Download as pdf or txt

You might also like

- Ch18-11 Worksheet Syed Qamar Osama Raheel Shahrukh MughalDocument2 pagesCh18-11 Worksheet Syed Qamar Osama Raheel Shahrukh MughalSyed Qamar100% (2)

- Lupin's Foray Into Japan - SolutionDocument14 pagesLupin's Foray Into Japan - Solutionvardhan100% (1)

- Company Valuation & Ratio Analysis (Tata Motors) 2021Document25 pagesCompany Valuation & Ratio Analysis (Tata Motors) 2021Manveet SinghNo ratings yet

- Chap 14 - Bret Company (Case Study)Document5 pagesChap 14 - Bret Company (Case Study)Al HiponiaNo ratings yet

- IPODocument53 pagesIPOvj_gupta9100% (5)

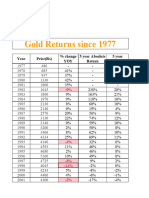

- Gold PriceDocument2 pagesGold PriceVikram MendaNo ratings yet

- Ejercicio Uso VariableDocument15 pagesEjercicio Uso VariableingenieromantencionNo ratings yet

- Punto 7 CatheDocument6 pagesPunto 7 CatheCatherine Astrid Figueroa MartinezNo ratings yet

- XLS317 XLS EngDocument10 pagesXLS317 XLS EngWilder Atalaya ChavezNo ratings yet

- TransitoDocument28 pagesTransitoKevin BarraganNo ratings yet

- GERDBYSOURCEDocument1 pageGERDBYSOURCEapi-3700445No ratings yet

- Fullerton AnalysisDocument8 pagesFullerton AnalysisSuman MandalNo ratings yet

- Housing Completions (1972 To 2007) : by Unit TypeDocument1 pageHousing Completions (1972 To 2007) : by Unit TypeM-NCPPCNo ratings yet

- Housing Completions, Montgomery County, Maryland (1972 To 2006)Document1 pageHousing Completions, Montgomery County, Maryland (1972 To 2006)M-NCPPCNo ratings yet

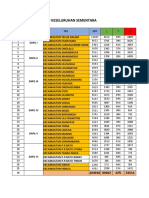

- Rekap Keseluruhan Sementara Pilkada Nisel 2020Document3 pagesRekap Keseluruhan Sementara Pilkada Nisel 2020kudusgiawaNo ratings yet

- Miones Tipo: Chart TitleDocument7 pagesMiones Tipo: Chart TitleYulieth CuacialpudNo ratings yet

- Customer Demand Cube: PurposeDocument15 pagesCustomer Demand Cube: PurposeTiyaNo ratings yet

- NSE Stock With SectorDocument243 pagesNSE Stock With SectorBeyond TechnicalsNo ratings yet

- Presentation 7Document8 pagesPresentation 7sammm vlogsNo ratings yet

- Crypto & Forex PlanDocument12 pagesCrypto & Forex PlanMouhamad BazziNo ratings yet

- PMP Project Management ExperienceDocument9 pagesPMP Project Management ExperienceVincent D. BlairNo ratings yet

- Caso PolaroidDocument45 pagesCaso PolaroidByron AlarcònNo ratings yet

- On The Ballot Recap - Initiative Usage 1998 - 2009Document1 pageOn The Ballot Recap - Initiative Usage 1998 - 2009Catherine SnowNo ratings yet

- Axiata Data Financials 4Q21bDocument11 pagesAxiata Data Financials 4Q21bhimu_050918No ratings yet

- Housing Completions (1972 To 2007) : by Unit TypeDocument1 pageHousing Completions (1972 To 2007) : by Unit TypeM-NCPPCNo ratings yet

- Section 4 - Group 13Document4 pagesSection 4 - Group 13Ravi KumarNo ratings yet

- Balkrishna IndsDocument9 pagesBalkrishna Indssaufin29No ratings yet

- Operator Search 20220419084949Document9 pagesOperator Search 20220419084949beriNo ratings yet

- 唯品会估值模型Document21 pages唯品会估值模型Yiang QinNo ratings yet

- Fase 1Document63 pagesFase 1Isabel CastilloNo ratings yet

- DCF ModelDocument51 pagesDCF Modelhugoe1969No ratings yet

- Perhitungan Trend, Siklus Dan MusimDocument14 pagesPerhitungan Trend, Siklus Dan MusimTuti SeptiowatiNo ratings yet

- Financial Modelling and Analysis ITCDocument9 pagesFinancial Modelling and Analysis ITCPriyam SarangiNo ratings yet

- Top Countries Off 52022Document6 pagesTop Countries Off 52022Nikhil SinghalNo ratings yet

- Bonus Chart 2010Document1 pageBonus Chart 2010jspectorNo ratings yet

- LibroDocument7 pagesLibroaleconstable16No ratings yet

- Pepper FryDocument13 pagesPepper FryMukesh KumarNo ratings yet

- Stock Screener Database - CROICDocument6 pagesStock Screener Database - CROICJay GalvanNo ratings yet

- Tpds - XLSX BUENODocument7 pagesTpds - XLSX BUENOEdwar ViverosNo ratings yet

- Base Case - Financial ModelDocument52 pagesBase Case - Financial Modeljuan.farrelNo ratings yet

- Base - Práctica 1Document19 pagesBase - Práctica 1Josue Cajacuri YarascaNo ratings yet

- AssignmentData1 - With AnalysisDocument28 pagesAssignmentData1 - With AnalysisAditya JandialNo ratings yet

- YTD DB TY Vs LYDocument31 pagesYTD DB TY Vs LYFabio FabNo ratings yet

- Dummy 1Document17 pagesDummy 1dafiq kamalNo ratings yet

- Adelanto TPD NARIÑO Clase 17-05Document6 pagesAdelanto TPD NARIÑO Clase 17-05LIZETH SAnUDO LOPEZNo ratings yet

- Olymp TradeDocument2 pagesOlymp TradeTina DiarNo ratings yet

- COGS Sheet FSD Sep-20Document11 pagesCOGS Sheet FSD Sep-20Fahad Khan TareenNo ratings yet

- IandF CM1B 202009 AnswerSheetDocument25 pagesIandF CM1B 202009 AnswerSheetvanessa8pangestuNo ratings yet

- Probation SupervisionDocument2 pagesProbation SupervisionLesson Plan ni Teacher GNo ratings yet

- Financial Year Ending in - Mar '18 Mar '17 Mar '16 Mar '15Document2 pagesFinancial Year Ending in - Mar '18 Mar '17 Mar '16 Mar '15B Akhil Sai KishoreNo ratings yet

- 03 - Marzo - PatentamientoDocument5 pages03 - Marzo - PatentamientoLeonardo PeirettiNo ratings yet

- Exercício de AplicaçãoDocument4 pagesExercício de AplicaçãoDeogracio Possiano JaimeNo ratings yet

- Sachaeffler India Ltd.Document63 pagesSachaeffler India Ltd.shivam vermaNo ratings yet

- Date Dia Total Cases Var PorcDocument15 pagesDate Dia Total Cases Var PorcJamill Jhosua Linares TejedaNo ratings yet

- Taller TránsitoDocument13 pagesTaller TránsitoAndresRangellNo ratings yet

- 02 - Febrero - PatentamientoDocument5 pages02 - Febrero - PatentamientoLeonardo PeirettiNo ratings yet

- Ebitda MarginDocument3 pagesEbitda MarginJinesh MehtaNo ratings yet

- Equty Analysis by Rameez Fazal Tayyeba JayanthDocument17 pagesEquty Analysis by Rameez Fazal Tayyeba JayanthtayyebaNo ratings yet

- ScreenshotsDocument98 pagesScreenshotsAishwarya SrivastavaNo ratings yet

- Europe Computer Sales DataDocument16 pagesEurope Computer Sales DataSebastián PaezNo ratings yet

- HDFC Bank - BaseDocument613 pagesHDFC Bank - BasebysqqqdxNo ratings yet

- Nigeria Faostat24.2. Final 3Document27 pagesNigeria Faostat24.2. Final 3Erika TadevosjanNo ratings yet

- United States Census Figures Back to 1630From EverandUnited States Census Figures Back to 1630No ratings yet

- Jei 2024003Document26 pagesJei 2024003Ahmadi AliNo ratings yet

- Jei 2024009Document13 pagesJei 2024009Ahmadi AliNo ratings yet

- Jei 2024001Document27 pagesJei 2024001Ahmadi AliNo ratings yet

- 10 1002@csr 2040Document15 pages10 1002@csr 2040Ahmadi AliNo ratings yet

- 10 1016@j Promfg 2020 03 043Document5 pages10 1016@j Promfg 2020 03 043Ahmadi AliNo ratings yet

- Bus Strat Env - 2020 - Shao - Environmental Regulation and Enterprise Innovation A ReviewDocument14 pagesBus Strat Env - 2020 - Shao - Environmental Regulation and Enterprise Innovation A ReviewAhmadi AliNo ratings yet

- 10 1016@j Techfore 2019 02 007Document8 pages10 1016@j Techfore 2019 02 007Ahmadi AliNo ratings yet

- Wans 2017Document32 pagesWans 2017Ahmadi AliNo ratings yet

- Becker Blease2011Document12 pagesBecker Blease2011Ahmadi AliNo ratings yet

- 1 s2.0 S2405844021026621 MainDocument10 pages1 s2.0 S2405844021026621 MainAhmadi AliNo ratings yet

- The Reaction To CSR Controversies by Institutional InvestorsDocument22 pagesThe Reaction To CSR Controversies by Institutional InvestorsAhmadi AliNo ratings yet

- Corporate Governance and Innovation Theory and EvidenceDocument47 pagesCorporate Governance and Innovation Theory and EvidenceAhmadi AliNo ratings yet

- Accounting Finance - 2020 - Xie - Internal Governance and InnovationDocument32 pagesAccounting Finance - 2020 - Xie - Internal Governance and InnovationAhmadi AliNo ratings yet

- 551 1162 2 PBDocument17 pages551 1162 2 PBAhmadi AliNo ratings yet

- Khan 2021Document18 pagesKhan 2021Ahmadi AliNo ratings yet

- Sustainability 14 15457Document15 pagesSustainability 14 15457Ahmadi AliNo ratings yet

- 10 1108 - Aea 11 2021 0297Document18 pages10 1108 - Aea 11 2021 0297Ahmadi AliNo ratings yet

- Wilcox2018 Module 2Document49 pagesWilcox2018 Module 2Ahmadi AliNo ratings yet

- Enpr S 21 00011Document20 pagesEnpr S 21 00011Ahmadi AliNo ratings yet

- Farhangdoust 2020Document27 pagesFarhangdoust 2020Ahmadi AliNo ratings yet

- Mujan 2019Document12 pagesMujan 2019Ahmadi AliNo ratings yet

- Gender Diversity and Earnings Management: The Case of Female Directors With Financial BackgroundDocument36 pagesGender Diversity and Earnings Management: The Case of Female Directors With Financial BackgroundAhmadi AliNo ratings yet

- 10.1108@RBF 12 2019 0169Document23 pages10.1108@RBF 12 2019 0169Ahmadi AliNo ratings yet

- Journal of Banking and Finance: Yi Feng, Keke Song, Yisong S. TianDocument19 pagesJournal of Banking and Finance: Yi Feng, Keke Song, Yisong S. TianAhmadi AliNo ratings yet

- Handbook of Guidelines: For Freelance Subject Matter ExpertsDocument11 pagesHandbook of Guidelines: For Freelance Subject Matter ExpertsAhmadi AliNo ratings yet

- Chat Landing Page - Journal Article Publishing Support CenterDocument2 pagesChat Landing Page - Journal Article Publishing Support CenterAhmadi AliNo ratings yet

- IPO Pricing With Accounting InformationDocument34 pagesIPO Pricing With Accounting InformationAhmadi AliNo ratings yet

- Initial Public Offerings: The Issue of Underpricing inDocument63 pagesInitial Public Offerings: The Issue of Underpricing inAhmadi AliNo ratings yet

- Safi 2021Document8 pagesSafi 2021Ahmadi AliNo ratings yet

- IPO Underpricing To Retain Family Control Under Concentrated Ownership: Evidence From Hong KongDocument30 pagesIPO Underpricing To Retain Family Control Under Concentrated Ownership: Evidence From Hong KongAhmadi AliNo ratings yet

- Timson Trade Platform Manual Version 2Document40 pagesTimson Trade Platform Manual Version 2Hibachi RufflesNo ratings yet

- Vanguard S&P 500 ETFDocument2 pagesVanguard S&P 500 ETFHeyu PermanaNo ratings yet

- ICICI Prudential Life Insurance ProspectusDocument616 pagesICICI Prudential Life Insurance ProspectusshamruthaNo ratings yet

- STT FinancilaDocument22 pagesSTT FinancilaravNo ratings yet

- CorpF ReviseDocument5 pagesCorpF ReviseTrang DangNo ratings yet

- The Fidelity Guide To Equity InvestingDocument16 pagesThe Fidelity Guide To Equity Investingmandar LawandeNo ratings yet

- Analisis Manajemen Strategi Pada PT. Mayora Indah J SmakkssDocument16 pagesAnalisis Manajemen Strategi Pada PT. Mayora Indah J SmakkssKucing OrenNo ratings yet

- 03 Share Split and Treasury SharesDocument17 pages03 Share Split and Treasury SharesAlloysius ParilNo ratings yet

- Valuation: A Conceptual Overview: Enterprise Value: The 30,000-Foot ViewDocument19 pagesValuation: A Conceptual Overview: Enterprise Value: The 30,000-Foot ViewCandelNo ratings yet

- Stock Market and Brand Awareness: Presented by Ronak ShahDocument11 pagesStock Market and Brand Awareness: Presented by Ronak Shahnarendra_thadani_1No ratings yet

- Basics of Stock MarketDocument26 pagesBasics of Stock MarketVenkat GV100% (1)

- Dividend PolicyDocument42 pagesDividend PolicysubraysNo ratings yet

- Annual Return 2020 21Document250 pagesAnnual Return 2020 21anil kumarNo ratings yet

- Solution To Case 12: What Are We Really Worth?Document4 pagesSolution To Case 12: What Are We Really Worth?khalil rebato100% (1)

- Problem 11-1 Problem 11-2 Answer A: MarketDocument8 pagesProblem 11-1 Problem 11-2 Answer A: MarketYen YenNo ratings yet

- MAS2 - 08 Capital Structure and Long-Term Financial DecisionsDocument3 pagesMAS2 - 08 Capital Structure and Long-Term Financial DecisionsBianca IyiyiNo ratings yet

- Ojk Regulation Number 32 2015.englishversionDocument18 pagesOjk Regulation Number 32 2015.englishversionGilang Mursito AjiNo ratings yet

- Annual Return: Form No. Mgt-7Document20 pagesAnnual Return: Form No. Mgt-7Esha ChaudharyNo ratings yet

- Demant AccountDocument78 pagesDemant AccountAmanjotNo ratings yet

- Chapter 7 Investment in Equity SecuritiesDocument12 pagesChapter 7 Investment in Equity SecuritiesGirlie Ann JimenezNo ratings yet

- Stocks, Bonds and Mutual BondsDocument4 pagesStocks, Bonds and Mutual BondsChrisNo ratings yet

- MVBS AnalysisDocument51 pagesMVBS AnalysisAtaiNo ratings yet

- Financial Analysis With Microsoft Excel 6th Edition Mayes Solutions ManualDocument24 pagesFinancial Analysis With Microsoft Excel 6th Edition Mayes Solutions Manualaramaismablative2ck3100% (20)

- Bowles Sporting Inc Is Prepared To Report The Following IncomeDocument1 pageBowles Sporting Inc Is Prepared To Report The Following IncomeAmit PandeyNo ratings yet

- Materi Rumus Uts MKDocument10 pagesMateri Rumus Uts MKMarsa ArrahmanNo ratings yet

- 7-4 PT Pandu Dan PT SadewaDocument5 pages7-4 PT Pandu Dan PT SadewaTeam 1No ratings yet

- Jurnal 1 Sinta 3Document7 pagesJurnal 1 Sinta 3nur helmiNo ratings yet