Cop Waste Management Solution

Cop Waste Management Solution

You might also like

- VALIX - IA 1 (2020 Ver.) Government GrantDocument9 pagesVALIX - IA 1 (2020 Ver.) Government GrantAriean Joy DequiñaNo ratings yet

- CP & NS Merger Case - GRP 1Document12 pagesCP & NS Merger Case - GRP 1Paul GhanimehNo ratings yet

- Space Star CaseDocument8 pagesSpace Star CasePaul GhanimehNo ratings yet

- CH 8 LiabilitiesDocument10 pagesCH 8 LiabilitiesKrizia Oliva100% (1)

- Sol. Man. - Chapter 4 - Nca Held For Sale & Discontinued Opns.Document10 pagesSol. Man. - Chapter 4 - Nca Held For Sale & Discontinued Opns.Crown Garcia50% (4)

- 1.1 A Practical Approach To FIDIC Contracts - Accompanying Documentation PDFDocument165 pages1.1 A Practical Approach To FIDIC Contracts - Accompanying Documentation PDFMamoon Riaz100% (1)

- Danelia Testbanks Quiz 2345Document46 pagesDanelia Testbanks Quiz 2345Tinatini BakashviliNo ratings yet

- Group RepoprtingDocument3 pagesGroup RepoprtingPaulNo ratings yet

- Batch 95 FAR First Preboard SolutionDocument7 pagesBatch 95 FAR First Preboard Solutionssslll2No ratings yet

- Years': PreviousDocument25 pagesYears': PreviousHarsahib SinghNo ratings yet

- Accountancy Answer Key - II Puc Annual Exam March 2019Document8 pagesAccountancy Answer Key - II Puc Annual Exam March 2019Akash kNo ratings yet

- Group FinancialDocument8 pagesGroup FinancialNever GonondoNo ratings yet

- Chapter 16 - Teacher's Manual - Aa Part 2Document18 pagesChapter 16 - Teacher's Manual - Aa Part 2IsyongNo ratings yet

- Accounting PracticeDocument24 pagesAccounting PracticeLloydNo ratings yet

- CA India Financial ManagementDocument30 pagesCA India Financial Managementomkumardepani070805No ratings yet

- Cpa Review School of The Philippines Mani LaDocument6 pagesCpa Review School of The Philippines Mani LaSophia PerezNo ratings yet

- Sample Test (Extract)Document6 pagesSample Test (Extract)Julie KimNo ratings yet

- Output No. 3Document1 pageOutput No. 3chingNo ratings yet

- Accounting 50 IMP QUESDocument94 pagesAccounting 50 IMP QUESVijayasri KumaravelNo ratings yet

- AFA IIP.L III SolutionJune 2016Document4 pagesAFA IIP.L III SolutionJune 2016HossainNo ratings yet

- Sept 2014 - 230716 - 233727Document22 pagesSept 2014 - 230716 - 233727mohddanialhanaffimustaffiNo ratings yet

- FMECO EM M.Test Answer 13.09.23Document13 pagesFMECO EM M.Test Answer 13.09.23tandelmohik10No ratings yet

- DocumentDocument4 pagesDocumentTûshar ThakúrNo ratings yet

- Batch 93 FAR First Preboard February 2023 - SolutionDocument5 pagesBatch 93 FAR First Preboard February 2023 - SolutionlorenzNo ratings yet

- Tutorial On Ratio AnalysisDocument4 pagesTutorial On Ratio AnalysisRajyaLakshmiNo ratings yet

- Sir Mac Book SolmanDocument10 pagesSir Mac Book SolmanJAY AUBREY PINEDANo ratings yet

- Ae 17 Midterms Assignment 1Document6 pagesAe 17 Midterms Assignment 1Ronald YNo ratings yet

- Assign 2 Chapter 5 Understanding The Financial Statements Prob 8 Answer Cabrera 2019-2020Document5 pagesAssign 2 Chapter 5 Understanding The Financial Statements Prob 8 Answer Cabrera 2019-2020mhikeedelantar100% (1)

- FIRST PB FAR Solutions PDFDocument6 pagesFIRST PB FAR Solutions PDFStephanie Joy NogollosNo ratings yet

- CH 2Document40 pagesCH 2danaNo ratings yet

- MaDocument6 pagesMaAashayNo ratings yet

- Ia3 FinalsDocument4 pagesIa3 FinalsGeraldine MayoNo ratings yet

- Chapter 4 Accounting For Business Combinations SolmanDocument16 pagesChapter 4 Accounting For Business Combinations SolmanCharlene Bolandres100% (1)

- CashflowDocument8 pagesCashflowShubhankar GuptaNo ratings yet

- Adv Acc - 3 CHDocument21 pagesAdv Acc - 3 CHhassan nassereddineNo ratings yet

- INTACCDocument4 pagesINTACCApple RoncalNo ratings yet

- Fin3702 EXAMPACKDocument30 pagesFin3702 EXAMPACKkevinedgarjacobsNo ratings yet

- Cash Flow ProbDocument3 pagesCash Flow Probbimbee 13No ratings yet

- Unit - Iv Cost and Management AccountingDocument12 pagesUnit - Iv Cost and Management AccountingRamakrishna RoshanNo ratings yet

- Suggested - FM Eco - Test 1Document8 pagesSuggested - FM Eco - Test 1Ritam chaturvediNo ratings yet

- 07 Receivable Financing 2 SolvingDocument3 pages07 Receivable Financing 2 Solvingkyle mandaresioNo ratings yet

- Goodwill Calculation ExercisesDocument8 pagesGoodwill Calculation ExercisesAikal HakimNo ratings yet

- Practice Paper SET A1Document3 pagesPractice Paper SET A1Aaditi VNo ratings yet

- Assignment in Financial Accounting: Jane B. Evangelista Bsba-2BDocument4 pagesAssignment in Financial Accounting: Jane B. Evangelista Bsba-2BJane Barcelona Evangelista0% (1)

- BUSINESS COMBI (Activity On Goodwill Computation) - PALLERDocument5 pagesBUSINESS COMBI (Activity On Goodwill Computation) - PALLERGlayca PallerNo ratings yet

- Final Mock1 - AnswerDocument7 pagesFinal Mock1 - AnswerK58 Hà Phương LinhNo ratings yet

- 2542 - Tut1Document14 pages2542 - Tut1(Alumna 2018-6A07) CHUCK LONG YAU 卓朗悠No ratings yet

- Corporate Finance Practice Problems: Jeter Corporation Income Statement For The Year Ended 31, 2001Document9 pagesCorporate Finance Practice Problems: Jeter Corporation Income Statement For The Year Ended 31, 2001Eunice NanaNo ratings yet

- Cash Flow 8 AprilDocument17 pagesCash Flow 8 AprilMayank MalhotraNo ratings yet

- F M ADocument11 pagesF M AAjay SahooNo ratings yet

- Unit-5 Mefa.Document12 pagesUnit-5 Mefa.Perumalla AkhilNo ratings yet

- Loyola College (Autonomous), Chennai - 600 034: Degree Examination - CommerceDocument4 pagesLoyola College (Autonomous), Chennai - 600 034: Degree Examination - CommerceHarish KapoorNo ratings yet

- Ratio AnalysisDocument3 pagesRatio AnalysisYash AgarwalNo ratings yet

- Class 12 Accountancy CBSE Cash Flow StatementDocument7 pagesClass 12 Accountancy CBSE Cash Flow StatementSarvesh SreedharNo ratings yet

- Acg5205 Solutions Ch.16 - Christensen 12eDocument10 pagesAcg5205 Solutions Ch.16 - Christensen 12eRyan NguyenNo ratings yet

- Problem 1 Summary 35 Problem 1 Solution 21 Problem 2 Jes 60 Problem 2 Worksheet 116 Grand TotalDocument23 pagesProblem 1 Summary 35 Problem 1 Solution 21 Problem 2 Jes 60 Problem 2 Worksheet 116 Grand TotalAngelica DizonNo ratings yet

- A. The Following Account Balances Were Presented On December 31, 2017Document3 pagesA. The Following Account Balances Were Presented On December 31, 2017Shiela Mae Pon AnNo ratings yet

- Advanced Accounting 2 - Chapter 4 James B. Cantorne Problem 1. T/FDocument7 pagesAdvanced Accounting 2 - Chapter 4 James B. Cantorne Problem 1. T/FJames CantorneNo ratings yet

- Ventura, Mary Mickaella R. - p.49 - Statement of Financial PositionDocument5 pagesVentura, Mary Mickaella R. - p.49 - Statement of Financial PositionMary VenturaNo ratings yet

- Comprehensive IllustrationDocument12 pagesComprehensive IllustrationNucke Febriana Putri RZNo ratings yet

- Quiz Inter1 C1Document3 pagesQuiz Inter1 C1Vanessa vnssNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Carreclerc SolutionDocument5 pagesCarreclerc SolutionPaul GhanimehNo ratings yet

- Forever Chic SolutionDocument19 pagesForever Chic SolutionPaul GhanimehNo ratings yet

- Ebit Capex Change in WC FCF: Risk Free Rate 1.67% Market Return (S&P 500) 9.30% Beta 1.13Document5 pagesEbit Capex Change in WC FCF: Risk Free Rate 1.67% Market Return (S&P 500) 9.30% Beta 1.13Paul GhanimehNo ratings yet

- Synergies and ValuationDocument16 pagesSynergies and ValuationPaul GhanimehNo ratings yet

- MA Material Oct 2021Document51 pagesMA Material Oct 2021Paul GhanimehNo ratings yet

- Full Paper VALUATION OF TARGET FIRMS IN MERGERS AND ACQUISITIONS A CASE STUDY ON MERGERDocument19 pagesFull Paper VALUATION OF TARGET FIRMS IN MERGERS AND ACQUISITIONS A CASE STUDY ON MERGERPaul GhanimehNo ratings yet

- Blockchain For Trade: November 2018, Port of SpainDocument13 pagesBlockchain For Trade: November 2018, Port of SpainPaul GhanimehNo ratings yet

- Merchant Integration Services IN-DL90024764734268T: E-StampDocument14 pagesMerchant Integration Services IN-DL90024764734268T: E-StampNewwayNo ratings yet

- Market Structure Worksheets and AnswersDocument16 pagesMarket Structure Worksheets and AnswersNate ChenNo ratings yet

- Full Download Advanced Accounting Beams 12th Edition Solutions Manual PDF Full ChapterDocument36 pagesFull Download Advanced Accounting Beams 12th Edition Solutions Manual PDF Full Chapterbeatencadiemha94100% (21)

- Strategic Management DifinationDocument2 pagesStrategic Management DifinationPrasanna SharmaNo ratings yet

- 3.7. Argentina's Fall Martin FeldsteinDocument4 pages3.7. Argentina's Fall Martin FeldsteinAbhinav UppalNo ratings yet

- Luxasia Pte. Ltd. and Its Subsidiaries Directors' Statement and Financial Statements Year Ended December 31, 2018Document73 pagesLuxasia Pte. Ltd. and Its Subsidiaries Directors' Statement and Financial Statements Year Ended December 31, 2018Joyce ChongNo ratings yet

- ACCY121 - REPORT - TND SquadDocument17 pagesACCY121 - REPORT - TND SquadToànNo ratings yet

- Advacc Midterm ExamDocument13 pagesAdvacc Midterm ExamJosh TanNo ratings yet

- MPOB PPT 1Document26 pagesMPOB PPT 1Parveen KumarNo ratings yet

- Top 40 Wealth Management Firms 2017Document3 pagesTop 40 Wealth Management Firms 2017JonNo ratings yet

- Emad A. Zikry - Implications of Recent Money Market Fund Reform PassageDocument2 pagesEmad A. Zikry - Implications of Recent Money Market Fund Reform PassageEmad-A-ZikryNo ratings yet

- Agriculture On Economic DevelopmentDocument16 pagesAgriculture On Economic DevelopmentAGRI CULTURENo ratings yet

- Tugas Auditing 1 Pertanyaan Dan Soal Diskusi No 14-30 Sampai 14-32 14-30 (Objective 14-5) You Have Been Asked by The Board of Trustees of A Local ChurchDocument4 pagesTugas Auditing 1 Pertanyaan Dan Soal Diskusi No 14-30 Sampai 14-32 14-30 (Objective 14-5) You Have Been Asked by The Board of Trustees of A Local ChurchHusnul KhatimahNo ratings yet

- Presentation Product PLC240228 A02Document8 pagesPresentation Product PLC240228 A02Crazed NinjaNo ratings yet

- Morning Fresh (Saud Afzal)Document7 pagesMorning Fresh (Saud Afzal)Ismail LoneNo ratings yet

- HBR IntroDocument3 pagesHBR IntroNeo4u44No ratings yet

- Running Head: WORKING CAPITAL 1Document4 pagesRunning Head: WORKING CAPITAL 1Priyanka TanwarNo ratings yet

- Strategy Analysis Assignment - M2Document12 pagesStrategy Analysis Assignment - M2Aravind KayampadyNo ratings yet

- 220411-Final Amman ProfileDocument196 pages220411-Final Amman Profilenahmeduo mansourNo ratings yet

- Economic Reforms - MeijiDocument7 pagesEconomic Reforms - Meijisourabh singhalNo ratings yet

- 'O' Level AccountsDocument241 pages'O' Level AccountsAlbert Muswewemombe100% (1)

- Engineering Management PDFDocument7 pagesEngineering Management PDFJay Dela CruzNo ratings yet

- Faqs Solutions: Brief About Sell - DoDocument5 pagesFaqs Solutions: Brief About Sell - DoAbhishek VRNo ratings yet

- Billionaire Bonanza - The Forbes 400 and The Rest of Us - IPSDocument28 pagesBillionaire Bonanza - The Forbes 400 and The Rest of Us - IPSPrince Tafari MartinNo ratings yet

- Sanchay Public Deposit FormDocument6 pagesSanchay Public Deposit Formmanoj barokaNo ratings yet

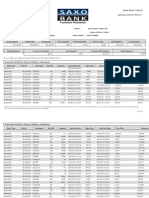

- Customer Statement: Ayman K KhlifatDocument5 pagesCustomer Statement: Ayman K KhlifatTFAL TEAMNo ratings yet

- Advanced Audit and Assurance: Acca P P7 ACCA Paper P7Document10 pagesAdvanced Audit and Assurance: Acca P P7 ACCA Paper P7Dustu CheleNo ratings yet

- Managerial Accounting and CostDocument19 pagesManagerial Accounting and CostIqra MughalNo ratings yet

Download as pdf or txt

You might also like

- VALIX - IA 1 (2020 Ver.) Government GrantDocument9 pagesVALIX - IA 1 (2020 Ver.) Government GrantAriean Joy DequiñaNo ratings yet

- CP & NS Merger Case - GRP 1Document12 pagesCP & NS Merger Case - GRP 1Paul GhanimehNo ratings yet

- Space Star CaseDocument8 pagesSpace Star CasePaul GhanimehNo ratings yet

- CH 8 LiabilitiesDocument10 pagesCH 8 LiabilitiesKrizia Oliva100% (1)

- Sol. Man. - Chapter 4 - Nca Held For Sale & Discontinued Opns.Document10 pagesSol. Man. - Chapter 4 - Nca Held For Sale & Discontinued Opns.Crown Garcia50% (4)

- 1.1 A Practical Approach To FIDIC Contracts - Accompanying Documentation PDFDocument165 pages1.1 A Practical Approach To FIDIC Contracts - Accompanying Documentation PDFMamoon Riaz100% (1)

- Danelia Testbanks Quiz 2345Document46 pagesDanelia Testbanks Quiz 2345Tinatini BakashviliNo ratings yet

- Group RepoprtingDocument3 pagesGroup RepoprtingPaulNo ratings yet

- Batch 95 FAR First Preboard SolutionDocument7 pagesBatch 95 FAR First Preboard Solutionssslll2No ratings yet

- Years': PreviousDocument25 pagesYears': PreviousHarsahib SinghNo ratings yet

- Accountancy Answer Key - II Puc Annual Exam March 2019Document8 pagesAccountancy Answer Key - II Puc Annual Exam March 2019Akash kNo ratings yet

- Group FinancialDocument8 pagesGroup FinancialNever GonondoNo ratings yet

- Chapter 16 - Teacher's Manual - Aa Part 2Document18 pagesChapter 16 - Teacher's Manual - Aa Part 2IsyongNo ratings yet

- Accounting PracticeDocument24 pagesAccounting PracticeLloydNo ratings yet

- CA India Financial ManagementDocument30 pagesCA India Financial Managementomkumardepani070805No ratings yet

- Cpa Review School of The Philippines Mani LaDocument6 pagesCpa Review School of The Philippines Mani LaSophia PerezNo ratings yet

- Sample Test (Extract)Document6 pagesSample Test (Extract)Julie KimNo ratings yet

- Output No. 3Document1 pageOutput No. 3chingNo ratings yet

- Accounting 50 IMP QUESDocument94 pagesAccounting 50 IMP QUESVijayasri KumaravelNo ratings yet

- AFA IIP.L III SolutionJune 2016Document4 pagesAFA IIP.L III SolutionJune 2016HossainNo ratings yet

- Sept 2014 - 230716 - 233727Document22 pagesSept 2014 - 230716 - 233727mohddanialhanaffimustaffiNo ratings yet

- FMECO EM M.Test Answer 13.09.23Document13 pagesFMECO EM M.Test Answer 13.09.23tandelmohik10No ratings yet

- DocumentDocument4 pagesDocumentTûshar ThakúrNo ratings yet

- Batch 93 FAR First Preboard February 2023 - SolutionDocument5 pagesBatch 93 FAR First Preboard February 2023 - SolutionlorenzNo ratings yet

- Tutorial On Ratio AnalysisDocument4 pagesTutorial On Ratio AnalysisRajyaLakshmiNo ratings yet

- Sir Mac Book SolmanDocument10 pagesSir Mac Book SolmanJAY AUBREY PINEDANo ratings yet

- Ae 17 Midterms Assignment 1Document6 pagesAe 17 Midterms Assignment 1Ronald YNo ratings yet

- Assign 2 Chapter 5 Understanding The Financial Statements Prob 8 Answer Cabrera 2019-2020Document5 pagesAssign 2 Chapter 5 Understanding The Financial Statements Prob 8 Answer Cabrera 2019-2020mhikeedelantar100% (1)

- FIRST PB FAR Solutions PDFDocument6 pagesFIRST PB FAR Solutions PDFStephanie Joy NogollosNo ratings yet

- CH 2Document40 pagesCH 2danaNo ratings yet

- MaDocument6 pagesMaAashayNo ratings yet

- Ia3 FinalsDocument4 pagesIa3 FinalsGeraldine MayoNo ratings yet

- Chapter 4 Accounting For Business Combinations SolmanDocument16 pagesChapter 4 Accounting For Business Combinations SolmanCharlene Bolandres100% (1)

- CashflowDocument8 pagesCashflowShubhankar GuptaNo ratings yet

- Adv Acc - 3 CHDocument21 pagesAdv Acc - 3 CHhassan nassereddineNo ratings yet

- INTACCDocument4 pagesINTACCApple RoncalNo ratings yet

- Fin3702 EXAMPACKDocument30 pagesFin3702 EXAMPACKkevinedgarjacobsNo ratings yet

- Cash Flow ProbDocument3 pagesCash Flow Probbimbee 13No ratings yet

- Unit - Iv Cost and Management AccountingDocument12 pagesUnit - Iv Cost and Management AccountingRamakrishna RoshanNo ratings yet

- Suggested - FM Eco - Test 1Document8 pagesSuggested - FM Eco - Test 1Ritam chaturvediNo ratings yet

- 07 Receivable Financing 2 SolvingDocument3 pages07 Receivable Financing 2 Solvingkyle mandaresioNo ratings yet

- Goodwill Calculation ExercisesDocument8 pagesGoodwill Calculation ExercisesAikal HakimNo ratings yet

- Practice Paper SET A1Document3 pagesPractice Paper SET A1Aaditi VNo ratings yet

- Assignment in Financial Accounting: Jane B. Evangelista Bsba-2BDocument4 pagesAssignment in Financial Accounting: Jane B. Evangelista Bsba-2BJane Barcelona Evangelista0% (1)

- BUSINESS COMBI (Activity On Goodwill Computation) - PALLERDocument5 pagesBUSINESS COMBI (Activity On Goodwill Computation) - PALLERGlayca PallerNo ratings yet

- Final Mock1 - AnswerDocument7 pagesFinal Mock1 - AnswerK58 Hà Phương LinhNo ratings yet

- 2542 - Tut1Document14 pages2542 - Tut1(Alumna 2018-6A07) CHUCK LONG YAU 卓朗悠No ratings yet

- Corporate Finance Practice Problems: Jeter Corporation Income Statement For The Year Ended 31, 2001Document9 pagesCorporate Finance Practice Problems: Jeter Corporation Income Statement For The Year Ended 31, 2001Eunice NanaNo ratings yet

- Cash Flow 8 AprilDocument17 pagesCash Flow 8 AprilMayank MalhotraNo ratings yet

- F M ADocument11 pagesF M AAjay SahooNo ratings yet

- Unit-5 Mefa.Document12 pagesUnit-5 Mefa.Perumalla AkhilNo ratings yet

- Loyola College (Autonomous), Chennai - 600 034: Degree Examination - CommerceDocument4 pagesLoyola College (Autonomous), Chennai - 600 034: Degree Examination - CommerceHarish KapoorNo ratings yet

- Ratio AnalysisDocument3 pagesRatio AnalysisYash AgarwalNo ratings yet

- Class 12 Accountancy CBSE Cash Flow StatementDocument7 pagesClass 12 Accountancy CBSE Cash Flow StatementSarvesh SreedharNo ratings yet

- Acg5205 Solutions Ch.16 - Christensen 12eDocument10 pagesAcg5205 Solutions Ch.16 - Christensen 12eRyan NguyenNo ratings yet

- Problem 1 Summary 35 Problem 1 Solution 21 Problem 2 Jes 60 Problem 2 Worksheet 116 Grand TotalDocument23 pagesProblem 1 Summary 35 Problem 1 Solution 21 Problem 2 Jes 60 Problem 2 Worksheet 116 Grand TotalAngelica DizonNo ratings yet

- A. The Following Account Balances Were Presented On December 31, 2017Document3 pagesA. The Following Account Balances Were Presented On December 31, 2017Shiela Mae Pon AnNo ratings yet

- Advanced Accounting 2 - Chapter 4 James B. Cantorne Problem 1. T/FDocument7 pagesAdvanced Accounting 2 - Chapter 4 James B. Cantorne Problem 1. T/FJames CantorneNo ratings yet

- Ventura, Mary Mickaella R. - p.49 - Statement of Financial PositionDocument5 pagesVentura, Mary Mickaella R. - p.49 - Statement of Financial PositionMary VenturaNo ratings yet

- Comprehensive IllustrationDocument12 pagesComprehensive IllustrationNucke Febriana Putri RZNo ratings yet

- Quiz Inter1 C1Document3 pagesQuiz Inter1 C1Vanessa vnssNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Carreclerc SolutionDocument5 pagesCarreclerc SolutionPaul GhanimehNo ratings yet

- Forever Chic SolutionDocument19 pagesForever Chic SolutionPaul GhanimehNo ratings yet

- Ebit Capex Change in WC FCF: Risk Free Rate 1.67% Market Return (S&P 500) 9.30% Beta 1.13Document5 pagesEbit Capex Change in WC FCF: Risk Free Rate 1.67% Market Return (S&P 500) 9.30% Beta 1.13Paul GhanimehNo ratings yet

- Synergies and ValuationDocument16 pagesSynergies and ValuationPaul GhanimehNo ratings yet

- MA Material Oct 2021Document51 pagesMA Material Oct 2021Paul GhanimehNo ratings yet

- Full Paper VALUATION OF TARGET FIRMS IN MERGERS AND ACQUISITIONS A CASE STUDY ON MERGERDocument19 pagesFull Paper VALUATION OF TARGET FIRMS IN MERGERS AND ACQUISITIONS A CASE STUDY ON MERGERPaul GhanimehNo ratings yet

- Blockchain For Trade: November 2018, Port of SpainDocument13 pagesBlockchain For Trade: November 2018, Port of SpainPaul GhanimehNo ratings yet

- Merchant Integration Services IN-DL90024764734268T: E-StampDocument14 pagesMerchant Integration Services IN-DL90024764734268T: E-StampNewwayNo ratings yet

- Market Structure Worksheets and AnswersDocument16 pagesMarket Structure Worksheets and AnswersNate ChenNo ratings yet

- Full Download Advanced Accounting Beams 12th Edition Solutions Manual PDF Full ChapterDocument36 pagesFull Download Advanced Accounting Beams 12th Edition Solutions Manual PDF Full Chapterbeatencadiemha94100% (21)

- Strategic Management DifinationDocument2 pagesStrategic Management DifinationPrasanna SharmaNo ratings yet

- 3.7. Argentina's Fall Martin FeldsteinDocument4 pages3.7. Argentina's Fall Martin FeldsteinAbhinav UppalNo ratings yet

- Luxasia Pte. Ltd. and Its Subsidiaries Directors' Statement and Financial Statements Year Ended December 31, 2018Document73 pagesLuxasia Pte. Ltd. and Its Subsidiaries Directors' Statement and Financial Statements Year Ended December 31, 2018Joyce ChongNo ratings yet

- ACCY121 - REPORT - TND SquadDocument17 pagesACCY121 - REPORT - TND SquadToànNo ratings yet

- Advacc Midterm ExamDocument13 pagesAdvacc Midterm ExamJosh TanNo ratings yet

- MPOB PPT 1Document26 pagesMPOB PPT 1Parveen KumarNo ratings yet

- Top 40 Wealth Management Firms 2017Document3 pagesTop 40 Wealth Management Firms 2017JonNo ratings yet

- Emad A. Zikry - Implications of Recent Money Market Fund Reform PassageDocument2 pagesEmad A. Zikry - Implications of Recent Money Market Fund Reform PassageEmad-A-ZikryNo ratings yet

- Agriculture On Economic DevelopmentDocument16 pagesAgriculture On Economic DevelopmentAGRI CULTURENo ratings yet

- Tugas Auditing 1 Pertanyaan Dan Soal Diskusi No 14-30 Sampai 14-32 14-30 (Objective 14-5) You Have Been Asked by The Board of Trustees of A Local ChurchDocument4 pagesTugas Auditing 1 Pertanyaan Dan Soal Diskusi No 14-30 Sampai 14-32 14-30 (Objective 14-5) You Have Been Asked by The Board of Trustees of A Local ChurchHusnul KhatimahNo ratings yet

- Presentation Product PLC240228 A02Document8 pagesPresentation Product PLC240228 A02Crazed NinjaNo ratings yet

- Morning Fresh (Saud Afzal)Document7 pagesMorning Fresh (Saud Afzal)Ismail LoneNo ratings yet

- HBR IntroDocument3 pagesHBR IntroNeo4u44No ratings yet

- Running Head: WORKING CAPITAL 1Document4 pagesRunning Head: WORKING CAPITAL 1Priyanka TanwarNo ratings yet

- Strategy Analysis Assignment - M2Document12 pagesStrategy Analysis Assignment - M2Aravind KayampadyNo ratings yet

- 220411-Final Amman ProfileDocument196 pages220411-Final Amman Profilenahmeduo mansourNo ratings yet

- Economic Reforms - MeijiDocument7 pagesEconomic Reforms - Meijisourabh singhalNo ratings yet

- 'O' Level AccountsDocument241 pages'O' Level AccountsAlbert Muswewemombe100% (1)

- Engineering Management PDFDocument7 pagesEngineering Management PDFJay Dela CruzNo ratings yet

- Faqs Solutions: Brief About Sell - DoDocument5 pagesFaqs Solutions: Brief About Sell - DoAbhishek VRNo ratings yet

- Billionaire Bonanza - The Forbes 400 and The Rest of Us - IPSDocument28 pagesBillionaire Bonanza - The Forbes 400 and The Rest of Us - IPSPrince Tafari MartinNo ratings yet

- Sanchay Public Deposit FormDocument6 pagesSanchay Public Deposit Formmanoj barokaNo ratings yet

- Customer Statement: Ayman K KhlifatDocument5 pagesCustomer Statement: Ayman K KhlifatTFAL TEAMNo ratings yet

- Advanced Audit and Assurance: Acca P P7 ACCA Paper P7Document10 pagesAdvanced Audit and Assurance: Acca P P7 ACCA Paper P7Dustu CheleNo ratings yet

- Managerial Accounting and CostDocument19 pagesManagerial Accounting and CostIqra MughalNo ratings yet