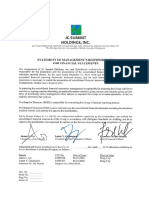

Auditors Report Standalone

Auditors Report Standalone

You might also like

- Advanced Accounting: Partnership LiquidationDocument33 pagesAdvanced Accounting: Partnership LiquidationVeesNo ratings yet

- Robi Axiata Limited: Report and Financial Statements As at and For The Year Ended 31 December 2019Document97 pagesRobi Axiata Limited: Report and Financial Statements As at and For The Year Ended 31 December 2019Anika hossainNo ratings yet

- Consolidated Financial StatementsDocument136 pagesConsolidated Financial Statementsganesh PALNo ratings yet

- Ar-18 7Document5 pagesAr-18 7jawad anwarNo ratings yet

- Kapco FinancialsDocument63 pagesKapco FinancialsGhulam MustafaNo ratings yet

- Financial Statements 201819 PDFDocument133 pagesFinancial Statements 201819 PDFRobinsNo ratings yet

- Cellnex Individual Annual Accounts and Management Report 2020 1Document234 pagesCellnex Individual Annual Accounts and Management Report 2020 1Fauzi Al nassarNo ratings yet

- Standalone FinancialDocument72 pagesStandalone FinancialRadhika AgrawalNo ratings yet

- Financial StatementsDocument181 pagesFinancial StatementsDivitya ChaudharyNo ratings yet

- Relience 2021 2022 ConsolidatedDocument107 pagesRelience 2021 2022 ConsolidatedpritamNo ratings yet

- Dabur Standalone FinancialsDocument83 pagesDabur Standalone Financialsankittomarrajput95No ratings yet

- Standalone Financial StatementsDocument68 pagesStandalone Financial StatementsMaaz ShamsherNo ratings yet

- Grameenphone Accounts 2020Document62 pagesGrameenphone Accounts 2020JUNAYED AHMED RAFINNo ratings yet

- Financial StatementsDocument198 pagesFinancial StatementsRK15 21100% (1)

- E MFC Afs 2019Document84 pagesE MFC Afs 2019Cassandra Ivana BermudezNo ratings yet

- Consolidated FinancialstmtDocument130 pagesConsolidated Financialstmtsahadhiraj1No ratings yet

- Reliance General Insurance Company Limited 2020-21Document70 pagesReliance General Insurance Company Limited 2020-21yaminp292No ratings yet

- Dabur ConsolidatedDocument92 pagesDabur ConsolidatedRatla Bhukya Rama KrishnaNo ratings yet

- Financial Statements For The Year 2019Document174 pagesFinancial Statements For The Year 2019MD. ISRAFIL PALASHNo ratings yet

- LG Chem, LTD.: Separate Financial Statements and Internal Control Over Financial Reporting December 31, 2019 and 2018Document97 pagesLG Chem, LTD.: Separate Financial Statements and Internal Control Over Financial Reporting December 31, 2019 and 2018Ayushika SinghNo ratings yet

- Independent Auditor's Report: Corporate Board and Management Reports Financial StatementsDocument81 pagesIndependent Auditor's Report: Corporate Board and Management Reports Financial Statements198 Murzello MignonneNo ratings yet

- E - MFC English Q423 FSDocument123 pagesE - MFC English Q423 FSEvan LoirtNo ratings yet

- Sleep Country Canada Holding IncDocument44 pagesSleep Country Canada Holding IncSunira PaudelNo ratings yet

- BWCL - 2020 Bestway Cement Limited - OpenDoors - PKDocument142 pagesBWCL - 2020 Bestway Cement Limited - OpenDoors - PKzainNo ratings yet

- TataSteel-IR23_Standalone-FinancialsDocument120 pagesTataSteel-IR23_Standalone-FinancialsJose HernandesNo ratings yet

- Audit BoschDocument55 pagesAudit BoschRohan SakhareNo ratings yet

- Ian - Chapter 3 #11 ValuationDocument11 pagesIan - Chapter 3 #11 ValuationBae Xu KaiNo ratings yet

- Format of New Audit ReportDocument4 pagesFormat of New Audit ReportSarowar AlamNo ratings yet

- LG Chem 2020 Contingent Financial StatementsDocument102 pagesLG Chem 2020 Contingent Financial StatementsAyushika SinghNo ratings yet

- Optiva Inc. Q4 2021 Financial Statements FinalDocument63 pagesOptiva Inc. Q4 2021 Financial Statements FinaldivyaNo ratings yet

- 1197astra AR 19-20 Final Organized PDFDocument8 pages1197astra AR 19-20 Final Organized PDFelenaNo ratings yet

- Standalone Financials 21Document101 pagesStandalone Financials 21rupikagupta1903No ratings yet

- TP Central Odisha Distribution Limited FY22 23Document62 pagesTP Central Odisha Distribution Limited FY22 23Soumya Ranjan PattnaikNo ratings yet

- RRHIS A1.1.0 CFS1219 Robinsons Retail Holdings IncDocument98 pagesRRHIS A1.1.0 CFS1219 Robinsons Retail Holdings Incherrera.angelaNo ratings yet

- SESI 10 ch17 - External Auditing Function - LectureDocument109 pagesSESI 10 ch17 - External Auditing Function - LecturekimkimberlyNo ratings yet

- ConsolidatedDocument76 pagesConsolidatedarunkumar.vxlNo ratings yet

- Hero Financial STMTDocument141 pagesHero Financial STMTLaksh SinghalNo ratings yet

- CAM-Accounting For Income Taxes - Nike 2020 10KDocument1 pageCAM-Accounting For Income Taxes - Nike 2020 10KnofeNo ratings yet

- SFG Consolidated FY2022.4Q FinalDocument291 pagesSFG Consolidated FY2022.4Q FinalSi Joon RyuNo ratings yet

- HBL Annual Report 2023Document4 pagesHBL Annual Report 2023azeem sandhuNo ratings yet

- SBI Life IAR 203 404 Download CenterDocument202 pagesSBI Life IAR 203 404 Download Centershashikumarb2277No ratings yet

- February 12, 2021: Consolidated Financial Statements and NotesDocument77 pagesFebruary 12, 2021: Consolidated Financial Statements and NotesAnujaNo ratings yet

- Dongyue Report 2023 + UpdateDocument85 pagesDongyue Report 2023 + UpdateRobert ManjoNo ratings yet

- AF304 Major Assignment DraftDocument25 pagesAF304 Major Assignment DraftShilpa KumarNo ratings yet

- Latest Sample Auditors ReportDocument5 pagesLatest Sample Auditors ReportABDUL REHMAN WARRIACHNo ratings yet

- Independent Auditors' Report: Basis For OpinionDocument10 pagesIndependent Auditors' Report: Basis For OpiniondeepakNo ratings yet

- Audited ReportDocument36 pagesAudited ReportverdeepNo ratings yet

- CAM-Acquisition of Business and Uncertain Tax Positions - IBM 2019 10KDocument2 pagesCAM-Acquisition of Business and Uncertain Tax Positions - IBM 2019 10KnofeNo ratings yet

- JG Summit Annual - FS 2019 PDFDocument210 pagesJG Summit Annual - FS 2019 PDFZo ThelfNo ratings yet

- China Ocean Group Development Limited (March 24) Draft ReportDocument65 pagesChina Ocean Group Development Limited (March 24) Draft ReportRobert ManjoNo ratings yet

- Unilever Financial StatementDocument77 pagesUnilever Financial StatementIrene CapilitanNo ratings yet

- Hero Financial STMTDocument149 pagesHero Financial STMTLaksh SinghalNo ratings yet

- Standalone Financials 2021 22Document82 pagesStandalone Financials 2021 22Adesh MarwariNo ratings yet

- Icai Final SyllabusDocument18 pagesIcai Final SyllabusJD Shah FamilyNo ratings yet

- Template of Auditors Report For Life Insurance Company in BangladeshDocument11 pagesTemplate of Auditors Report For Life Insurance Company in BangladeshMohammad IslamNo ratings yet

- 2022 02 28 Gestamp Automocion 2021 Consolidated Financial StatementsDocument333 pages2022 02 28 Gestamp Automocion 2021 Consolidated Financial StatementsRicardo SequeiraNo ratings yet

- Ashourn Industries Audit Opinion 2023Document2 pagesAshourn Industries Audit Opinion 2023millydengu18No ratings yet

- 2022년 영문연결감사보고서Document92 pages2022년 영문연결감사보고서Thu HồngNo ratings yet

- 2019 Audit Report (Separate)Document86 pages2019 Audit Report (Separate)tasnimaNo ratings yet

- HayleysDocument7 pagesHayleysSANDALI FERNANDONo ratings yet

- Audit Risk Alert: General Accounting and Auditing Developments, 2017/18From EverandAudit Risk Alert: General Accounting and Auditing Developments, 2017/18No ratings yet

- HCR 3031Document3 pagesHCR 3031Rob PortNo ratings yet

- Las Normas NIIF Ilustradas Parte BDocument6 pagesLas Normas NIIF Ilustradas Parte BRampante2014No ratings yet

- EDITED ALICE Motion Correction To Amend Final OrderDocument3 pagesEDITED ALICE Motion Correction To Amend Final OrderJenifer PaglinawanNo ratings yet

- 482 Quashing Shibani Parti & AnotherDocument14 pages482 Quashing Shibani Parti & AnotherOjaswa PathakNo ratings yet

- 15 U.S. Code 1692e - False or Misleading Representations - U.S. Code - US Law - LII - Legal Information InstituteDocument4 pages15 U.S. Code 1692e - False or Misleading Representations - U.S. Code - US Law - LII - Legal Information InstituteJunius EdwardNo ratings yet

- Questions Asked in RRB NTPC 30 Dec 2020 All ShiftDocument4 pagesQuestions Asked in RRB NTPC 30 Dec 2020 All ShiftVipul BhardwajNo ratings yet

- Frcra (Q5ffi9rr6q, IH: TF, (, (IlrcqDocument3 pagesFrcra (Q5ffi9rr6q, IH: TF, (, (IlrcqSam SamNo ratings yet

- Edited - Jadwal Pengawas PTS Gasal 2324Document1 pageEdited - Jadwal Pengawas PTS Gasal 2324Irawan Joko HariyonoNo ratings yet

- Role & Responsibilities of ICC Under POSH - Program BrochureDocument3 pagesRole & Responsibilities of ICC Under POSH - Program BrochureKARNA JayNo ratings yet

- May 21 Thornburg Incident ReportDocument2 pagesMay 21 Thornburg Incident ReportJ RohrlichNo ratings yet

- CFN 9334 Law Question PaperDocument2 pagesCFN 9334 Law Question PaperSurya SinghNo ratings yet

- Ftra 2 RenewalDocument3 pagesFtra 2 RenewalNimiloteNo ratings yet

- Kaplan Order in Carroll Defamation CaseDocument2 pagesKaplan Order in Carroll Defamation CaseLaw&Crime100% (2)

- Marcos BurialDocument9 pagesMarcos BurialVic DizonNo ratings yet

- Taxn Quiz Number 1Document16 pagesTaxn Quiz Number 1justine cabanaNo ratings yet

- Duty of CareDocument79 pagesDuty of CareMuhamad HanafiNo ratings yet

- Latin MaximDocument10 pagesLatin MaximPeng ManiegoNo ratings yet

- Test Bank For Human Heredity Principles and Issues 11th EditionDocument36 pagesTest Bank For Human Heredity Principles and Issues 11th Editionoutborn.piste5ols3q100% (50)

- Different Kinds of Obligation (Midterms)Document17 pagesDifferent Kinds of Obligation (Midterms)Jay GalleroNo ratings yet

- Cis Naviera Meljacan SLDocument3 pagesCis Naviera Meljacan SLİbrahim KocakNo ratings yet

- Use of Pro SeDocument6 pagesUse of Pro SeMin Hotep Tzaddik BeyNo ratings yet

- CHILD LEARNING CENTER v. TAGARIODocument1 pageCHILD LEARNING CENTER v. TAGARIOHoreb Felix VillaNo ratings yet

- Evidence BOC 2022Document108 pagesEvidence BOC 2022loschudentNo ratings yet

- Appointment Letter For Administrative AssisstantDocument4 pagesAppointment Letter For Administrative Assisstantnadia67% (3)

- JUVENILE DELINQUENCY AND JUVENILE JUSTICE SYSTEM ReviewerDocument30 pagesJUVENILE DELINQUENCY AND JUVENILE JUSTICE SYSTEM ReviewerDarlen Paule Penaso Borja100% (2)

- Harper & Row, Publishers, Inc. v. Nation EnterprisesDocument39 pagesHarper & Row, Publishers, Inc. v. Nation Enterprisessamantha.makayan.abNo ratings yet

- IG1 Element 1Document22 pagesIG1 Element 1ali rezaNo ratings yet

- Abcd QD 2Document52 pagesAbcd QD 2Cristine AvancenaNo ratings yet

- Gago V MamuyacDocument1 pageGago V MamuyacPretz VinluanNo ratings yet

Download as pdf or txt

You might also like

- Advanced Accounting: Partnership LiquidationDocument33 pagesAdvanced Accounting: Partnership LiquidationVeesNo ratings yet

- Robi Axiata Limited: Report and Financial Statements As at and For The Year Ended 31 December 2019Document97 pagesRobi Axiata Limited: Report and Financial Statements As at and For The Year Ended 31 December 2019Anika hossainNo ratings yet

- Consolidated Financial StatementsDocument136 pagesConsolidated Financial Statementsganesh PALNo ratings yet

- Ar-18 7Document5 pagesAr-18 7jawad anwarNo ratings yet

- Kapco FinancialsDocument63 pagesKapco FinancialsGhulam MustafaNo ratings yet

- Financial Statements 201819 PDFDocument133 pagesFinancial Statements 201819 PDFRobinsNo ratings yet

- Cellnex Individual Annual Accounts and Management Report 2020 1Document234 pagesCellnex Individual Annual Accounts and Management Report 2020 1Fauzi Al nassarNo ratings yet

- Standalone FinancialDocument72 pagesStandalone FinancialRadhika AgrawalNo ratings yet

- Financial StatementsDocument181 pagesFinancial StatementsDivitya ChaudharyNo ratings yet

- Relience 2021 2022 ConsolidatedDocument107 pagesRelience 2021 2022 ConsolidatedpritamNo ratings yet

- Dabur Standalone FinancialsDocument83 pagesDabur Standalone Financialsankittomarrajput95No ratings yet

- Standalone Financial StatementsDocument68 pagesStandalone Financial StatementsMaaz ShamsherNo ratings yet

- Grameenphone Accounts 2020Document62 pagesGrameenphone Accounts 2020JUNAYED AHMED RAFINNo ratings yet

- Financial StatementsDocument198 pagesFinancial StatementsRK15 21100% (1)

- E MFC Afs 2019Document84 pagesE MFC Afs 2019Cassandra Ivana BermudezNo ratings yet

- Consolidated FinancialstmtDocument130 pagesConsolidated Financialstmtsahadhiraj1No ratings yet

- Reliance General Insurance Company Limited 2020-21Document70 pagesReliance General Insurance Company Limited 2020-21yaminp292No ratings yet

- Dabur ConsolidatedDocument92 pagesDabur ConsolidatedRatla Bhukya Rama KrishnaNo ratings yet

- Financial Statements For The Year 2019Document174 pagesFinancial Statements For The Year 2019MD. ISRAFIL PALASHNo ratings yet

- LG Chem, LTD.: Separate Financial Statements and Internal Control Over Financial Reporting December 31, 2019 and 2018Document97 pagesLG Chem, LTD.: Separate Financial Statements and Internal Control Over Financial Reporting December 31, 2019 and 2018Ayushika SinghNo ratings yet

- Independent Auditor's Report: Corporate Board and Management Reports Financial StatementsDocument81 pagesIndependent Auditor's Report: Corporate Board and Management Reports Financial Statements198 Murzello MignonneNo ratings yet

- E - MFC English Q423 FSDocument123 pagesE - MFC English Q423 FSEvan LoirtNo ratings yet

- Sleep Country Canada Holding IncDocument44 pagesSleep Country Canada Holding IncSunira PaudelNo ratings yet

- BWCL - 2020 Bestway Cement Limited - OpenDoors - PKDocument142 pagesBWCL - 2020 Bestway Cement Limited - OpenDoors - PKzainNo ratings yet

- TataSteel-IR23_Standalone-FinancialsDocument120 pagesTataSteel-IR23_Standalone-FinancialsJose HernandesNo ratings yet

- Audit BoschDocument55 pagesAudit BoschRohan SakhareNo ratings yet

- Ian - Chapter 3 #11 ValuationDocument11 pagesIan - Chapter 3 #11 ValuationBae Xu KaiNo ratings yet

- Format of New Audit ReportDocument4 pagesFormat of New Audit ReportSarowar AlamNo ratings yet

- LG Chem 2020 Contingent Financial StatementsDocument102 pagesLG Chem 2020 Contingent Financial StatementsAyushika SinghNo ratings yet

- Optiva Inc. Q4 2021 Financial Statements FinalDocument63 pagesOptiva Inc. Q4 2021 Financial Statements FinaldivyaNo ratings yet

- 1197astra AR 19-20 Final Organized PDFDocument8 pages1197astra AR 19-20 Final Organized PDFelenaNo ratings yet

- Standalone Financials 21Document101 pagesStandalone Financials 21rupikagupta1903No ratings yet

- TP Central Odisha Distribution Limited FY22 23Document62 pagesTP Central Odisha Distribution Limited FY22 23Soumya Ranjan PattnaikNo ratings yet

- RRHIS A1.1.0 CFS1219 Robinsons Retail Holdings IncDocument98 pagesRRHIS A1.1.0 CFS1219 Robinsons Retail Holdings Incherrera.angelaNo ratings yet

- SESI 10 ch17 - External Auditing Function - LectureDocument109 pagesSESI 10 ch17 - External Auditing Function - LecturekimkimberlyNo ratings yet

- ConsolidatedDocument76 pagesConsolidatedarunkumar.vxlNo ratings yet

- Hero Financial STMTDocument141 pagesHero Financial STMTLaksh SinghalNo ratings yet

- CAM-Accounting For Income Taxes - Nike 2020 10KDocument1 pageCAM-Accounting For Income Taxes - Nike 2020 10KnofeNo ratings yet

- SFG Consolidated FY2022.4Q FinalDocument291 pagesSFG Consolidated FY2022.4Q FinalSi Joon RyuNo ratings yet

- HBL Annual Report 2023Document4 pagesHBL Annual Report 2023azeem sandhuNo ratings yet

- SBI Life IAR 203 404 Download CenterDocument202 pagesSBI Life IAR 203 404 Download Centershashikumarb2277No ratings yet

- February 12, 2021: Consolidated Financial Statements and NotesDocument77 pagesFebruary 12, 2021: Consolidated Financial Statements and NotesAnujaNo ratings yet

- Dongyue Report 2023 + UpdateDocument85 pagesDongyue Report 2023 + UpdateRobert ManjoNo ratings yet

- AF304 Major Assignment DraftDocument25 pagesAF304 Major Assignment DraftShilpa KumarNo ratings yet

- Latest Sample Auditors ReportDocument5 pagesLatest Sample Auditors ReportABDUL REHMAN WARRIACHNo ratings yet

- Independent Auditors' Report: Basis For OpinionDocument10 pagesIndependent Auditors' Report: Basis For OpiniondeepakNo ratings yet

- Audited ReportDocument36 pagesAudited ReportverdeepNo ratings yet

- CAM-Acquisition of Business and Uncertain Tax Positions - IBM 2019 10KDocument2 pagesCAM-Acquisition of Business and Uncertain Tax Positions - IBM 2019 10KnofeNo ratings yet

- JG Summit Annual - FS 2019 PDFDocument210 pagesJG Summit Annual - FS 2019 PDFZo ThelfNo ratings yet

- China Ocean Group Development Limited (March 24) Draft ReportDocument65 pagesChina Ocean Group Development Limited (March 24) Draft ReportRobert ManjoNo ratings yet

- Unilever Financial StatementDocument77 pagesUnilever Financial StatementIrene CapilitanNo ratings yet

- Hero Financial STMTDocument149 pagesHero Financial STMTLaksh SinghalNo ratings yet

- Standalone Financials 2021 22Document82 pagesStandalone Financials 2021 22Adesh MarwariNo ratings yet

- Icai Final SyllabusDocument18 pagesIcai Final SyllabusJD Shah FamilyNo ratings yet

- Template of Auditors Report For Life Insurance Company in BangladeshDocument11 pagesTemplate of Auditors Report For Life Insurance Company in BangladeshMohammad IslamNo ratings yet

- 2022 02 28 Gestamp Automocion 2021 Consolidated Financial StatementsDocument333 pages2022 02 28 Gestamp Automocion 2021 Consolidated Financial StatementsRicardo SequeiraNo ratings yet

- Ashourn Industries Audit Opinion 2023Document2 pagesAshourn Industries Audit Opinion 2023millydengu18No ratings yet

- 2022년 영문연결감사보고서Document92 pages2022년 영문연결감사보고서Thu HồngNo ratings yet

- 2019 Audit Report (Separate)Document86 pages2019 Audit Report (Separate)tasnimaNo ratings yet

- HayleysDocument7 pagesHayleysSANDALI FERNANDONo ratings yet

- Audit Risk Alert: General Accounting and Auditing Developments, 2017/18From EverandAudit Risk Alert: General Accounting and Auditing Developments, 2017/18No ratings yet

- HCR 3031Document3 pagesHCR 3031Rob PortNo ratings yet

- Las Normas NIIF Ilustradas Parte BDocument6 pagesLas Normas NIIF Ilustradas Parte BRampante2014No ratings yet

- EDITED ALICE Motion Correction To Amend Final OrderDocument3 pagesEDITED ALICE Motion Correction To Amend Final OrderJenifer PaglinawanNo ratings yet

- 482 Quashing Shibani Parti & AnotherDocument14 pages482 Quashing Shibani Parti & AnotherOjaswa PathakNo ratings yet

- 15 U.S. Code 1692e - False or Misleading Representations - U.S. Code - US Law - LII - Legal Information InstituteDocument4 pages15 U.S. Code 1692e - False or Misleading Representations - U.S. Code - US Law - LII - Legal Information InstituteJunius EdwardNo ratings yet

- Questions Asked in RRB NTPC 30 Dec 2020 All ShiftDocument4 pagesQuestions Asked in RRB NTPC 30 Dec 2020 All ShiftVipul BhardwajNo ratings yet

- Frcra (Q5ffi9rr6q, IH: TF, (, (IlrcqDocument3 pagesFrcra (Q5ffi9rr6q, IH: TF, (, (IlrcqSam SamNo ratings yet

- Edited - Jadwal Pengawas PTS Gasal 2324Document1 pageEdited - Jadwal Pengawas PTS Gasal 2324Irawan Joko HariyonoNo ratings yet

- Role & Responsibilities of ICC Under POSH - Program BrochureDocument3 pagesRole & Responsibilities of ICC Under POSH - Program BrochureKARNA JayNo ratings yet

- May 21 Thornburg Incident ReportDocument2 pagesMay 21 Thornburg Incident ReportJ RohrlichNo ratings yet

- CFN 9334 Law Question PaperDocument2 pagesCFN 9334 Law Question PaperSurya SinghNo ratings yet

- Ftra 2 RenewalDocument3 pagesFtra 2 RenewalNimiloteNo ratings yet

- Kaplan Order in Carroll Defamation CaseDocument2 pagesKaplan Order in Carroll Defamation CaseLaw&Crime100% (2)

- Marcos BurialDocument9 pagesMarcos BurialVic DizonNo ratings yet

- Taxn Quiz Number 1Document16 pagesTaxn Quiz Number 1justine cabanaNo ratings yet

- Duty of CareDocument79 pagesDuty of CareMuhamad HanafiNo ratings yet

- Latin MaximDocument10 pagesLatin MaximPeng ManiegoNo ratings yet

- Test Bank For Human Heredity Principles and Issues 11th EditionDocument36 pagesTest Bank For Human Heredity Principles and Issues 11th Editionoutborn.piste5ols3q100% (50)

- Different Kinds of Obligation (Midterms)Document17 pagesDifferent Kinds of Obligation (Midterms)Jay GalleroNo ratings yet

- Cis Naviera Meljacan SLDocument3 pagesCis Naviera Meljacan SLİbrahim KocakNo ratings yet

- Use of Pro SeDocument6 pagesUse of Pro SeMin Hotep Tzaddik BeyNo ratings yet

- CHILD LEARNING CENTER v. TAGARIODocument1 pageCHILD LEARNING CENTER v. TAGARIOHoreb Felix VillaNo ratings yet

- Evidence BOC 2022Document108 pagesEvidence BOC 2022loschudentNo ratings yet

- Appointment Letter For Administrative AssisstantDocument4 pagesAppointment Letter For Administrative Assisstantnadia67% (3)

- JUVENILE DELINQUENCY AND JUVENILE JUSTICE SYSTEM ReviewerDocument30 pagesJUVENILE DELINQUENCY AND JUVENILE JUSTICE SYSTEM ReviewerDarlen Paule Penaso Borja100% (2)

- Harper & Row, Publishers, Inc. v. Nation EnterprisesDocument39 pagesHarper & Row, Publishers, Inc. v. Nation Enterprisessamantha.makayan.abNo ratings yet

- IG1 Element 1Document22 pagesIG1 Element 1ali rezaNo ratings yet

- Abcd QD 2Document52 pagesAbcd QD 2Cristine AvancenaNo ratings yet

- Gago V MamuyacDocument1 pageGago V MamuyacPretz VinluanNo ratings yet