Download as pdf or txt

You might also like

- Market Report Home Appliances Industry in India (2023 - 2028)Document28 pagesMarket Report Home Appliances Industry in India (2023 - 2028)sameer tajneNo ratings yet

- Foreign Direct Investment in India - Case StudiesDocument72 pagesForeign Direct Investment in India - Case StudiesManish Solanki73% (15)

- Knowing God Study Guide - Section TwoDocument56 pagesKnowing God Study Guide - Section Twomercab15100% (2)

- SCADAPack 334 Hardware ManualDocument165 pagesSCADAPack 334 Hardware ManualFeri HandoyoNo ratings yet

- IIM-K IB-E 2021-22 AB S2-3 DynamicsDocument37 pagesIIM-K IB-E 2021-22 AB S2-3 DynamicsNeeharika DangetiNo ratings yet

- Bulls BearsDocument50 pagesBulls BearsVivek SinghalNo ratings yet

- Bain - India Private Equity Report 2022Document40 pagesBain - India Private Equity Report 2022Taher JavanNo ratings yet

- What We Are Reading - Volume 2.096Document104 pagesWhat We Are Reading - Volume 2.096Dhar RakulNo ratings yet

- Life Insurance Corporation's Future ProspectsDocument13 pagesLife Insurance Corporation's Future ProspectsAman GedamNo ratings yet

- The Age of Coming of d2c in India 1latticeDocument62 pagesThe Age of Coming of d2c in India 1latticeDivyansh TiwariNo ratings yet

- A Year of RecordsDocument4 pagesA Year of RecordsAdobe AcrobatNo ratings yet

- ChapriDocument72 pagesChaprishweta100% (1)

- The Coming of Age of D2C in IndiaDocument62 pagesThe Coming of Age of D2C in IndiaAbhinav NaiduNo ratings yet

- Ey Private Credit in IndiaDocument32 pagesEy Private Credit in IndiaLeggings LivingNo ratings yet

- India As A Global Hub For White Goods: Presented By: Group 4Document14 pagesIndia As A Global Hub For White Goods: Presented By: Group 4Prerna DhandNo ratings yet

- Industry ReportsDocument50 pagesIndustry ReportshamzaNo ratings yet

- BULLS BEARS India Valuations Handbook 20221103 MOSLDocument48 pagesBULLS BEARS India Valuations Handbook 20221103 MOSLRohan ShahNo ratings yet

- Creating Markets in Thailand Rebooting Productivity For Resilient GrowthDocument164 pagesCreating Markets in Thailand Rebooting Productivity For Resilient Growthengenharia_carlosNo ratings yet

- Kbuzz: Sector InsightsDocument41 pagesKbuzz: Sector InsightsSuvin NambiarNo ratings yet

- Adjustment-En-Sovereign Solutions 2022 Business Plan v2 October 3 - ReviewedDocument31 pagesAdjustment-En-Sovereign Solutions 2022 Business Plan v2 October 3 - Reviewedminhbu114No ratings yet

- Gleeds India Construction Cost January 2022Document36 pagesGleeds India Construction Cost January 2022Timoty Travaagan100% (1)

- Holiday HOME WORK FOR Class XI and XIIDocument4 pagesHoliday HOME WORK FOR Class XI and XIIAryaman NegiNo ratings yet

- India Domestic BPO Market: A Idc I M C SDocument2 pagesIndia Domestic BPO Market: A Idc I M C Skes7No ratings yet

- 30 Ijr February 2022Document5 pages30 Ijr February 2022patrababai2003No ratings yet

- How India Lends Fy22Document57 pagesHow India Lends Fy22Arindam MondalNo ratings yet

- Realising The Potential of Real EstateDocument28 pagesRealising The Potential of Real EstateKunal BawaneNo ratings yet

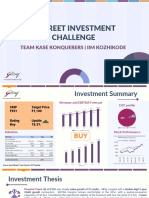

- R-Street Investment Challenge: Team Kase Konquerers - Iim KozhikodeDocument12 pagesR-Street Investment Challenge: Team Kase Konquerers - Iim KozhikodeApoorva JainNo ratings yet

- Resilience of Hyderabad Residential Market During COVID-19Document5 pagesResilience of Hyderabad Residential Market During COVID-19Celestine DcruzNo ratings yet

- India Furniture ReportDocument91 pagesIndia Furniture ReportKumar IyerNo ratings yet

- India's post-COVID-19 Economic Recovery: The M&A ImperativeDocument6 pagesIndia's post-COVID-19 Economic Recovery: The M&A ImperativehvsbouaNo ratings yet

- JLL Construction Cost Guide Book India 2022Document26 pagesJLL Construction Cost Guide Book India 2022svNo ratings yet

- Fra Cia 2BDocument17 pagesFra Cia 2BJohnsey RoyNo ratings yet

- 1613021865economy Matters December 2020 - Gems & JewelleryDocument33 pages1613021865economy Matters December 2020 - Gems & Jewellerysara eltonyNo ratings yet

- Unit 1.1 India's Stalled RiseDocument3 pagesUnit 1.1 India's Stalled RiseKushagra AroraNo ratings yet

- Ey Pe VC Trend BookDocument80 pagesEy Pe VC Trend BookRama KumarNo ratings yet

- Bain IVCA India Venture Capital Report 2022 1648706342Document42 pagesBain IVCA India Venture Capital Report 2022 1648706342Kiran MaadamshettiNo ratings yet

- KnightFrank - India Real Estate H2 2020Document150 pagesKnightFrank - India Real Estate H2 2020Swanand KulkarniNo ratings yet

- Cosmo FilmsDocument271 pagesCosmo FilmsReTHINK INDIANo ratings yet

- 8f0ek-B9nyr - G Manjusha MalliaDocument3 pages8f0ek-B9nyr - G Manjusha MalliaNaman AgrawalNo ratings yet

- Business Standard: Article - What Is Pli For?Document2 pagesBusiness Standard: Article - What Is Pli For?Manish MeenaNo ratings yet

- Environment Scanning of Kotak Mahindra BankDocument17 pagesEnvironment Scanning of Kotak Mahindra Bankmba globalNo ratings yet

- IEC GRP Assignment - SECB - MAKE IN INDIADocument27 pagesIEC GRP Assignment - SECB - MAKE IN INDIASunny ShuklaNo ratings yet

- MacroEco Initiate BuyDocument21 pagesMacroEco Initiate BuymittleNo ratings yet

- Can REIT Address Expectations of Indian Real Estate Investors?Document7 pagesCan REIT Address Expectations of Indian Real Estate Investors?alim shaikhNo ratings yet

- Decoding Housing For All 2022Document36 pagesDecoding Housing For All 2022Tanvi YadavNo ratings yet

- Managing Organizational and Management Challenges in IndiaDocument24 pagesManaging Organizational and Management Challenges in Indiamukeshsomani1No ratings yet

- GBM - Answers ChatGPT&BingDocument12 pagesGBM - Answers ChatGPT&BingRishabh NishadNo ratings yet

- Economics - Mains Syllabus & PYQs - Topicwise - FDocument8 pagesEconomics - Mains Syllabus & PYQs - Topicwise - FtamizhanmusickingNo ratings yet

- Pulse of Fintech h1 22Document62 pagesPulse of Fintech h1 22prokonektNo ratings yet

- Role of Nbfcs and Hfcs in Driving Sustainable GDP Growth in IndiaDocument44 pagesRole of Nbfcs and Hfcs in Driving Sustainable GDP Growth in IndiaVivek BandebucheNo ratings yet

- BULLS BEARS - India Valuations Handbook-20221006-MOSL-PG048Document48 pagesBULLS BEARS - India Valuations Handbook-20221006-MOSL-PG048coinage capitalNo ratings yet

- India Manufacturing MomentDocument16 pagesIndia Manufacturing MomentArmeet ChhatwalNo ratings yet

- Services IndustryDocument13 pagesServices IndustryAbhishek pathangeNo ratings yet

- KNOW Your Consumer - Final Web Single PageDocument64 pagesKNOW Your Consumer - Final Web Single PageAakash MalhotraNo ratings yet

- IndiaDocument8 pagesIndiaDivisha AgarwalNo ratings yet

- Skills PPT For NSDA WorkshopDocument44 pagesSkills PPT For NSDA WorkshopMuktadir IslamNo ratings yet

- ORF GVC Survey Report AugustDocument72 pagesORF GVC Survey Report August王思远No ratings yet

- FOSL Sept 27 2018 Investor Pres Final1Document26 pagesFOSL Sept 27 2018 Investor Pres Final1mayankNo ratings yet

- India Consumer DeloitteDocument60 pagesIndia Consumer DeloittevidhiNo ratings yet

- Global in ContextDocument9 pagesGlobal in ContextOluwadunsin OlajideNo ratings yet

- DBI AssignmentDocument20 pagesDBI AssignmentMojahidaNo ratings yet

- A New Dawn for Global Value Chain Participation in the PhilippinesFrom EverandA New Dawn for Global Value Chain Participation in the PhilippinesNo ratings yet

- IIM-K IB-E 2021-22 AB S6 Investment Forex RiskDocument14 pagesIIM-K IB-E 2021-22 AB S6 Investment Forex RiskNeeharika DangetiNo ratings yet

- IIM-K IB-E 2021-22 AB S4-5 Exports ImportsDocument20 pagesIIM-K IB-E 2021-22 AB S4-5 Exports ImportsNeeharika DangetiNo ratings yet

- Iim-K Ib-E 2021-22 Ab s23-24 Emerging ChinaDocument28 pagesIim-K Ib-E 2021-22 Ab s23-24 Emerging ChinaNeeharika DangetiNo ratings yet

- IIM-K IB-E 2021-22 AB S2-3 DynamicsDocument37 pagesIIM-K IB-E 2021-22 AB S2-3 DynamicsNeeharika DangetiNo ratings yet

- IIM-K IB-E 2021-22 AB S19-20 Ethical AspectsDocument31 pagesIIM-K IB-E 2021-22 AB S19-20 Ethical AspectsNeeharika DangetiNo ratings yet

- IIM-K IB-E 2021-22 AB S15-16 Organization ControlDocument40 pagesIIM-K IB-E 2021-22 AB S15-16 Organization ControlNeeharika DangetiNo ratings yet

- IIM-K IB-E 2021-22 AB S1 Introduction OverviewDocument10 pagesIIM-K IB-E 2021-22 AB S1 Introduction OverviewNeeharika DangetiNo ratings yet

- Iim-K Ib-E 2021-22 Ab s11-12 Operations TPDocument21 pagesIim-K Ib-E 2021-22 Ab s11-12 Operations TPNeeharika DangetiNo ratings yet

- Hspice Simulation of SRAM PDFDocument65 pagesHspice Simulation of SRAM PDFYatheesh KaggereNo ratings yet

- The Origin of The CosmosDocument508 pagesThe Origin of The CosmosAntonio Pinto RenedoNo ratings yet

- Creative Writing - Q4 - M6Document8 pagesCreative Writing - Q4 - M6Aldous AngcayNo ratings yet

- Jaka Index6 PDFDocument85 pagesJaka Index6 PDFFábio Origuela de LiraNo ratings yet

- Bible: A Blind Man SeesDocument8 pagesBible: A Blind Man SeesBeth DNo ratings yet

- 1 SPDocument36 pages1 SPVăn VẹoNo ratings yet

- E PerioTherapyDocument5 pagesE PerioTherapymaherinoNo ratings yet

- STM29 - Lower Half Martinito, John Patrick Eldwin Recto, Jan Ralph Yanga, Nicole Francine BDocument2 pagesSTM29 - Lower Half Martinito, John Patrick Eldwin Recto, Jan Ralph Yanga, Nicole Francine BJan Ralph RectoNo ratings yet

- CH 18Document9 pagesCH 18Julie Nix FrazierNo ratings yet

- Original Research Paper Geography: M.A Geography, UGC NET-JRF (Government P.G College Badli, Haryana)Document4 pagesOriginal Research Paper Geography: M.A Geography, UGC NET-JRF (Government P.G College Badli, Haryana)neeraj kumarNo ratings yet

- Astm A570 1979Document5 pagesAstm A570 1979set_ltdaNo ratings yet

- F-Mark2 Setup User ManualDocument65 pagesF-Mark2 Setup User ManualMaria FedaltoNo ratings yet

- Flight Vehicle LoadsDocument15 pagesFlight Vehicle LoadsSantosh G Pattanad100% (1)

- Comparative Evaluation of Antibacterial Efficacy.9Document6 pagesComparative Evaluation of Antibacterial Efficacy.9Shivani DubeyNo ratings yet

- Chandrayaan-2 Indias Second Lunar Exploration MisDocument16 pagesChandrayaan-2 Indias Second Lunar Exploration MisTanu SinghNo ratings yet

- 9 Quick Test: Grammar Tick ( ) A, B, or C To Complete The SentencesDocument3 pages9 Quick Test: Grammar Tick ( ) A, B, or C To Complete The SentencesMaria Guadalupe BedollaNo ratings yet

- B.Tech UG Project Ideas 4Document11 pagesB.Tech UG Project Ideas 4nambimunnaNo ratings yet

- Vegan Mayonnaise - Simple Vegan Blog PDFDocument2 pagesVegan Mayonnaise - Simple Vegan Blog PDFjkoiluNo ratings yet

- Name: - : InstructionsDocument8 pagesName: - : InstructionsAnushka YadavNo ratings yet

- Nanazoxid 0Document5 pagesNanazoxid 0hnn9gfqzqxNo ratings yet

- The Tell-Tale Heart by Edgar Allan PoeDocument9 pagesThe Tell-Tale Heart by Edgar Allan PoegicacosmaNo ratings yet

- Aem 499 Final Powerpoint Andrewdelili 4-28-2021Document20 pagesAem 499 Final Powerpoint Andrewdelili 4-28-2021api-548751501No ratings yet

- Ilmenite Mineral Data PDFDocument5 pagesIlmenite Mineral Data PDFNande Arcelia NaliniNo ratings yet

- Seasonal Variations in Kangra Tea QualityDocument6 pagesSeasonal Variations in Kangra Tea QualityashugulatiNo ratings yet

- Behind-The-Ear: Aries - Aries Pro 6 7 5 B T EDocument1 pageBehind-The-Ear: Aries - Aries Pro 6 7 5 B T Eanon_948155620No ratings yet

- DC SwitchgearDocument10 pagesDC SwitchgearpjchauhanNo ratings yet

- What Hetman Do I NeedDocument2 pagesWhat Hetman Do I NeedCem GüngörNo ratings yet

- Nerd Chef: Joshua Davidson's ResumeDocument2 pagesNerd Chef: Joshua Davidson's ResumejwdavidsonNo ratings yet