paints Broker Reportsj singhNo ratings yet

- Centrum Dabur India Company UpdateDocument7 pagesCentrum Dabur India Company UpdateprasaadrajputNo ratings yet

- SH Kelkar: All-Round Performance Outlook Remains StrongDocument8 pagesSH Kelkar: All-Round Performance Outlook Remains StrongJehan BhadhaNo ratings yet

- Butterfly Gandhimathi Appliances LTD - Stock Update - 01.12.2021-1Document12 pagesButterfly Gandhimathi Appliances LTD - Stock Update - 01.12.2021-1sundar iyerNo ratings yet

- V Guard Industries Q3 FY22 Results PresentationDocument17 pagesV Guard Industries Q3 FY22 Results PresentationRATHINo ratings yet

- Raymond-Q2FY22-RU LKPDocument9 pagesRaymond-Q2FY22-RU LKP56 AA Prathamesh WarangNo ratings yet

- 1Q FY 2021-22 Financial ResultsDocument54 pages1Q FY 2021-22 Financial Resultsaditya tripathiNo ratings yet

- Page Industries: Revenue Growth Improves While Margins DeclineDocument8 pagesPage Industries: Revenue Growth Improves While Margins DeclinePuneet367No ratings yet

- Edita 3Q2023 Earnings Release E v4Document10 pagesEdita 3Q2023 Earnings Release E v4Habiba HishamNo ratings yet

- 211428182023567dabur India Limited - 20230808Document5 pages211428182023567dabur India Limited - 20230808Jigar PitrodaNo ratings yet

- Indofood Sukses Makmur TBK (INDF IJ) : Strong Performance From All SegmentsDocument6 pagesIndofood Sukses Makmur TBK (INDF IJ) : Strong Performance From All SegmentsPutu Chantika Putri DhammayantiNo ratings yet

- RIL 3Q FY24 Analyst Presentation 19jan24Document55 pagesRIL 3Q FY24 Analyst Presentation 19jan24meetpanchal172006No ratings yet

- Earnings Release - 01.30.2023 FINALDocument20 pagesEarnings Release - 01.30.2023 FINALDuangjitr WongNo ratings yet

- Infosys (INFO IN) : Q1FY22 Result UpdateDocument13 pagesInfosys (INFO IN) : Q1FY22 Result UpdatePrahladNo ratings yet

- Mrs. Bectors Food Specialities 04062024 AcDocument6 pagesMrs. Bectors Food Specialities 04062024 AcgreyistariNo ratings yet

- Indofood CBP Sukses Makmur: Equity ResearchDocument5 pagesIndofood CBP Sukses Makmur: Equity ResearchAbimanyu LearingNo ratings yet

- Income Statement Analysis of Vitarich CorporationDocument11 pagesIncome Statement Analysis of Vitarich CorporationLynnie Jane JauculanNo ratings yet

- Infosys (INFO IN) : Q1FY21 Result UpdateDocument14 pagesInfosys (INFO IN) : Q1FY21 Result UpdatewhitenagarNo ratings yet

- UNVR SekuritasDocument7 pagesUNVR Sekuritasfaizal ardiNo ratings yet

- Financial Highlights: Values in R$ ('000)Document33 pagesFinancial Highlights: Values in R$ ('000)renatoNo ratings yet

- Nestle India: Project RURBAN To Support Strong Growth Inflationary Clouds RemainDocument11 pagesNestle India: Project RURBAN To Support Strong Growth Inflationary Clouds Remainkrishna_buntyNo ratings yet

- Prabhudas Lilladher Apar Industries Q2FY24 Results ReviewDocument7 pagesPrabhudas Lilladher Apar Industries Q2FY24 Results ReviewyoursaaryaNo ratings yet

- CTEC 2021 4Q Press ReleaseDocument46 pagesCTEC 2021 4Q Press Releasefatso68No ratings yet

- BP Plastics Holding Berhad Outperform : 1HFY21 Above ExpectationDocument4 pagesBP Plastics Holding Berhad Outperform : 1HFY21 Above ExpectationZhi_Ming_Cheah_8136No ratings yet

- Burger King India (BURGERKI IN) : Q4FY21 Result UpdateDocument8 pagesBurger King India (BURGERKI IN) : Q4FY21 Result UpdateSushilNo ratings yet

- Nestle India Equity Research ReportDocument9 pagesNestle India Equity Research ReportDurgesh ShuklaNo ratings yet

- Economic Indicators for East Asia: Input–Output TablesFrom EverandEconomic Indicators for East Asia: Input–Output TablesNo ratings yet

- Business Analysis and Valuation Using Financial Statements Text and Cases 5th Edition Palepu Solutions ManualDocument18 pagesBusiness Analysis and Valuation Using Financial Statements Text and Cases 5th Edition Palepu Solutions Manualdaviddulcieagt6100% (35)

- Infosys Annual Report 2018-19Document1 pageInfosys Annual Report 2018-19Prachi SharmaNo ratings yet

- Introduction To Accounting Practice Exercises: Exercise 1: The Accounting Equation Problem 1.1Document10 pagesIntroduction To Accounting Practice Exercises: Exercise 1: The Accounting Equation Problem 1.1Arbie Joy Olofernes SibilNo ratings yet

- Lecture 8 - Exercises - SolutionDocument8 pagesLecture 8 - Exercises - SolutionIsyraf Hatim Mohd TamizamNo ratings yet

- Chattanooga State AuditDocument78 pagesChattanooga State AuditDan LehrNo ratings yet

- Account AssignmentDocument10 pagesAccount AssignmentkanchanghengNo ratings yet

- Page 1 of 4 Chapter 4 - Intermediate Accounting 3Document4 pagesPage 1 of 4 Chapter 4 - Intermediate Accounting 3happy2408230% (1)

- List of Sub-Object Code - 20160322Document135 pagesList of Sub-Object Code - 20160322Julius AlemanNo ratings yet

- 185f8question BankDocument18 pages185f8question Bank55amonNo ratings yet

- Kelompok 10 - Kelas o - Week 9Document10 pagesKelompok 10 - Kelas o - Week 9willyNo ratings yet

- Decision MakingDocument28 pagesDecision MakingGelyn CruzNo ratings yet

- Chapter 2Document54 pagesChapter 2Léo AudibertNo ratings yet

- Bank Maybank Indonesia Bilingual 31des21 ReleasedDocument350 pagesBank Maybank Indonesia Bilingual 31des21 ReleasedNidaNo ratings yet

- Tata Consultancy ServicesDocument6 pagesTata Consultancy ServicesHarshad PawarNo ratings yet

- Quiz 1-EIB10403 - Oct 2023 ComfirmDocument6 pagesQuiz 1-EIB10403 - Oct 2023 ComfirmprfznvtczdNo ratings yet

- SPSPS DatabaseDocument226 pagesSPSPS DatabaseElc Elc ElcNo ratings yet

- Solutions To Solution E12-1: Chapler 12Document38 pagesSolutions To Solution E12-1: Chapler 12Carlo VillanNo ratings yet

- Tuprag - RTR - Explore Design Workshop Deck - Manage General LedgerDocument26 pagesTuprag - RTR - Explore Design Workshop Deck - Manage General LedgerANISHA ROYNo ratings yet

- Chapter 7 Investment PropertyDocument8 pagesChapter 7 Investment PropertyKrissa Mae Longos100% (2)

- Fabozzi BMAS7 CH04 Bond Price Volatility SolutionsDocument40 pagesFabozzi BMAS7 CH04 Bond Price Volatility Solutionsvishal kanekarNo ratings yet

- Acctg1205 - Chapter 8Document48 pagesAcctg1205 - Chapter 8Elj Grace BaronNo ratings yet

- Capital BudgetingDocument44 pagesCapital Budgetingrisbd appliancesNo ratings yet

- Cpa Review School of The Philippines Mani LaDocument2 pagesCpa Review School of The Philippines Mani LaJustine CruzNo ratings yet

- Name: Date: Instructor: Course: Accounting Principles Primer On Using Excel in AccountingDocument2 pagesName: Date: Instructor: Course: Accounting Principles Primer On Using Excel in AccountingHernando MaulanaNo ratings yet

- Date General Journal Debit CreditDocument14 pagesDate General Journal Debit CreditJalaj GuptaNo ratings yet

- Chapter 1 - Introduction ToDocument30 pagesChapter 1 - Introduction ToCostAcct1No ratings yet

- Sbi q42019-2020Document66 pagesSbi q42019-2020Nihal YnNo ratings yet

- UBT - CBA - Final ProjectDocument24 pagesUBT - CBA - Final ProjectLUKE WHITENo ratings yet

- InternshipDocument30 pagesInternshipSumithra K - Kodaikanal centerNo ratings yet

Download as pdf or txt

You might also like

- Financial Analysis of - Toys "R" Us, Inc.Document30 pagesFinancial Analysis of - Toys "R" Us, Inc.Arabi AsadNo ratings yet

- UAE Equity Research - Agthia Group 4Q22 - First Look NoteDocument5 pagesUAE Equity Research - Agthia Group 4Q22 - First Look Notexen101No ratings yet

- UAE Equity Research: First Look Note - 3Q22Document5 pagesUAE Equity Research: First Look Note - 3Q22xen101No ratings yet

- Top Stories:: THU 11 APR 2024Document3 pagesTop Stories:: THU 11 APR 2024philnabank1217No ratings yet

- Ceylon Cold Stores PLC: Limited Disruptions To Support CCS's Growth AvenuesDocument3 pagesCeylon Cold Stores PLC: Limited Disruptions To Support CCS's Growth AvenuesantiqurrNo ratings yet

- 536248112021255dabur India Limited - 20210806Document5 pages536248112021255dabur India Limited - 20210806Michelle CastelinoNo ratings yet

- Earnings Update DANGCEM 2021FY 1Document6 pagesEarnings Update DANGCEM 2021FY 1kazeemsheriff8No ratings yet

- Stove Kraft-1QFY22 Result Update - 01 August 2021Document7 pagesStove Kraft-1QFY22 Result Update - 01 August 2021Raghu KuchiNo ratings yet

- Granules - India BP - Wealth 151121Document7 pagesGranules - India BP - Wealth 151121Lakshay SainiNo ratings yet

- JollibeeDocument4 pagesJollibeeJoyce C.No ratings yet

- VMART Q4FY22 ResultDocument6 pagesVMART Q4FY22 ResultKhush GosraniNo ratings yet

- Coal India (COAL IN) : Q4FY19 Result UpdateDocument6 pagesCoal India (COAL IN) : Q4FY19 Result Updatesaran21No ratings yet

- Godrej Consumer Products Result Update - Q1FY23Document4 pagesGodrej Consumer Products Result Update - Q1FY23Prity KumariNo ratings yet

- Padenga Holdings FY22 Earnings UpdateDocument3 pagesPadenga Holdings FY22 Earnings UpdateMichael MatambanadzoNo ratings yet

- Bayer Cropscience (BYRCS IN) : Q1FY21 Result UpdateDocument7 pagesBayer Cropscience (BYRCS IN) : Q1FY21 Result UpdateChockalingam SundharNo ratings yet

- Motilal Oswal On Devyani InternationalDocument10 pagesMotilal Oswal On Devyani InternationalbapianshumanNo ratings yet

- q2 2021 Results AnnouncementDocument71 pagesq2 2021 Results AnnouncementmarceloNo ratings yet

- Suryoday Small Finance Bank Q1FY24 Result Update Centrum 11082023Document13 pagesSuryoday Small Finance Bank Q1FY24 Result Update Centrum 11082023yoursaaryaNo ratings yet

- Cpin 130524 PtosDocument4 pagesCpin 130524 Ptosmaradona ligaNo ratings yet

- 1Q21 Profits Jump 23.5% Y/y, in Line With Estimates: Century Pacific Food, IncDocument7 pages1Q21 Profits Jump 23.5% Y/y, in Line With Estimates: Century Pacific Food, IncJajahinaNo ratings yet

- CNPF Sustains Growth Momentum in 3Q21: Century Pacific Food, IncDocument8 pagesCNPF Sustains Growth Momentum in 3Q21: Century Pacific Food, IncJajahinaNo ratings yet

- Hold Hindustan Unilever: Strong Performance Inflation Pressure Continues To PersistDocument13 pagesHold Hindustan Unilever: Strong Performance Inflation Pressure Continues To PersistAbhishek SaxenaNo ratings yet

- Fineorg 25 5 23 PLDocument8 pagesFineorg 25 5 23 PLSubhash MsNo ratings yet

- Indofood CBP: Navigating WellDocument11 pagesIndofood CBP: Navigating WellAbimanyu LearingNo ratings yet

- Weekly Wrap: Recovery Hopes Bolster PCOMP Above 6,600Document2 pagesWeekly Wrap: Recovery Hopes Bolster PCOMP Above 6,600Romel Alvendia ValenciaNo ratings yet

- HSIE Results Daily - 04 August 21-202108040822126132901Document9 pagesHSIE Results Daily - 04 August 21-202108040822126132901Michelle CastelinoNo ratings yet

- DNL 1Q21 Earnings Grow 35% Y/y, Ahead of Estimates: D&L Industries, IncDocument9 pagesDNL 1Q21 Earnings Grow 35% Y/y, Ahead of Estimates: D&L Industries, IncJajahinaNo ratings yet

- Financial AnalysisDocument14 pagesFinancial Analysismuzaffarovh271No ratings yet

- ICICI Securities REDUCE on Adani Wilmar With 6 DOWNSIDE ProfitabilityDocument8 pagesICICI Securities REDUCE on Adani Wilmar With 6 DOWNSIDE ProfitabilityPratham IngaleNo ratings yet

- Quarterly Update Q1FY22: Krishna Institute of Medical Sciences LTDDocument10 pagesQuarterly Update Q1FY22: Krishna Institute of Medical Sciences LTDhackmaverickNo ratings yet

- Nirmal Bang PDFDocument11 pagesNirmal Bang PDFBook MonkNo ratings yet

- Varun Beverages Q1CY22 Result UpdateDocument5 pagesVarun Beverages Q1CY22 Result UpdateBaria VirenNo ratings yet

- 2Q FY22 Financial Results Presentation: 22 October 2021Document58 pages2Q FY22 Financial Results Presentation: 22 October 2021chaitanya varma ChekuriNo ratings yet

- Burger King India (BURGERKI IN) : Q2FY22 Result UpdateDocument8 pagesBurger King India (BURGERKI IN) : Q2FY22 Result UpdatebradburywillsNo ratings yet

- Asian-Paints Broker ReportDocument7 pagesAsian-Paints Broker Reportsj singhNo ratings yet

- Centrum Dabur India Company UpdateDocument7 pagesCentrum Dabur India Company UpdateprasaadrajputNo ratings yet

- SH Kelkar: All-Round Performance Outlook Remains StrongDocument8 pagesSH Kelkar: All-Round Performance Outlook Remains StrongJehan BhadhaNo ratings yet

- Butterfly Gandhimathi Appliances LTD - Stock Update - 01.12.2021-1Document12 pagesButterfly Gandhimathi Appliances LTD - Stock Update - 01.12.2021-1sundar iyerNo ratings yet

- V Guard Industries Q3 FY22 Results PresentationDocument17 pagesV Guard Industries Q3 FY22 Results PresentationRATHINo ratings yet

- Raymond-Q2FY22-RU LKPDocument9 pagesRaymond-Q2FY22-RU LKP56 AA Prathamesh WarangNo ratings yet

- 1Q FY 2021-22 Financial ResultsDocument54 pages1Q FY 2021-22 Financial Resultsaditya tripathiNo ratings yet

- Page Industries: Revenue Growth Improves While Margins DeclineDocument8 pagesPage Industries: Revenue Growth Improves While Margins DeclinePuneet367No ratings yet

- Edita 3Q2023 Earnings Release E v4Document10 pagesEdita 3Q2023 Earnings Release E v4Habiba HishamNo ratings yet

- 211428182023567dabur India Limited - 20230808Document5 pages211428182023567dabur India Limited - 20230808Jigar PitrodaNo ratings yet

- Indofood Sukses Makmur TBK (INDF IJ) : Strong Performance From All SegmentsDocument6 pagesIndofood Sukses Makmur TBK (INDF IJ) : Strong Performance From All SegmentsPutu Chantika Putri DhammayantiNo ratings yet

- RIL 3Q FY24 Analyst Presentation 19jan24Document55 pagesRIL 3Q FY24 Analyst Presentation 19jan24meetpanchal172006No ratings yet

- Earnings Release - 01.30.2023 FINALDocument20 pagesEarnings Release - 01.30.2023 FINALDuangjitr WongNo ratings yet

- Infosys (INFO IN) : Q1FY22 Result UpdateDocument13 pagesInfosys (INFO IN) : Q1FY22 Result UpdatePrahladNo ratings yet

- Mrs. Bectors Food Specialities 04062024 AcDocument6 pagesMrs. Bectors Food Specialities 04062024 AcgreyistariNo ratings yet

- Indofood CBP Sukses Makmur: Equity ResearchDocument5 pagesIndofood CBP Sukses Makmur: Equity ResearchAbimanyu LearingNo ratings yet

- Income Statement Analysis of Vitarich CorporationDocument11 pagesIncome Statement Analysis of Vitarich CorporationLynnie Jane JauculanNo ratings yet

- Infosys (INFO IN) : Q1FY21 Result UpdateDocument14 pagesInfosys (INFO IN) : Q1FY21 Result UpdatewhitenagarNo ratings yet

- UNVR SekuritasDocument7 pagesUNVR Sekuritasfaizal ardiNo ratings yet

- Financial Highlights: Values in R$ ('000)Document33 pagesFinancial Highlights: Values in R$ ('000)renatoNo ratings yet

- Nestle India: Project RURBAN To Support Strong Growth Inflationary Clouds RemainDocument11 pagesNestle India: Project RURBAN To Support Strong Growth Inflationary Clouds Remainkrishna_buntyNo ratings yet

- Prabhudas Lilladher Apar Industries Q2FY24 Results ReviewDocument7 pagesPrabhudas Lilladher Apar Industries Q2FY24 Results ReviewyoursaaryaNo ratings yet

- CTEC 2021 4Q Press ReleaseDocument46 pagesCTEC 2021 4Q Press Releasefatso68No ratings yet

- BP Plastics Holding Berhad Outperform : 1HFY21 Above ExpectationDocument4 pagesBP Plastics Holding Berhad Outperform : 1HFY21 Above ExpectationZhi_Ming_Cheah_8136No ratings yet

- Burger King India (BURGERKI IN) : Q4FY21 Result UpdateDocument8 pagesBurger King India (BURGERKI IN) : Q4FY21 Result UpdateSushilNo ratings yet

- Nestle India Equity Research ReportDocument9 pagesNestle India Equity Research ReportDurgesh ShuklaNo ratings yet

- Economic Indicators for East Asia: Input–Output TablesFrom EverandEconomic Indicators for East Asia: Input–Output TablesNo ratings yet

- Business Analysis and Valuation Using Financial Statements Text and Cases 5th Edition Palepu Solutions ManualDocument18 pagesBusiness Analysis and Valuation Using Financial Statements Text and Cases 5th Edition Palepu Solutions Manualdaviddulcieagt6100% (35)

- Infosys Annual Report 2018-19Document1 pageInfosys Annual Report 2018-19Prachi SharmaNo ratings yet

- Introduction To Accounting Practice Exercises: Exercise 1: The Accounting Equation Problem 1.1Document10 pagesIntroduction To Accounting Practice Exercises: Exercise 1: The Accounting Equation Problem 1.1Arbie Joy Olofernes SibilNo ratings yet

- Lecture 8 - Exercises - SolutionDocument8 pagesLecture 8 - Exercises - SolutionIsyraf Hatim Mohd TamizamNo ratings yet

- Chattanooga State AuditDocument78 pagesChattanooga State AuditDan LehrNo ratings yet

- Account AssignmentDocument10 pagesAccount AssignmentkanchanghengNo ratings yet

- Page 1 of 4 Chapter 4 - Intermediate Accounting 3Document4 pagesPage 1 of 4 Chapter 4 - Intermediate Accounting 3happy2408230% (1)

- List of Sub-Object Code - 20160322Document135 pagesList of Sub-Object Code - 20160322Julius AlemanNo ratings yet

- 185f8question BankDocument18 pages185f8question Bank55amonNo ratings yet

- Kelompok 10 - Kelas o - Week 9Document10 pagesKelompok 10 - Kelas o - Week 9willyNo ratings yet

- Decision MakingDocument28 pagesDecision MakingGelyn CruzNo ratings yet

- Chapter 2Document54 pagesChapter 2Léo AudibertNo ratings yet

- Bank Maybank Indonesia Bilingual 31des21 ReleasedDocument350 pagesBank Maybank Indonesia Bilingual 31des21 ReleasedNidaNo ratings yet

- Tata Consultancy ServicesDocument6 pagesTata Consultancy ServicesHarshad PawarNo ratings yet

- Quiz 1-EIB10403 - Oct 2023 ComfirmDocument6 pagesQuiz 1-EIB10403 - Oct 2023 ComfirmprfznvtczdNo ratings yet

- SPSPS DatabaseDocument226 pagesSPSPS DatabaseElc Elc ElcNo ratings yet

- Solutions To Solution E12-1: Chapler 12Document38 pagesSolutions To Solution E12-1: Chapler 12Carlo VillanNo ratings yet

- Tuprag - RTR - Explore Design Workshop Deck - Manage General LedgerDocument26 pagesTuprag - RTR - Explore Design Workshop Deck - Manage General LedgerANISHA ROYNo ratings yet

- Chapter 7 Investment PropertyDocument8 pagesChapter 7 Investment PropertyKrissa Mae Longos100% (2)

- Fabozzi BMAS7 CH04 Bond Price Volatility SolutionsDocument40 pagesFabozzi BMAS7 CH04 Bond Price Volatility Solutionsvishal kanekarNo ratings yet

- Acctg1205 - Chapter 8Document48 pagesAcctg1205 - Chapter 8Elj Grace BaronNo ratings yet

- Capital BudgetingDocument44 pagesCapital Budgetingrisbd appliancesNo ratings yet

- Cpa Review School of The Philippines Mani LaDocument2 pagesCpa Review School of The Philippines Mani LaJustine CruzNo ratings yet

- Name: Date: Instructor: Course: Accounting Principles Primer On Using Excel in AccountingDocument2 pagesName: Date: Instructor: Course: Accounting Principles Primer On Using Excel in AccountingHernando MaulanaNo ratings yet

- Date General Journal Debit CreditDocument14 pagesDate General Journal Debit CreditJalaj GuptaNo ratings yet

- Chapter 1 - Introduction ToDocument30 pagesChapter 1 - Introduction ToCostAcct1No ratings yet

- Sbi q42019-2020Document66 pagesSbi q42019-2020Nihal YnNo ratings yet

- UBT - CBA - Final ProjectDocument24 pagesUBT - CBA - Final ProjectLUKE WHITENo ratings yet

- InternshipDocument30 pagesInternshipSumithra K - Kodaikanal centerNo ratings yet