I. Introduction To Accounting For Grants and Contracts: A. Overview

I. Introduction To Accounting For Grants and Contracts: A. Overview

You might also like

- Ppa LetterDocument1 pagePpa LetterDestiny TobiNo ratings yet

- Let Export Copy: Indian Customs Edi SystemDocument10 pagesLet Export Copy: Indian Customs Edi Systemsaikatpaul22No ratings yet

- VCE Summer Internship Program 2021: Ruchira Parwanda 3 Financial Modelling (Infra)Document4 pagesVCE Summer Internship Program 2021: Ruchira Parwanda 3 Financial Modelling (Infra)Ruchira ParwandaNo ratings yet

- Department of Agriculture Republic of The Philippines: Da-Cso Application FormDocument7 pagesDepartment of Agriculture Republic of The Philippines: Da-Cso Application FormVerna BeNo ratings yet

- Introduction To Project Finance - A Guide For Contractors and EngineersDocument9 pagesIntroduction To Project Finance - A Guide For Contractors and Engineershazemdiab100% (1)

- Creditcardrush JSONDocument31 pagesCreditcardrush JSONmacroniess khanNo ratings yet

- 13-SOP For Safe Operation Limestone CrusherDocument2 pages13-SOP For Safe Operation Limestone Crushergothic centuary60% (5)

- Aef 2013 Audit Acc ReqDocument9 pagesAef 2013 Audit Acc Reqvikas_ojha54706No ratings yet

- ToR 516Document4 pagesToR 516Rumki SarkarNo ratings yet

- RFP DocumentsDocument10 pagesRFP DocumentsYasir FahadNo ratings yet

- Smart Task 3Document5 pagesSmart Task 3Utkarsh ChaturvediNo ratings yet

- Funding Programme - Long-Term ProjectDocument3 pagesFunding Programme - Long-Term ProjectmarkzwikNo ratings yet

- Master Agreement For Services 4Document11 pagesMaster Agreement For Services 4Tamer SayedNo ratings yet

- Capital Project FundDocument7 pagesCapital Project FundmeseleNo ratings yet

- III. Compensation and Effort Reporting For Grants & ContractsDocument7 pagesIII. Compensation and Effort Reporting For Grants & ContractsMATIULLAHNo ratings yet

- Chapter Four-Part Ii: Accounting For Governmental FundsDocument30 pagesChapter Four-Part Ii: Accounting For Governmental FundsabateNo ratings yet

- 24C00087 - Bid Documents - FMP Sitio Brown Phase IDocument58 pages24C00087 - Bid Documents - FMP Sitio Brown Phase ISamNo ratings yet

- Process of Project Financing: Feasibility StudyDocument23 pagesProcess of Project Financing: Feasibility StudyRohit PadalkarNo ratings yet

- PFDocument16 pagesPFadabotor7No ratings yet

- Chapter Four CPFDocument28 pagesChapter Four CPFtame kibruNo ratings yet

- BID DOCS LEDBillboardDocument30 pagesBID DOCS LEDBillboardNanz11 SerranoNo ratings yet

- PCOA Module 6 - PAS 23 and 24Document8 pagesPCOA Module 6 - PAS 23 and 24Jan JanNo ratings yet

- Report On Funds RaisingDocument28 pagesReport On Funds RaisingNikita MajiNo ratings yet

- Module 2: Financing of ProjectsDocument24 pagesModule 2: Financing of Projectsmy VinayNo ratings yet

- Unit 4Document19 pagesUnit 4Dawit NegashNo ratings yet

- Bidding DocumentsDocument62 pagesBidding DocumentskriforbizNo ratings yet

- Bidding-Document-PR No. 2021-10-276Document43 pagesBidding-Document-PR No. 2021-10-276Daniel TuazonNo ratings yet

- Itb Design and Build Six-Storey With Roof Deck Mez Administration Office BuildingDocument89 pagesItb Design and Build Six-Storey With Roof Deck Mez Administration Office BuildingKarl MoralejoNo ratings yet

- Module 3 - Borrowing CostsDocument3 pagesModule 3 - Borrowing CostsLui100% (1)

- Invitation To BidDocument92 pagesInvitation To BidAnita QueNo ratings yet

- Project Finance Documents: Fretutorial Free TutorialDocument7 pagesProject Finance Documents: Fretutorial Free TutorialColin TanNo ratings yet

- Completion of Ten Storey Higher Education Building in Batangas State University Pablo BorbonDocument184 pagesCompletion of Ten Storey Higher Education Building in Batangas State University Pablo BorbonraezenbukalNo ratings yet

- Guidelines For Financing To Housing Builders/Developers: State Bank of Pakistan, KarachiDocument6 pagesGuidelines For Financing To Housing Builders/Developers: State Bank of Pakistan, KarachiAnush VedhNo ratings yet

- PC 22 - Practice Set 7Document16 pagesPC 22 - Practice Set 7Shadab RashidNo ratings yet

- Bac 20210923001Document189 pagesBac 20210923001Jeremy YabutNo ratings yet

- Projects Analysis and Implementation Assignment-Ii: Group No: 4Document13 pagesProjects Analysis and Implementation Assignment-Ii: Group No: 4Bindu_Shree_4565No ratings yet

- AF210: Financial Accounting: School of Accounting and FinanceDocument11 pagesAF210: Financial Accounting: School of Accounting and FinanceShikhaNo ratings yet

- BIDDING DOCUMENTS 1.5M BaliwananDocument41 pagesBIDDING DOCUMENTS 1.5M BaliwananRubie Anne SaducosNo ratings yet

- PBD - Blinds and CurtainsDocument46 pagesPBD - Blinds and CurtainsM C Dela CrzNo ratings yet

- Bid Docs PB-I-2023-09-009 Construction of Multi-Purpose Building, Carmen Integrated School - TakerDocument37 pagesBid Docs PB-I-2023-09-009 Construction of Multi-Purpose Building, Carmen Integrated School - TakerJustin YuabNo ratings yet

- Bac 20211020001Document181 pagesBac 20211020001Cherry DuldulaoNo ratings yet

- Delay and Disruption Claims March 2014 PDFDocument31 pagesDelay and Disruption Claims March 2014 PDFNuruddin CuevaNo ratings yet

- Procurement Guide: CHP Financing: 1. OverviewDocument9 pagesProcurement Guide: CHP Financing: 1. OverviewCarlos LinaresNo ratings yet

- PBDs - SECURITY SERVICES FOR MEZ and SEZsDocument44 pagesPBDs - SECURITY SERVICES FOR MEZ and SEZsPatrickNo ratings yet

- Bid Docs - 24HG0092Document70 pagesBid Docs - 24HG0092SamNo ratings yet

- 0060 2021 Dayao, Burias Infrastructure Project 07.19 09.16 09.28 9AMDocument35 pages0060 2021 Dayao, Burias Infrastructure Project 07.19 09.16 09.28 9AMJecyl GuelosNo ratings yet

- Itb Proposed Design and Build of Mez Administration Office BuildingDocument38 pagesItb Proposed Design and Build of Mez Administration Office BuildingMarjan CañaNo ratings yet

- Bid Docs-StpDocument57 pagesBid Docs-StpkhuNo ratings yet

- Chapter 2 Summary Financial Statement AnalysisDocument5 pagesChapter 2 Summary Financial Statement AnalysisAzlanNo ratings yet

- Procurement of Projects: InfrastructureDocument47 pagesProcurement of Projects: InfrastructureNicole RodilNo ratings yet

- PBD PR 21-07-0323 Re BidDocument72 pagesPBD PR 21-07-0323 Re BidAayan’s VlogNo ratings yet

- Chapter 5 CPFDocument15 pagesChapter 5 CPFSara NegashNo ratings yet

- Class 6 Notes 04072022Document4 pagesClass 6 Notes 04072022Munyangoga BonaventureNo ratings yet

- Bidding Docs - 24KM0059Document36 pagesBidding Docs - 24KM0059Tine HernaneNo ratings yet

- PFI ManualDocument46 pagesPFI ManualMaggie HartonoNo ratings yet

- BIDDING DOCUMENTS 1M, HatcherymDocument41 pagesBIDDING DOCUMENTS 1M, HatcherymRubie Anne SaducosNo ratings yet

- Accounting For Public Sector Chap 5Document38 pagesAccounting For Public Sector Chap 5fekadegebretsadik478729No ratings yet

- PBD Infrastructure+Projects Office+Fit-Out GLO+110621 PDFDocument67 pagesPBD Infrastructure+Projects Office+Fit-Out GLO+110621 PDFVanessa de VeraNo ratings yet

- Tugas Kasus Construction Company - Fahmi Izzuddin - 1506750296Document3 pagesTugas Kasus Construction Company - Fahmi Izzuddin - 1506750296Fahmi IzzuddinNo ratings yet

- VCE Summer Internship Program 2020: Name Email-ID Smart Task No. Project TopicDocument4 pagesVCE Summer Internship Program 2020: Name Email-ID Smart Task No. Project TopicYaShNo ratings yet

- Bid Docs Multipurpose BC Ez 102021Document154 pagesBid Docs Multipurpose BC Ez 102021Justin YuabNo ratings yet

- Mega Project Assurance: Volume One - The Terminological DictionaryFrom EverandMega Project Assurance: Volume One - The Terminological DictionaryNo ratings yet

- 320 Accountancy Eng Lesson5Document23 pages320 Accountancy Eng Lesson5MATIULLAHNo ratings yet

- Accounting Conventions and Standards: Module - 1Document12 pagesAccounting Conventions and Standards: Module - 1MATIULLAHNo ratings yet

- Accounting For Business Transactions: Module - 1Document30 pagesAccounting For Business Transactions: Module - 1MATIULLAHNo ratings yet

- E-Ticket Receipt & Itinerary: 2021 Emirates. All Rights ReservedDocument2 pagesE-Ticket Receipt & Itinerary: 2021 Emirates. All Rights ReservedMATIULLAHNo ratings yet

- Reference Letter For Immigration 01Document1 pageReference Letter For Immigration 01MATIULLAHNo ratings yet

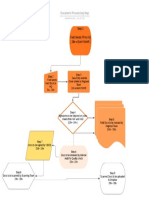

- Document Processing Map: Step 1 Field Sends FR To HQ (28 Each Month)Document1 pageDocument Processing Map: Step 1 Field Sends FR To HQ (28 Each Month)MATIULLAHNo ratings yet

- WAW Audit Findings 113394 & 109111Document2 pagesWAW Audit Findings 113394 & 109111MATIULLAHNo ratings yet

- 2007 Sida-UNDP Evaluation Revised Final Report - 9 August 07Document79 pages2007 Sida-UNDP Evaluation Revised Final Report - 9 August 07MATIULLAHNo ratings yet

- GIZ-Afghanistan: A. Position Applied ForDocument3 pagesGIZ-Afghanistan: A. Position Applied ForMATIULLAHNo ratings yet

- Detailed Project Proposal For: Earnesta Child and Youth Development ProjectDocument11 pagesDetailed Project Proposal For: Earnesta Child and Youth Development ProjectMATIULLAHNo ratings yet

- Asylum Declaration Writing Guide: WWW - Uscis.govDocument14 pagesAsylum Declaration Writing Guide: WWW - Uscis.govMATIULLAHNo ratings yet

- Changes To Non - Exempt Payslips and Check StubsDocument14 pagesChanges To Non - Exempt Payslips and Check StubsMATIULLAHNo ratings yet

- V - Audits and Compliance - FINAL - SEBDocument9 pagesV - Audits and Compliance - FINAL - SEBMATIULLAHNo ratings yet

- Unaccompanied Asylum Seeking Children Statement of Evidence (SEF)Document43 pagesUnaccompanied Asylum Seeking Children Statement of Evidence (SEF)MATIULLAHNo ratings yet

- Itemized Budget - WAW 972 002 SOMDocument4 pagesItemized Budget - WAW 972 002 SOMMATIULLAHNo ratings yet

- Template Letter To MP-1Document1 pageTemplate Letter To MP-1MATIULLAHNo ratings yet

- SIV Bio DataDocument1 pageSIV Bio DataMATIULLAHNo ratings yet

- IRAP SIV Report 2020Document43 pagesIRAP SIV Report 2020MATIULLAHNo ratings yet

- Request For Quotation The Procurement of Goods or Non-Consulting ServicesDocument42 pagesRequest For Quotation The Procurement of Goods or Non-Consulting Serviceslathasin somxaiyNo ratings yet

- WIN 12-Digit NRIC Number Without Spacing 66628 WIN Passport Number Without Spacing 66628Document9 pagesWIN 12-Digit NRIC Number Without Spacing 66628 WIN Passport Number Without Spacing 66628nitekillerNo ratings yet

- Brown and Green Scrapbook Meditation Healthcare Medical PresentationDocument9 pagesBrown and Green Scrapbook Meditation Healthcare Medical PresentationSiti UmairahNo ratings yet

- Ensun-Sundrop PI 17.08.2022Document1 pageEnsun-Sundrop PI 17.08.2022prabhakaranNo ratings yet

- Contract of LeaseDocument1 pageContract of LeaseJules Clyde Fernandez IsaacNo ratings yet

- Bayview Beach Resort PenangDocument2 pagesBayview Beach Resort PenangVeraNo ratings yet

- Lion Air Eticket (JHWEKY) - ShabriDocument2 pagesLion Air Eticket (JHWEKY) - ShabriAmrullah SattarNo ratings yet

- AlyssaDocument3 pagesAlyssaJonathan Val Fernandez PagdilaoNo ratings yet

- Package: Bridges No 2 - 9 Sivok Rangpo New BG Rail Line Project Tender DocumentsDocument6 pagesPackage: Bridges No 2 - 9 Sivok Rangpo New BG Rail Line Project Tender DocumentsKawrw DgedeaNo ratings yet

- PPE - FinalDocument71 pagesPPE - FinalKristen KooNo ratings yet

- Flipkart Labels 01 Apr 2024 09 52Document1 pageFlipkart Labels 01 Apr 2024 09 524frontenterprises.2023No ratings yet

- Jharkhand Ajay InstructorDocument3 pagesJharkhand Ajay InstructorAjay ChauhanNo ratings yet

- MSME CertificateDocument1 pageMSME Certificatearunjoshi12345No ratings yet

- Project Information and Evaluation FormDocument3 pagesProject Information and Evaluation FormRichard LabroNo ratings yet

- Attendance Sheet For Dialysis UnitDocument4 pagesAttendance Sheet For Dialysis UnitgoshidanieltasleemNo ratings yet

- Dwnload Full Accounting Information Systems 10th Edition Gelinas Solutions Manual PDFDocument35 pagesDwnload Full Accounting Information Systems 10th Edition Gelinas Solutions Manual PDFwaymarkbirdlimengh1j100% (17)

- Cockatoo Island SubmissionDocument30 pagesCockatoo Island SubmissionThe Sydney Morning Herald100% (1)

- Bourns v. Carman, 7 Phils. 117 - 1906Document3 pagesBourns v. Carman, 7 Phils. 117 - 1906josephinelogronoNo ratings yet

- Commu BBI LUPONDocument3 pagesCommu BBI LUPONDenielle DelosoNo ratings yet

- Accounting Standard ResumeDocument7 pagesAccounting Standard ResumeIvana YustitiaNo ratings yet

- 27A1100001972546Document2 pages27A1100001972546Meet Communication ServicesNo ratings yet

- Revised Corporation Code 11.16.19Document118 pagesRevised Corporation Code 11.16.19Ed Apalla100% (1)

- LTC Form - DarDocument2 pagesLTC Form - DarFred BagbagenNo ratings yet

- Spa Bir UpdatingDocument1 pageSpa Bir Updatingannette leonardoNo ratings yet

- Argentina: Cash and Treasury ManagementDocument45 pagesArgentina: Cash and Treasury Managementshahid2opuNo ratings yet

Download as pdf or txt

You might also like

- Ppa LetterDocument1 pagePpa LetterDestiny TobiNo ratings yet

- Let Export Copy: Indian Customs Edi SystemDocument10 pagesLet Export Copy: Indian Customs Edi Systemsaikatpaul22No ratings yet

- VCE Summer Internship Program 2021: Ruchira Parwanda 3 Financial Modelling (Infra)Document4 pagesVCE Summer Internship Program 2021: Ruchira Parwanda 3 Financial Modelling (Infra)Ruchira ParwandaNo ratings yet

- Department of Agriculture Republic of The Philippines: Da-Cso Application FormDocument7 pagesDepartment of Agriculture Republic of The Philippines: Da-Cso Application FormVerna BeNo ratings yet

- Introduction To Project Finance - A Guide For Contractors and EngineersDocument9 pagesIntroduction To Project Finance - A Guide For Contractors and Engineershazemdiab100% (1)

- Creditcardrush JSONDocument31 pagesCreditcardrush JSONmacroniess khanNo ratings yet

- 13-SOP For Safe Operation Limestone CrusherDocument2 pages13-SOP For Safe Operation Limestone Crushergothic centuary60% (5)

- Aef 2013 Audit Acc ReqDocument9 pagesAef 2013 Audit Acc Reqvikas_ojha54706No ratings yet

- ToR 516Document4 pagesToR 516Rumki SarkarNo ratings yet

- RFP DocumentsDocument10 pagesRFP DocumentsYasir FahadNo ratings yet

- Smart Task 3Document5 pagesSmart Task 3Utkarsh ChaturvediNo ratings yet

- Funding Programme - Long-Term ProjectDocument3 pagesFunding Programme - Long-Term ProjectmarkzwikNo ratings yet

- Master Agreement For Services 4Document11 pagesMaster Agreement For Services 4Tamer SayedNo ratings yet

- Capital Project FundDocument7 pagesCapital Project FundmeseleNo ratings yet

- III. Compensation and Effort Reporting For Grants & ContractsDocument7 pagesIII. Compensation and Effort Reporting For Grants & ContractsMATIULLAHNo ratings yet

- Chapter Four-Part Ii: Accounting For Governmental FundsDocument30 pagesChapter Four-Part Ii: Accounting For Governmental FundsabateNo ratings yet

- 24C00087 - Bid Documents - FMP Sitio Brown Phase IDocument58 pages24C00087 - Bid Documents - FMP Sitio Brown Phase ISamNo ratings yet

- Process of Project Financing: Feasibility StudyDocument23 pagesProcess of Project Financing: Feasibility StudyRohit PadalkarNo ratings yet

- PFDocument16 pagesPFadabotor7No ratings yet

- Chapter Four CPFDocument28 pagesChapter Four CPFtame kibruNo ratings yet

- BID DOCS LEDBillboardDocument30 pagesBID DOCS LEDBillboardNanz11 SerranoNo ratings yet

- PCOA Module 6 - PAS 23 and 24Document8 pagesPCOA Module 6 - PAS 23 and 24Jan JanNo ratings yet

- Report On Funds RaisingDocument28 pagesReport On Funds RaisingNikita MajiNo ratings yet

- Module 2: Financing of ProjectsDocument24 pagesModule 2: Financing of Projectsmy VinayNo ratings yet

- Unit 4Document19 pagesUnit 4Dawit NegashNo ratings yet

- Bidding DocumentsDocument62 pagesBidding DocumentskriforbizNo ratings yet

- Bidding-Document-PR No. 2021-10-276Document43 pagesBidding-Document-PR No. 2021-10-276Daniel TuazonNo ratings yet

- Itb Design and Build Six-Storey With Roof Deck Mez Administration Office BuildingDocument89 pagesItb Design and Build Six-Storey With Roof Deck Mez Administration Office BuildingKarl MoralejoNo ratings yet

- Module 3 - Borrowing CostsDocument3 pagesModule 3 - Borrowing CostsLui100% (1)

- Invitation To BidDocument92 pagesInvitation To BidAnita QueNo ratings yet

- Project Finance Documents: Fretutorial Free TutorialDocument7 pagesProject Finance Documents: Fretutorial Free TutorialColin TanNo ratings yet

- Completion of Ten Storey Higher Education Building in Batangas State University Pablo BorbonDocument184 pagesCompletion of Ten Storey Higher Education Building in Batangas State University Pablo BorbonraezenbukalNo ratings yet

- Guidelines For Financing To Housing Builders/Developers: State Bank of Pakistan, KarachiDocument6 pagesGuidelines For Financing To Housing Builders/Developers: State Bank of Pakistan, KarachiAnush VedhNo ratings yet

- PC 22 - Practice Set 7Document16 pagesPC 22 - Practice Set 7Shadab RashidNo ratings yet

- Bac 20210923001Document189 pagesBac 20210923001Jeremy YabutNo ratings yet

- Projects Analysis and Implementation Assignment-Ii: Group No: 4Document13 pagesProjects Analysis and Implementation Assignment-Ii: Group No: 4Bindu_Shree_4565No ratings yet

- AF210: Financial Accounting: School of Accounting and FinanceDocument11 pagesAF210: Financial Accounting: School of Accounting and FinanceShikhaNo ratings yet

- BIDDING DOCUMENTS 1.5M BaliwananDocument41 pagesBIDDING DOCUMENTS 1.5M BaliwananRubie Anne SaducosNo ratings yet

- PBD - Blinds and CurtainsDocument46 pagesPBD - Blinds and CurtainsM C Dela CrzNo ratings yet

- Bid Docs PB-I-2023-09-009 Construction of Multi-Purpose Building, Carmen Integrated School - TakerDocument37 pagesBid Docs PB-I-2023-09-009 Construction of Multi-Purpose Building, Carmen Integrated School - TakerJustin YuabNo ratings yet

- Bac 20211020001Document181 pagesBac 20211020001Cherry DuldulaoNo ratings yet

- Delay and Disruption Claims March 2014 PDFDocument31 pagesDelay and Disruption Claims March 2014 PDFNuruddin CuevaNo ratings yet

- Procurement Guide: CHP Financing: 1. OverviewDocument9 pagesProcurement Guide: CHP Financing: 1. OverviewCarlos LinaresNo ratings yet

- PBDs - SECURITY SERVICES FOR MEZ and SEZsDocument44 pagesPBDs - SECURITY SERVICES FOR MEZ and SEZsPatrickNo ratings yet

- Bid Docs - 24HG0092Document70 pagesBid Docs - 24HG0092SamNo ratings yet

- 0060 2021 Dayao, Burias Infrastructure Project 07.19 09.16 09.28 9AMDocument35 pages0060 2021 Dayao, Burias Infrastructure Project 07.19 09.16 09.28 9AMJecyl GuelosNo ratings yet

- Itb Proposed Design and Build of Mez Administration Office BuildingDocument38 pagesItb Proposed Design and Build of Mez Administration Office BuildingMarjan CañaNo ratings yet

- Bid Docs-StpDocument57 pagesBid Docs-StpkhuNo ratings yet

- Chapter 2 Summary Financial Statement AnalysisDocument5 pagesChapter 2 Summary Financial Statement AnalysisAzlanNo ratings yet

- Procurement of Projects: InfrastructureDocument47 pagesProcurement of Projects: InfrastructureNicole RodilNo ratings yet

- PBD PR 21-07-0323 Re BidDocument72 pagesPBD PR 21-07-0323 Re BidAayan’s VlogNo ratings yet

- Chapter 5 CPFDocument15 pagesChapter 5 CPFSara NegashNo ratings yet

- Class 6 Notes 04072022Document4 pagesClass 6 Notes 04072022Munyangoga BonaventureNo ratings yet

- Bidding Docs - 24KM0059Document36 pagesBidding Docs - 24KM0059Tine HernaneNo ratings yet

- PFI ManualDocument46 pagesPFI ManualMaggie HartonoNo ratings yet

- BIDDING DOCUMENTS 1M, HatcherymDocument41 pagesBIDDING DOCUMENTS 1M, HatcherymRubie Anne SaducosNo ratings yet

- Accounting For Public Sector Chap 5Document38 pagesAccounting For Public Sector Chap 5fekadegebretsadik478729No ratings yet

- PBD Infrastructure+Projects Office+Fit-Out GLO+110621 PDFDocument67 pagesPBD Infrastructure+Projects Office+Fit-Out GLO+110621 PDFVanessa de VeraNo ratings yet

- Tugas Kasus Construction Company - Fahmi Izzuddin - 1506750296Document3 pagesTugas Kasus Construction Company - Fahmi Izzuddin - 1506750296Fahmi IzzuddinNo ratings yet

- VCE Summer Internship Program 2020: Name Email-ID Smart Task No. Project TopicDocument4 pagesVCE Summer Internship Program 2020: Name Email-ID Smart Task No. Project TopicYaShNo ratings yet

- Bid Docs Multipurpose BC Ez 102021Document154 pagesBid Docs Multipurpose BC Ez 102021Justin YuabNo ratings yet

- Mega Project Assurance: Volume One - The Terminological DictionaryFrom EverandMega Project Assurance: Volume One - The Terminological DictionaryNo ratings yet

- 320 Accountancy Eng Lesson5Document23 pages320 Accountancy Eng Lesson5MATIULLAHNo ratings yet

- Accounting Conventions and Standards: Module - 1Document12 pagesAccounting Conventions and Standards: Module - 1MATIULLAHNo ratings yet

- Accounting For Business Transactions: Module - 1Document30 pagesAccounting For Business Transactions: Module - 1MATIULLAHNo ratings yet

- E-Ticket Receipt & Itinerary: 2021 Emirates. All Rights ReservedDocument2 pagesE-Ticket Receipt & Itinerary: 2021 Emirates. All Rights ReservedMATIULLAHNo ratings yet

- Reference Letter For Immigration 01Document1 pageReference Letter For Immigration 01MATIULLAHNo ratings yet

- Document Processing Map: Step 1 Field Sends FR To HQ (28 Each Month)Document1 pageDocument Processing Map: Step 1 Field Sends FR To HQ (28 Each Month)MATIULLAHNo ratings yet

- WAW Audit Findings 113394 & 109111Document2 pagesWAW Audit Findings 113394 & 109111MATIULLAHNo ratings yet

- 2007 Sida-UNDP Evaluation Revised Final Report - 9 August 07Document79 pages2007 Sida-UNDP Evaluation Revised Final Report - 9 August 07MATIULLAHNo ratings yet

- GIZ-Afghanistan: A. Position Applied ForDocument3 pagesGIZ-Afghanistan: A. Position Applied ForMATIULLAHNo ratings yet

- Detailed Project Proposal For: Earnesta Child and Youth Development ProjectDocument11 pagesDetailed Project Proposal For: Earnesta Child and Youth Development ProjectMATIULLAHNo ratings yet

- Asylum Declaration Writing Guide: WWW - Uscis.govDocument14 pagesAsylum Declaration Writing Guide: WWW - Uscis.govMATIULLAHNo ratings yet

- Changes To Non - Exempt Payslips and Check StubsDocument14 pagesChanges To Non - Exempt Payslips and Check StubsMATIULLAHNo ratings yet

- V - Audits and Compliance - FINAL - SEBDocument9 pagesV - Audits and Compliance - FINAL - SEBMATIULLAHNo ratings yet

- Unaccompanied Asylum Seeking Children Statement of Evidence (SEF)Document43 pagesUnaccompanied Asylum Seeking Children Statement of Evidence (SEF)MATIULLAHNo ratings yet

- Itemized Budget - WAW 972 002 SOMDocument4 pagesItemized Budget - WAW 972 002 SOMMATIULLAHNo ratings yet

- Template Letter To MP-1Document1 pageTemplate Letter To MP-1MATIULLAHNo ratings yet

- SIV Bio DataDocument1 pageSIV Bio DataMATIULLAHNo ratings yet

- IRAP SIV Report 2020Document43 pagesIRAP SIV Report 2020MATIULLAHNo ratings yet

- Request For Quotation The Procurement of Goods or Non-Consulting ServicesDocument42 pagesRequest For Quotation The Procurement of Goods or Non-Consulting Serviceslathasin somxaiyNo ratings yet

- WIN 12-Digit NRIC Number Without Spacing 66628 WIN Passport Number Without Spacing 66628Document9 pagesWIN 12-Digit NRIC Number Without Spacing 66628 WIN Passport Number Without Spacing 66628nitekillerNo ratings yet

- Brown and Green Scrapbook Meditation Healthcare Medical PresentationDocument9 pagesBrown and Green Scrapbook Meditation Healthcare Medical PresentationSiti UmairahNo ratings yet

- Ensun-Sundrop PI 17.08.2022Document1 pageEnsun-Sundrop PI 17.08.2022prabhakaranNo ratings yet

- Contract of LeaseDocument1 pageContract of LeaseJules Clyde Fernandez IsaacNo ratings yet

- Bayview Beach Resort PenangDocument2 pagesBayview Beach Resort PenangVeraNo ratings yet

- Lion Air Eticket (JHWEKY) - ShabriDocument2 pagesLion Air Eticket (JHWEKY) - ShabriAmrullah SattarNo ratings yet

- AlyssaDocument3 pagesAlyssaJonathan Val Fernandez PagdilaoNo ratings yet

- Package: Bridges No 2 - 9 Sivok Rangpo New BG Rail Line Project Tender DocumentsDocument6 pagesPackage: Bridges No 2 - 9 Sivok Rangpo New BG Rail Line Project Tender DocumentsKawrw DgedeaNo ratings yet

- PPE - FinalDocument71 pagesPPE - FinalKristen KooNo ratings yet

- Flipkart Labels 01 Apr 2024 09 52Document1 pageFlipkart Labels 01 Apr 2024 09 524frontenterprises.2023No ratings yet

- Jharkhand Ajay InstructorDocument3 pagesJharkhand Ajay InstructorAjay ChauhanNo ratings yet

- MSME CertificateDocument1 pageMSME Certificatearunjoshi12345No ratings yet

- Project Information and Evaluation FormDocument3 pagesProject Information and Evaluation FormRichard LabroNo ratings yet

- Attendance Sheet For Dialysis UnitDocument4 pagesAttendance Sheet For Dialysis UnitgoshidanieltasleemNo ratings yet

- Dwnload Full Accounting Information Systems 10th Edition Gelinas Solutions Manual PDFDocument35 pagesDwnload Full Accounting Information Systems 10th Edition Gelinas Solutions Manual PDFwaymarkbirdlimengh1j100% (17)

- Cockatoo Island SubmissionDocument30 pagesCockatoo Island SubmissionThe Sydney Morning Herald100% (1)

- Bourns v. Carman, 7 Phils. 117 - 1906Document3 pagesBourns v. Carman, 7 Phils. 117 - 1906josephinelogronoNo ratings yet

- Commu BBI LUPONDocument3 pagesCommu BBI LUPONDenielle DelosoNo ratings yet

- Accounting Standard ResumeDocument7 pagesAccounting Standard ResumeIvana YustitiaNo ratings yet

- 27A1100001972546Document2 pages27A1100001972546Meet Communication ServicesNo ratings yet

- Revised Corporation Code 11.16.19Document118 pagesRevised Corporation Code 11.16.19Ed Apalla100% (1)

- LTC Form - DarDocument2 pagesLTC Form - DarFred BagbagenNo ratings yet

- Spa Bir UpdatingDocument1 pageSpa Bir Updatingannette leonardoNo ratings yet

- Argentina: Cash and Treasury ManagementDocument45 pagesArgentina: Cash and Treasury Managementshahid2opuNo ratings yet