Download as docx, pdf, or txt

You might also like

- Carlinsoskice Solutions ch03Document15 pagesCarlinsoskice Solutions ch03Clara LustosaNo ratings yet

- Praktikum Akuntansi Biaya 2021 VEA - Template KerjaDocument228 pagesPraktikum Akuntansi Biaya 2021 VEA - Template KerjaHendy Prastyo W0% (2)

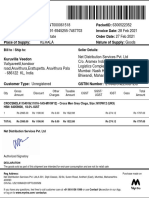

- Bill To / Ship To: Seller DetailsDocument1 pageBill To / Ship To: Seller DetailsErick MathewNo ratings yet

- LSCM Case StudyDocument14 pagesLSCM Case StudyBittoo Sharma0% (1)

- Monetary Policy of IndiaDocument34 pagesMonetary Policy of IndiaJhankar MishraNo ratings yet

- 1.1 Monetary PolicyDocument77 pages1.1 Monetary PolicyS SrinivasanNo ratings yet

- Monetary Policy of IndiaDocument5 pagesMonetary Policy of IndiaSudesh SharmaNo ratings yet

- Monetary PolicyDocument10 pagesMonetary PolicyPRAKHAR KAUSHIKNo ratings yet

- What Is Monetary PolicyDocument5 pagesWhat Is Monetary PolicyBhagat DeepakNo ratings yet

- What Is A Liquidity Adjustment Facility?Document4 pagesWhat Is A Liquidity Adjustment Facility?Shiva MehtaNo ratings yet

- Assignment of Buisness Enviroment MGT 511: TOPIC: Changes in Monetary Policy On Banking Sector or IndustryDocument9 pagesAssignment of Buisness Enviroment MGT 511: TOPIC: Changes in Monetary Policy On Banking Sector or IndustryRohit VermaNo ratings yet

- Top of FormDocument14 pagesTop of Formprnjlgoswami86No ratings yet

- Credit ControlDocument5 pagesCredit ControlHimanshu GargNo ratings yet

- Fiscal and Monetary PolicyDocument17 pagesFiscal and Monetary Policyrajan tiwariNo ratings yet

- Monetary Policy in IndiaDocument8 pagesMonetary Policy in Indiaamitwaghela50No ratings yet

- Monetary Policy and Its Instruments: DefinitionDocument11 pagesMonetary Policy and Its Instruments: Definitionamandeep singhNo ratings yet

- Monetary Policy Initiatives Since 2008-09 and Its Effectiveness in Containing Inflation"Document31 pagesMonetary Policy Initiatives Since 2008-09 and Its Effectiveness in Containing Inflation"Arpit PangasaNo ratings yet

- Rbi Monetary PolicyDocument5 pagesRbi Monetary PolicyRohit GuptaNo ratings yet

- Monetary Policy of India - WikipediaDocument4 pagesMonetary Policy of India - Wikipediaambikesh008No ratings yet

- Monetary Policy Is of Two KindsDocument16 pagesMonetary Policy Is of Two KindsSainath SindheNo ratings yet

- What Is Monetary Policy?Document13 pagesWhat Is Monetary Policy?meghakharkwalNo ratings yet

- Monetary PolicyDocument39 pagesMonetary PolicyTirupal PuliNo ratings yet

- Monetary Policy Monetary Policy DefinedDocument9 pagesMonetary Policy Monetary Policy DefinedXyz YxzNo ratings yet

- RBI Credit Policy (Rough)Document15 pagesRBI Credit Policy (Rough)Nidhi NavneetNo ratings yet

- Monetary Policy NotesDocument13 pagesMonetary Policy NotesMehak joshiNo ratings yet

- Ibe - Unit-3Document37 pagesIbe - Unit-3Pranav YeleswarapuNo ratings yet

- News Analysis (05 Mar, 2022)Document22 pagesNews Analysis (05 Mar, 2022)Vivaswan DeekshitNo ratings yet

- Financial Management Report: On "Repo Rate and Impact On GDP"Document10 pagesFinancial Management Report: On "Repo Rate and Impact On GDP"Anjali BhatiaNo ratings yet

- Monetary Policy - IndicatorsDocument4 pagesMonetary Policy - IndicatorsGJ RamNo ratings yet

- Indian Economy Part-II in EnglishDocument116 pagesIndian Economy Part-II in EnglishWTF NewsNo ratings yet

- Monetary Policy Rbi PPT NewDocument14 pagesMonetary Policy Rbi PPT Newpraharshitha100% (2)

- Monetary PolicyDocument15 pagesMonetary PolicyGurvi SinghNo ratings yet

- 9 1Document17 pages9 1VikasRoshanNo ratings yet

- Central Bank & Monetary Policy - 1Document30 pagesCentral Bank & Monetary Policy - 1Dr.Ashok Kumar PanigrahiNo ratings yet

- Credit Authorisation SchemeDocument6 pagesCredit Authorisation SchemeOngwang KonyakNo ratings yet

- Monetary PolicyDocument23 pagesMonetary PolicyManjunath ShettigarNo ratings yet

- Central BankingDocument24 pagesCentral BankingKARISHMAATA2No ratings yet

- Monetary PolicyDocument18 pagesMonetary PolicySarada NagNo ratings yet

- Assignment 2 Monetary PolicyDocument14 pagesAssignment 2 Monetary PolicyAman BrarNo ratings yet

- Monetary PolicyDocument3 pagesMonetary PolicymbapritiNo ratings yet

- Balaji - Eco - Module 4 & 5Document13 pagesBalaji - Eco - Module 4 & 5Sami NisarNo ratings yet

- Monetary PolicyDocument15 pagesMonetary PolicyrajagctNo ratings yet

- Fiscal and Monetary PolicyDocument17 pagesFiscal and Monetary PolicySuresh Sen100% (1)

- Monetary and Credit Policy of RBIDocument9 pagesMonetary and Credit Policy of RBIHONEYNo ratings yet

- Group3 - Monetory & Credit PolicyDocument23 pagesGroup3 - Monetory & Credit PolicyDivya SinghNo ratings yet

- RBI's Monetary Measures To Monitor Recession: Issue VII - April 2011Document5 pagesRBI's Monetary Measures To Monitor Recession: Issue VII - April 2011prakhar jainNo ratings yet

- Monetary Policy ReviewsDocument6 pagesMonetary Policy ReviewspundirsandeepNo ratings yet

- Monetary Policy of IndiaDocument6 pagesMonetary Policy of IndiaKushal PatilNo ratings yet

- Monetary Policy RBI.Document28 pagesMonetary Policy RBI.santoshys50% (2)

- Monetary Policy ToolsDocument7 pagesMonetary Policy ToolsDeepak PathakNo ratings yet

- The Goal(s) of Monetary PolicyDocument8 pagesThe Goal(s) of Monetary PolicyHafiz Saddique MalikNo ratings yet

- Credit Control by RBIDocument10 pagesCredit Control by RBIRishi exportsNo ratings yet

- Monetary Policy - Managerial EconomicsDocument2 pagesMonetary Policy - Managerial EconomicsPrincess Ela Mae CatibogNo ratings yet

- Monetary and Fiscal PoliciesDocument27 pagesMonetary and Fiscal PoliciesEkta SuriNo ratings yet

- Monetary Policy PresentationDocument22 pagesMonetary Policy Presentationanon_792919970No ratings yet

- Monetary Policy: Reserve Bank of IndiaDocument5 pagesMonetary Policy: Reserve Bank of IndiaRicky RoyNo ratings yet

- Financial Institutions and Markets ProjectDocument10 pagesFinancial Institutions and Markets ProjectPallavi AgrawallaNo ratings yet

- Monetary PolicyDocument5 pagesMonetary PolicyThiruNo ratings yet

- Monetary Policy: By-Rahul Prajapat Cmat 1St SemDocument6 pagesMonetary Policy: By-Rahul Prajapat Cmat 1St SemRahul PrajapatNo ratings yet

- Central BankingDocument28 pagesCentral Bankingneha16septNo ratings yet

- Monetary Policy of RBI (Feb, 2018)Document6 pagesMonetary Policy of RBI (Feb, 2018)Pranit ShahNo ratings yet

- RBI Credit Control in IndiaDocument11 pagesRBI Credit Control in IndiaDeepjyotiNo ratings yet

- Financial Soundness Indicators for Financial Sector Stability: A Tale of Three Asian CountriesFrom EverandFinancial Soundness Indicators for Financial Sector Stability: A Tale of Three Asian CountriesNo ratings yet

- NameDocument1 pageNameORGI GROWNo ratings yet

- 7 Major Barriers To International TradeDocument3 pages7 Major Barriers To International TradeMuzaFar50% (8)

- Mansa-X KES Fact Sheet Q1 2023Document1 pageMansa-X KES Fact Sheet Q1 2023KevinNo ratings yet

- Who Is A Service Exporter?: Posted On 04 February 2019 Category: For Beginners (/For-Beginners/default - Aspx)Document4 pagesWho Is A Service Exporter?: Posted On 04 February 2019 Category: For Beginners (/For-Beginners/default - Aspx)amit kumarNo ratings yet

- Working Capital ManagementDocument60 pagesWorking Capital ManagementkirubelNo ratings yet

- Chapter 22 - Business Finance - Needs and SourcesDocument3 pagesChapter 22 - Business Finance - Needs and SourcesKhoa DaoNo ratings yet

- Bill of Lading For Ocean Transport or Multimodal TransportDocument45 pagesBill of Lading For Ocean Transport or Multimodal TransportAndrea MuñozNo ratings yet

- The Competitiveness of Ready Made Garments Industry of Bangladesh in Post MFA EraDocument11 pagesThe Competitiveness of Ready Made Garments Industry of Bangladesh in Post MFA EraMohammad Mushfiqur Rahman KhanNo ratings yet

- Principles of Business For CSEC®: 2nd EditionDocument6 pagesPrinciples of Business For CSEC®: 2nd EditionKerine Williams-FigaroNo ratings yet

- Changxing Bufuna Textile Co., LTD.: We Hereby Confirm The Sales Information As BelowDocument1 pageChangxing Bufuna Textile Co., LTD.: We Hereby Confirm The Sales Information As BelowALRAYAN GOLDNo ratings yet

- CU-2021 B.A. B.sc. (Honours) Economics Semester-3 Paper-CC-5 QPDocument3 pagesCU-2021 B.A. B.sc. (Honours) Economics Semester-3 Paper-CC-5 QPsourojeetsenNo ratings yet

- Certificate of Insurance 2Document3 pagesCertificate of Insurance 2patmaroopan22No ratings yet

- Test Bank For International Economics 13th Edition Dominick SalvatoreDocument4 pagesTest Bank For International Economics 13th Edition Dominick Salvatorerillefroweyt4mNo ratings yet

- CH 1 - Scope of International FinanceDocument7 pagesCH 1 - Scope of International Financepritesh_baidya269100% (3)

- Tax Invoice Original AmountDocument8 pagesTax Invoice Original AmountaroshrokzzzNo ratings yet

- Kklujkt436403 BL - Copy 20210312 082402Document5 pagesKklujkt436403 BL - Copy 20210312 082402Dysa Satria AnggaraNo ratings yet

- GST and BankingDocument8 pagesGST and BankingRudranil RoyNo ratings yet

- Nouns: Activity, Service, Materials, Operation, Production, Opportunities, SystemDocument2 pagesNouns: Activity, Service, Materials, Operation, Production, Opportunities, SystemPaulius KnezevičiusNo ratings yet

- Financing Your Franchised BusinessDocument17 pagesFinancing Your Franchised BusinessDanna Marie BanayNo ratings yet

- Economics 2019 v1.1: IA1 High-Level Annotated Sample ResponseDocument8 pagesEconomics 2019 v1.1: IA1 High-Level Annotated Sample ResponseAahz MandiusNo ratings yet

- Liquor Retailers Selected BackgrounderDocument2 pagesLiquor Retailers Selected BackgrounderDavid A. GilesNo ratings yet

- Chapter 13 Refund Under GSTDocument68 pagesChapter 13 Refund Under GSTDR. PREETI JINDALNo ratings yet

- Tutorial 9 & 10-Qs-2Document2 pagesTutorial 9 & 10-Qs-2YunesshwaaryNo ratings yet

- Topic 2 - Australia's Place in The Global EconomyDocument19 pagesTopic 2 - Australia's Place in The Global EconomyKRISH SURANANo ratings yet

- Economies of ScaleDocument24 pagesEconomies of ScaleRohan SrivastavaNo ratings yet

- Test Kl.9.b.tremujori 3.spark 4Document4 pagesTest Kl.9.b.tremujori 3.spark 4Ester XhaferriNo ratings yet