Download as pdf or txt

You might also like

- TNL21903417 082022Document2 pagesTNL21903417 082022Chetan ChoudharyNo ratings yet

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- Investor S Perception Towards Mutual Funds Project ReportDocument80 pagesInvestor S Perception Towards Mutual Funds Project ReportRavi SharmaNo ratings yet

- Revenue Regulations No 01-81Document5 pagesRevenue Regulations No 01-81RaymondNo ratings yet

- US Internal Revenue Service: f1042 - 2003Document4 pagesUS Internal Revenue Service: f1042 - 2003IRSNo ratings yet

- US Internal Revenue Service: f1042 - 1997Document4 pagesUS Internal Revenue Service: f1042 - 1997IRSNo ratings yet

- Annual Withholding Tax Return For U.S. Source Income of Foreign PersonsDocument2 pagesAnnual Withholding Tax Return For U.S. Source Income of Foreign PersonsJunior WalsonNo ratings yet

- US Internal Revenue Service: f1042 - 1992Document1 pageUS Internal Revenue Service: f1042 - 1992IRSNo ratings yet

- US Internal Revenue Service: f1042 - 1991Document1 pageUS Internal Revenue Service: f1042 - 1991IRSNo ratings yet

- Statement No.: Assignment 1Document12 pagesStatement No.: Assignment 1karthikgs123No ratings yet

- PIF Masterlist 2019Document1,125 pagesPIF Masterlist 2019Mary Ann Labiano DomingoNo ratings yet

- Rental Equipments Time Sheet TEMPLETEDocument1 pageRental Equipments Time Sheet TEMPLETEFood andfoodNo ratings yet

- Tax Calendar 2022 2023 Deloitte PrivateDocument1 pageTax Calendar 2022 2023 Deloitte PrivatePrativa RayNo ratings yet

- ZetkjretkjzrtkrzDocument2 pagesZetkjretkjzrtkrzHyacinth BalmacedaNo ratings yet

- Dec23 Strategy by J.k.shahDocument36 pagesDec23 Strategy by J.k.shahkrjm2004No ratings yet

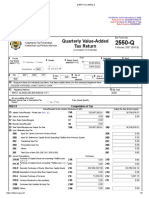

- gaddi_2550q_2Q_2022Document2 pagesgaddi_2550q_2Q_2022Romeo Niño BautistaNo ratings yet

- Capital Markets: 2020 SEC Filing Deadlines and Financial Statement Staleness DatesDocument3 pagesCapital Markets: 2020 SEC Filing Deadlines and Financial Statement Staleness DatesNepean Philippines IncNo ratings yet

- Timesheet: Periode Date Month Year To Date Month Year Regular Days Work DetailDocument2 pagesTimesheet: Periode Date Month Year To Date Month Year Regular Days Work DetailAfandi AffanNo ratings yet

- Day 1 Excel Format of BOADocument18 pagesDay 1 Excel Format of BOAErica FlorentinoNo ratings yet

- BIR Form 2551 - PDFDocument1 pageBIR Form 2551 - PDFMichael LaquianNo ratings yet

- BED 3 LEVEL 4 - Pagadian City NCHSDocument2 pagesBED 3 LEVEL 4 - Pagadian City NCHSNicole SilorioNo ratings yet

- Medical Canvas. Cash Flow Forecast For 1 YearDocument1 pageMedical Canvas. Cash Flow Forecast For 1 Yearazhar hussainNo ratings yet

- Meggitt-Flight Disp MMDocument49 pagesMeggitt-Flight Disp MMMarcos PauloNo ratings yet

- 5 Appendix VDocument79 pages5 Appendix Vparth sharmaNo ratings yet

- Balance of Payments of The Russian Federation For January-September of 2017 Main ComponentsDocument2 pagesBalance of Payments of The Russian Federation For January-September of 2017 Main ComponentsLee AhmedNo ratings yet

- AugustDocument2 pagesAugustRheno Lloyd LalisanNo ratings yet

- UntitledDocument44 pagesUntitledRafay AnwarNo ratings yet

- Strategy For Clearing CAFC June 2024 (Final)Document29 pagesStrategy For Clearing CAFC June 2024 (Final)srihari.eserveNo ratings yet

- BED 3 LEVEL 4 - Pagadian City NHSDocument2 pagesBED 3 LEVEL 4 - Pagadian City NHSNicole SilorioNo ratings yet

- Far 5 - Quarterly Report of Revenue and Receipts As of December 31, 2022Document3 pagesFar 5 - Quarterly Report of Revenue and Receipts As of December 31, 2022Whenng LopezNo ratings yet

- IMS 10 - Appendix B Record of Ship CertificatesDocument2 pagesIMS 10 - Appendix B Record of Ship Certificatestusharmitra12No ratings yet

- Appendix 3 - CDJDocument2 pagesAppendix 3 - CDJelizabeth medranoNo ratings yet

- Progress Report For The of June, 2022Document133 pagesProgress Report For The of June, 2022YeshiwondimNo ratings yet

- Strategy To Clear CA Inter May 2023 PDFDocument57 pagesStrategy To Clear CA Inter May 2023 PDFParag RaiyaniNo ratings yet

- Job Cost SheetDocument13 pagesJob Cost Sheetnshamsundar7929No ratings yet

- Fiscal Calendar FY 22 23Document1 pageFiscal Calendar FY 22 23Naufal ZabadyNo ratings yet

- Copia de 5. 1893 3000 Inst Ste PR LH 0014 Lookahead p20Document20 pagesCopia de 5. 1893 3000 Inst Ste PR LH 0014 Lookahead p20Jonathan baltaNo ratings yet

- Jawaban Test ToeflDocument2 pagesJawaban Test Toeflpraz acerNo ratings yet

- Jawaban Test ToeflDocument2 pagesJawaban Test ToeflOcky Kyocky RiadiNo ratings yet

- Gts 1stDocument2 pagesGts 1stGOLDEN TOPSTEEL CONSTRUCTION SUPPLYNo ratings yet

- Mor - Aug 2021Document3 pagesMor - Aug 2021Kiran PapalNo ratings yet

- Ca InterDocument48 pagesCa InterVANSHNo ratings yet

- 2007 Event Schedule PlannerDocument1 page2007 Event Schedule PlannerLana LaRae Williamson-HortonNo ratings yet

- Time Sheet TempleteDocument1 pageTime Sheet TempleteAhmed SaleemNo ratings yet

- Capital Markets: 2022 SEC Filing Deadlines and Financial Statement Staleness DeadlinesDocument3 pagesCapital Markets: 2022 SEC Filing Deadlines and Financial Statement Staleness DeadlinesHannah Dale Pacheco CardozaNo ratings yet

- Marks SheetDocument4 pagesMarks SheetTahir AzizNo ratings yet

- RCM Implemantation PlanDocument6 pagesRCM Implemantation PlanSam ShumbaNo ratings yet

- StaffhouseDocument1 pageStaffhouseVic ValdezNo ratings yet

- Contoh Post-Employment Benefits 2021Document39 pagesContoh Post-Employment Benefits 2021Judiono JoemanaNo ratings yet

- Time Study Observation Form: Element No. and DescriptionDocument3 pagesTime Study Observation Form: Element No. and DescriptionPaola HernandezNo ratings yet

- Form - Over-Time Request - Update 2018 - IanDocument2 pagesForm - Over-Time Request - Update 2018 - IanIonutz RobertNo ratings yet

- EPCK SerigneDocument1 pageEPCK Serignesokhnacom362No ratings yet

- What-If-Analysis & ForecastDocument6 pagesWhat-If-Analysis & ForecastuzairNo ratings yet

- Cambio 2Document1 pageCambio 2JESUS CRISTOBAL RIVERANo ratings yet

- Quarterly Value-Added Tax ReturnDocument2 pagesQuarterly Value-Added Tax ReturnFrancis M. TabajondaNo ratings yet

- Ezxcel 1Document4 pagesEzxcel 1Renato Paucar PreciadoNo ratings yet

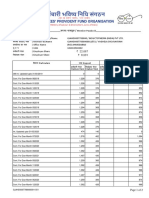

- LNL Iklcqd /: Employee Share Employer Share Employee Share Employer ShareDocument2 pagesLNL Iklcqd /: Employee Share Employer Share Employee Share Employer SharevijayNo ratings yet

- LNL Iklcqd /: Employee Share Employer Share Employee Share Employer ShareDocument2 pagesLNL Iklcqd /: Employee Share Employer Share Employee Share Employer SharevijayNo ratings yet

- J-Emotion (NS) 16 - AWP - PLDocument29 pagesJ-Emotion (NS) 16 - AWP - PLFatin AliesaNo ratings yet

- JBT Ofm Reports 9152020Document25 pagesJBT Ofm Reports 9152020Rhobbie NolloraNo ratings yet

- Calculation of PF ESI Damages & IntrestDocument5 pagesCalculation of PF ESI Damages & IntrestDeepak DasNo ratings yet

- Calendar 1011Document1 pageCalendar 1011Chris WilliamsNo ratings yet

- GNGGN00252970000208293 NewDocument3 pagesGNGGN00252970000208293 NewHimachali VloggerNo ratings yet

- US Internal Revenue Service: 2290rulesty2007v4 0Document6 pagesUS Internal Revenue Service: 2290rulesty2007v4 0IRSNo ratings yet

- 2008 Objectives Report To Congress v2Document153 pages2008 Objectives Report To Congress v2IRSNo ratings yet

- 2008 Data DictionaryDocument260 pages2008 Data DictionaryIRSNo ratings yet

- 2008 Credit Card Bulk Provider RequirementsDocument112 pages2008 Credit Card Bulk Provider RequirementsIRSNo ratings yet

- Capital BudgetingDocument68 pagesCapital Budgetingbemerkung100% (1)

- Chap 008Document69 pagesChap 008dbjnNo ratings yet

- Exercises (Capital Budgeting)Document2 pagesExercises (Capital Budgeting)bdiitNo ratings yet

- Credit Appraisal of RBLDocument58 pagesCredit Appraisal of RBLNishita SolankiNo ratings yet

- Maxicare Digest Attach After Page 66Document1 pageMaxicare Digest Attach After Page 66twenty19 lawNo ratings yet

- JPM US Value Fund Deck - 1120 - SEASGAIDocument33 pagesJPM US Value Fund Deck - 1120 - SEASGAIsidharth guptaNo ratings yet

- Intercorporate InvestmentsDocument30 pagesIntercorporate InvestmentsMia ramosNo ratings yet

- Business Startup ChecklistDocument5 pagesBusiness Startup ChecklistGhanapathi RamanathanNo ratings yet

- Ejercicios ProformaDocument3 pagesEjercicios ProformaSaira veru bernalNo ratings yet

- Safal Niveshak Stock Analysis Excel Version 5.0Document49 pagesSafal Niveshak Stock Analysis Excel Version 5.0mcmaklerNo ratings yet

- Business PlanDocument32 pagesBusiness PlanIbrahim Arafat ZicoNo ratings yet

- Chapter 2 Engineering EconomicsDocument34 pagesChapter 2 Engineering EconomicsharoonNo ratings yet

- Accounting For Derivative InstrumentsDocument30 pagesAccounting For Derivative InstrumentsKriti Saxena67% (3)

- Chapter 13 Solutions ManualDocument110 pagesChapter 13 Solutions Manualmarlon ventulan67% (3)

- TTD CaseDocument14 pagesTTD CaseAnil KardamNo ratings yet

- Indocement Tunggal Prakarsa TBK - Bilingual - 30jun2018 - INTP - 300718 PDFDocument128 pagesIndocement Tunggal Prakarsa TBK - Bilingual - 30jun2018 - INTP - 300718 PDFAditya CandraNo ratings yet

- Indus Motor Company LTD Ratio AnalysisDocument166 pagesIndus Motor Company LTD Ratio AnalysisAqeel IfthkharNo ratings yet

- Chapter 19 - AnswerDocument9 pagesChapter 19 - AnswerRey Aurel TayagNo ratings yet

- Waste Treatment Fzco Dubai Branch: Employee DetailsDocument1 pageWaste Treatment Fzco Dubai Branch: Employee Detailsg.herwinNo ratings yet

- 2005 Jotun Group Report - tcm29 1282Document23 pages2005 Jotun Group Report - tcm29 1282Ramesh JohnNo ratings yet

- RM 3Document6 pagesRM 3Harsh KumarNo ratings yet

- Solved MR and Mrs Lund and Their Two Children Ben andDocument1 pageSolved MR and Mrs Lund and Their Two Children Ben andAnbu jaromiaNo ratings yet

- DTR & BillingDocument190 pagesDTR & Billingkate perezNo ratings yet

- Joint Products and By-ProductsDocument16 pagesJoint Products and By-ProductsAnmol AgalNo ratings yet

- Determine Size of Sales ForceDocument15 pagesDetermine Size of Sales ForceShikha Jain100% (1)

- Acc 123 Final Requirement 2Document9 pagesAcc 123 Final Requirement 2Charlene Mae MalaluanNo ratings yet

- Icfai Law School The Icfai University, Dehradun: Submitted To: Ms. Stuti Tiwari Faculty, Principles of Taxation LawsDocument3 pagesIcfai Law School The Icfai University, Dehradun: Submitted To: Ms. Stuti Tiwari Faculty, Principles of Taxation LawsAditya PandeyNo ratings yet