Download as pdf or txt

You might also like

- LBO Analysis TemplateDocument11 pagesLBO Analysis TemplateBobby Watkins75% (4)

- WMG Business Model SummaryDocument1 pageWMG Business Model SummaryAugustus CignaNo ratings yet

- Digital Supply Networks: Transform Your Supply Chain and Gain Competitive Advantage with Disruptive Technology and Reimagined ProcessesFrom EverandDigital Supply Networks: Transform Your Supply Chain and Gain Competitive Advantage with Disruptive Technology and Reimagined ProcessesRating: 5 out of 5 stars5/5 (5)

- The Analysis of The Impact of Digitalisation in South AfricaDocument19 pagesThe Analysis of The Impact of Digitalisation in South AfricaFady EaliaNo ratings yet

- It ParkDocument8 pagesIt ParkGurpreet Singh67% (3)

- The New IT: How Technology Leaders are Enabling Business Strategy in the Digital AgeFrom EverandThe New IT: How Technology Leaders are Enabling Business Strategy in the Digital AgeNo ratings yet

- Sesi3-Pwerpoint Dato' Dr. Ibrahim Ahmad Bajunid-ColorDocument81 pagesSesi3-Pwerpoint Dato' Dr. Ibrahim Ahmad Bajunid-ColorResearchJSPNo ratings yet

- Pendidikan Sepanjang Hayat - Iradat Dan Tindakan PeribadiDocument113 pagesPendidikan Sepanjang Hayat - Iradat Dan Tindakan Peribadisszma100% (6)

- 5.1 Ramasamy MalaysiaDocument31 pages5.1 Ramasamy MalaysiaDr. Khattab ImranNo ratings yet

- Assignment International Business ManagementDocument5 pagesAssignment International Business ManagementPrabhat ShuklaNo ratings yet

- TELKOM Indonesia - Kongress Indonesia Kompete PDFDocument28 pagesTELKOM Indonesia - Kongress Indonesia Kompete PDFAmir Maro100% (2)

- Kartika Wirjoatmodjo-Vice Minister of State-Owned Enterprises Republic of IndonesiaDocument13 pagesKartika Wirjoatmodjo-Vice Minister of State-Owned Enterprises Republic of Indonesiawardhana wardhanaNo ratings yet

- Gigabit Magazine TruePDF-January 2020 PDFDocument202 pagesGigabit Magazine TruePDF-January 2020 PDFm NNo ratings yet

- Data Science Nigeria Annual ReportDocument64 pagesData Science Nigeria Annual Reportbayo4toyinNo ratings yet

- ED Presentation On Indian IT IndustryDocument26 pagesED Presentation On Indian IT IndustryKunal RajNo ratings yet

- PTC GENERAL TALKS 2019Document77 pagesPTC GENERAL TALKS 2019Syahrul Aidil Mohamad TajuddinNo ratings yet

- Digital EntrepreneurshipDocument6 pagesDigital EntrepreneurshipkiranNo ratings yet

- Infodev's Business Incubator InitiativeDocument5 pagesInfodev's Business Incubator InitiativeeducationcaribbeanNo ratings yet

- Roxas City Digital Roadmap V1Document58 pagesRoxas City Digital Roadmap V1Pinoy TVNo ratings yet

- 220 - HRD - APEC Closing The Digital Skills Gap Report - RevDocument41 pages220 - HRD - APEC Closing The Digital Skills Gap Report - Revokky2006No ratings yet

- Digital Bangladesh PresentationDocument16 pagesDigital Bangladesh PresentationMd. Zahid HossainNo ratings yet

- Unlocking The Potential Business Value By: Data Driven EnterpriseDocument25 pagesUnlocking The Potential Business Value By: Data Driven EnterpriseIcaloke Seger100% (1)

- Technology & Market Assessment in Iraq PDFDocument14 pagesTechnology & Market Assessment in Iraq PDFFadiNo ratings yet

- RDF-ARB Session4 Presentation3 EmploymentAndEconomicGrowth EDocument37 pagesRDF-ARB Session4 Presentation3 EmploymentAndEconomicGrowth EXIKAMNo ratings yet

- Implementando La Transformacion DIgitalDocument33 pagesImplementando La Transformacion DIgitalWalterNo ratings yet

- 2022 - Ghana Innovation Journal ReportDocument45 pages2022 - Ghana Innovation Journal ReportKobina KyemNo ratings yet

- ASEAN Growth and Scale Talent PlaybookDocument86 pagesASEAN Growth and Scale Talent PlaybookRicky KurniawanNo ratings yet

- SkillsFuture - Digital Workplace For Tourist GuidesDocument10 pagesSkillsFuture - Digital Workplace For Tourist GuidesSTBNo ratings yet

- 05 Session 3 - FujitsuDocument20 pages05 Session 3 - FujitsuWelly MahardhikaNo ratings yet

- Reimagining The Future: Anufacturing AS A ServiceDocument32 pagesReimagining The Future: Anufacturing AS A ServiceAnnaNo ratings yet

- Global Network of IncubatoDocument138 pagesGlobal Network of Incubatoapi-3708437No ratings yet

- Submitted By: Mukul Raj Shekhar Bbamba Submitted To: Mrs Saba MamDocument21 pagesSubmitted By: Mukul Raj Shekhar Bbamba Submitted To: Mrs Saba MamMukul Raj ShekharNo ratings yet

- ASIOTI Support For Wantiknas Indonesia July 2019Document18 pagesASIOTI Support For Wantiknas Indonesia July 2019danitoNo ratings yet

- Technical Services & IT SolutionsDocument6 pagesTechnical Services & IT SolutionsVernon VellozoNo ratings yet

- Information and Communicatin TechnologiesDocument13 pagesInformation and Communicatin TechnologiesКундыз МаксутоваNo ratings yet

- GoI, Annual Report, IT, 2008-09Document116 pagesGoI, Annual Report, IT, 2008-09Deepak PareekNo ratings yet

- 2017 Salary Benefits Skills in Vietnam - Report by TopITworks - enDocument40 pages2017 Salary Benefits Skills in Vietnam - Report by TopITworks - enpesbarcavnNo ratings yet

- Digitale Agenda ENGELSE VERSIEDocument44 pagesDigitale Agenda ENGELSE VERSIEMichael WallNo ratings yet

- Computer Art Integrated ProjectDocument10 pagesComputer Art Integrated Projectsheen cyriac mathewNo ratings yet

- AI Application & Digi-Tech Summit & Expo - BroDocument4 pagesAI Application & Digi-Tech Summit & Expo - BrokavenindiaNo ratings yet

- 4 Hal - Industrial Transformation Indonesia BrosurDocument4 pages4 Hal - Industrial Transformation Indonesia Brosurindra faisalNo ratings yet

- DTI 2021 Priority PAPsDocument70 pagesDTI 2021 Priority PAPsVictoria SalazarNo ratings yet

- Policy For The Networked Society: Rene SummerDocument28 pagesPolicy For The Networked Society: Rene Summerabey.mulugetaNo ratings yet

- 3rd DTI Presentation Leonard FloresDocument37 pages3rd DTI Presentation Leonard FloresDerwin DomiderNo ratings yet

- FIle 1 - MDocument48 pagesFIle 1 - MTomás CastañedaNo ratings yet

- Approaching Infrastructure For Planning of Cities Digitalization Smart CitiesDocument3 pagesApproaching Infrastructure For Planning of Cities Digitalization Smart CitiesIJARP PublicationsNo ratings yet

- Building Without Barriers: Do You Own, Operate, Construct or Maintain Physical Built Assets?Document10 pagesBuilding Without Barriers: Do You Own, Operate, Construct or Maintain Physical Built Assets?Unknown020No ratings yet

- Labor Market InformationDocument60 pagesLabor Market InformationHershell ContaNo ratings yet

- Knowledge Economy in PakistanDocument18 pagesKnowledge Economy in Pakistan77chimNo ratings yet

- DSInnovate Startup Report 2023Document50 pagesDSInnovate Startup Report 2023Arman WiratmokoNo ratings yet

- Roxas City Digital Roadmap 2022Document49 pagesRoxas City Digital Roadmap 2022armagnetoNo ratings yet

- Tullao Fernandez Cabuay SerranoDocument4 pagesTullao Fernandez Cabuay SerranoyelNo ratings yet

- Office of The Project Director: Bangladesh Hi-Tech Park AuthorityDocument3 pagesOffice of The Project Director: Bangladesh Hi-Tech Park Authorityএম আর সজীবNo ratings yet

- MNC Investor Forum 2021 v3Document10 pagesMNC Investor Forum 2021 v3Deddy Mahyarto Kresnoputro PrawirodirdjoNo ratings yet

- Lecture2 2 Msia HistoryDocument23 pagesLecture2 2 Msia HistoryTommy Dee..Death Silent87No ratings yet

- 2018-06-11 The European Construction Industry Manifesto On Digital Construction - A4Document4 pages2018-06-11 The European Construction Industry Manifesto On Digital Construction - A4CPittmanNo ratings yet

- Materi Sesi 1. Swasono SatyoDocument16 pagesMateri Sesi 1. Swasono SatyowosamotaNo ratings yet

- VanillaPlus IoT Report 2017Document9 pagesVanillaPlus IoT Report 2017hoainamcomitNo ratings yet

- Artifical Intelligence InvestmentOpportunityBriefDocument17 pagesArtifical Intelligence InvestmentOpportunityBriefRoseller Sumonod100% (1)

- Winning in 2025: Digital and Data Transformation: The Keys to SuccessFrom EverandWinning in 2025: Digital and Data Transformation: The Keys to SuccessNo ratings yet

- Digital Senegal for Inclusive Growth: Technological Transformation for Better and More JobsFrom EverandDigital Senegal for Inclusive Growth: Technological Transformation for Better and More JobsNo ratings yet

- Forgiveness and ReconciliationDocument7 pagesForgiveness and ReconciliationJoseph Kuria100% (1)

- Rwanda - Rwanda Automated Local Government Revenue Management System - EOIDocument3 pagesRwanda - Rwanda Automated Local Government Revenue Management System - EOIJoseph KuriaNo ratings yet

- Health Benefits of Vegetables and FruitsDocument57 pagesHealth Benefits of Vegetables and FruitsJoseph KuriaNo ratings yet

- NAROK COUNTY - MarginalizationDocument6 pagesNAROK COUNTY - MarginalizationJoseph KuriaNo ratings yet

- Hacks To Lose WeightDocument7 pagesHacks To Lose WeightJoseph Kuria100% (1)

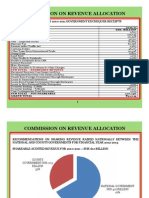

- Commission On Revenua Allocation PresentationDocument7 pagesCommission On Revenua Allocation PresentationJoseph KuriaNo ratings yet

- BIR Collection and Payment Summary SampleDocument14 pagesBIR Collection and Payment Summary SampleNeeco1 FinanceNo ratings yet

- This Study Resource Was: E-Tivity 3: On Basics of Process and Job Order Costing and Short Exercise DrillDocument1 pageThis Study Resource Was: E-Tivity 3: On Basics of Process and Job Order Costing and Short Exercise DrillitsmenatoyNo ratings yet

- How Multiple Strategic Orientations Impact Brand Equity of B2B SmesDocument22 pagesHow Multiple Strategic Orientations Impact Brand Equity of B2B SmesimamNo ratings yet

- Group 9Document10 pagesGroup 9normieotaku2001No ratings yet

- Marketplace Tracker v2Document23 pagesMarketplace Tracker v2Sandi IrawanNo ratings yet

- Global Hospitality PortalDocument1 pageGlobal Hospitality PortalKhanxa KhanNo ratings yet

- PRTY Party City Corporate Presentation October 2017Document28 pagesPRTY Party City Corporate Presentation October 2017Ala BasterNo ratings yet

- Lesson 1 - The Nature and Forms of Business OrganizationDocument3 pagesLesson 1 - The Nature and Forms of Business OrganizationJose Emmanuel CalagNo ratings yet

- PS - Activity No. 4Document2 pagesPS - Activity No. 4eliakimNo ratings yet

- Business Paper COMPLETEDocument3 pagesBusiness Paper COMPLETEDavid KaranuNo ratings yet

- Importance of Managerial EconomicsDocument5 pagesImportance of Managerial Economicsprabhatrc4235100% (2)

- W. W. Grainger: Maintenance, Repair and Operations (MRO) ProductsDocument33 pagesW. W. Grainger: Maintenance, Repair and Operations (MRO) ProductsHitisha agrawalNo ratings yet

- Snake LTD - Class WorkingsDocument2 pagesSnake LTD - Class Workingsmusa morinNo ratings yet

- Introduction To Consumer Behavior: Unit IDocument39 pagesIntroduction To Consumer Behavior: Unit ILalith Sai Yaswanth YadavNo ratings yet

- Packaging and Marketing Household Linens II GRADE 6 DLPDocument5 pagesPackaging and Marketing Household Linens II GRADE 6 DLPElizabeth Tausa100% (1)

- FIA - MA2 - Final Mock Exam - Qs - 2023Document18 pagesFIA - MA2 - Final Mock Exam - Qs - 2023cnarinNo ratings yet

- Case Study: Culture Clash in The Boardroom OB AssignmentDocument4 pagesCase Study: Culture Clash in The Boardroom OB AssignmentmohammedNo ratings yet

- Lesson 2 2Document15 pagesLesson 2 2Angela MagtibayNo ratings yet

- Loan Application Form Please Complete in BLOCK LETTERS.: Office UseDocument4 pagesLoan Application Form Please Complete in BLOCK LETTERS.: Office UseKennedy SimumbaNo ratings yet

- English Biscuit ManufacturersDocument5 pagesEnglish Biscuit ManufacturersfizaAhaiderNo ratings yet

- Finance Company: DirectoryDocument6 pagesFinance Company: DirectoryLara Silva AndradeNo ratings yet

- RFQ For Early Train Operator ADDENDUM3Document88 pagesRFQ For Early Train Operator ADDENDUM3jackson michaelNo ratings yet

- Retail Offer Advantage Through Brand Orienttaion in Luxury High Fashion StoresDocument161 pagesRetail Offer Advantage Through Brand Orienttaion in Luxury High Fashion StoresSugan PragasamNo ratings yet

- Description and Use: Date: Rev. 0Document1 pageDescription and Use: Date: Rev. 0corporacion kbboNo ratings yet

- Model Lucrare de Licenta Universitatea Transilvania Din BrașovDocument41 pagesModel Lucrare de Licenta Universitatea Transilvania Din BrașovElena MădălinaNo ratings yet

- Strategic Audit and Strategy Evaluation & ControlDocument47 pagesStrategic Audit and Strategy Evaluation & Controlshweta_4666493% (14)

- Exam 2 Q&ADocument7 pagesExam 2 Q&AJennifer WillardNo ratings yet

- 2018 Shelby Township Bill RunsDocument893 pages2018 Shelby Township Bill RunsBlahNo ratings yet