Download as pdf or txt

You might also like

- Comparative Analysis of Shariah Review and AuditDocument14 pagesComparative Analysis of Shariah Review and AuditNurazalia Zakaria100% (3)

- Shariah Non Compliance Through Auditing and Risk ManagementDocument22 pagesShariah Non Compliance Through Auditing and Risk ManagementAzah Atikah Anwar BatchaNo ratings yet

- The Foundations of Islamic Economics and BankingFrom EverandThe Foundations of Islamic Economics and BankingNo ratings yet

- Their Eyes Were Watching GodDocument13 pagesTheir Eyes Were Watching Godapi-316773627100% (1)

- Shahzad Asgharet Al Shariah Governance of IBIs in Pakistan An Empirical InvestigationDocument14 pagesShahzad Asgharet Al Shariah Governance of IBIs in Pakistan An Empirical InvestigationMuhammad Asghar ShahzadNo ratings yet

- Assessing The Effectiveness of Internal Sharī Ah Audit Structure and Its Practices in Islamic Financial InstitutionsDocument21 pagesAssessing The Effectiveness of Internal Sharī Ah Audit Structure and Its Practices in Islamic Financial InstitutionsUswah HanifNo ratings yet

- 2013 4thAsiaIslamicBankingConference CRMDocument25 pages2013 4thAsiaIslamicBankingConference CRMabdullaahjalilNo ratings yet

- Line of Reporting and CommunicationDocument18 pagesLine of Reporting and CommunicationSolomon TekalignNo ratings yet

- Shariah Governance Framework-MergedDocument125 pagesShariah Governance Framework-MergedThineshNo ratings yet

- Factors Affecting Sharı Ah AuditDocument17 pagesFactors Affecting Sharı Ah AuditYougie PoerbaNo ratings yet

- Shariah Supervisory BoardDocument31 pagesShariah Supervisory BoardMaas Riyaz MalikNo ratings yet

- Shariah Audit by Nabila and AthiqahDocument25 pagesShariah Audit by Nabila and AthiqahNurathiqah FadzilNo ratings yet

- Chapter 7 - Regulation NewDocument35 pagesChapter 7 - Regulation Newamirul hakimNo ratings yet

- Shariah Governance Practices in Malaysian Islamic Financial InstitutionsDocument16 pagesShariah Governance Practices in Malaysian Islamic Financial Institutionszabardast099No ratings yet

- Issues in Corporate and Shari'ah Governance Practices in Islamic Financial Institutions What Went WrongDocument14 pagesIssues in Corporate and Shari'ah Governance Practices in Islamic Financial Institutions What Went WrongWarriorNo ratings yet

- AC 5033: Shariah Audit: Assignment 1 GroupDocument14 pagesAC 5033: Shariah Audit: Assignment 1 GroupJubair Al AmeenNo ratings yet

- Proposal On Sharia ScholarDocument14 pagesProposal On Sharia ScholarSolomon TekalignNo ratings yet

- 10 1108 - Imefm 02 2013 0021Document12 pages10 1108 - Imefm 02 2013 0021alfauziyasserNo ratings yet

- ISRA, (2011) - International Shari' Ah Research Academy For Islamic Finance, MalaysiaDocument24 pagesISRA, (2011) - International Shari' Ah Research Academy For Islamic Finance, MalaysiaMohamed AlgzereyNo ratings yet

- Admin,+13 CIMAE Rifqi EndDocument13 pagesAdmin,+13 CIMAE Rifqi EndHafiz RezaNo ratings yet

- Islamic FinaceDocument4 pagesIslamic FinaceMohsin NoorNo ratings yet

- Islamic Finance - Audit Issues in Islamic Finance PDFDocument51 pagesIslamic Finance - Audit Issues in Islamic Finance PDFJIREN SHIS HAMUNo ratings yet

- 9-Article Text-15-1-10-20200814Document16 pages9-Article Text-15-1-10-20200814Daria PearNo ratings yet

- Shariah Governance System in Islamic Financial InsDocument17 pagesShariah Governance System in Islamic Financial InsWan RuschdeyNo ratings yet

- Shariah Governance Framework For Islamic Insurance or TakafulDocument19 pagesShariah Governance Framework For Islamic Insurance or TakafulRayhanNo ratings yet

- Materi Kelompok 1Document25 pagesMateri Kelompok 12 Ashlih Al TsabatNo ratings yet

- ISRA Research Paper Shariah Governance Accross JurisdictionDocument63 pagesISRA Research Paper Shariah Governance Accross JurisdictionRaudhatun NisaNo ratings yet

- Shari'ah Risk Management Framework For Islamic Financial InstitutionsDocument22 pagesShari'ah Risk Management Framework For Islamic Financial InstitutionsjawadNo ratings yet

- Islamic Financial System Principles and Operations PDF 701 800Document100 pagesIslamic Financial System Principles and Operations PDF 701 800Asdelina R100% (1)

- The Effects of Shariah Board Composition On Islamic Equity Indices ' PerformanceDocument12 pagesThe Effects of Shariah Board Composition On Islamic Equity Indices ' PerformanceGhulam NabiNo ratings yet

- Issues of Shariah AuditDocument12 pagesIssues of Shariah AuditFATIN 'AISYAH MASLAN ABDUL HAFIZNo ratings yet

- Special Feature Islamic Finance at The Current Sta PDFDocument14 pagesSpecial Feature Islamic Finance at The Current Sta PDFCode PutraNo ratings yet

- Shariah Audit Certification Contents: Views of Regulators, Shariah Committee, Shariah Reviewers and Undergraduat..Document19 pagesShariah Audit Certification Contents: Views of Regulators, Shariah Committee, Shariah Reviewers and Undergraduat..baehaqi17No ratings yet

- 335 1 1312 1 10 20130909 PDFDocument16 pages335 1 1312 1 10 20130909 PDFkristin_kim_13No ratings yet

- Constructs of Shariah Audit Effectiveness in IFIsDocument16 pagesConstructs of Shariah Audit Effectiveness in IFIsNurazalia Zakaria100% (1)

- 374-Article Text-866-1-10-20190925 PDFDocument37 pages374-Article Text-866-1-10-20190925 PDFVita Citra MulyandiniNo ratings yet

- Islamic Finance AsiaDocument2 pagesIslamic Finance AsiaAhmad FaresNo ratings yet

- The Development of Shariah Audit Scope in Malaysian Takaful Industry: A Preliminary AnalysisDocument22 pagesThe Development of Shariah Audit Scope in Malaysian Takaful Industry: A Preliminary AnalysisnsNo ratings yet

- External Shariah Audit: Current Development, Issues and Implementation ChallengesDocument23 pagesExternal Shariah Audit: Current Development, Issues and Implementation ChallengesHalimah Bibi Zurina ShafiiNo ratings yet

- Guiding Principles For Shariah Governance SystemDocument7 pagesGuiding Principles For Shariah Governance SystemHamad AbdulazizNo ratings yet

- Governance, Religious Assurance and Islamic Banks: Do Shariah Boards Effectively Serve?Document29 pagesGovernance, Religious Assurance and Islamic Banks: Do Shariah Boards Effectively Serve?Farid ZafarNo ratings yet

- Emifvoice Saunit10Document26 pagesEmifvoice Saunit10MANU OKAYNo ratings yet

- Gorvernance 2Document26 pagesGorvernance 2nurul nadzirahNo ratings yet

- Ife761 Final AssessmentDocument12 pagesIfe761 Final AssessmentElySya SyaNo ratings yet

- Shariah Audit, Shariah Certification & Shariah ReviewDocument11 pagesShariah Audit, Shariah Certification & Shariah ReviewAlHuda Centre of Islamic Banking & Economics (CIBE)No ratings yet

- Haridan2018 Article GovernanceReligiousAssuranceAnDocument32 pagesHaridan2018 Article GovernanceReligiousAssuranceAnRaffi RamliNo ratings yet

- Lec 7 Shariah GovernanceDocument20 pagesLec 7 Shariah GovernanceAina KhairunnisaNo ratings yet

- Summary Ifsb Puteri F1025Document5 pagesSummary Ifsb Puteri F1025Siti Nur QamarinaNo ratings yet

- Accounting and Auditing Standards For Islamic Banks1Document71 pagesAccounting and Auditing Standards For Islamic Banks1Amine ElghaziNo ratings yet

- WP-05 - En-Shariah NOn Compliance RiskDocument116 pagesWP-05 - En-Shariah NOn Compliance RiskDila Fadiya FarrasNo ratings yet

- Islamic Financial Service Board (Ifsb)Document5 pagesIslamic Financial Service Board (Ifsb)Siti Nur QamarinaNo ratings yet

- Irma Kasri Dan N. LukviarmanDocument29 pagesIrma Kasri Dan N. Lukviarmanjaharuddin.hannoverNo ratings yet

- Talent Management 2019 IJof Fin ResearchDocument16 pagesTalent Management 2019 IJof Fin ResearchnsNo ratings yet

- Overview of Financial Services Act 2013Document11 pagesOverview of Financial Services Act 2013FatehahNo ratings yet

- IE2001Document8 pagesIE2001eyaacobNo ratings yet

- Alternative Financial SystemDocument11 pagesAlternative Financial SystemMohammed SaifulNo ratings yet

- The Development in Shariah Auditing in MalaysiaDocument20 pagesThe Development in Shariah Auditing in MalaysiaAshween Raj яMc100% (1)

- Weathering the Global Crisis: Can the Traits of Islamic Banking System Make a Difference?From EverandWeathering the Global Crisis: Can the Traits of Islamic Banking System Make a Difference?No ratings yet

- Corporate Governance - Effective Performance Evaluation of the BoardFrom EverandCorporate Governance - Effective Performance Evaluation of the BoardNo ratings yet

- 3 2 1 Code It 6th Edition Green Solutions Manual DOWNLOAD YOUR FILES DownloadDocument131 pages3 2 1 Code It 6th Edition Green Solutions Manual DOWNLOAD YOUR FILES DownloadelizabethNo ratings yet

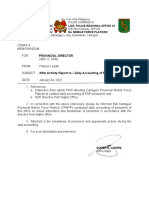

- Philippine National Police, Police Regional Office 10 Camiguin Provincial Mobile Force PlatoonDocument3 pagesPhilippine National Police, Police Regional Office 10 Camiguin Provincial Mobile Force PlatoonIan Vic S. DalisNo ratings yet

- Gemba Walk Checklist QuestionsDocument2 pagesGemba Walk Checklist QuestionsDhurga SivanathanNo ratings yet

- Chapter 1 Project Management The Key To Achieving ResultsDocument40 pagesChapter 1 Project Management The Key To Achieving Resultslyster badenasNo ratings yet

- Applications of Rational ExpressionsDocument3 pagesApplications of Rational ExpressionslzttimNo ratings yet

- Washing Machine: Service ManualDocument59 pagesWashing Machine: Service ManualHama AieaNo ratings yet

- History of Western Society Since 1300 12Th Edition Mckay Test Bank Full Chapter PDFDocument35 pagesHistory of Western Society Since 1300 12Th Edition Mckay Test Bank Full Chapter PDFJakeOwensbnpm100% (12)

- EprDocument8 pagesEprcyrimathewNo ratings yet

- mth202 Solved Subjectives Final Term PDFDocument14 pagesmth202 Solved Subjectives Final Term PDFHumayunKhalid50% (2)

- ISKCON GBC Role and ResponsibilityDocument11 pagesISKCON GBC Role and ResponsibilityDeenanathaNo ratings yet

- 03-04-17 EditionDocument32 pages03-04-17 EditionSan Mateo Daily JournalNo ratings yet

- 123Document10 pages123Aryan SanezNo ratings yet

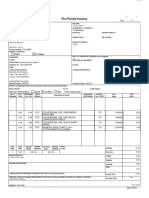

- FACTURADocument1 pageFACTURAAnny CañasNo ratings yet

- The Geology of The Panama-Chocó Arc: Stewart D. RedwoodDocument32 pagesThe Geology of The Panama-Chocó Arc: Stewart D. RedwoodFelipe ArrublaNo ratings yet

- Necromancer Bone Spear Build With Masquerade (Patch 2.6.10 Season 22) - Diablo 3 - Icy Veins 3Document1 pageNecromancer Bone Spear Build With Masquerade (Patch 2.6.10 Season 22) - Diablo 3 - Icy Veins 3filipNo ratings yet

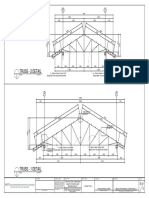

- Truss - 2 Detail: Scale 1: 50 MTRSDocument1 pageTruss - 2 Detail: Scale 1: 50 MTRSGerald MasangayNo ratings yet

- SBL BPP Kit-2019 Copy 457Document1 pageSBL BPP Kit-2019 Copy 457Reever RiverNo ratings yet

- Refrigeration and Air Conditioning Mechanic Harmonized Record Book June 2020Document36 pagesRefrigeration and Air Conditioning Mechanic Harmonized Record Book June 2020Certified Rabbits LoverNo ratings yet

- 3.2.4 - Design Info-Water SupplyDocument5 pages3.2.4 - Design Info-Water SupplyNyu123456No ratings yet

- Adverb Clauses With TimeDocument3 pagesAdverb Clauses With TimeDeni KurniawanNo ratings yet

- WWW Echalone COM: Techalon EDocument26 pagesWWW Echalone COM: Techalon EVara Prasad VemulaNo ratings yet

- Annex 1 - Preparation of GMP Report - ASPECT FinalDocument4 pagesAnnex 1 - Preparation of GMP Report - ASPECT FinalVõ Phi TrúcNo ratings yet

- Internet Programming With Delphi (Marco Cantu)Document14 pagesInternet Programming With Delphi (Marco Cantu)nadutNo ratings yet

- Astm C 750 - 03 Qzc1maDocument4 pagesAstm C 750 - 03 Qzc1mamario neriNo ratings yet

- General Bearing Requirements and Design CriteriaDocument6 pagesGeneral Bearing Requirements and Design Criteriaapi-3701567100% (2)

- Session #9 SAS - Nutrition (Lecture)Document9 pagesSession #9 SAS - Nutrition (Lecture)Mariel Gwen RetorcaNo ratings yet

- Non-Circumvention, Non-Disclosure Agreement (Ncnda)Document5 pagesNon-Circumvention, Non-Disclosure Agreement (Ncnda)fabrizio ballesiNo ratings yet

- Experiment 2 - Classes and Changes in MatterDocument4 pagesExperiment 2 - Classes and Changes in MatterLaurrence CapindianNo ratings yet

- Deployment Guide Series IBM Total Storage Productivity Center For Data Sg247140Document602 pagesDeployment Guide Series IBM Total Storage Productivity Center For Data Sg247140bupbechanhNo ratings yet