Download as txt, pdf, or txt

You might also like

- Aerocomp Inc Case Study Week 7Document5 pagesAerocomp Inc Case Study Week 7Aguntuk Shawon100% (4)

- PRINCE2 7 PRT SamplePaper2Document44 pagesPRINCE2 7 PRT SamplePaper2yaninaNo ratings yet

- Phuket Beach Hotel FinalDocument23 pagesPhuket Beach Hotel FinalTosheef Allen Kropenski100% (1)

- Preview PDFDocument3 pagesPreview PDFmutiaNo ratings yet

- Petroleum Refinery Relocation Projects: 5-Phases of Project ManagementFrom EverandPetroleum Refinery Relocation Projects: 5-Phases of Project ManagementNo ratings yet

- Planning Case Study D1Document5 pagesPlanning Case Study D1Van Vien NguyenNo ratings yet

- 100 Case Study In Project Management and Right Decision (Project Management Professional Exam)From Everand100 Case Study In Project Management and Right Decision (Project Management Professional Exam)Rating: 4 out of 5 stars4/5 (3)

- GRC FinMan Capital Budgeting ModuleDocument10 pagesGRC FinMan Capital Budgeting ModuleJasmine FiguraNo ratings yet

- Phuket CaseDocument4 pagesPhuket Casejperez1980100% (1)

- The Phuket Beach CaseDocument4 pagesThe Phuket Beach Casepeilin tongNo ratings yet

- Chapter 09 IM 10th EdDocument24 pagesChapter 09 IM 10th EdBenny KhorNo ratings yet

- Amazon Seller Affiliate ProgramDocument3 pagesAmazon Seller Affiliate Programcharsaubees420No ratings yet

- Muhammad Yunus, Building Social Business: The New Kind of Capitalism That Serves Humanity's Most Pressing NeedsDocument3 pagesMuhammad Yunus, Building Social Business: The New Kind of Capitalism That Serves Humanity's Most Pressing NeedsJackaBecker100% (4)

- MIS Business ProcessesDocument6 pagesMIS Business Processesdenin joyNo ratings yet

- Phuket Beach Hotel (Final)Document23 pagesPhuket Beach Hotel (Final)adee_uson67% (3)

- Phuket Beach Hotel Final 1Document23 pagesPhuket Beach Hotel Final 1neha konarNo ratings yet

- Case... Phuket Beach HotelDocument3 pagesCase... Phuket Beach HotelSanjay Kumar JainNo ratings yet

- Acc 121 Case StudyDocument18 pagesAcc 121 Case StudySophia Zavynne Ancheta BuenoNo ratings yet

- Case 1 Phuket Beach HotelDocument7 pagesCase 1 Phuket Beach HotelYana Dela CernaNo ratings yet

- CASE STUDY 4B JenzDocument5 pagesCASE STUDY 4B Jenzlawrence.jlawaccNo ratings yet

- Phuket Beach HotelDocument3 pagesPhuket Beach HotelKislay KisuNo ratings yet

- Phuket Beach Hotel Case Analysis: Corporate Finance F3, 2015Document9 pagesPhuket Beach Hotel Case Analysis: Corporate Finance F3, 2015Ashadi CahyadiNo ratings yet

- Saber Pro Workshop 2 Project ManagementDocument2 pagesSaber Pro Workshop 2 Project ManagementScribdTranslationsNo ratings yet

- Financial Risk Management Fs Analysis StudentsDocument7 pagesFinancial Risk Management Fs Analysis Studentsshai santiagoNo ratings yet

- Specimen 3 Answers NebhyDocument10 pagesSpecimen 3 Answers NebhywowwwNo ratings yet

- Finance Midterm QuestionsDocument3 pagesFinance Midterm QuestionsAnonymous x4LL5ecNCRNo ratings yet

- FFM12, CH 13, IM, 01-08-09Document20 pagesFFM12, CH 13, IM, 01-08-09seventeenlopez100% (1)

- Class Case 5thDocument13 pagesClass Case 5thAngelica B. PatagNo ratings yet

- MBALN-622 - Midterm Examination BriefDocument6 pagesMBALN-622 - Midterm Examination BriefwebsternhidzaNo ratings yet

- A. The Importance of Capital BudgetingDocument98 pagesA. The Importance of Capital BudgetingShoniqua JohnsonNo ratings yet

- Boeing Case:: 1. Why Is Boeing Contemplating The Launch of The 7E7 Project? Is This A Good Time To Do So?Document4 pagesBoeing Case:: 1. Why Is Boeing Contemplating The Launch of The 7E7 Project? Is This A Good Time To Do So?HouDaAakNo ratings yet

- 09-Capital Budgeting TechniquesDocument19 pages09-Capital Budgeting TechniquesJean Jane EstradaNo ratings yet

- 143 Quiz4Document3 pages143 Quiz4Leigh PilapilNo ratings yet

- CH 8Document18 pagesCH 8ahngehlah100% (3)

- Quiz Capital Budgeting 2018 2019 1st SemDocument6 pagesQuiz Capital Budgeting 2018 2019 1st Semjethro carlobosNo ratings yet

- TMP - 5567 PK10 191431902Document16 pagesTMP - 5567 PK10 191431902Pijus BiswasNo ratings yet

- Final Exam 2006 Sem-1Document10 pagesFinal Exam 2006 Sem-1shikharaneja20005047No ratings yet

- FFM12, CH 13, IM, 01-08-09Document18 pagesFFM12, CH 13, IM, 01-08-09James Louis B. AntonioNo ratings yet

- Investment DecisionsDocument17 pagesInvestment Decisionssajith santyNo ratings yet

- Capital BugetingDocument6 pagesCapital BugetingMichael ReyesNo ratings yet

- PMP Exam QuestionsDocument31 pagesPMP Exam QuestionsAsuelimen tito100% (1)

- Financial Management 2: UCP-001BDocument3 pagesFinancial Management 2: UCP-001BRobert RamirezNo ratings yet

- CAC Tutorial 11Document4 pagesCAC Tutorial 11zachariaseNo ratings yet

- Activity - Capital Investment AnalysisDocument5 pagesActivity - Capital Investment AnalysisKATHRYN CLAUDETTE RESENTENo ratings yet

- M12 Gitm4380 13e Im C12 PDFDocument23 pagesM12 Gitm4380 13e Im C12 PDFGolamSarwar0% (1)

- Finance - Egret Printing (Finance Case Study Solution)Document12 pagesFinance - Egret Printing (Finance Case Study Solution)Shivshankar YadavNo ratings yet

- Wright Technological College of Antique Senior High School Sibalom Branch Sibalom, AntiqueDocument6 pagesWright Technological College of Antique Senior High School Sibalom Branch Sibalom, AntiqueLen PenieroNo ratings yet

- Finman MidtermDocument4 pagesFinman Midtermmarc rodriguezNo ratings yet

- De Ramos - Strategic Cost Management (Acct 1107)Document20 pagesDe Ramos - Strategic Cost Management (Acct 1107)May RamosNo ratings yet

- Chapter-3 ExercisesDocument17 pagesChapter-3 Exercisesminhanhvu2406No ratings yet

- Investment Appraisal DissertationDocument8 pagesInvestment Appraisal DissertationSyracuse100% (1)

- Egret Case StudyDocument35 pagesEgret Case StudyHimalaya BanNo ratings yet

- Strategic Cost Management (Acct 1107)Document19 pagesStrategic Cost Management (Acct 1107)jaeNo ratings yet

- Toaz - Info Chapter 12 PRDocument34 pagesToaz - Info Chapter 12 PRtaponic390No ratings yet

- Feasibility Study 13 PDF FreeDocument74 pagesFeasibility Study 13 PDF FreeAlesa DaffonNo ratings yet

- ChecklistforModularefDocument5 pagesChecklistforModularefofforma NwaforNo ratings yet

- Chapter 6 - Investment Decisions - Capital BudgetingDocument21 pagesChapter 6 - Investment Decisions - Capital BudgetingYasir ShaikhNo ratings yet

- FM Testbank Ch13Document29 pagesFM Testbank Ch13David LarryNo ratings yet

- Name Smart Task No. Project TopicDocument3 pagesName Smart Task No. Project Topichemanth kumarNo ratings yet

- Af208 Fe PDFDocument14 pagesAf208 Fe PDFTetzNo ratings yet

- June 2019: Summary Points BY TAHA POPATIADocument3 pagesJune 2019: Summary Points BY TAHA POPATIASriram RatnamNo ratings yet

- Evaluation of Foreign ProjectsDocument18 pagesEvaluation of Foreign ProjectsMJ jNo ratings yet

- Financial Management Chapter 09 IM 10th EdDocument24 pagesFinancial Management Chapter 09 IM 10th EdDr Rushen SinghNo ratings yet

- Project Financing: Asset-Based Financial EngineeringFrom EverandProject Financing: Asset-Based Financial EngineeringRating: 4 out of 5 stars4/5 (2)

- ICICI Personal Loan StatementDocument3 pagesICICI Personal Loan StatementChandra AnandNo ratings yet

- Application - 5.html: Financial Management and Application Paper View Solved atDocument2 pagesApplication - 5.html: Financial Management and Application Paper View Solved atHaris KhanNo ratings yet

- 406 Invoice-INV-04228Document2 pages406 Invoice-INV-04228Eduardo Martinez De la peñaNo ratings yet

- CH 4 PPTDocument40 pagesCH 4 PPTMekoninn HylemariamNo ratings yet

- MBI-R-002 Rental of 14m ScissorliftDocument2 pagesMBI-R-002 Rental of 14m ScissorliftLaemarc Estrada100% (1)

- Financiele-Verslaggeving 1664Document231 pagesFinanciele-Verslaggeving 1664Ştefania FcSbNo ratings yet

- Slide 1Document6 pagesSlide 1marwaNo ratings yet

- Time Value of MoneyDocument17 pagesTime Value of Moneyabdiel100% (3)

- Lecture 04 - Currency DerivativesDocument10 pagesLecture 04 - Currency DerivativesTrương Ngọc Minh ĐăngNo ratings yet

- Electricity Bill AprilDocument1 pageElectricity Bill Aprilyouvsyou333No ratings yet

- Uptime Awards: Recognizing The Best of The Best!Document40 pagesUptime Awards: Recognizing The Best of The Best!Eric Sonny García AngelesNo ratings yet

- G D Goenka Public School, Jammu: "INDIAN ECONOMY 1950-1990"Document3 pagesG D Goenka Public School, Jammu: "INDIAN ECONOMY 1950-1990"Keshvi AggarwalNo ratings yet

- Price ListDocument11 pagesPrice ListPraveen SharmaNo ratings yet

- Cash BudgetDocument15 pagesCash Budgetpriyanshu kumari0% (1)

- Chapter 22 Economic Growth: Parkin/Bade, Economics: Canada in The Global Environment, 8eDocument31 pagesChapter 22 Economic Growth: Parkin/Bade, Economics: Canada in The Global Environment, 8ePranta SahaNo ratings yet

- Types of Businesses Chart WorksheetDocument1 pageTypes of Businesses Chart WorksheetYousif Jamal Al Naqbi 12BENo ratings yet

- Space Matrix - Air India + Air Asia Internal EnvironmentDocument3 pagesSpace Matrix - Air India + Air Asia Internal EnvironmentSubham PatraNo ratings yet

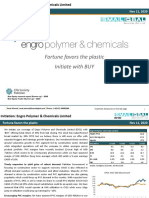

- EPCL - Fortune Favors The Plastic-3Document14 pagesEPCL - Fortune Favors The Plastic-3Fawad SaleemNo ratings yet

- Invoice I Phone 7Document1 pageInvoice I Phone 7tanishkrajak3108No ratings yet

- The Impact of Accounting Information System On TheDocument8 pagesThe Impact of Accounting Information System On TheRezky RamadhaniNo ratings yet

- Basics of Engineering Economy: Lecture Slides To Accompany by Leland Blank and Anthony TarquinDocument34 pagesBasics of Engineering Economy: Lecture Slides To Accompany by Leland Blank and Anthony TarquinWED1000No ratings yet

- Municipal Corporation of DelhiDocument2 pagesMunicipal Corporation of DelhisunilchhindraNo ratings yet

- Banking and Insurance Law ProjectDocument14 pagesBanking and Insurance Law ProjectVanshita GuptaNo ratings yet

- FA2 Accruals and PrepaymentsDocument4 pagesFA2 Accruals and Prepaymentsamna zaman100% (1)

- Fair Value (Pfrs 13) :: PAS 41: AgricultureDocument2 pagesFair Value (Pfrs 13) :: PAS 41: AgricultureCzar RabayaNo ratings yet