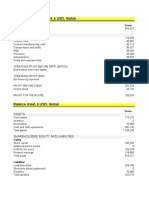

Boa Financials For q3 30 Sept. 2021

Boa Financials For q3 30 Sept. 2021

You might also like

- World's Best SME Banks 2024-Regional Winners - Global Finance MagazineDocument9 pagesWorld's Best SME Banks 2024-Regional Winners - Global Finance MagazinebisnisdigitalNo ratings yet

- Advanced Accounting Guerrero Peralta Volume 1 Solution Manual PDFDocument190 pagesAdvanced Accounting Guerrero Peralta Volume 1 Solution Manual PDFErica Daprosa50% (2)

- Instant Download Ebook PDF Financial Accounting 10th Australian Edition PDF ScribdDocument41 pagesInstant Download Ebook PDF Financial Accounting 10th Australian Edition PDF Scribdmarian.hillis984100% (47)

- NAD 2019-2020 Annual ReportDocument1 pageNAD 2019-2020 Annual ReportNational Association of the DeafNo ratings yet

- ACCN 304 Revision QuestionsDocument11 pagesACCN 304 Revision Questionskelvinmunashenyamutumba100% (1)

- Anual Report CscecDocument303 pagesAnual Report CscecsachithNo ratings yet

- Arabtec FSDocument46 pagesArabtec FSShakib ApNo ratings yet

- Montefiore Health System 2019 Financial StatementsDocument27 pagesMontefiore Health System 2019 Financial StatementsJonathan LaMantiaNo ratings yet

- Internal Audit Self Assessment GuideDocument32 pagesInternal Audit Self Assessment GuideLilith LunaNo ratings yet

- Financial Publication MarchDocument2 pagesFinancial Publication MarchFuaad DodooNo ratings yet

- PSO StatementDocument1 pagePSO StatementNaseeb Ullah TareenNo ratings yet

- 7-E Fin Statement 2022Document4 pages7-E Fin Statement 20222021892056No ratings yet

- Psaf Revision Day 3 May 2023Document8 pagesPsaf Revision Day 3 May 2023Esther AkpanNo ratings yet

- Arab Bank Ir Presentation q4 2023Document30 pagesArab Bank Ir Presentation q4 2023tl3tNo ratings yet

- QFB Fact SheetDocument2 pagesQFB Fact SheetRianovel MareNo ratings yet

- The Arab Bank - Governance and Ethics - FINALDocument26 pagesThe Arab Bank - Governance and Ethics - FINALHum92reNo ratings yet

- 71465exam57501 p1Document32 pages71465exam57501 p1ManaliNo ratings yet

- q1 Ifrs Usd Earnings ReleaseDocument26 pagesq1 Ifrs Usd Earnings Releaseashokdb2kNo ratings yet

- Sail Annual Report - 2022.inddDocument11 pagesSail Annual Report - 2022.inddSandeep SharmaNo ratings yet

- Montefiore Health System Q3 2019 Financial StatementsDocument25 pagesMontefiore Health System Q3 2019 Financial StatementsJonathan LaMantiaNo ratings yet

- Baniya Kirana Stores F.Y. 2074-75 TaxDocument17 pagesBaniya Kirana Stores F.Y. 2074-75 TaxasasasNo ratings yet

- Eicher Motors BSDocument2 pagesEicher Motors BSVaishnav SunilNo ratings yet

- GCB-Q3 2023 - Interim - ReportDocument16 pagesGCB-Q3 2023 - Interim - ReportGan ZhiHanNo ratings yet

- ITC Balance Sheet PDFDocument1 pageITC Balance Sheet PDFKeran VarmaNo ratings yet

- 1st Qtr.2021 ReportDocument31 pages1st Qtr.2021 ReportMurad HasanNo ratings yet

- Opensys An20200518a2 1Document17 pagesOpensys An20200518a2 1Nor FarizalNo ratings yet

- PhoenixSolar-Annual Report 2015Document152 pagesPhoenixSolar-Annual Report 2015Alex MartayanNo ratings yet

- Balance Sheet: Share Capital and ReservesDocument42 pagesBalance Sheet: Share Capital and ReservesaaliaccaNo ratings yet

- 23MB0026 FAR AssignmentDocument14 pages23MB0026 FAR Assignmenthimanshu011623No ratings yet

- Results r01Document28 pagesResults r01Antony Ramiro Gutierrez RiosNo ratings yet

- 8 MIS November 2012Document129 pages8 MIS November 2012kr__santoshNo ratings yet

- MS Brothers Super Rice MillDocument9 pagesMS Brothers Super Rice MillMasud Ahmed khan100% (1)

- The Group AssetsDocument46 pagesThe Group Assetsit4728No ratings yet

- Financial Statements - Standalone and ConsolidatedDocument182 pagesFinancial Statements - Standalone and ConsolidatedPranav AdityaNo ratings yet

- Statement of Assets and Liabilities - H1 2018-19 8Document1 pageStatement of Assets and Liabilities - H1 2018-19 8saichakrapani3807No ratings yet

- Ezz Steel Ratio Analysis - Fall21Document10 pagesEzz Steel Ratio Analysis - Fall21farahNo ratings yet

- Financial ReportsDocument14 pagesFinancial Reportssardar amanat aliHadian00rNo ratings yet

- Lii Hen - Q1 (2017) 1Document15 pagesLii Hen - Q1 (2017) 1Jordan YiiNo ratings yet

- Bac 3 Review QNSDocument16 pagesBac 3 Review QNSsaidkhatib368No ratings yet

- Annual-Report-FML-30-June-2020 Vol 1Document1 pageAnnual-Report-FML-30-June-2020 Vol 1Bluish FlameNo ratings yet

- Hindalco Industries Balance Sheet, Hindalco Industries Financial Statement & AccountsDocument3 pagesHindalco Industries Balance Sheet, Hindalco Industries Financial Statement & AccountsSharon T100% (1)

- FinancialsDocument26 pagesFinancials崔梦炎No ratings yet

- FF 2011 enDocument55 pagesFF 2011 enWang Hon YuenNo ratings yet

- Balance Sheet As at March 31, 2020: Property, Plant and EquipmentDocument8 pagesBalance Sheet As at March 31, 2020: Property, Plant and Equipmentishwaryaishu0708No ratings yet

- Profit and Loss TableDocument3 pagesProfit and Loss Table龍徤No ratings yet

- Careplus Group Berhad: Unaudited Condensed Consolidated Statements of Comprehensive IncomeDocument21 pagesCareplus Group Berhad: Unaudited Condensed Consolidated Statements of Comprehensive IncomethamNo ratings yet

- Financial AnalysisDocument15 pagesFinancial AnalysisLiza KhanNo ratings yet

- JHM 1Qtr21 Financial Report (Amendment)Document13 pagesJHM 1Qtr21 Financial Report (Amendment)Ooi Gim SengNo ratings yet

- LSH Financial ReportDocument12 pagesLSH Financial ReportJohnny TehNo ratings yet

- Quarterly Report 20160331Document17 pagesQuarterly Report 20160331Ang SHNo ratings yet

- Aknight Quarter Report-Sept 2012Document8 pagesAknight Quarter Report-Sept 2012James WarrenNo ratings yet

- MDGH 2021 HY Consolidated Financial StatementsDocument39 pagesMDGH 2021 HY Consolidated Financial StatementsMmatos InvestimentosNo ratings yet

- SIB Result Q1 2024 FinalDocument24 pagesSIB Result Q1 2024 Finalseeme55runNo ratings yet

- Raymond Limited Financial StatementsDocument85 pagesRaymond Limited Financial StatementsVinay KukrejaNo ratings yet

- UCrest Bhd-Q4 Financial Result Ended 31.5.2022Document8 pagesUCrest Bhd-Q4 Financial Result Ended 31.5.2022Jeff WongNo ratings yet

- ZTBL 2008Document62 pagesZTBL 2008Mahmood KhanNo ratings yet

- Unaudited Financial Results 30.06.2021 1Document11 pagesUnaudited Financial Results 30.06.2021 1Kartik AroraNo ratings yet

- Profit and Loss Statement 31.12.20Document1 pageProfit and Loss Statement 31.12.20Si HadiNo ratings yet

- Consolidated Balance Sheet: Asat31 March, 2021 All Amounts Are in H Crores, Unless Otherwise StatedDocument7 pagesConsolidated Balance Sheet: Asat31 March, 2021 All Amounts Are in H Crores, Unless Otherwise StateddevrishabhNo ratings yet

- SUBEXLTD 20062022131358 QuickResultsDocument23 pagesSUBEXLTD 20062022131358 QuickResultsSocial OnlyNo ratings yet

- Q3 Interim Condensed Consolidated FS 2019Document8 pagesQ3 Interim Condensed Consolidated FS 2019FaizanSulNo ratings yet

- New Model of NetflixDocument17 pagesNew Model of NetflixPencil ArtistNo ratings yet

- UBA - June2021 FN StatementsDocument2 pagesUBA - June2021 FN StatementsFuaad DodooNo ratings yet

- 19th Edition of The Ghana Club 100 Rankings OutcomeDocument3 pages19th Edition of The Ghana Club 100 Rankings OutcomeFuaad DodooNo ratings yet

- Daily Equity Market Report - 18.10.2022Document1 pageDaily Equity Market Report - 18.10.2022Fuaad DodooNo ratings yet

- Daily Equity Market Report - 17.10.2022Document1 pageDaily Equity Market Report - 17.10.2022Fuaad DodooNo ratings yet

- Press Release 2Document1 pagePress Release 2Fuaad DodooNo ratings yet

- Daily Equity Market Report - 05.10.2022Document1 pageDaily Equity Market Report - 05.10.2022Fuaad DodooNo ratings yet

- Weekly Capital Market Report - Week Ending 14.10.2022Document2 pagesWeekly Capital Market Report - Week Ending 14.10.2022Fuaad DodooNo ratings yet

- Weekly Capital Market Report - Week Ending 07.10.2022Document2 pagesWeekly Capital Market Report - Week Ending 07.10.2022Fuaad DodooNo ratings yet

- Daily Equity Market Report - 11.10.2022Document1 pageDaily Equity Market Report - 11.10.2022Fuaad DodooNo ratings yet

- Daily Equity Market Report - 06.10.2022Document1 pageDaily Equity Market Report - 06.10.2022Fuaad DodooNo ratings yet

- Substandard (Contaminated) Paediatric Medicines Identified in WHODocument4 pagesSubstandard (Contaminated) Paediatric Medicines Identified in WHOFuaad DodooNo ratings yet

- Regulatory Order To ECG - 221004 - 180752Document6 pagesRegulatory Order To ECG - 221004 - 180752Fuaad DodooNo ratings yet

- Fixed Income Market Report - 10.10.2022Document1 pageFixed Income Market Report - 10.10.2022Fuaad DodooNo ratings yet

- R9 News Release Gender Inequalities Persist in Ghana Afrobarometer BH MA 4oct22Document4 pagesR9 News Release Gender Inequalities Persist in Ghana Afrobarometer BH MA 4oct22Fuaad DodooNo ratings yet

- Press ReleaseDocument1 pagePress ReleaseFuaad DodooNo ratings yet

- Daily Equity Market Report - 29.09.2022Document1 pageDaily Equity Market Report - 29.09.2022Fuaad DodooNo ratings yet

- Daily Equity Market Report 03.10.2022 2022-10-03Document1 pageDaily Equity Market Report 03.10.2022 2022-10-03Fuaad DodooNo ratings yet

- Weekly Capital Market Report - Week Ending 30.09.2022Document2 pagesWeekly Capital Market Report - Week Ending 30.09.2022Fuaad DodooNo ratings yet

- Fixed Income Market Report - 03.10.2022Document1 pageFixed Income Market Report - 03.10.2022Fuaad DodooNo ratings yet

- Daily Equity Market Report - 28.09.2022Document1 pageDaily Equity Market Report - 28.09.2022Fuaad DodooNo ratings yet

- Daily Equity Market Report - 04.10.2022Document1 pageDaily Equity Market Report - 04.10.2022Fuaad DodooNo ratings yet

- Daily Equity Market Report - 22.09.2022Document1 pageDaily Equity Market Report - 22.09.2022Fuaad DodooNo ratings yet

- Daily Equity Market Report - 27.09.2022Document1 pageDaily Equity Market Report - 27.09.2022Fuaad DodooNo ratings yet

- Imf MeetingDocument1 pageImf MeetingFuaad DodooNo ratings yet

- Daily Equity Market Report 20.09.2022 2022-09-20Document1 pageDaily Equity Market Report 20.09.2022 2022-09-20Fuaad DodooNo ratings yet

- Weekly Capital Market Report - Week Ending 23.09.2022Document2 pagesWeekly Capital Market Report - Week Ending 23.09.2022Fuaad DodooNo ratings yet

- Fixed Income Market Report - 26.09.2022Document1 pageFixed Income Market Report - 26.09.2022Fuaad DodooNo ratings yet

- Nimed Financial Market Review (16.09.2022)Document4 pagesNimed Financial Market Review (16.09.2022)Fuaad DodooNo ratings yet

- Daily Equity Market Report - 26.09.2022Document1 pageDaily Equity Market Report - 26.09.2022Fuaad DodooNo ratings yet

- Auctresults 1817Document1 pageAuctresults 1817Fuaad DodooNo ratings yet

- Daily Equity Market Report - 19.09.2022Document1 pageDaily Equity Market Report - 19.09.2022Fuaad DodooNo ratings yet

- John Berendt - Destination UnknownDocument10 pagesJohn Berendt - Destination UnknownaddunsireNo ratings yet

- Financial Accounting and Reporting Notes PDFDocument232 pagesFinancial Accounting and Reporting Notes PDFsmlingwa75% (4)

- Advanced Financial Accounting QuizDocument53 pagesAdvanced Financial Accounting Quizanon nimusNo ratings yet

- Working Capital ManagementDocument59 pagesWorking Capital ManagementkeerthiNo ratings yet

- Finance FunctionDocument25 pagesFinance FunctionKane0% (1)

- Acc Topic 7Document7 pagesAcc Topic 7BM10622P Nur Alyaa Nadhirah Bt Mohd RosliNo ratings yet

- CE On Quasi-ReorganizationDocument1 pageCE On Quasi-ReorganizationalyssaNo ratings yet

- Tallu Spinning Mills: Particulars 2009 2010 2011 2012 2013Document109 pagesTallu Spinning Mills: Particulars 2009 2010 2011 2012 2013Shovon MustaryNo ratings yet

- Monarch Industries DPR TakeoverDocument23 pagesMonarch Industries DPR TakeoverJAWED MOHAMMADNo ratings yet

- Not Configuration in SAPDocument6 pagesNot Configuration in SAPVenkat Ram NarasimhaNo ratings yet

- Balance Sheet: (Company Name)Document2 pagesBalance Sheet: (Company Name)Bleep NewsNo ratings yet

- NEW MFRS 116 Property, Plant and EquipmentDocument53 pagesNEW MFRS 116 Property, Plant and EquipmentUmairah HusnaNo ratings yet

- LB 2013-2014 Standardized Statements MinervaDocument9 pagesLB 2013-2014 Standardized Statements MinervaArmand HajdarajNo ratings yet

- Final Project Financial ManagementDocument10 pagesFinal Project Financial ManagementMaryam SaeedNo ratings yet

- 1stLecture-Partnership LiquidationDocument25 pages1stLecture-Partnership LiquidationRechelle Dalusung100% (1)

- Santoshi Patil Pattan 11Document60 pagesSantoshi Patil Pattan 11balaji xeroxNo ratings yet

- BKDP - Annual Report - 2017 PDFDocument119 pagesBKDP - Annual Report - 2017 PDFAmbo DalleNo ratings yet

- Financialmanagementworkbook 121105064928 Phpapp01Document881 pagesFinancialmanagementworkbook 121105064928 Phpapp01sunnysainani1No ratings yet

- Annual Report Analysis - Oct-14-EDEL PDFDocument259 pagesAnnual Report Analysis - Oct-14-EDEL PDFhiteshaNo ratings yet

- Project ReportDocument9 pagesProject ReportYod8 TdpNo ratings yet

- W2 - Key Tutorial 3Document5 pagesW2 - Key Tutorial 3Rules of Survival MALAYSIANo ratings yet

- Financial Accounting September 2012 Marks Plan ICAEWDocument14 pagesFinancial Accounting September 2012 Marks Plan ICAEWMuhammad Ziaul HaqueNo ratings yet

- SIM ACC 226ACCE 411 Week 4 To 5 COPY 1Document31 pagesSIM ACC 226ACCE 411 Week 4 To 5 COPY 1Mireya Yue100% (1)

- ACTG115 - Ch02 SolutionsDocument16 pagesACTG115 - Ch02 SolutionsxxmbetaNo ratings yet

- 12 Igcse - Accounting - Ratios - Unlocked PDFDocument47 pages12 Igcse - Accounting - Ratios - Unlocked PDFshivom talrejaNo ratings yet

- 4th Sem BBA Industrial ProjectDocument60 pages4th Sem BBA Industrial Projectαβђเکђ€к ηєσgเ67% (12)

- Account Formats and Statements LayoutsDocument5 pagesAccount Formats and Statements LayoutsCynNo ratings yet

Download as pdf or txt

You might also like

- World's Best SME Banks 2024-Regional Winners - Global Finance MagazineDocument9 pagesWorld's Best SME Banks 2024-Regional Winners - Global Finance MagazinebisnisdigitalNo ratings yet

- Advanced Accounting Guerrero Peralta Volume 1 Solution Manual PDFDocument190 pagesAdvanced Accounting Guerrero Peralta Volume 1 Solution Manual PDFErica Daprosa50% (2)

- Instant Download Ebook PDF Financial Accounting 10th Australian Edition PDF ScribdDocument41 pagesInstant Download Ebook PDF Financial Accounting 10th Australian Edition PDF Scribdmarian.hillis984100% (47)

- NAD 2019-2020 Annual ReportDocument1 pageNAD 2019-2020 Annual ReportNational Association of the DeafNo ratings yet

- ACCN 304 Revision QuestionsDocument11 pagesACCN 304 Revision Questionskelvinmunashenyamutumba100% (1)

- Anual Report CscecDocument303 pagesAnual Report CscecsachithNo ratings yet

- Arabtec FSDocument46 pagesArabtec FSShakib ApNo ratings yet

- Montefiore Health System 2019 Financial StatementsDocument27 pagesMontefiore Health System 2019 Financial StatementsJonathan LaMantiaNo ratings yet

- Internal Audit Self Assessment GuideDocument32 pagesInternal Audit Self Assessment GuideLilith LunaNo ratings yet

- Financial Publication MarchDocument2 pagesFinancial Publication MarchFuaad DodooNo ratings yet

- PSO StatementDocument1 pagePSO StatementNaseeb Ullah TareenNo ratings yet

- 7-E Fin Statement 2022Document4 pages7-E Fin Statement 20222021892056No ratings yet

- Psaf Revision Day 3 May 2023Document8 pagesPsaf Revision Day 3 May 2023Esther AkpanNo ratings yet

- Arab Bank Ir Presentation q4 2023Document30 pagesArab Bank Ir Presentation q4 2023tl3tNo ratings yet

- QFB Fact SheetDocument2 pagesQFB Fact SheetRianovel MareNo ratings yet

- The Arab Bank - Governance and Ethics - FINALDocument26 pagesThe Arab Bank - Governance and Ethics - FINALHum92reNo ratings yet

- 71465exam57501 p1Document32 pages71465exam57501 p1ManaliNo ratings yet

- q1 Ifrs Usd Earnings ReleaseDocument26 pagesq1 Ifrs Usd Earnings Releaseashokdb2kNo ratings yet

- Sail Annual Report - 2022.inddDocument11 pagesSail Annual Report - 2022.inddSandeep SharmaNo ratings yet

- Montefiore Health System Q3 2019 Financial StatementsDocument25 pagesMontefiore Health System Q3 2019 Financial StatementsJonathan LaMantiaNo ratings yet

- Baniya Kirana Stores F.Y. 2074-75 TaxDocument17 pagesBaniya Kirana Stores F.Y. 2074-75 TaxasasasNo ratings yet

- Eicher Motors BSDocument2 pagesEicher Motors BSVaishnav SunilNo ratings yet

- GCB-Q3 2023 - Interim - ReportDocument16 pagesGCB-Q3 2023 - Interim - ReportGan ZhiHanNo ratings yet

- ITC Balance Sheet PDFDocument1 pageITC Balance Sheet PDFKeran VarmaNo ratings yet

- 1st Qtr.2021 ReportDocument31 pages1st Qtr.2021 ReportMurad HasanNo ratings yet

- Opensys An20200518a2 1Document17 pagesOpensys An20200518a2 1Nor FarizalNo ratings yet

- PhoenixSolar-Annual Report 2015Document152 pagesPhoenixSolar-Annual Report 2015Alex MartayanNo ratings yet

- Balance Sheet: Share Capital and ReservesDocument42 pagesBalance Sheet: Share Capital and ReservesaaliaccaNo ratings yet

- 23MB0026 FAR AssignmentDocument14 pages23MB0026 FAR Assignmenthimanshu011623No ratings yet

- Results r01Document28 pagesResults r01Antony Ramiro Gutierrez RiosNo ratings yet

- 8 MIS November 2012Document129 pages8 MIS November 2012kr__santoshNo ratings yet

- MS Brothers Super Rice MillDocument9 pagesMS Brothers Super Rice MillMasud Ahmed khan100% (1)

- The Group AssetsDocument46 pagesThe Group Assetsit4728No ratings yet

- Financial Statements - Standalone and ConsolidatedDocument182 pagesFinancial Statements - Standalone and ConsolidatedPranav AdityaNo ratings yet

- Statement of Assets and Liabilities - H1 2018-19 8Document1 pageStatement of Assets and Liabilities - H1 2018-19 8saichakrapani3807No ratings yet

- Ezz Steel Ratio Analysis - Fall21Document10 pagesEzz Steel Ratio Analysis - Fall21farahNo ratings yet

- Financial ReportsDocument14 pagesFinancial Reportssardar amanat aliHadian00rNo ratings yet

- Lii Hen - Q1 (2017) 1Document15 pagesLii Hen - Q1 (2017) 1Jordan YiiNo ratings yet

- Bac 3 Review QNSDocument16 pagesBac 3 Review QNSsaidkhatib368No ratings yet

- Annual-Report-FML-30-June-2020 Vol 1Document1 pageAnnual-Report-FML-30-June-2020 Vol 1Bluish FlameNo ratings yet

- Hindalco Industries Balance Sheet, Hindalco Industries Financial Statement & AccountsDocument3 pagesHindalco Industries Balance Sheet, Hindalco Industries Financial Statement & AccountsSharon T100% (1)

- FinancialsDocument26 pagesFinancials崔梦炎No ratings yet

- FF 2011 enDocument55 pagesFF 2011 enWang Hon YuenNo ratings yet

- Balance Sheet As at March 31, 2020: Property, Plant and EquipmentDocument8 pagesBalance Sheet As at March 31, 2020: Property, Plant and Equipmentishwaryaishu0708No ratings yet

- Profit and Loss TableDocument3 pagesProfit and Loss Table龍徤No ratings yet

- Careplus Group Berhad: Unaudited Condensed Consolidated Statements of Comprehensive IncomeDocument21 pagesCareplus Group Berhad: Unaudited Condensed Consolidated Statements of Comprehensive IncomethamNo ratings yet

- Financial AnalysisDocument15 pagesFinancial AnalysisLiza KhanNo ratings yet

- JHM 1Qtr21 Financial Report (Amendment)Document13 pagesJHM 1Qtr21 Financial Report (Amendment)Ooi Gim SengNo ratings yet

- LSH Financial ReportDocument12 pagesLSH Financial ReportJohnny TehNo ratings yet

- Quarterly Report 20160331Document17 pagesQuarterly Report 20160331Ang SHNo ratings yet

- Aknight Quarter Report-Sept 2012Document8 pagesAknight Quarter Report-Sept 2012James WarrenNo ratings yet

- MDGH 2021 HY Consolidated Financial StatementsDocument39 pagesMDGH 2021 HY Consolidated Financial StatementsMmatos InvestimentosNo ratings yet

- SIB Result Q1 2024 FinalDocument24 pagesSIB Result Q1 2024 Finalseeme55runNo ratings yet

- Raymond Limited Financial StatementsDocument85 pagesRaymond Limited Financial StatementsVinay KukrejaNo ratings yet

- UCrest Bhd-Q4 Financial Result Ended 31.5.2022Document8 pagesUCrest Bhd-Q4 Financial Result Ended 31.5.2022Jeff WongNo ratings yet

- ZTBL 2008Document62 pagesZTBL 2008Mahmood KhanNo ratings yet

- Unaudited Financial Results 30.06.2021 1Document11 pagesUnaudited Financial Results 30.06.2021 1Kartik AroraNo ratings yet

- Profit and Loss Statement 31.12.20Document1 pageProfit and Loss Statement 31.12.20Si HadiNo ratings yet

- Consolidated Balance Sheet: Asat31 March, 2021 All Amounts Are in H Crores, Unless Otherwise StatedDocument7 pagesConsolidated Balance Sheet: Asat31 March, 2021 All Amounts Are in H Crores, Unless Otherwise StateddevrishabhNo ratings yet

- SUBEXLTD 20062022131358 QuickResultsDocument23 pagesSUBEXLTD 20062022131358 QuickResultsSocial OnlyNo ratings yet

- Q3 Interim Condensed Consolidated FS 2019Document8 pagesQ3 Interim Condensed Consolidated FS 2019FaizanSulNo ratings yet

- New Model of NetflixDocument17 pagesNew Model of NetflixPencil ArtistNo ratings yet

- UBA - June2021 FN StatementsDocument2 pagesUBA - June2021 FN StatementsFuaad DodooNo ratings yet

- 19th Edition of The Ghana Club 100 Rankings OutcomeDocument3 pages19th Edition of The Ghana Club 100 Rankings OutcomeFuaad DodooNo ratings yet

- Daily Equity Market Report - 18.10.2022Document1 pageDaily Equity Market Report - 18.10.2022Fuaad DodooNo ratings yet

- Daily Equity Market Report - 17.10.2022Document1 pageDaily Equity Market Report - 17.10.2022Fuaad DodooNo ratings yet

- Press Release 2Document1 pagePress Release 2Fuaad DodooNo ratings yet

- Daily Equity Market Report - 05.10.2022Document1 pageDaily Equity Market Report - 05.10.2022Fuaad DodooNo ratings yet

- Weekly Capital Market Report - Week Ending 14.10.2022Document2 pagesWeekly Capital Market Report - Week Ending 14.10.2022Fuaad DodooNo ratings yet

- Weekly Capital Market Report - Week Ending 07.10.2022Document2 pagesWeekly Capital Market Report - Week Ending 07.10.2022Fuaad DodooNo ratings yet

- Daily Equity Market Report - 11.10.2022Document1 pageDaily Equity Market Report - 11.10.2022Fuaad DodooNo ratings yet

- Daily Equity Market Report - 06.10.2022Document1 pageDaily Equity Market Report - 06.10.2022Fuaad DodooNo ratings yet

- Substandard (Contaminated) Paediatric Medicines Identified in WHODocument4 pagesSubstandard (Contaminated) Paediatric Medicines Identified in WHOFuaad DodooNo ratings yet

- Regulatory Order To ECG - 221004 - 180752Document6 pagesRegulatory Order To ECG - 221004 - 180752Fuaad DodooNo ratings yet

- Fixed Income Market Report - 10.10.2022Document1 pageFixed Income Market Report - 10.10.2022Fuaad DodooNo ratings yet

- R9 News Release Gender Inequalities Persist in Ghana Afrobarometer BH MA 4oct22Document4 pagesR9 News Release Gender Inequalities Persist in Ghana Afrobarometer BH MA 4oct22Fuaad DodooNo ratings yet

- Press ReleaseDocument1 pagePress ReleaseFuaad DodooNo ratings yet

- Daily Equity Market Report - 29.09.2022Document1 pageDaily Equity Market Report - 29.09.2022Fuaad DodooNo ratings yet

- Daily Equity Market Report 03.10.2022 2022-10-03Document1 pageDaily Equity Market Report 03.10.2022 2022-10-03Fuaad DodooNo ratings yet

- Weekly Capital Market Report - Week Ending 30.09.2022Document2 pagesWeekly Capital Market Report - Week Ending 30.09.2022Fuaad DodooNo ratings yet

- Fixed Income Market Report - 03.10.2022Document1 pageFixed Income Market Report - 03.10.2022Fuaad DodooNo ratings yet

- Daily Equity Market Report - 28.09.2022Document1 pageDaily Equity Market Report - 28.09.2022Fuaad DodooNo ratings yet

- Daily Equity Market Report - 04.10.2022Document1 pageDaily Equity Market Report - 04.10.2022Fuaad DodooNo ratings yet

- Daily Equity Market Report - 22.09.2022Document1 pageDaily Equity Market Report - 22.09.2022Fuaad DodooNo ratings yet

- Daily Equity Market Report - 27.09.2022Document1 pageDaily Equity Market Report - 27.09.2022Fuaad DodooNo ratings yet

- Imf MeetingDocument1 pageImf MeetingFuaad DodooNo ratings yet

- Daily Equity Market Report 20.09.2022 2022-09-20Document1 pageDaily Equity Market Report 20.09.2022 2022-09-20Fuaad DodooNo ratings yet

- Weekly Capital Market Report - Week Ending 23.09.2022Document2 pagesWeekly Capital Market Report - Week Ending 23.09.2022Fuaad DodooNo ratings yet

- Fixed Income Market Report - 26.09.2022Document1 pageFixed Income Market Report - 26.09.2022Fuaad DodooNo ratings yet

- Nimed Financial Market Review (16.09.2022)Document4 pagesNimed Financial Market Review (16.09.2022)Fuaad DodooNo ratings yet

- Daily Equity Market Report - 26.09.2022Document1 pageDaily Equity Market Report - 26.09.2022Fuaad DodooNo ratings yet

- Auctresults 1817Document1 pageAuctresults 1817Fuaad DodooNo ratings yet

- Daily Equity Market Report - 19.09.2022Document1 pageDaily Equity Market Report - 19.09.2022Fuaad DodooNo ratings yet

- John Berendt - Destination UnknownDocument10 pagesJohn Berendt - Destination UnknownaddunsireNo ratings yet

- Financial Accounting and Reporting Notes PDFDocument232 pagesFinancial Accounting and Reporting Notes PDFsmlingwa75% (4)

- Advanced Financial Accounting QuizDocument53 pagesAdvanced Financial Accounting Quizanon nimusNo ratings yet

- Working Capital ManagementDocument59 pagesWorking Capital ManagementkeerthiNo ratings yet

- Finance FunctionDocument25 pagesFinance FunctionKane0% (1)

- Acc Topic 7Document7 pagesAcc Topic 7BM10622P Nur Alyaa Nadhirah Bt Mohd RosliNo ratings yet

- CE On Quasi-ReorganizationDocument1 pageCE On Quasi-ReorganizationalyssaNo ratings yet

- Tallu Spinning Mills: Particulars 2009 2010 2011 2012 2013Document109 pagesTallu Spinning Mills: Particulars 2009 2010 2011 2012 2013Shovon MustaryNo ratings yet

- Monarch Industries DPR TakeoverDocument23 pagesMonarch Industries DPR TakeoverJAWED MOHAMMADNo ratings yet

- Not Configuration in SAPDocument6 pagesNot Configuration in SAPVenkat Ram NarasimhaNo ratings yet

- Balance Sheet: (Company Name)Document2 pagesBalance Sheet: (Company Name)Bleep NewsNo ratings yet

- NEW MFRS 116 Property, Plant and EquipmentDocument53 pagesNEW MFRS 116 Property, Plant and EquipmentUmairah HusnaNo ratings yet

- LB 2013-2014 Standardized Statements MinervaDocument9 pagesLB 2013-2014 Standardized Statements MinervaArmand HajdarajNo ratings yet

- Final Project Financial ManagementDocument10 pagesFinal Project Financial ManagementMaryam SaeedNo ratings yet

- 1stLecture-Partnership LiquidationDocument25 pages1stLecture-Partnership LiquidationRechelle Dalusung100% (1)

- Santoshi Patil Pattan 11Document60 pagesSantoshi Patil Pattan 11balaji xeroxNo ratings yet

- BKDP - Annual Report - 2017 PDFDocument119 pagesBKDP - Annual Report - 2017 PDFAmbo DalleNo ratings yet

- Financialmanagementworkbook 121105064928 Phpapp01Document881 pagesFinancialmanagementworkbook 121105064928 Phpapp01sunnysainani1No ratings yet

- Annual Report Analysis - Oct-14-EDEL PDFDocument259 pagesAnnual Report Analysis - Oct-14-EDEL PDFhiteshaNo ratings yet

- Project ReportDocument9 pagesProject ReportYod8 TdpNo ratings yet

- W2 - Key Tutorial 3Document5 pagesW2 - Key Tutorial 3Rules of Survival MALAYSIANo ratings yet

- Financial Accounting September 2012 Marks Plan ICAEWDocument14 pagesFinancial Accounting September 2012 Marks Plan ICAEWMuhammad Ziaul HaqueNo ratings yet

- SIM ACC 226ACCE 411 Week 4 To 5 COPY 1Document31 pagesSIM ACC 226ACCE 411 Week 4 To 5 COPY 1Mireya Yue100% (1)

- ACTG115 - Ch02 SolutionsDocument16 pagesACTG115 - Ch02 SolutionsxxmbetaNo ratings yet

- 12 Igcse - Accounting - Ratios - Unlocked PDFDocument47 pages12 Igcse - Accounting - Ratios - Unlocked PDFshivom talrejaNo ratings yet

- 4th Sem BBA Industrial ProjectDocument60 pages4th Sem BBA Industrial Projectαβђเکђ€к ηєσgเ67% (12)

- Account Formats and Statements LayoutsDocument5 pagesAccount Formats and Statements LayoutsCynNo ratings yet