Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5835)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (853)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (350)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (824)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (405)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Tpdd Sl Trfs Gb Msip v13 Fab Lxwp Purely Purple (Add Fighter완료 12.28) (8221) 342 0005)Document14 pagesTpdd Sl Trfs Gb Msip v13 Fab Lxwp Purely Purple (Add Fighter완료 12.28) (8221) 342 0005)pista0629No ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Seven & I Management Report (For Viewing)Document74 pagesSeven & I Management Report (For Viewing)prabathnilanNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- VP2100 ConfigurationDocument2 pagesVP2100 ConfigurationLuz Stella Calixto GomezNo ratings yet

- Viscopro 2100 Brochure A4 LRDocument4 pagesViscopro 2100 Brochure A4 LRLuz Stella Calixto GomezNo ratings yet

- Orange Research Catalog SmallDocument32 pagesOrange Research Catalog SmallLuz Stella Calixto GomezNo ratings yet

- Viscopro 2000: Monitoring and Control For Single-Line Process EnvironmentsDocument4 pagesViscopro 2000: Monitoring and Control For Single-Line Process EnvironmentsLuz Stella Calixto GomezNo ratings yet

- Dial Case Styles: CL of Ga. Falls Below CL of PortDocument2 pagesDial Case Styles: CL of Ga. Falls Below CL of PortLuz Stella Calixto GomezNo ratings yet

- GN128 Explosion Proof Piston - 0Document2 pagesGN128 Explosion Proof Piston - 0Luz Stella Calixto GomezNo ratings yet

- Optibar DP 7060 Optibar DP 7060 Optibar DP 7060 Optibar DP 7060Document52 pagesOptibar DP 7060 Optibar DP 7060 Optibar DP 7060 Optibar DP 7060Luz Stella Calixto GomezNo ratings yet

- CIU Plus & CIU Prime PDFDocument8 pagesCIU Plus & CIU Prime PDFLuz Stella Calixto GomezNo ratings yet

- Visco Pro 2000Document63 pagesVisco Pro 2000Luz Stella Calixto GomezNo ratings yet

- Datasheet MeshGuard DS 1017 09Document2 pagesDatasheet MeshGuard DS 1017 09Luz Stella Calixto GomezNo ratings yet

- !!! CA OPTIWAVE 24-80Ghz Highlights en 170523Document28 pages!!! CA OPTIWAVE 24-80Ghz Highlights en 170523Luz Stella Calixto GomezNo ratings yet

- Honeywell 2017 Outlook: December 16, 2016Document24 pagesHoneywell 2017 Outlook: December 16, 2016Luz Stella Calixto GomezNo ratings yet

- Abb CMD 2016 Fact SheetsDocument16 pagesAbb CMD 2016 Fact SheetsLuz Stella Calixto GomezNo ratings yet

- EEx-Cert RCCx2 Ex-96.D.3826 EngDocument5 pagesEEx-Cert RCCx2 Ex-96.D.3826 EngLuz Stella Calixto GomezNo ratings yet

- Abb CMD 2016 Fact SheetsDocument16 pagesAbb CMD 2016 Fact SheetsLuz Stella Calixto GomezNo ratings yet

- Regression: Variables Entered/RemovedDocument2 pagesRegression: Variables Entered/RemovedAryanNo ratings yet

- Electricity Bill PDFDocument1 pageElectricity Bill PDFSonuNo ratings yet

- IMEE Ch3. Plant LayoutDocument68 pagesIMEE Ch3. Plant LayoutDalasa OljiraNo ratings yet

- Tax Invoice SampleDocument1 pageTax Invoice SampleRahul DeyNo ratings yet

- Reachin 301 (TDS)Document1 pageReachin 301 (TDS)Christian Patrick FernandezNo ratings yet

- 002 - Orient Air Services V CADocument2 pages002 - Orient Air Services V CAChristine Joy AngatNo ratings yet

- Ficha Técnica - Structural Poly Glass Vessels - Pentair - Tanques PolyglassDocument4 pagesFicha Técnica - Structural Poly Glass Vessels - Pentair - Tanques PolyglassJuan GutierrezNo ratings yet

- نظام الجودة الشاملة كآلية لتحسين تنافسية الجامعات.Document18 pagesنظام الجودة الشاملة كآلية لتحسين تنافسية الجامعات.Ahmed AbdelradyNo ratings yet

- My Chhota School My Chhota SchoolDocument2 pagesMy Chhota School My Chhota Schoolbasha gNo ratings yet

- Processes and Technology: BITS PilaniDocument29 pagesProcesses and Technology: BITS Pilanipavan hydNo ratings yet

- Benefit Illustration: UIN: 104N116V11 Page 1 of 3Document3 pagesBenefit Illustration: UIN: 104N116V11 Page 1 of 3Abhimanyu Singh BhatiNo ratings yet

- Samastipur Distric Block Wise Plastic Collection DetailDocument149 pagesSamastipur Distric Block Wise Plastic Collection Detailnikhilkumarchaudhary12No ratings yet

- SMC Stock Transfer Service CorpDocument1 pageSMC Stock Transfer Service CorpJasmine Nouvel CruzNo ratings yet

- Circular Regarding Creche FacilityDocument1 pageCircular Regarding Creche FacilityDinesh KushwahaNo ratings yet

- Assignment 1 - Case Study Analysis: ECON1193B: Business Statistics 1Document7 pagesAssignment 1 - Case Study Analysis: ECON1193B: Business Statistics 1Phong LữNo ratings yet

- Bayana in EnglishDocument4 pagesBayana in Englishrrrahul1703No ratings yet

- Zeppini Ecoflex Catalogo EnglishDocument10 pagesZeppini Ecoflex Catalogo EnglishANGEL PRADANo ratings yet

- Economics Assignment Group 5Document6 pagesEconomics Assignment Group 5Jaymeet PatilNo ratings yet

- Chapter-1 Business StatisticsDocument11 pagesChapter-1 Business StatisticsMd. Anhar Sharif MollahNo ratings yet

- Po 202394Document1 pagePo 202394RHH. EngineeringNo ratings yet

- Oligopoly and Strategic BehaviorDocument4 pagesOligopoly and Strategic BehaviorJaninelaraNo ratings yet

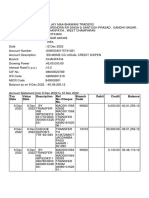

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDocument7 pagesTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceRohan SinghNo ratings yet

- The Stakeholder or The Firm (Balancing The Strategic Framework)Document8 pagesThe Stakeholder or The Firm (Balancing The Strategic Framework)AndreaLumbanAmaytaNo ratings yet

- Unit 2 pom-BNDocument45 pagesUnit 2 pom-BNsachinNo ratings yet

- Solved Suppose That Marginal Product Tripled While Product Price Fell BDocument1 pageSolved Suppose That Marginal Product Tripled While Product Price Fell BM Bilal SaleemNo ratings yet

- ΝΕΟΜΑ course 7Document25 pagesΝΕΟΜΑ course 7Leo LTNo ratings yet

- KTQTDocument3 pagesKTQTTrần Nguyễn Tuệ MinhNo ratings yet

- 3500 Series Competitive Presentation (50 HZ)Document40 pages3500 Series Competitive Presentation (50 HZ)Mohamed HamdallahNo ratings yet