Asutay Islamicmoraleconomyasthefoundationofislamicfinance Inislamicfinanceineurope Ee 2013

Asutay Islamicmoraleconomyasthefoundationofislamicfinance Inislamicfinanceineurope Ee 2013

You might also like

- Rules Governing Redeemable and Treasury SharesDocument2 pagesRules Governing Redeemable and Treasury SharesTosca Mansujeto50% (2)

- 08 - Chapter 3Document91 pages08 - Chapter 3Mansi SankhalaNo ratings yet

- Conceptualising and Locating The Social Failure of Islamic Finance: Aspirations of Islamic Moral EconomyDocument21 pagesConceptualising and Locating The Social Failure of Islamic Finance: Aspirations of Islamic Moral EconomyŞehmus AYDINNo ratings yet

- Shafiullah Jan and Mehmet Asutay - 9781788116732 Downloaded From Elgar Online at 07/13/2020 12:46:53AM Via Free AccessDocument12 pagesShafiullah Jan and Mehmet Asutay - 9781788116732 Downloaded From Elgar Online at 07/13/2020 12:46:53AM Via Free Accesscmcox22No ratings yet

- Islamic Banking and Finance Concept and Reality Jib FDocument16 pagesIslamic Banking and Finance Concept and Reality Jib FElsa SalsabilaNo ratings yet

- MPRA Paper 42046Document26 pagesMPRA Paper 42046Martini Dwi Pusparini S.H.I., M.S.I.No ratings yet

- Dr. Mehmet AsutayDocument17 pagesDr. Mehmet AsutayHasanovMirasovičNo ratings yet

- Aslam Haneef Contemporary Islamic Economics The Missing Dimension of Genuine IslamizationDocument20 pagesAslam Haneef Contemporary Islamic Economics The Missing Dimension of Genuine IslamizationmohammedzaidiNo ratings yet

- Thesis Islamic EconomicsDocument5 pagesThesis Islamic Economicsimddtsief100% (1)

- A Comparative Analysis On Capitalism and Islamic Economic SystemDocument15 pagesA Comparative Analysis On Capitalism and Islamic Economic SystemAbdul Salam NMNo ratings yet

- A Note On Islamic Economics-Abbas Mirakhor PDFDocument56 pagesA Note On Islamic Economics-Abbas Mirakhor PDFPurnama PutraNo ratings yet

- Islamic Economics: Still in Search of An Identity: Abdulkader Cassim MahomedyDocument14 pagesIslamic Economics: Still in Search of An Identity: Abdulkader Cassim MahomedySon Go HanNo ratings yet

- Role of Islamic Banks in Economic Develo PDFDocument78 pagesRole of Islamic Banks in Economic Develo PDFshittuidNo ratings yet

- Islamic Economy Option: SWOT Case Study Analysis: Suzanna El MassahDocument22 pagesIslamic Economy Option: SWOT Case Study Analysis: Suzanna El MassahAhmed AchichNo ratings yet

- Entrepreneurship, Islamic Finance and SME Financing - enDocument56 pagesEntrepreneurship, Islamic Finance and SME Financing - enSeada AliyiNo ratings yet

- SASE 2020 Research Network R-Call For Paper-Islamic Moral Economy & FinanceDocument3 pagesSASE 2020 Research Network R-Call For Paper-Islamic Moral Economy & FinanceFoyasal KhanNo ratings yet

- Community Development Financial Institutions: Lessons in Social Banking For The Islamic Financial Industry Dr. Salma SairallyDocument20 pagesCommunity Development Financial Institutions: Lessons in Social Banking For The Islamic Financial Industry Dr. Salma SairallyStarterrrsNo ratings yet

- Islamic Microfinance: Fulfilling Social and Developmental Expectations Mehmet Asutay Executive SummaryDocument6 pagesIslamic Microfinance: Fulfilling Social and Developmental Expectations Mehmet Asutay Executive Summaryتقوى زيتونيNo ratings yet

- Islamic Finance Today Is A Buzzword That No One Actually Knows What It Stands ForDocument3 pagesIslamic Finance Today Is A Buzzword That No One Actually Knows What It Stands ForSaiful Azhar RoslyNo ratings yet

- PDF Islamic Monetary Economics and Institutions Theory and Practice Muhamed Zulkhibri Ebook Full ChapterDocument53 pagesPDF Islamic Monetary Economics and Institutions Theory and Practice Muhamed Zulkhibri Ebook Full Chapterjose.colvin171100% (2)

- Saddam Assignment Islamic StudiesDocument18 pagesSaddam Assignment Islamic Studiessahilkhan45456677No ratings yet

- Article 1Document28 pagesArticle 1kainatvalani25No ratings yet

- A Paradigm of Islamic Money and Banking (Research Proposal)Document15 pagesA Paradigm of Islamic Money and Banking (Research Proposal)JediGodNo ratings yet

- B4.1 Money and Banking in An Islamic FrameworkDocument9 pagesB4.1 Money and Banking in An Islamic FrameworkZohaib OmerNo ratings yet

- Islamic Wealth Management PDFDocument10 pagesIslamic Wealth Management PDFislamicthinkerNo ratings yet

- Literature Review of Islamic Economics SystemDocument8 pagesLiterature Review of Islamic Economics Systemeqcusqwgf100% (2)

- 04asutay PDFDocument16 pages04asutay PDFM Ridwan UmarNo ratings yet

- Asutay (2007) PDFDocument16 pagesAsutay (2007) PDFanwaradem225No ratings yet

- Shariah Economics and The Progress of Islamic Finance The Role of Shariah ExpertsDocument5 pagesShariah Economics and The Progress of Islamic Finance The Role of Shariah ExpertsmohamedNo ratings yet

- Towards A More Socially Inclusive and Sustainable Framework For Islamic Banking and FinanceDocument31 pagesTowards A More Socially Inclusive and Sustainable Framework For Islamic Banking and FinanceGairuzazmi M GhaniNo ratings yet

- Islamic Banking Ideal N RealityDocument19 pagesIslamic Banking Ideal N RealityIbnu TaimiyyahNo ratings yet

- Islamic Economics and The Islamic Sub EconomyDocument18 pagesIslamic Economics and The Islamic Sub EconomyNoerma Madjid Riyadi100% (1)

- What Is Wrong With Islamic EconomicDocument6 pagesWhat Is Wrong With Islamic EconomicadsolahNo ratings yet

- Significance.104 SairDocument6 pagesSignificance.104 SairSyed sair SheraziNo ratings yet

- Contemporary Islamic Finance: An Introductory Analysis: MR - Najeebzada DR - Salim Ur RahmanDocument17 pagesContemporary Islamic Finance: An Introductory Analysis: MR - Najeebzada DR - Salim Ur RahmanInzemam Ul HaqNo ratings yet

- Islamic Business in MalaysiaDocument27 pagesIslamic Business in Malaysiabrendan lanzaNo ratings yet

- Innovation Versus Replication Some Notes On The Approaches in Defining Shariah Compliance in Islamic FinanceDocument24 pagesInnovation Versus Replication Some Notes On The Approaches in Defining Shariah Compliance in Islamic Financebayu pratama putraNo ratings yet

- The Future of Islamic Finance: A Reflection Based On Maqāćid Al-SharąăahDocument14 pagesThe Future of Islamic Finance: A Reflection Based On Maqāćid Al-SharąăahFaizan ChNo ratings yet

- Isalmic EnterprenuershipDocument6 pagesIsalmic EnterprenuershipMuhammad Umer Farooq AwanNo ratings yet

- 1997 SADEQ Development and Finance in IslamDocument7 pages1997 SADEQ Development and Finance in IslamDiaz HasvinNo ratings yet

- My Part Review FIE AssignmentDocument5 pagesMy Part Review FIE AssignmentSiti Safiah Binti BakhtiarliliNo ratings yet

- K.HosainDocument6 pagesK.HosainSaqib GondalNo ratings yet

- Name AQIB BBHM-F19-067 BBA-5ADocument5 pagesName AQIB BBHM-F19-067 BBA-5AJabbar GondalNo ratings yet

- Asutay and Yilmaz (2021) PDFDocument17 pagesAsutay and Yilmaz (2021) PDFanwaradem225No ratings yet

- Role of Shariah Experts BankingDocument7 pagesRole of Shariah Experts BankingMUHAMMED UVAIS PTNo ratings yet

- Islamic Economics and Finance Education: Consensus On ReformDocument23 pagesIslamic Economics and Finance Education: Consensus On Reformahmad syafiiNo ratings yet

- Fundamentals of An Islamic Economic System Compared To The Social Market EconomyDocument22 pagesFundamentals of An Islamic Economic System Compared To The Social Market EconomySyed MehboobNo ratings yet

- Economic Development and Islamic Finance: Vol. 22, No.1, May, 2014 DOI No. 10.12816/0004138Document4 pagesEconomic Development and Islamic Finance: Vol. 22, No.1, May, 2014 DOI No. 10.12816/0004138Agus ArwaniNo ratings yet

- 2125-Article Text-2876-1-10-20231123Document8 pages2125-Article Text-2876-1-10-20231123Cem KorkutNo ratings yet

- Sustainability 10 00637 PDFDocument11 pagesSustainability 10 00637 PDFDila Estu KinasihNo ratings yet

- School of Post Graduate Studies Nasarawa State University Keffi Faculty of Administration Department of AccountingDocument22 pagesSchool of Post Graduate Studies Nasarawa State University Keffi Faculty of Administration Department of AccountingAbdullahiNo ratings yet

- A Theory and Contractual Framework of Islamic Micro-Financial Institutions' OperationsDocument9 pagesA Theory and Contractual Framework of Islamic Micro-Financial Institutions' OperationsIbrahim KouzoNo ratings yet

- Islamic Science of EconomicsDocument53 pagesIslamic Science of Economicshwoarang2010No ratings yet

- Islamic Political Economy SystemicDocument16 pagesIslamic Political Economy SystemicWana MaliNo ratings yet

- Shariah PerspectiveDocument8 pagesShariah PerspectiveQarinaNo ratings yet

- Islamic Finance: A Review of The LiteratureDocument18 pagesIslamic Finance: A Review of The LiteratureAhmad AriefNo ratings yet

- 18 - (Iqbal, - Zamir - Mirakhor, - Abbas) - 2017 - Ethical Dimensions of Islamic FinanceDocument203 pages18 - (Iqbal, - Zamir - Mirakhor, - Abbas) - 2017 - Ethical Dimensions of Islamic FinanceMohammad RazaNo ratings yet

- Islamic Economics and Islamic Finance in The World Ibrahim - Et - Al-2017-The - World - EconomyDocument7 pagesIslamic Economics and Islamic Finance in The World Ibrahim - Et - Al-2017-The - World - Economyhendi nugrahaNo ratings yet

- The Philosophy of Islamic Economic ParadigmDocument3 pagesThe Philosophy of Islamic Economic ParadigmFakhri MubarokNo ratings yet

- A Genealogy of The Islamic Development Discourse: Underlying Assumptions and Policy Implications From A Development Studies PerspectiveDocument34 pagesA Genealogy of The Islamic Development Discourse: Underlying Assumptions and Policy Implications From A Development Studies PerspectiveLuis J. González OquendoNo ratings yet

- Money with Morals: The Necessity of Islamic Finance in Today's WorldFrom EverandMoney with Morals: The Necessity of Islamic Finance in Today's WorldNo ratings yet

- Pertemuan 2 - Financial Reporting MechanicDocument32 pagesPertemuan 2 - Financial Reporting MechanicJhoni LimNo ratings yet

- Part 2 - Chapter 27 The Basic Tools of FinanceDocument14 pagesPart 2 - Chapter 27 The Basic Tools of FinanceCon CừuNo ratings yet

- Manvendra Singh - Bajaj FinanceDocument3 pagesManvendra Singh - Bajaj FinanceManvendra SinghNo ratings yet

- JCOT InstrumentsDocument107 pagesJCOT InstrumentsvaymigadeNo ratings yet

- Compare and Contrast Proclamation No 451Document1 pageCompare and Contrast Proclamation No 451liya100% (3)

- IIPM, BengaluruDocument4 pagesIIPM, BengaluruPrakash KcNo ratings yet

- Apptuto CFA L1 LOS Changes 2016Document18 pagesApptuto CFA L1 LOS Changes 2016NattKoonNo ratings yet

- Education Loan FAQs - Manav Rachna International UniversityDocument5 pagesEducation Loan FAQs - Manav Rachna International UniversityKumarPintuNo ratings yet

- Ias 19 Employee BenefitsDocument43 pagesIas 19 Employee BenefitsHasan Ali BokhariNo ratings yet

- Funds Transfer Pricing: Cracking The Code On Deposit ValuationDocument4 pagesFunds Transfer Pricing: Cracking The Code On Deposit ValuationHoàng Trần HữuNo ratings yet

- Auditing Standards ListDocument2 pagesAuditing Standards ListSree SAINo ratings yet

- CF Quiz AprilDocument5 pagesCF Quiz Aprilsumeet9surana9744100% (1)

- Memorial For RespondentDocument28 pagesMemorial For Respondentdevil_3565100% (1)

- Nepal Accounting Standard 2: InventoriesDocument10 pagesNepal Accounting Standard 2: InventoriesHem JosheeNo ratings yet

- Pre-Foreclosure Complaint Plaintiff)Document49 pagesPre-Foreclosure Complaint Plaintiff)tmccand75% (4)

- Seagull OptionDocument3 pagesSeagull OptionabrNo ratings yet

- Practical Accounting 1Document4 pagesPractical Accounting 1Gelo Caranyagan100% (1)

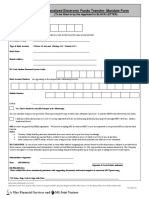

- NEFT MandateDocument1 pageNEFT MandateGirishNo ratings yet

- Chester Levings RobosignerDocument1 pageChester Levings RobosignerBradley WalkerNo ratings yet

- Pag Ibig Housing LoanDocument5 pagesPag Ibig Housing LoanHeber BacolodNo ratings yet

- Crypto Currency and Block ChainDocument38 pagesCrypto Currency and Block ChainShabeel ShabuNo ratings yet

- Credit 5Document7 pagesCredit 5Maria SyNo ratings yet

- Project Report ON Electrical&Electronics Repairing (Service Sector Unit) Under P.M.E.G.PDocument6 pagesProject Report ON Electrical&Electronics Repairing (Service Sector Unit) Under P.M.E.G.PGlobal Law FirmNo ratings yet

- Candlestick Cheat Sheet RGB FINAL PDFDocument16 pagesCandlestick Cheat Sheet RGB FINAL PDFNutzu ConstantinNo ratings yet

- Checklist For DividendDocument2 pagesChecklist For DividendKhalid MahmoodNo ratings yet

- Interest Rates and Interest Charges: FR833282333 - MEIJER CREDIT CARDDocument6 pagesInterest Rates and Interest Charges: FR833282333 - MEIJER CREDIT CARDAmeer Ullah KhanNo ratings yet

- Strategic Cost Management Midterm Examination SY 2021-2022 FIRST SEMESTERDocument4 pagesStrategic Cost Management Midterm Examination SY 2021-2022 FIRST SEMESTERMixx MineNo ratings yet

- Ajanta Annual Report FY22Document208 pagesAjanta Annual Report FY22MAHI LADNo ratings yet

Download as pdf or txt

You might also like

- Rules Governing Redeemable and Treasury SharesDocument2 pagesRules Governing Redeemable and Treasury SharesTosca Mansujeto50% (2)

- 08 - Chapter 3Document91 pages08 - Chapter 3Mansi SankhalaNo ratings yet

- Conceptualising and Locating The Social Failure of Islamic Finance: Aspirations of Islamic Moral EconomyDocument21 pagesConceptualising and Locating The Social Failure of Islamic Finance: Aspirations of Islamic Moral EconomyŞehmus AYDINNo ratings yet

- Shafiullah Jan and Mehmet Asutay - 9781788116732 Downloaded From Elgar Online at 07/13/2020 12:46:53AM Via Free AccessDocument12 pagesShafiullah Jan and Mehmet Asutay - 9781788116732 Downloaded From Elgar Online at 07/13/2020 12:46:53AM Via Free Accesscmcox22No ratings yet

- Islamic Banking and Finance Concept and Reality Jib FDocument16 pagesIslamic Banking and Finance Concept and Reality Jib FElsa SalsabilaNo ratings yet

- MPRA Paper 42046Document26 pagesMPRA Paper 42046Martini Dwi Pusparini S.H.I., M.S.I.No ratings yet

- Dr. Mehmet AsutayDocument17 pagesDr. Mehmet AsutayHasanovMirasovičNo ratings yet

- Aslam Haneef Contemporary Islamic Economics The Missing Dimension of Genuine IslamizationDocument20 pagesAslam Haneef Contemporary Islamic Economics The Missing Dimension of Genuine IslamizationmohammedzaidiNo ratings yet

- Thesis Islamic EconomicsDocument5 pagesThesis Islamic Economicsimddtsief100% (1)

- A Comparative Analysis On Capitalism and Islamic Economic SystemDocument15 pagesA Comparative Analysis On Capitalism and Islamic Economic SystemAbdul Salam NMNo ratings yet

- A Note On Islamic Economics-Abbas Mirakhor PDFDocument56 pagesA Note On Islamic Economics-Abbas Mirakhor PDFPurnama PutraNo ratings yet

- Islamic Economics: Still in Search of An Identity: Abdulkader Cassim MahomedyDocument14 pagesIslamic Economics: Still in Search of An Identity: Abdulkader Cassim MahomedySon Go HanNo ratings yet

- Role of Islamic Banks in Economic Develo PDFDocument78 pagesRole of Islamic Banks in Economic Develo PDFshittuidNo ratings yet

- Islamic Economy Option: SWOT Case Study Analysis: Suzanna El MassahDocument22 pagesIslamic Economy Option: SWOT Case Study Analysis: Suzanna El MassahAhmed AchichNo ratings yet

- Entrepreneurship, Islamic Finance and SME Financing - enDocument56 pagesEntrepreneurship, Islamic Finance and SME Financing - enSeada AliyiNo ratings yet

- SASE 2020 Research Network R-Call For Paper-Islamic Moral Economy & FinanceDocument3 pagesSASE 2020 Research Network R-Call For Paper-Islamic Moral Economy & FinanceFoyasal KhanNo ratings yet

- Community Development Financial Institutions: Lessons in Social Banking For The Islamic Financial Industry Dr. Salma SairallyDocument20 pagesCommunity Development Financial Institutions: Lessons in Social Banking For The Islamic Financial Industry Dr. Salma SairallyStarterrrsNo ratings yet

- Islamic Microfinance: Fulfilling Social and Developmental Expectations Mehmet Asutay Executive SummaryDocument6 pagesIslamic Microfinance: Fulfilling Social and Developmental Expectations Mehmet Asutay Executive Summaryتقوى زيتونيNo ratings yet

- Islamic Finance Today Is A Buzzword That No One Actually Knows What It Stands ForDocument3 pagesIslamic Finance Today Is A Buzzword That No One Actually Knows What It Stands ForSaiful Azhar RoslyNo ratings yet

- PDF Islamic Monetary Economics and Institutions Theory and Practice Muhamed Zulkhibri Ebook Full ChapterDocument53 pagesPDF Islamic Monetary Economics and Institutions Theory and Practice Muhamed Zulkhibri Ebook Full Chapterjose.colvin171100% (2)

- Saddam Assignment Islamic StudiesDocument18 pagesSaddam Assignment Islamic Studiessahilkhan45456677No ratings yet

- Article 1Document28 pagesArticle 1kainatvalani25No ratings yet

- A Paradigm of Islamic Money and Banking (Research Proposal)Document15 pagesA Paradigm of Islamic Money and Banking (Research Proposal)JediGodNo ratings yet

- B4.1 Money and Banking in An Islamic FrameworkDocument9 pagesB4.1 Money and Banking in An Islamic FrameworkZohaib OmerNo ratings yet

- Islamic Wealth Management PDFDocument10 pagesIslamic Wealth Management PDFislamicthinkerNo ratings yet

- Literature Review of Islamic Economics SystemDocument8 pagesLiterature Review of Islamic Economics Systemeqcusqwgf100% (2)

- 04asutay PDFDocument16 pages04asutay PDFM Ridwan UmarNo ratings yet

- Asutay (2007) PDFDocument16 pagesAsutay (2007) PDFanwaradem225No ratings yet

- Shariah Economics and The Progress of Islamic Finance The Role of Shariah ExpertsDocument5 pagesShariah Economics and The Progress of Islamic Finance The Role of Shariah ExpertsmohamedNo ratings yet

- Towards A More Socially Inclusive and Sustainable Framework For Islamic Banking and FinanceDocument31 pagesTowards A More Socially Inclusive and Sustainable Framework For Islamic Banking and FinanceGairuzazmi M GhaniNo ratings yet

- Islamic Banking Ideal N RealityDocument19 pagesIslamic Banking Ideal N RealityIbnu TaimiyyahNo ratings yet

- Islamic Economics and The Islamic Sub EconomyDocument18 pagesIslamic Economics and The Islamic Sub EconomyNoerma Madjid Riyadi100% (1)

- What Is Wrong With Islamic EconomicDocument6 pagesWhat Is Wrong With Islamic EconomicadsolahNo ratings yet

- Significance.104 SairDocument6 pagesSignificance.104 SairSyed sair SheraziNo ratings yet

- Contemporary Islamic Finance: An Introductory Analysis: MR - Najeebzada DR - Salim Ur RahmanDocument17 pagesContemporary Islamic Finance: An Introductory Analysis: MR - Najeebzada DR - Salim Ur RahmanInzemam Ul HaqNo ratings yet

- Islamic Business in MalaysiaDocument27 pagesIslamic Business in Malaysiabrendan lanzaNo ratings yet

- Innovation Versus Replication Some Notes On The Approaches in Defining Shariah Compliance in Islamic FinanceDocument24 pagesInnovation Versus Replication Some Notes On The Approaches in Defining Shariah Compliance in Islamic Financebayu pratama putraNo ratings yet

- The Future of Islamic Finance: A Reflection Based On Maqāćid Al-SharąăahDocument14 pagesThe Future of Islamic Finance: A Reflection Based On Maqāćid Al-SharąăahFaizan ChNo ratings yet

- Isalmic EnterprenuershipDocument6 pagesIsalmic EnterprenuershipMuhammad Umer Farooq AwanNo ratings yet

- 1997 SADEQ Development and Finance in IslamDocument7 pages1997 SADEQ Development and Finance in IslamDiaz HasvinNo ratings yet

- My Part Review FIE AssignmentDocument5 pagesMy Part Review FIE AssignmentSiti Safiah Binti BakhtiarliliNo ratings yet

- K.HosainDocument6 pagesK.HosainSaqib GondalNo ratings yet

- Name AQIB BBHM-F19-067 BBA-5ADocument5 pagesName AQIB BBHM-F19-067 BBA-5AJabbar GondalNo ratings yet

- Asutay and Yilmaz (2021) PDFDocument17 pagesAsutay and Yilmaz (2021) PDFanwaradem225No ratings yet

- Role of Shariah Experts BankingDocument7 pagesRole of Shariah Experts BankingMUHAMMED UVAIS PTNo ratings yet

- Islamic Economics and Finance Education: Consensus On ReformDocument23 pagesIslamic Economics and Finance Education: Consensus On Reformahmad syafiiNo ratings yet

- Fundamentals of An Islamic Economic System Compared To The Social Market EconomyDocument22 pagesFundamentals of An Islamic Economic System Compared To The Social Market EconomySyed MehboobNo ratings yet

- Economic Development and Islamic Finance: Vol. 22, No.1, May, 2014 DOI No. 10.12816/0004138Document4 pagesEconomic Development and Islamic Finance: Vol. 22, No.1, May, 2014 DOI No. 10.12816/0004138Agus ArwaniNo ratings yet

- 2125-Article Text-2876-1-10-20231123Document8 pages2125-Article Text-2876-1-10-20231123Cem KorkutNo ratings yet

- Sustainability 10 00637 PDFDocument11 pagesSustainability 10 00637 PDFDila Estu KinasihNo ratings yet

- School of Post Graduate Studies Nasarawa State University Keffi Faculty of Administration Department of AccountingDocument22 pagesSchool of Post Graduate Studies Nasarawa State University Keffi Faculty of Administration Department of AccountingAbdullahiNo ratings yet

- A Theory and Contractual Framework of Islamic Micro-Financial Institutions' OperationsDocument9 pagesA Theory and Contractual Framework of Islamic Micro-Financial Institutions' OperationsIbrahim KouzoNo ratings yet

- Islamic Science of EconomicsDocument53 pagesIslamic Science of Economicshwoarang2010No ratings yet

- Islamic Political Economy SystemicDocument16 pagesIslamic Political Economy SystemicWana MaliNo ratings yet

- Shariah PerspectiveDocument8 pagesShariah PerspectiveQarinaNo ratings yet

- Islamic Finance: A Review of The LiteratureDocument18 pagesIslamic Finance: A Review of The LiteratureAhmad AriefNo ratings yet

- 18 - (Iqbal, - Zamir - Mirakhor, - Abbas) - 2017 - Ethical Dimensions of Islamic FinanceDocument203 pages18 - (Iqbal, - Zamir - Mirakhor, - Abbas) - 2017 - Ethical Dimensions of Islamic FinanceMohammad RazaNo ratings yet

- Islamic Economics and Islamic Finance in The World Ibrahim - Et - Al-2017-The - World - EconomyDocument7 pagesIslamic Economics and Islamic Finance in The World Ibrahim - Et - Al-2017-The - World - Economyhendi nugrahaNo ratings yet

- The Philosophy of Islamic Economic ParadigmDocument3 pagesThe Philosophy of Islamic Economic ParadigmFakhri MubarokNo ratings yet

- A Genealogy of The Islamic Development Discourse: Underlying Assumptions and Policy Implications From A Development Studies PerspectiveDocument34 pagesA Genealogy of The Islamic Development Discourse: Underlying Assumptions and Policy Implications From A Development Studies PerspectiveLuis J. González OquendoNo ratings yet

- Money with Morals: The Necessity of Islamic Finance in Today's WorldFrom EverandMoney with Morals: The Necessity of Islamic Finance in Today's WorldNo ratings yet

- Pertemuan 2 - Financial Reporting MechanicDocument32 pagesPertemuan 2 - Financial Reporting MechanicJhoni LimNo ratings yet

- Part 2 - Chapter 27 The Basic Tools of FinanceDocument14 pagesPart 2 - Chapter 27 The Basic Tools of FinanceCon CừuNo ratings yet

- Manvendra Singh - Bajaj FinanceDocument3 pagesManvendra Singh - Bajaj FinanceManvendra SinghNo ratings yet

- JCOT InstrumentsDocument107 pagesJCOT InstrumentsvaymigadeNo ratings yet

- Compare and Contrast Proclamation No 451Document1 pageCompare and Contrast Proclamation No 451liya100% (3)

- IIPM, BengaluruDocument4 pagesIIPM, BengaluruPrakash KcNo ratings yet

- Apptuto CFA L1 LOS Changes 2016Document18 pagesApptuto CFA L1 LOS Changes 2016NattKoonNo ratings yet

- Education Loan FAQs - Manav Rachna International UniversityDocument5 pagesEducation Loan FAQs - Manav Rachna International UniversityKumarPintuNo ratings yet

- Ias 19 Employee BenefitsDocument43 pagesIas 19 Employee BenefitsHasan Ali BokhariNo ratings yet

- Funds Transfer Pricing: Cracking The Code On Deposit ValuationDocument4 pagesFunds Transfer Pricing: Cracking The Code On Deposit ValuationHoàng Trần HữuNo ratings yet

- Auditing Standards ListDocument2 pagesAuditing Standards ListSree SAINo ratings yet

- CF Quiz AprilDocument5 pagesCF Quiz Aprilsumeet9surana9744100% (1)

- Memorial For RespondentDocument28 pagesMemorial For Respondentdevil_3565100% (1)

- Nepal Accounting Standard 2: InventoriesDocument10 pagesNepal Accounting Standard 2: InventoriesHem JosheeNo ratings yet

- Pre-Foreclosure Complaint Plaintiff)Document49 pagesPre-Foreclosure Complaint Plaintiff)tmccand75% (4)

- Seagull OptionDocument3 pagesSeagull OptionabrNo ratings yet

- Practical Accounting 1Document4 pagesPractical Accounting 1Gelo Caranyagan100% (1)

- NEFT MandateDocument1 pageNEFT MandateGirishNo ratings yet

- Chester Levings RobosignerDocument1 pageChester Levings RobosignerBradley WalkerNo ratings yet

- Pag Ibig Housing LoanDocument5 pagesPag Ibig Housing LoanHeber BacolodNo ratings yet

- Crypto Currency and Block ChainDocument38 pagesCrypto Currency and Block ChainShabeel ShabuNo ratings yet

- Credit 5Document7 pagesCredit 5Maria SyNo ratings yet

- Project Report ON Electrical&Electronics Repairing (Service Sector Unit) Under P.M.E.G.PDocument6 pagesProject Report ON Electrical&Electronics Repairing (Service Sector Unit) Under P.M.E.G.PGlobal Law FirmNo ratings yet

- Candlestick Cheat Sheet RGB FINAL PDFDocument16 pagesCandlestick Cheat Sheet RGB FINAL PDFNutzu ConstantinNo ratings yet

- Checklist For DividendDocument2 pagesChecklist For DividendKhalid MahmoodNo ratings yet

- Interest Rates and Interest Charges: FR833282333 - MEIJER CREDIT CARDDocument6 pagesInterest Rates and Interest Charges: FR833282333 - MEIJER CREDIT CARDAmeer Ullah KhanNo ratings yet

- Strategic Cost Management Midterm Examination SY 2021-2022 FIRST SEMESTERDocument4 pagesStrategic Cost Management Midterm Examination SY 2021-2022 FIRST SEMESTERMixx MineNo ratings yet

- Ajanta Annual Report FY22Document208 pagesAjanta Annual Report FY22MAHI LADNo ratings yet