Download as pdf or txt

You might also like

- Encana FinalDocument15 pagesEncana FinalSushant Rajputra100% (3)

- Merrill Lynch 2007 Analyst Valuation TrainingDocument74 pagesMerrill Lynch 2007 Analyst Valuation TrainingJose Garcia100% (22)

- First Quarter 2021 EarningsDocument11 pagesFirst Quarter 2021 EarningsCarlos FrancoNo ratings yet

- Second Quarter 2021 EarningsDocument11 pagesSecond Quarter 2021 EarningsCarlos FrancoNo ratings yet

- AAP Q4 2022 Earnings - FinalDocument10 pagesAAP Q4 2022 Earnings - FinalDaniel KwanNo ratings yet

- Wells Fargo - First-Quarter-2020-EarningsDocument40 pagesWells Fargo - First-Quarter-2020-EarningsAlexNo ratings yet

- FINANCIAL ACCOUNTING & REPORTING - JA-23 - Suggested - AnswersDocument11 pagesFINANCIAL ACCOUNTING & REPORTING - JA-23 - Suggested - AnswerssummerfashionlimitedNo ratings yet

- Course Name Course Code Student Name Student ID DateDocument7 pagesCourse Name Course Code Student Name Student ID Datemona asgharNo ratings yet

- JPM 1q11 PresDocument21 pagesJPM 1q11 PresyellowpigNo ratings yet

- Budget Study Session 1 April 27Document33 pagesBudget Study Session 1 April 27eonfjrminNo ratings yet

- TROW Q1 2022 Earnings ReleaseDocument15 pagesTROW Q1 2022 Earnings ReleaseKevin ParkerNo ratings yet

- Joaxjill NotesDocument6 pagesJoaxjill NotesAlliah Czyrielle Amorado PersinculaNo ratings yet

- Chapter 18 PDFDocument2 pagesChapter 18 PDFkrygyztanNo ratings yet

- CIA Cia3 AppbDocument4 pagesCIA Cia3 AppbertugrulrizvanNo ratings yet

- Citi 2nd QTR ResultsDocument10 pagesCiti 2nd QTR ResultsTim MooreNo ratings yet

- B2Holding ReportDocument155 pagesB2Holding ReportRoshan RahejaNo ratings yet

- ChinaNet 2012 Investor PresentationDocument74 pagesChinaNet 2012 Investor PresentationJosé ivan LópezNo ratings yet

- Eicher Motors CFProject Group11Document10 pagesEicher Motors CFProject Group11Greeshma SharathNo ratings yet

- Marsh MC Lennan 2021-77-81Document5 pagesMarsh MC Lennan 2021-77-81socialsim07No ratings yet

- Assignment 01Document18 pagesAssignment 01Md. Real MiahNo ratings yet

- Performance As of October 31, 2020 Holdings by Company Size: Institutional ClassDocument1 pagePerformance As of October 31, 2020 Holdings by Company Size: Institutional ClassLjubisa MaticNo ratings yet

- Uol Group Fy2020 Results 26 FEBRUARY 2021Document33 pagesUol Group Fy2020 Results 26 FEBRUARY 2021Pat KwekNo ratings yet

- Examen Ingles HitesDocument2 pagesExamen Ingles HitesKawaii SoledadNo ratings yet

- 2023 q2 Earnings Results PresentationDocument15 pages2023 q2 Earnings Results PresentationZerohedgeNo ratings yet

- Glacier Reports Second Quarter 2021 ResultsDocument3 pagesGlacier Reports Second Quarter 2021 ResultsriditoppoNo ratings yet

- GS PresentationDocument14 pagesGS PresentationZerohedgeNo ratings yet

- 107 25 Walmart 10 K ExcerptsDocument6 pages107 25 Walmart 10 K Excerptsi wayan suputraNo ratings yet

- MGI Q3 2010 EarningsDocument5 pagesMGI Q3 2010 EarningsBrian_Markwort_5393No ratings yet

- NYSE_CIT_1997Document8 pagesNYSE_CIT_1997pcelica77No ratings yet

- Ch03 ShowDocument54 pagesCh03 ShowMahmoud AbdullahNo ratings yet

- Performance As of October 31, 2020 Holdings by Company Size: Institutional ClassDocument1 pagePerformance As of October 31, 2020 Holdings by Company Size: Institutional ClassLjubisa MaticNo ratings yet

- 3q 2022 Earnings ReleaseDocument46 pages3q 2022 Earnings Releasecerohad333No ratings yet

- 3Q10 Earnings PresentationDocument24 pages3Q10 Earnings PresentationfcamargoeNo ratings yet

- BOB Analyst Presentation Q4 FY 2019 27052019 PDFDocument77 pagesBOB Analyst Presentation Q4 FY 2019 27052019 PDFSandeep KumarNo ratings yet

- The Presentation MaterialsDocument28 pagesThe Presentation MaterialsValter SilveiraNo ratings yet

- FAD 2022 - Dr. Lisa Su - Opening Final PostDocument38 pagesFAD 2022 - Dr. Lisa Su - Opening Final PostVashishth DudhiaNo ratings yet

- 1h23 Items Impacting Financial ReportingDocument17 pages1h23 Items Impacting Financial ReportingChris murrayNo ratings yet

- Financial Report - EditedDocument7 pagesFinancial Report - EditedMaina PeterNo ratings yet

- 2022Q1 PR EN FinalDocument13 pages2022Q1 PR EN FinalMATHU MOHANNo ratings yet

- Morgan Stanley 2nd QTR ResultsDocument9 pagesMorgan Stanley 2nd QTR ResultsTim MooreNo ratings yet

- Kin Pang Holdings Limited 建 鵬 控 股 有 限 公 司: Audited Annual Results Announcement For The Year Ended 31 December 2021Document37 pagesKin Pang Holdings Limited 建 鵬 控 股 有 限 公 司: Audited Annual Results Announcement For The Year Ended 31 December 2021ALNo ratings yet

- DIS q1 Fy21 EarningsDocument16 pagesDIS q1 Fy21 EarningsGeurlin AneusNo ratings yet

- Vicom 2Document7 pagesVicom 2johnsolarpanelsNo ratings yet

- Extra Ex QTTC28129Document4 pagesExtra Ex QTTC28129Quang TiếnNo ratings yet

- Financial Analysis - WalmartDocument3 pagesFinancial Analysis - WalmartLuka KhmaladzeNo ratings yet

- Visa Inc Fiscal 2021 Annual ReportDocument134 pagesVisa Inc Fiscal 2021 Annual ReportzoolandoNo ratings yet

- Visa Inc Fiscal 2023 Annual ReportDocument133 pagesVisa Inc Fiscal 2023 Annual ReportjonjreyesNo ratings yet

- Q3 2010 ResultsDocument8 pagesQ3 2010 Resultspatburchall6278No ratings yet

- CPG Annual Report 2015Document56 pagesCPG Annual Report 2015Anonymous 2vtxh4No ratings yet

- Annual Report 2020Document248 pagesAnnual Report 2020Trina NaskarNo ratings yet

- Annual Results 2022 Media ReleaseDocument29 pagesAnnual Results 2022 Media ReleaseNikhil KulkarniNo ratings yet

- JPM Q2 2023 PresentationDocument15 pagesJPM Q2 2023 PresentationZerohedgeNo ratings yet

- Emlak Konut REIC: Price Target RevisionDocument6 pagesEmlak Konut REIC: Price Target RevisionCbpNo ratings yet

- q4 Fy21 EarningsDocument19 pagesq4 Fy21 EarningsJoseph Adinolfi Jr.No ratings yet

- FY24 Q1 Combined NIKE Press Release Schedules FINALDocument7 pagesFY24 Q1 Combined NIKE Press Release Schedules FINALTADIWANo ratings yet

- FIN202 - SU23 - Individual AssignmentDocument5 pagesFIN202 - SU23 - Individual AssignmentÁnh Dương NguyễnNo ratings yet

- 3Q09 Earnings Presentation FINALDocument61 pages3Q09 Earnings Presentation FINALZerohedgeNo ratings yet

- AMZN Webslides - Q322 - FinalDocument19 pagesAMZN Webslides - Q322 - FinalBonnie DebbarmaNo ratings yet

- Parrino Corp Fin 5e PPT Ch03Document76 pagesParrino Corp Fin 5e PPT Ch03trangnnhhs180588No ratings yet

- Nyse Bac 2000Document36 pagesNyse Bac 2000aditya tripathiNo ratings yet

- q3 Fy22 EarningsDocument20 pagesq3 Fy22 EarningsMani packageNo ratings yet

- Private Debt: Yield, Safety and the Emergence of Alternative LendingFrom EverandPrivate Debt: Yield, Safety and the Emergence of Alternative LendingNo ratings yet

- 2Q22 Alcoa Financial ResultsDocument16 pages2Q22 Alcoa Financial ResultsRafa BorgesNo ratings yet

- VIV PR Vivendi Q1 2022 RevenuesDocument9 pagesVIV PR Vivendi Q1 2022 RevenuesRafa BorgesNo ratings yet

- Z# ( - ! # $# ") $" $!# $$# # !" # $# %!$#) !" ! # # !#) !# - ! ) # - ! (# #) (!# $# # (# # (# !!) $# # " (# ( - ! # ZZ# ! - ) $) #) # " (# # $" # ZZZ# ! - ) $) #) # " (# # $" # "Document2 pagesZ# ( - ! # $# ") $" $!# $$# # !" # $# %!$#) !" ! # # !#) !# - ! ) # - ! (# #) (!# $# # (# # (# !!) $# # " (# ( - ! # ZZ# ! - ) $) #) # " (# # $" # ZZZ# ! - ) $) #) # " (# # $" # "Rafa BorgesNo ratings yet

- Adp National Employment Report December2021 Final Press ReleaseDocument5 pagesAdp National Employment Report December2021 Final Press ReleaseRafa BorgesNo ratings yet

- Z! ( - ! "!) " "! ""! ! ! "! #"!) ! ! !) ! - ) ! - (! !) (! "! ! (! ! (!) "! ! (! ( - ! ZZ! - ) ") !) ! (! ! " ! ZZZ! - ) ") !) ! (! ! " !Document2 pagesZ! ( - ! "!) " "! ""! ! ! "! #"!) ! ! !) ! - ) ! - (! !) (! "! ! (! ! (!) "! ! (! ( - ! ZZ! - ) ") !) ! (! ! " ! ZZZ! - ) ") !) ! (! ! " !Rafa BorgesNo ratings yet

- Z! ( - ! "!) " "! ""! ! ! "! #"!) ! ! !) ! - ) ! - (! !) (! "! ! (! ! (!) "! ! (! ( - ! ZZ! - ) ") !) ! (! ! " ! ZZZ! - ) ") !) ! (! ! " !Document2 pagesZ! ( - ! "!) " "! ""! ! ! "! #"!) ! ! !) ! - ) ! - (! !) (! "! ! (! ! (!) "! ! (! ( - ! ZZ! - ) ") !) ! (! ! " ! ZZZ! - ) ") !) ! (! ! " !Rafa BorgesNo ratings yet

- The Press ReleaseDocument19 pagesThe Press ReleaseRafa BorgesNo ratings yet

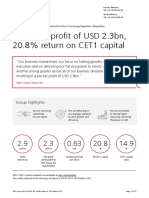

- 3Q21 Net Profit of USD 2.3bn, 20.8% Return On CET1 Capital: Group HighlightsDocument14 pages3Q21 Net Profit of USD 2.3bn, 20.8% Return On CET1 Capital: Group HighlightsRafa BorgesNo ratings yet

- C P I - N 2021Document38 pagesC P I - N 2021Rafa BorgesNo ratings yet

- Bank of America Reports Q3-21 Net Income of $7.7 Billion, EPS of $0.85Document19 pagesBank of America Reports Q3-21 Net Income of $7.7 Billion, EPS of $0.85Rafa BorgesNo ratings yet

- Morgan StanleyDocument9 pagesMorgan StanleyRafa BorgesNo ratings yet

- Z" ( - " #" !) #! # " ##" " ! " #" $ #") ! " " ") " - ) " - (" ") (" #" " (" " (") #" " ! (" ( - " ZZ" - ) #) ") " ! (" " #! " ZZZ" - ) #) ") " ! (" " #! " !Document2 pagesZ" ( - " #" !) #! # " ##" " ! " #" $ #") ! " " ") " - ) " - (" ") (" #" " (" " (") #" " ! (" ( - " ZZ" - ) #) ") " ! (" " #! " ZZZ" - ) #) ") " ! (" " #! " !Rafa BorgesNo ratings yet

- PayrollDocument41 pagesPayrollRafa BorgesNo ratings yet

- Beige Book: For Use at 2:00 PM EDT Wednesday July 14, 2021Document32 pagesBeige Book: For Use at 2:00 PM EDT Wednesday July 14, 2021Rafa BorgesNo ratings yet

- Release: 2 Quarter of 2021Document29 pagesRelease: 2 Quarter of 2021Rafa BorgesNo ratings yet

- Report USADocument12 pagesReport USARafa BorgesNo ratings yet

- Brazil's Economic Outlook and Agenda BC#: Roberto Campos NetoDocument48 pagesBrazil's Economic Outlook and Agenda BC#: Roberto Campos NetoRafa BorgesNo ratings yet

- 2013 Whos Next in LineDocument8 pages2013 Whos Next in LineZerohedgeNo ratings yet

- SECURITISATIONDocument40 pagesSECURITISATIONHARSHA SHENOYNo ratings yet

- Module 3 - BusimathDocument5 pagesModule 3 - BusimathAcelin Rayelle TULAGANNo ratings yet

- Citimortgage LawsuitDocument120 pagesCitimortgage LawsuitAdam Belz100% (1)

- Chapter14 SolutionsDocument46 pagesChapter14 Solutionsaboodyuae2000No ratings yet

- The Financial System - Chapter 1Document26 pagesThe Financial System - Chapter 1Fox ButtlerNo ratings yet

- Internship ReportDocument33 pagesInternship ReportNurul AlyaNo ratings yet

- 10 - AKPKs Workplace Financial Education ServicesDocument29 pages10 - AKPKs Workplace Financial Education ServicesLawrence KhohNo ratings yet

- Guingona, Jr. vs. Carague 196 SCRA 221, April 22, 1991Document11 pagesGuingona, Jr. vs. Carague 196 SCRA 221, April 22, 1991CHENGNo ratings yet

- General Math Second Quarter ExamDocument2 pagesGeneral Math Second Quarter ExamShiena Rhose Lucero100% (1)

- Babst vs. CADocument3 pagesBabst vs. CAOlan Dave LachicaNo ratings yet

- Title: Understanding The Challenges of Sari - Sari Store Owners at Brgy. Sala Balete, BatangasDocument1 pageTitle: Understanding The Challenges of Sari - Sari Store Owners at Brgy. Sala Balete, BatangasKimberly Solomon JavierNo ratings yet

- Paper - 8: Financial Management and Economics For Finance Section - A: Financial ManagementDocument31 pagesPaper - 8: Financial Management and Economics For Finance Section - A: Financial ManagementRonak ChhabriaNo ratings yet

- Jay Fishman Transcripts. Michael Jackson Exe. Branca V IRSDocument84 pagesJay Fishman Transcripts. Michael Jackson Exe. Branca V IRSTeamMichaelNo ratings yet

- 92 PNB MadecorDocument10 pages92 PNB MadecorGgh FghjNo ratings yet

- Week # 10 MortgagesDocument24 pagesWeek # 10 MortgagesFatema AkhterNo ratings yet

- Introduction To Corporate FinanceDocument43 pagesIntroduction To Corporate Financeanjali shilpa kajalNo ratings yet

- BMC ActDocument551 pagesBMC ActRatnesh DubeNo ratings yet

- Accounting Top 50 QuestionsDocument152 pagesAccounting Top 50 QuestionsDeep Mehta0% (1)

- Financial Planning Guide, School of Medicine, Ross University, 2013-2014Document12 pagesFinancial Planning Guide, School of Medicine, Ross University, 2013-2014coxfnNo ratings yet

- Financial Markets and InstitutionsDocument21 pagesFinancial Markets and InstitutionsDaryl PanganibanNo ratings yet

- Case Study Bhushan SteelDocument17 pagesCase Study Bhushan Steelharsh agarwal100% (1)

- Receivable FinancingDocument18 pagesReceivable FinancingGab IgnacioNo ratings yet

- Net Present Value: A Primer: BM63002: Corporate FinanceDocument17 pagesNet Present Value: A Primer: BM63002: Corporate FinanceSagaeNo ratings yet

- Working Capital Aanalysis IciciDocument114 pagesWorking Capital Aanalysis Icicifunkisanju1No ratings yet

- Banking Law - Atty. James Keith HeffronDocument18 pagesBanking Law - Atty. James Keith HeffronJadeNo ratings yet

- FS AnalysisDocument51 pagesFS AnalysisJecelyn PaganaNo ratings yet

- The Anti-Thought-Control DictionaryDocument120 pagesThe Anti-Thought-Control DictionaryPambas AmaralNo ratings yet