Download as pdf or txt

You might also like

- 9708 Specimen Paper Answers Paper 2 (For Examination From 2023)Document19 pages9708 Specimen Paper Answers Paper 2 (For Examination From 2023)Rabee Basit100% (1)

- Working Capital ManagementDocument95 pagesWorking Capital Managementabhishek11/85100% (1)

- 2015 A Levels H2 Paper 2 Essay Q5Document6 pages2015 A Levels H2 Paper 2 Essay Q5nasyrah100% (1)

- CFA Level 3 2012 Guideline AnswersDocument42 pagesCFA Level 3 2012 Guideline AnswersmerrylmorleyNo ratings yet

- 5-Aggregate Demand and Aggregate SupplyDocument58 pages5-Aggregate Demand and Aggregate SupplyThảo UyênNo ratings yet

- Conomics: The Influence of Monetary and Fiscal Policy On Aggregate DemandDocument48 pagesConomics: The Influence of Monetary and Fiscal Policy On Aggregate DemandWilsonNo ratings yet

- CH 34 Aggregate Demand and Aggregate Supply 10e - EditedDocument82 pagesCH 34 Aggregate Demand and Aggregate Supply 10e - Editeda24244573No ratings yet

- Part 5 - Chapter 33 Aggregate Demand and Aggregate SupplyDocument36 pagesPart 5 - Chapter 33 Aggregate Demand and Aggregate SupplyTHU DUONG MINHNo ratings yet

- Macro Ch7 Ch21 Presentation7eDocument65 pagesMacro Ch7 Ch21 Presentation7ek61.2211115124No ratings yet

- Macro Lecture08Document64 pagesMacro Lecture08Lê Văn KhánhNo ratings yet

- AS Level Economics Ch04Document5 pagesAS Level Economics Ch04taj qaiserNo ratings yet

- International Economics 8Th Edition Appleyard Solutions Manual Full Chapter PDFDocument34 pagesInternational Economics 8Th Edition Appleyard Solutions Manual Full Chapter PDFmargarita.hoffman902100% (22)

- International Economics 8th Edition Appleyard Solutions Manual 1Document13 pagesInternational Economics 8th Edition Appleyard Solutions Manual 1judith100% (51)

- Interactive CH 33 Aggregate Demand and Aggregate Supply 9eDocument60 pagesInteractive CH 33 Aggregate Demand and Aggregate Supply 9e文華暄No ratings yet

- ADAS Presentation UpdatedDocument43 pagesADAS Presentation UpdatedDivine GamingNo ratings yet

- Introduction To Economic Fluctuations Introduction To Economic FluctuationsDocument30 pagesIntroduction To Economic Fluctuations Introduction To Economic FluctuationsmekemomekemoNo ratings yet

- Aggregate Demand and Supply ReportDocument25 pagesAggregate Demand and Supply ReportAliyaaaahNo ratings yet

- Chapter 30 Money Growth and InflationDocument53 pagesChapter 30 Money Growth and InflationluluNo ratings yet

- Ch20 AD ASDocument58 pagesCh20 AD ASĐào Việt PhúcNo ratings yet

- Instant Download PDF Macroeconomics 9th Edition Boyes Solutions Manual Full ChapterDocument39 pagesInstant Download PDF Macroeconomics 9th Edition Boyes Solutions Manual Full Chaptertalibheyley6100% (5)

- Full Macroeconomics 9Th Edition Boyes Solutions Manual Online PDF All ChapterDocument39 pagesFull Macroeconomics 9Th Edition Boyes Solutions Manual Online PDF All Chapterstevenjordan961980100% (5)

- Multiplier Model Web Chapter Colander HgdAMRUlA2Document30 pagesMultiplier Model Web Chapter Colander HgdAMRUlA2Himanshu SethNo ratings yet

- Economics For BusinessDocument14 pagesEconomics For BusinessgodwinNo ratings yet

- Instant Download PDF Economics 12th Edition Arnold Solutions Manual Full ChapterDocument41 pagesInstant Download PDF Economics 12th Edition Arnold Solutions Manual Full Chapterjonnikdabol100% (4)

- Chapter1 PDFDocument45 pagesChapter1 PDFOruc MeherremliNo ratings yet

- EEC 11 2016 17 IgnouAssignmentGuru PDFDocument12 pagesEEC 11 2016 17 IgnouAssignmentGuru PDFAnonymous Pac475uSXNo ratings yet

- Chapter 33 Aggregate Demand and Aggregate SupplyDocument72 pagesChapter 33 Aggregate Demand and Aggregate SupplyVương VõNo ratings yet

- CHAP03Document58 pagesCHAP03anuska2037No ratings yet

- Lecture - CH 23Document60 pagesLecture - CH 23burucsgNo ratings yet

- Some Basic Concept of MacroeconomicsDocument3 pagesSome Basic Concept of Macroeconomicsharshit2714sharmaNo ratings yet

- Review PPT MakroekonomiDocument13 pagesReview PPT MakroekonomiSiti HumairahNo ratings yet

- Engineering Economy: Chapter 11: Breakeven and Sensitivity AnalysisDocument17 pagesEngineering Economy: Chapter 11: Breakeven and Sensitivity AnalysisKasturi LetchumananNo ratings yet

- Langdana, F. Macroeconomic Policy Demystifying Monetary and Fiscal Policy. Cap. 4Document26 pagesLangdana, F. Macroeconomic Policy Demystifying Monetary and Fiscal Policy. Cap. 4Flor MartinezNo ratings yet

- Chapter 1 - Macroeconomic OverviewDocument30 pagesChapter 1 - Macroeconomic OverviewFatin Arisha FarhahNo ratings yet

- CH 2 Economics QuestionsDocument106 pagesCH 2 Economics QuestionsAkshayNo ratings yet

- Aggregate Demand and Aggregate Supply: Week 10Document24 pagesAggregate Demand and Aggregate Supply: Week 10Dewi Ushriyah UlyaNo ratings yet

- PPC DolDocument7 pagesPPC DolabdullahkhanazeemNo ratings yet

- 1.ad As BasicDocument50 pages1.ad As BasicruhiNo ratings yet

- Macroeconomics: Introduction To Economic FluctuationsDocument40 pagesMacroeconomics: Introduction To Economic Fluctuationsnazia naziaNo ratings yet

- Session1 Introduction PDFDocument19 pagesSession1 Introduction PDFANJULI AGARWALNo ratings yet

- MSS231501Document9 pagesMSS231501Tariqul Islam TareqNo ratings yet

- Macroeconomics 9th Edition Boyes Solutions Manual Full Chapter PDFDocument37 pagesMacroeconomics 9th Edition Boyes Solutions Manual Full Chapter PDFcaibache0x60h100% (18)

- Macroeconomics 9th Edition Boyes Solutions ManualDocument16 pagesMacroeconomics 9th Edition Boyes Solutions Manualgrainnematthew7cr3xy100% (34)

- Virtual Instruction Lesson - 3.1 - 3-3-3.7 - ReviewDocument38 pagesVirtual Instruction Lesson - 3.1 - 3-3-3.7 - ReviewparminderpcsNo ratings yet

- 1324instant Download PDF Economics 11th Edition Arnold Solutions Manual Full ChapterDocument38 pages1324instant Download PDF Economics 11th Edition Arnold Solutions Manual Full Chaptersakalilailia100% (2)

- Chapter 20 Aggregate Demand and Aggregate SupplyDocument76 pagesChapter 20 Aggregate Demand and Aggregate Supplyyohana yNo ratings yet

- Virtual Instruction Lesson - 5.6 - Economic GrowthDocument32 pagesVirtual Instruction Lesson - 5.6 - Economic GrowthparminderpcsNo ratings yet

- Arnold - Econ12e - Ch06 Introduction To MacroeconomicDocument43 pagesArnold - Econ12e - Ch06 Introduction To MacroeconomicMartinChooNo ratings yet

- The Short-Run Trade-Off Between Inflation and UnemploymentDocument48 pagesThe Short-Run Trade-Off Between Inflation and UnemploymentVương VõNo ratings yet

- Principles of Economics, Chapter 31 - N.Gregory MankiwDocument49 pagesPrinciples of Economics, Chapter 31 - N.Gregory MankiwdilayNo ratings yet

- Fundamentals of Economics 6th Edition Boyes Solutions Manual DownloadDocument6 pagesFundamentals of Economics 6th Edition Boyes Solutions Manual DownloadLonnie Beck100% (27)

- Ch.9Document22 pagesCh.9Hokyee ChanNo ratings yet

- Business Confidence & Depression PreventionDocument8 pagesBusiness Confidence & Depression PreventionShriram DusaneNo ratings yet

- Microeconomics For Today 9th Edition Tucker Solutions ManualDocument8 pagesMicroeconomics For Today 9th Edition Tucker Solutions ManualGeorgePalmerkqgd100% (41)

- ReillyBrown CH 8 2019Document48 pagesReillyBrown CH 8 2019Aaron HoardNo ratings yet

- MBB3523 Macroeconomics - Topic 4Document60 pagesMBB3523 Macroeconomics - Topic 4bba22090030No ratings yet

- PDF Macroeconomics Principles Problems and Policies Mcconnell 20Th Edition Solutions Manual Online Ebook Full ChapterDocument21 pagesPDF Macroeconomics Principles Problems and Policies Mcconnell 20Th Edition Solutions Manual Online Ebook Full Chapterdouglas.lasley663100% (9)

- Full Economics For Today Asia Pacific 5Th Edition Layton Solutions Manual Online PDF All ChapterDocument31 pagesFull Economics For Today Asia Pacific 5Th Edition Layton Solutions Manual Online PDF All Chaptermauraanaviolat284100% (6)

- Financing and TariffDocument94 pagesFinancing and Tariffgaurang1111No ratings yet

- Lect 3 Part 1. The Econ of Prodn Cost and Profit MaximizationDocument17 pagesLect 3 Part 1. The Econ of Prodn Cost and Profit MaximizationkonchojNo ratings yet

- Economics 21st Edition McConnell Solutions Manual 1Document14 pagesEconomics 21st Edition McConnell Solutions Manual 1melissa100% (36)

- Lecture On Ch. 5 ElasticityDocument18 pagesLecture On Ch. 5 ElasticityCheyenne Megan Kohchet-ChuaNo ratings yet

- Chapter 17 OligopolyDocument47 pagesChapter 17 OligopolyabdkennantNo ratings yet

- Lecture 7 Ethical Issues in Human Resource ManagementDocument9 pagesLecture 7 Ethical Issues in Human Resource ManagementDevyansh GuptaNo ratings yet

- Lecture 6 Environment Act, 1986Document4 pagesLecture 6 Environment Act, 1986Devyansh GuptaNo ratings yet

- CSR - A Strategic Tool For BusinessDocument19 pagesCSR - A Strategic Tool For BusinessDevyansh GuptaNo ratings yet

- Unit 5Document20 pagesUnit 5Devyansh GuptaNo ratings yet

- Unit 2Document13 pagesUnit 2Devyansh GuptaNo ratings yet

- Scala NotesDocument71 pagesScala NotesDevyansh GuptaNo ratings yet

- Unit 1Document14 pagesUnit 1Devyansh GuptaNo ratings yet

- Lecture 2.2 (Risk and Return)Document33 pagesLecture 2.2 (Risk and Return)Devyansh GuptaNo ratings yet

- Indian Partnership ActDocument5 pagesIndian Partnership ActDevyansh GuptaNo ratings yet

- Lecture 0Document33 pagesLecture 0Devyansh GuptaNo ratings yet

- Lecture 8.2 (Capm and Apt)Document30 pagesLecture 8.2 (Capm and Apt)Devyansh GuptaNo ratings yet

- Unit 3Document17 pagesUnit 3Devyansh GuptaNo ratings yet

- Lecture 18 MGNM571Document33 pagesLecture 18 MGNM571Devyansh GuptaNo ratings yet

- Lecture 2.3 (Risk and Return)Document47 pagesLecture 2.3 (Risk and Return)Devyansh GuptaNo ratings yet

- What Is Ensemble LearningDocument4 pagesWhat Is Ensemble LearningDevyansh GuptaNo ratings yet

- Lecture 8.1 (Beta and CAPM)Document17 pagesLecture 8.1 (Beta and CAPM)Devyansh GuptaNo ratings yet

- Lecture 16 MGNM571Document14 pagesLecture 16 MGNM571Devyansh GuptaNo ratings yet

- Lecture 2.1 (Risk and Return)Document40 pagesLecture 2.1 (Risk and Return)Devyansh GuptaNo ratings yet

- Lecture 1 (Introduction To Security Analysis)Document44 pagesLecture 1 (Introduction To Security Analysis)Devyansh GuptaNo ratings yet

- Lecture 4 (Efficient Market Hypothesis)Document46 pagesLecture 4 (Efficient Market Hypothesis)Devyansh GuptaNo ratings yet

- Central TendencyDocument32 pagesCentral TendencyDevyansh GuptaNo ratings yet

- Lecture (Free Cash Flow Model - DDM)Document23 pagesLecture (Free Cash Flow Model - DDM)Devyansh GuptaNo ratings yet

- Unit 2 Measures of Central Tendency: Dr. Pooja Kansra Associate Professor Mittal School of BusinessDocument49 pagesUnit 2 Measures of Central Tendency: Dr. Pooja Kansra Associate Professor Mittal School of BusinessDevyansh GuptaNo ratings yet

- Lecture 1 Investment BankingDocument35 pagesLecture 1 Investment BankingDevyansh GuptaNo ratings yet

- Book Building: IPO Price Discovery MechanismDocument35 pagesBook Building: IPO Price Discovery MechanismDevyansh GuptaNo ratings yet

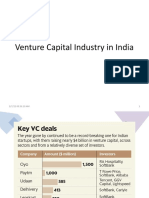

- Venture Capital Industry in IndiaDocument69 pagesVenture Capital Industry in IndiaDevyansh GuptaNo ratings yet

- Buy-Backs AND De-Listings: Unit 4Document48 pagesBuy-Backs AND De-Listings: Unit 4Devyansh GuptaNo ratings yet

- Lecture 4Document28 pagesLecture 4Devyansh GuptaNo ratings yet

- QTTM509 Research Methodology-I: What It's All About?Document30 pagesQTTM509 Research Methodology-I: What It's All About?Devyansh GuptaNo ratings yet

- Lecture 2 Investment Banking - The Emerging ChallengesDocument3 pagesLecture 2 Investment Banking - The Emerging ChallengesDevyansh GuptaNo ratings yet

- Basic Concept of Macro Economics: Unit 1Document31 pagesBasic Concept of Macro Economics: Unit 1Roxanne OsalboNo ratings yet

- Sociology Project: Madras School of Social WorkDocument10 pagesSociology Project: Madras School of Social WorkJananee RajagopalanNo ratings yet

- Parkinmacro5 1300Document16 pagesParkinmacro5 1300Mr. JahirNo ratings yet

- KondratievDocument4 pagesKondratievDavid BriggsNo ratings yet

- SubmitDocument266 pagesSubmitNitika GuptaNo ratings yet

- KitchinDocument8 pagesKitchinsport.kacperNo ratings yet

- Not All Oil Price Shocks Are Alike - Disentangling Demand and Supply Shocks in The Crude Oil Market (Lutz Kilian)Document22 pagesNot All Oil Price Shocks Are Alike - Disentangling Demand and Supply Shocks in The Crude Oil Market (Lutz Kilian)Andrés JiménezNo ratings yet

- The Federal Reserve - GarrisonDocument17 pagesThe Federal Reserve - Garrisontinman2009No ratings yet

- The Financial System: Opportunities and Dangers: Chapter 20 of Edition, by N. Gregory Mankiw ECO62Document97 pagesThe Financial System: Opportunities and Dangers: Chapter 20 of Edition, by N. Gregory Mankiw ECO62Usman FaruqueNo ratings yet

- Unit-Iii Fundamental AnalysisDocument36 pagesUnit-Iii Fundamental Analysisharesh KNo ratings yet

- Business Taxation MaterialDocument18 pagesBusiness Taxation MaterialKhushboo ParikhNo ratings yet

- 2023 Macroeconomics Final Test SampleDocument2 pages2023 Macroeconomics Final Test Samplek. nastyasNo ratings yet

- (Cambridge Studies in Comparative Politics) Carles Boix-Political Parties, Growth and Equality_ Conservative and Social Democratic Economic Strategies in the World Economy-Cambridge University Press (Document297 pages(Cambridge Studies in Comparative Politics) Carles Boix-Political Parties, Growth and Equality_ Conservative and Social Democratic Economic Strategies in the World Economy-Cambridge University Press (Reza R. W. Tehusalawany100% (1)

- Unit - 1 KMBN-102 Managerial EconomicsDocument22 pagesUnit - 1 KMBN-102 Managerial EconomicsAnshitaNo ratings yet

- C-5 BlockDocument22 pagesC-5 BlockM Bilal KhattakNo ratings yet

- Module 2 The Philippine Economy and Its 21st Century Socioeconomic ChallengesDocument34 pagesModule 2 The Philippine Economy and Its 21st Century Socioeconomic ChallengesAlvin OroscoNo ratings yet

- Definition of EconomicsDocument16 pagesDefinition of EconomicsAadityaVasuNo ratings yet

- Alchian InflationDocument20 pagesAlchian InflationIvan JankovicNo ratings yet

- Thesis - Mkhululi NcubeDocument64 pagesThesis - Mkhululi NcubeKamran AbdullahNo ratings yet

- PGDM 22 24 MacroeconomicsDocument11 pagesPGDM 22 24 MacroeconomicsAnimesh Verma-1 8 3 0 1No ratings yet

- Macro Syllabus Fall12Document5 pagesMacro Syllabus Fall12bofwNo ratings yet

- Real Estate & Construction Market Research in IndiaDocument7 pagesReal Estate & Construction Market Research in IndiaSatheeshDisousaNo ratings yet

- End of Unit Test 1 (70 Minutes) : SECTION 1: Vocabulary and Structure (30 Marks, 1 Mark/answer)Document18 pagesEnd of Unit Test 1 (70 Minutes) : SECTION 1: Vocabulary and Structure (30 Marks, 1 Mark/answer)Tnt0102No ratings yet

- Economics Placement Preparation MaterialDocument17 pagesEconomics Placement Preparation MaterialTopsy KreateNo ratings yet

- Macroeconomics 214: Introductory LectureDocument28 pagesMacroeconomics 214: Introductory LectureLiezl NieuwoudtNo ratings yet

- Grade 12 Term 1 RevisionDocument17 pagesGrade 12 Term 1 Revisionthabileshab08No ratings yet