Non-Current Assets: Hnda 3 Year - 2 Semester 2016 Advanced Financial Reporting Model Answers

Non-Current Assets: Hnda 3 Year - 2 Semester 2016 Advanced Financial Reporting Model Answers

You might also like

- Magsino Hannah Florence Activity 5 Discounted Cash FlowsDocument36 pagesMagsino Hannah Florence Activity 5 Discounted Cash FlowsKathyrine Claire Edrolin100% (2)

- Customer Service Request FormDocument1 pageCustomer Service Request FormParang Tumpul67% (3)

- Phillip Glass Buys A Loaf of BreadDocument32 pagesPhillip Glass Buys A Loaf of Breadsmtony10No ratings yet

- Study Guide For Brigham Houston Fundamentas of Financial Management-13th Edition - 2012Document1 pageStudy Guide For Brigham Houston Fundamentas of Financial Management-13th Edition - 2012Rajib Dahal50% (2)

- BA 118.3 Module 2 Post and Sage AnswersDocument18 pagesBA 118.3 Module 2 Post and Sage AnswersRed Ashley De LeonNo ratings yet

- Acct6005 Company Accounting: Assessment 2 Case StudyDocument8 pagesAcct6005 Company Accounting: Assessment 2 Case StudyRuhan SinghNo ratings yet

- Jawaban Soal Quiz No 2 Dan 3Document4 pagesJawaban Soal Quiz No 2 Dan 3Anthony indrahalimNo ratings yet

- 4BSA2 GROUP2 GroupActivityNo.1Document4 pages4BSA2 GROUP2 GroupActivityNo.1Lizerie Joy Kristine CristobalNo ratings yet

- Kunci Quiz 3 Bond BaruDocument1 pageKunci Quiz 3 Bond BaruKoko D'DemonsongNo ratings yet

- Pembahasan Kuiz Indirect HoldingsDocument3 pagesPembahasan Kuiz Indirect HoldingsAdara KiranaNo ratings yet

- B2 2021 Nov AnsDocument13 pagesB2 2021 Nov AnsRashid AbeidNo ratings yet

- NPV Lesson 2Document5 pagesNPV Lesson 2Barack MikeNo ratings yet

- Q1) May 2011 ZA Q1 - Ear, Mouth & Nose Mouth LTD Nose LTDDocument8 pagesQ1) May 2011 ZA Q1 - Ear, Mouth & Nose Mouth LTD Nose LTDduong duongNo ratings yet

- BA 118.3 Module 2 - Lesson 2 and 3 - Consolidating Financial StatementsDocument23 pagesBA 118.3 Module 2 - Lesson 2 and 3 - Consolidating Financial StatementsRed Ashley De LeonNo ratings yet

- Ffa ADocument5 pagesFfa Aaccounts officerNo ratings yet

- 1.) Answer: 1 050 000: Prelim Bring Home ExamDocument12 pages1.) Answer: 1 050 000: Prelim Bring Home ExamMary Joy CabilNo ratings yet

- AFAR2 CH. 3 - Problem Quiz 1Document19 pagesAFAR2 CH. 3 - Problem Quiz 1Von Andrei MedinaNo ratings yet

- FAR Final Preboard SolutionsDocument6 pagesFAR Final Preboard SolutionsVillanueva, Mariella De VeraNo ratings yet

- Tugas 5 - InventoryDocument11 pagesTugas 5 - InventoryMuhammad RochimNo ratings yet

- Complete Investment Appraisal - 2Document7 pagesComplete Investment Appraisal - 2Reagan SsebbaaleNo ratings yet

- Exercises On DividendsDocument16 pagesExercises On DividendsGrace RoqueNo ratings yet

- LabChapt 4 Meisya Vianqa ADocument7 pagesLabChapt 4 Meisya Vianqa AMeisya VianqaNo ratings yet

- MN30315 January 2023 Exam - SOLUTIONSDocument15 pagesMN30315 January 2023 Exam - SOLUTIONSjoshuachan1411No ratings yet

- ExpensesDocument3 pagesExpensesJezerie Kaye T. FerrerNo ratings yet

- H.W ch4q7 Acc418Document4 pagesH.W ch4q7 Acc418SARA ALKHODAIRNo ratings yet

- UntitledDocument5 pagesUntitledm habiburrahman55No ratings yet

- Allowable DeductionsDocument9 pagesAllowable DeductionsLyka RoguelNo ratings yet

- Cash Flow Master Question With SolutionDocument6 pagesCash Flow Master Question With Solutionft2vny7nytNo ratings yet

- Answer Key Discussion of Sir Paul of PreweekDocument2 pagesAnswer Key Discussion of Sir Paul of PreweekElaine Joyce GarciaNo ratings yet

- Consolidated FinancialDocument21 pagesConsolidated FinancialMaria Raven Joy Espartinez ValmadridNo ratings yet

- AE 120 Group Activity AnswersDocument5 pagesAE 120 Group Activity AnswersRichard Rhamil Carganillo Garcia Jr.No ratings yet

- REBYUDocument16 pagesREBYUChi EstrellaNo ratings yet

- Group Assesment Part B 1,2,3Document7 pagesGroup Assesment Part B 1,2,3YajZaragozaNo ratings yet

- Via BIR Form 1706Document1 pageVia BIR Form 1706YnnaNo ratings yet

- Corporate Reporting - ND2020 - Suggested - Answers - Review by SBDocument13 pagesCorporate Reporting - ND2020 - Suggested - Answers - Review by SBTamanna KinnoreNo ratings yet

- CPAR B94 FAR Final PB Exam - Answers - SolutionsDocument8 pagesCPAR B94 FAR Final PB Exam - Answers - SolutionsJazehl ValdezNo ratings yet

- Dahon CompanyDocument2 pagesDahon CompanyPrankyJellyNo ratings yet

- Fac2601-2013-6 - Answers PDFDocument9 pagesFac2601-2013-6 - Answers PDFcandiceNo ratings yet

- Problem Solving - Statement of Cash FlowDocument7 pagesProblem Solving - Statement of Cash FlowHossain AlmasNo ratings yet

- For Classroom Discussion: SolutionDocument4 pagesFor Classroom Discussion: SolutionMisherene MagpileNo ratings yet

- Gross Profit For The Year 2021-2023Document6 pagesGross Profit For The Year 2021-2023Beverly DatuNo ratings yet

- Exercises On Implementation of DCF ApproachDocument10 pagesExercises On Implementation of DCF ApproachVincenzoPizzulliNo ratings yet

- BT Tổng Hợp Topic 7 8 2Document12 pagesBT Tổng Hợp Topic 7 8 2Man Tran Y NhiNo ratings yet

- Interco Trans AnsDocument5 pagesInterco Trans Ansmartinfaith958No ratings yet

- AACA2 AssignmentsDocument20 pagesAACA2 AssignmentsadieNo ratings yet

- Spread Sheet ModelingDocument9 pagesSpread Sheet ModelingAbhay BaraNo ratings yet

- Soal AKM 2015Document24 pagesSoal AKM 2015Siti Armayani RayNo ratings yet

- Corporate Tax Return Project Book-Tax Reconciliation (Adrian Purnama)Document6 pagesCorporate Tax Return Project Book-Tax Reconciliation (Adrian Purnama)akpNo ratings yet

- Adv Level Corporate Reporting (CR)Document24 pagesAdv Level Corporate Reporting (CR)FarhadNo ratings yet

- July 22 Far620Document8 pagesJuly 22 Far620FARAH ZAFIRAH ISHAMNo ratings yet

- Nur Atiqah Binti Saadon (Kba2761a) - 2023448576Document3 pagesNur Atiqah Binti Saadon (Kba2761a) - 2023448576nuratiqahsaadon89No ratings yet

- Jawaban 9-1a (Struktur Induk-Anak-Cucu)Document2 pagesJawaban 9-1a (Struktur Induk-Anak-Cucu)felicia sunartaNo ratings yet

- Generales, Capital, 01/01/2022 650,000 Add: Profit 0 Total 650,000 Less: Withdrawals 0 Total: 650,000Document12 pagesGenerales, Capital, 01/01/2022 650,000 Add: Profit 0 Total 650,000 Less: Withdrawals 0 Total: 650,000Kirstelle VelezNo ratings yet

- Sol. Man. - Chapter 14 - Investments in Assoc. - Ia Part 1BDocument15 pagesSol. Man. - Chapter 14 - Investments in Assoc. - Ia Part 1BChristian James RiveraNo ratings yet

- TaxationDocument5 pagesTaxationPauline Jasmine Sta AnaNo ratings yet

- C. Pilar Corporation and Subsidiary Working Paper For Consolidated Financial Statement December 31,2017Document1 pageC. Pilar Corporation and Subsidiary Working Paper For Consolidated Financial Statement December 31,2017Shaira GampongNo ratings yet

- REV AFAR2 - Partnership (Operation)Document10 pagesREV AFAR2 - Partnership (Operation)Richard LamagnaNo ratings yet

- Dr-Acc. Depreciation RM 25 Mill CR - Building RM25 MillDocument7 pagesDr-Acc. Depreciation RM 25 Mill CR - Building RM25 MillsyuhadahNo ratings yet

- Financial Statement Activity W AnswersDocument4 pagesFinancial Statement Activity W AnswersLizlee LaluanNo ratings yet

- 21 FAR460 SS SET 1 Dec21 Kel - StudentDocument9 pages21 FAR460 SS SET 1 Dec21 Kel - StudentRuzaikha razaliNo ratings yet

- Akuntansi Keuangan Lanjutan 2Document6 pagesAkuntansi Keuangan Lanjutan 2Marselinus Aditya Hartanto TjungadiNo ratings yet

- System - Designing PrasentationDocument2 pagesSystem - Designing Prasentationrwl s.r.lNo ratings yet

- Business System AssignmentDocument6 pagesBusiness System Assignmentrwl s.r.lNo ratings yet

- WK 1Document24 pagesWK 1rwl s.r.lNo ratings yet

- SWOT Analysis TemplateDocument3 pagesSWOT Analysis Templaterwl s.r.l100% (1)

- CreditCardStatement 3Document4 pagesCreditCardStatement 3rwl s.r.lNo ratings yet

- 2016 AFR PaperDocument6 pages2016 AFR Paperrwl s.r.lNo ratings yet

- Agency Law: Third-Party General Agent Special Agent Mandate Principal Agent Procuratio MandatumDocument37 pagesAgency Law: Third-Party General Agent Special Agent Mandate Principal Agent Procuratio Mandatumrwl s.r.lNo ratings yet

- Avissawella Area SummaryDocument13 pagesAvissawella Area Summaryrwl s.r.lNo ratings yet

- Corporate Social Responsibilit1Document4 pagesCorporate Social Responsibilit1rwl s.r.lNo ratings yet

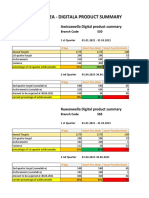

- Embilipitiya Area - Digitala Product SummaryDocument14 pagesEmbilipitiya Area - Digitala Product Summaryrwl s.r.lNo ratings yet

- Corporate Social ResponsibilityDocument3 pagesCorporate Social Responsibilityrwl s.r.lNo ratings yet

- Business Communication Process and Product 7th Edition Guffey Test BankDocument35 pagesBusiness Communication Process and Product 7th Edition Guffey Test Banksoutaneetchingnqcdtv100% (32)

- 500 Words EssayDocument2 pages500 Words EssayEskit Godalle NosidalNo ratings yet

- Cloud Storage Limit Monitoring MeasuresDocument3 pagesCloud Storage Limit Monitoring MeasuresesatjournalsNo ratings yet

- M W Patterson - The Church of EnglandDocument464 pagesM W Patterson - The Church of Englandds1112225198No ratings yet

- Pfi Es-3 (2000)Document4 pagesPfi Es-3 (2000)Esteban Calderón NavarroNo ratings yet

- GO Ms No 38Document93 pagesGO Ms No 38SubhashNo ratings yet

- Canadian Importers Database - HS6-620920-2021-11-20Document2 pagesCanadian Importers Database - HS6-620920-2021-11-20Nikunj SatraNo ratings yet

- PrinciplesDocument13 pagesPrinciplesRosalie PenedaNo ratings yet

- Describe A JourneyDocument15 pagesDescribe A JourneyEmma NguyenNo ratings yet

- Foreign Lang NewsletterDocument1 pageForeign Lang Newsletterapi-544334671No ratings yet

- 08 - Chapter 2 PDFDocument21 pages08 - Chapter 2 PDFSaumya RanjanNo ratings yet

- Путинский нацизм (ENG)Document54 pagesПутинский нацизм (ENG)valeriyap25No ratings yet

- Setup GuideDocument5 pagesSetup GuideBiwott MNo ratings yet

- Opportunities Weight Rating Weighted Score: Chosen Opportunity: Chosen ThreatDocument8 pagesOpportunities Weight Rating Weighted Score: Chosen Opportunity: Chosen ThreatUmbertoNo ratings yet

- Meredith Rosenberg ResumeDocument2 pagesMeredith Rosenberg ResumeMeredith Rosenberg-AlexanderNo ratings yet

- Implementing ERP in OrganizationsDocument12 pagesImplementing ERP in Organizationsprachi_rane_4No ratings yet

- Rationale of The Study: The Scope and Its ProblemDocument52 pagesRationale of The Study: The Scope and Its ProblemCarmen Albiso100% (1)

- Corporate Social Responsibility of CosmoDocument17 pagesCorporate Social Responsibility of CosmoJanvi MehtaNo ratings yet

- Gmail - (ETBEX) Confirmation For Purchase of 1 Ticket(s) From BusOnlineTicket - Com (Ref - VEUQ6QAF)Document1 pageGmail - (ETBEX) Confirmation For Purchase of 1 Ticket(s) From BusOnlineTicket - Com (Ref - VEUQ6QAF)Siriepathi SeetharamanNo ratings yet

- Brigada Eskwela Certificates 2022Document23 pagesBrigada Eskwela Certificates 2022RITCHEL DAGUPANNo ratings yet

- Eng CH 1,2Document3 pagesEng CH 1,2hahirwar35No ratings yet

- Aspire Issue 6Document41 pagesAspire Issue 6HelenNo ratings yet

- PNP Memorandum Circular No 2021-16Document5 pagesPNP Memorandum Circular No 2021-16Dong Lupz100% (2)

- Fin119 Activities PDFDocument226 pagesFin119 Activities PDFjamesbookNo ratings yet

- GLOBAL PRACTICE OF ARCHITECTURE The Impacts of Globalization of The Architectural PracticeDocument1 pageGLOBAL PRACTICE OF ARCHITECTURE The Impacts of Globalization of The Architectural PracticeMark Russell DimayugaNo ratings yet

- Mario Erasmo (2012) - Death Antiquity and Its Legacy (Z-Library)Document194 pagesMario Erasmo (2012) - Death Antiquity and Its Legacy (Z-Library)dserranolozanoNo ratings yet

- Growing The Business, The Value Proposition of The PmoDocument40 pagesGrowing The Business, The Value Proposition of The PmolglfigueiredoNo ratings yet

- The Mineral Industry of CambodiaDocument6 pagesThe Mineral Industry of CambodiaAC-ARIZONACOWBOYNo ratings yet

Download as pdf or txt

You might also like

- Magsino Hannah Florence Activity 5 Discounted Cash FlowsDocument36 pagesMagsino Hannah Florence Activity 5 Discounted Cash FlowsKathyrine Claire Edrolin100% (2)

- Customer Service Request FormDocument1 pageCustomer Service Request FormParang Tumpul67% (3)

- Phillip Glass Buys A Loaf of BreadDocument32 pagesPhillip Glass Buys A Loaf of Breadsmtony10No ratings yet

- Study Guide For Brigham Houston Fundamentas of Financial Management-13th Edition - 2012Document1 pageStudy Guide For Brigham Houston Fundamentas of Financial Management-13th Edition - 2012Rajib Dahal50% (2)

- BA 118.3 Module 2 Post and Sage AnswersDocument18 pagesBA 118.3 Module 2 Post and Sage AnswersRed Ashley De LeonNo ratings yet

- Acct6005 Company Accounting: Assessment 2 Case StudyDocument8 pagesAcct6005 Company Accounting: Assessment 2 Case StudyRuhan SinghNo ratings yet

- Jawaban Soal Quiz No 2 Dan 3Document4 pagesJawaban Soal Quiz No 2 Dan 3Anthony indrahalimNo ratings yet

- 4BSA2 GROUP2 GroupActivityNo.1Document4 pages4BSA2 GROUP2 GroupActivityNo.1Lizerie Joy Kristine CristobalNo ratings yet

- Kunci Quiz 3 Bond BaruDocument1 pageKunci Quiz 3 Bond BaruKoko D'DemonsongNo ratings yet

- Pembahasan Kuiz Indirect HoldingsDocument3 pagesPembahasan Kuiz Indirect HoldingsAdara KiranaNo ratings yet

- B2 2021 Nov AnsDocument13 pagesB2 2021 Nov AnsRashid AbeidNo ratings yet

- NPV Lesson 2Document5 pagesNPV Lesson 2Barack MikeNo ratings yet

- Q1) May 2011 ZA Q1 - Ear, Mouth & Nose Mouth LTD Nose LTDDocument8 pagesQ1) May 2011 ZA Q1 - Ear, Mouth & Nose Mouth LTD Nose LTDduong duongNo ratings yet

- BA 118.3 Module 2 - Lesson 2 and 3 - Consolidating Financial StatementsDocument23 pagesBA 118.3 Module 2 - Lesson 2 and 3 - Consolidating Financial StatementsRed Ashley De LeonNo ratings yet

- Ffa ADocument5 pagesFfa Aaccounts officerNo ratings yet

- 1.) Answer: 1 050 000: Prelim Bring Home ExamDocument12 pages1.) Answer: 1 050 000: Prelim Bring Home ExamMary Joy CabilNo ratings yet

- AFAR2 CH. 3 - Problem Quiz 1Document19 pagesAFAR2 CH. 3 - Problem Quiz 1Von Andrei MedinaNo ratings yet

- FAR Final Preboard SolutionsDocument6 pagesFAR Final Preboard SolutionsVillanueva, Mariella De VeraNo ratings yet

- Tugas 5 - InventoryDocument11 pagesTugas 5 - InventoryMuhammad RochimNo ratings yet

- Complete Investment Appraisal - 2Document7 pagesComplete Investment Appraisal - 2Reagan SsebbaaleNo ratings yet

- Exercises On DividendsDocument16 pagesExercises On DividendsGrace RoqueNo ratings yet

- LabChapt 4 Meisya Vianqa ADocument7 pagesLabChapt 4 Meisya Vianqa AMeisya VianqaNo ratings yet

- MN30315 January 2023 Exam - SOLUTIONSDocument15 pagesMN30315 January 2023 Exam - SOLUTIONSjoshuachan1411No ratings yet

- ExpensesDocument3 pagesExpensesJezerie Kaye T. FerrerNo ratings yet

- H.W ch4q7 Acc418Document4 pagesH.W ch4q7 Acc418SARA ALKHODAIRNo ratings yet

- UntitledDocument5 pagesUntitledm habiburrahman55No ratings yet

- Allowable DeductionsDocument9 pagesAllowable DeductionsLyka RoguelNo ratings yet

- Cash Flow Master Question With SolutionDocument6 pagesCash Flow Master Question With Solutionft2vny7nytNo ratings yet

- Answer Key Discussion of Sir Paul of PreweekDocument2 pagesAnswer Key Discussion of Sir Paul of PreweekElaine Joyce GarciaNo ratings yet

- Consolidated FinancialDocument21 pagesConsolidated FinancialMaria Raven Joy Espartinez ValmadridNo ratings yet

- AE 120 Group Activity AnswersDocument5 pagesAE 120 Group Activity AnswersRichard Rhamil Carganillo Garcia Jr.No ratings yet

- REBYUDocument16 pagesREBYUChi EstrellaNo ratings yet

- Group Assesment Part B 1,2,3Document7 pagesGroup Assesment Part B 1,2,3YajZaragozaNo ratings yet

- Via BIR Form 1706Document1 pageVia BIR Form 1706YnnaNo ratings yet

- Corporate Reporting - ND2020 - Suggested - Answers - Review by SBDocument13 pagesCorporate Reporting - ND2020 - Suggested - Answers - Review by SBTamanna KinnoreNo ratings yet

- CPAR B94 FAR Final PB Exam - Answers - SolutionsDocument8 pagesCPAR B94 FAR Final PB Exam - Answers - SolutionsJazehl ValdezNo ratings yet

- Dahon CompanyDocument2 pagesDahon CompanyPrankyJellyNo ratings yet

- Fac2601-2013-6 - Answers PDFDocument9 pagesFac2601-2013-6 - Answers PDFcandiceNo ratings yet

- Problem Solving - Statement of Cash FlowDocument7 pagesProblem Solving - Statement of Cash FlowHossain AlmasNo ratings yet

- For Classroom Discussion: SolutionDocument4 pagesFor Classroom Discussion: SolutionMisherene MagpileNo ratings yet

- Gross Profit For The Year 2021-2023Document6 pagesGross Profit For The Year 2021-2023Beverly DatuNo ratings yet

- Exercises On Implementation of DCF ApproachDocument10 pagesExercises On Implementation of DCF ApproachVincenzoPizzulliNo ratings yet

- BT Tổng Hợp Topic 7 8 2Document12 pagesBT Tổng Hợp Topic 7 8 2Man Tran Y NhiNo ratings yet

- Interco Trans AnsDocument5 pagesInterco Trans Ansmartinfaith958No ratings yet

- AACA2 AssignmentsDocument20 pagesAACA2 AssignmentsadieNo ratings yet

- Spread Sheet ModelingDocument9 pagesSpread Sheet ModelingAbhay BaraNo ratings yet

- Soal AKM 2015Document24 pagesSoal AKM 2015Siti Armayani RayNo ratings yet

- Corporate Tax Return Project Book-Tax Reconciliation (Adrian Purnama)Document6 pagesCorporate Tax Return Project Book-Tax Reconciliation (Adrian Purnama)akpNo ratings yet

- Adv Level Corporate Reporting (CR)Document24 pagesAdv Level Corporate Reporting (CR)FarhadNo ratings yet

- July 22 Far620Document8 pagesJuly 22 Far620FARAH ZAFIRAH ISHAMNo ratings yet

- Nur Atiqah Binti Saadon (Kba2761a) - 2023448576Document3 pagesNur Atiqah Binti Saadon (Kba2761a) - 2023448576nuratiqahsaadon89No ratings yet

- Jawaban 9-1a (Struktur Induk-Anak-Cucu)Document2 pagesJawaban 9-1a (Struktur Induk-Anak-Cucu)felicia sunartaNo ratings yet

- Generales, Capital, 01/01/2022 650,000 Add: Profit 0 Total 650,000 Less: Withdrawals 0 Total: 650,000Document12 pagesGenerales, Capital, 01/01/2022 650,000 Add: Profit 0 Total 650,000 Less: Withdrawals 0 Total: 650,000Kirstelle VelezNo ratings yet

- Sol. Man. - Chapter 14 - Investments in Assoc. - Ia Part 1BDocument15 pagesSol. Man. - Chapter 14 - Investments in Assoc. - Ia Part 1BChristian James RiveraNo ratings yet

- TaxationDocument5 pagesTaxationPauline Jasmine Sta AnaNo ratings yet

- C. Pilar Corporation and Subsidiary Working Paper For Consolidated Financial Statement December 31,2017Document1 pageC. Pilar Corporation and Subsidiary Working Paper For Consolidated Financial Statement December 31,2017Shaira GampongNo ratings yet

- REV AFAR2 - Partnership (Operation)Document10 pagesREV AFAR2 - Partnership (Operation)Richard LamagnaNo ratings yet

- Dr-Acc. Depreciation RM 25 Mill CR - Building RM25 MillDocument7 pagesDr-Acc. Depreciation RM 25 Mill CR - Building RM25 MillsyuhadahNo ratings yet

- Financial Statement Activity W AnswersDocument4 pagesFinancial Statement Activity W AnswersLizlee LaluanNo ratings yet

- 21 FAR460 SS SET 1 Dec21 Kel - StudentDocument9 pages21 FAR460 SS SET 1 Dec21 Kel - StudentRuzaikha razaliNo ratings yet

- Akuntansi Keuangan Lanjutan 2Document6 pagesAkuntansi Keuangan Lanjutan 2Marselinus Aditya Hartanto TjungadiNo ratings yet

- System - Designing PrasentationDocument2 pagesSystem - Designing Prasentationrwl s.r.lNo ratings yet

- Business System AssignmentDocument6 pagesBusiness System Assignmentrwl s.r.lNo ratings yet

- WK 1Document24 pagesWK 1rwl s.r.lNo ratings yet

- SWOT Analysis TemplateDocument3 pagesSWOT Analysis Templaterwl s.r.l100% (1)

- CreditCardStatement 3Document4 pagesCreditCardStatement 3rwl s.r.lNo ratings yet

- 2016 AFR PaperDocument6 pages2016 AFR Paperrwl s.r.lNo ratings yet

- Agency Law: Third-Party General Agent Special Agent Mandate Principal Agent Procuratio MandatumDocument37 pagesAgency Law: Third-Party General Agent Special Agent Mandate Principal Agent Procuratio Mandatumrwl s.r.lNo ratings yet

- Avissawella Area SummaryDocument13 pagesAvissawella Area Summaryrwl s.r.lNo ratings yet

- Corporate Social Responsibilit1Document4 pagesCorporate Social Responsibilit1rwl s.r.lNo ratings yet

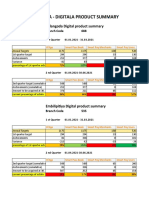

- Embilipitiya Area - Digitala Product SummaryDocument14 pagesEmbilipitiya Area - Digitala Product Summaryrwl s.r.lNo ratings yet

- Corporate Social ResponsibilityDocument3 pagesCorporate Social Responsibilityrwl s.r.lNo ratings yet

- Business Communication Process and Product 7th Edition Guffey Test BankDocument35 pagesBusiness Communication Process and Product 7th Edition Guffey Test Banksoutaneetchingnqcdtv100% (32)

- 500 Words EssayDocument2 pages500 Words EssayEskit Godalle NosidalNo ratings yet

- Cloud Storage Limit Monitoring MeasuresDocument3 pagesCloud Storage Limit Monitoring MeasuresesatjournalsNo ratings yet

- M W Patterson - The Church of EnglandDocument464 pagesM W Patterson - The Church of Englandds1112225198No ratings yet

- Pfi Es-3 (2000)Document4 pagesPfi Es-3 (2000)Esteban Calderón NavarroNo ratings yet

- GO Ms No 38Document93 pagesGO Ms No 38SubhashNo ratings yet

- Canadian Importers Database - HS6-620920-2021-11-20Document2 pagesCanadian Importers Database - HS6-620920-2021-11-20Nikunj SatraNo ratings yet

- PrinciplesDocument13 pagesPrinciplesRosalie PenedaNo ratings yet

- Describe A JourneyDocument15 pagesDescribe A JourneyEmma NguyenNo ratings yet

- Foreign Lang NewsletterDocument1 pageForeign Lang Newsletterapi-544334671No ratings yet

- 08 - Chapter 2 PDFDocument21 pages08 - Chapter 2 PDFSaumya RanjanNo ratings yet

- Путинский нацизм (ENG)Document54 pagesПутинский нацизм (ENG)valeriyap25No ratings yet

- Setup GuideDocument5 pagesSetup GuideBiwott MNo ratings yet

- Opportunities Weight Rating Weighted Score: Chosen Opportunity: Chosen ThreatDocument8 pagesOpportunities Weight Rating Weighted Score: Chosen Opportunity: Chosen ThreatUmbertoNo ratings yet

- Meredith Rosenberg ResumeDocument2 pagesMeredith Rosenberg ResumeMeredith Rosenberg-AlexanderNo ratings yet

- Implementing ERP in OrganizationsDocument12 pagesImplementing ERP in Organizationsprachi_rane_4No ratings yet

- Rationale of The Study: The Scope and Its ProblemDocument52 pagesRationale of The Study: The Scope and Its ProblemCarmen Albiso100% (1)

- Corporate Social Responsibility of CosmoDocument17 pagesCorporate Social Responsibility of CosmoJanvi MehtaNo ratings yet

- Gmail - (ETBEX) Confirmation For Purchase of 1 Ticket(s) From BusOnlineTicket - Com (Ref - VEUQ6QAF)Document1 pageGmail - (ETBEX) Confirmation For Purchase of 1 Ticket(s) From BusOnlineTicket - Com (Ref - VEUQ6QAF)Siriepathi SeetharamanNo ratings yet

- Brigada Eskwela Certificates 2022Document23 pagesBrigada Eskwela Certificates 2022RITCHEL DAGUPANNo ratings yet

- Eng CH 1,2Document3 pagesEng CH 1,2hahirwar35No ratings yet

- Aspire Issue 6Document41 pagesAspire Issue 6HelenNo ratings yet

- PNP Memorandum Circular No 2021-16Document5 pagesPNP Memorandum Circular No 2021-16Dong Lupz100% (2)

- Fin119 Activities PDFDocument226 pagesFin119 Activities PDFjamesbookNo ratings yet

- GLOBAL PRACTICE OF ARCHITECTURE The Impacts of Globalization of The Architectural PracticeDocument1 pageGLOBAL PRACTICE OF ARCHITECTURE The Impacts of Globalization of The Architectural PracticeMark Russell DimayugaNo ratings yet

- Mario Erasmo (2012) - Death Antiquity and Its Legacy (Z-Library)Document194 pagesMario Erasmo (2012) - Death Antiquity and Its Legacy (Z-Library)dserranolozanoNo ratings yet

- Growing The Business, The Value Proposition of The PmoDocument40 pagesGrowing The Business, The Value Proposition of The PmolglfigueiredoNo ratings yet

- The Mineral Industry of CambodiaDocument6 pagesThe Mineral Industry of CambodiaAC-ARIZONACOWBOYNo ratings yet