GLOBUSSPR - Investor Presentation - 16-Jun-21 - Tickertape

GLOBUSSPR - Investor Presentation - 16-Jun-21 - Tickertape

You might also like

- The Basics of Public Budgeting and Financial Management: A Handbook for Academics and PractitionersFrom EverandThe Basics of Public Budgeting and Financial Management: A Handbook for Academics and PractitionersNo ratings yet

- Ezz Steel Financial AnalysisDocument31 pagesEzz Steel Financial Analysismohamed ashorNo ratings yet

- Week 1 - Partnership Formation and Partnership OperationDocument10 pagesWeek 1 - Partnership Formation and Partnership OperationJanna Mari Frias100% (1)

- BIR Audit ManualDocument89 pagesBIR Audit ManualRivera RwlrNo ratings yet

- Car Wash Business PlanDocument26 pagesCar Wash Business PlanAmi BangladeshiNo ratings yet

- Chapter 13Document75 pagesChapter 13Anonymous rh4M7A100% (2)

- AnalysisDocument7 pagesAnalysisrajibzzamanibcsNo ratings yet

- 1Q21 Profit in Line With Estimates: SM Investments CorporationDocument8 pages1Q21 Profit in Line With Estimates: SM Investments CorporationJajahinaNo ratings yet

- Tech Mahindra Valuation Report FY21 Equity Inv CIA3Document5 pagesTech Mahindra Valuation Report FY21 Equity Inv CIA3safwan hosainNo ratings yet

- Retail Industry Retail Industry Retail IndustryDocument8 pagesRetail Industry Retail Industry Retail IndustryTanmay PokaleNo ratings yet

- Quarterly Update Q4FY20: Visaka Industries LTDDocument10 pagesQuarterly Update Q4FY20: Visaka Industries LTDsherwinmitraNo ratings yet

- Telenor Group: First Quarter 2021Document37 pagesTelenor Group: First Quarter 2021Jawwad ZakiNo ratings yet

- H AnhDocument8 pagesH AnhVăn ĐứcNo ratings yet

- Madhuvanthi Raja-Accounts Minor 2Document11 pagesMadhuvanthi Raja-Accounts Minor 2madhuvanthi.rajaaNo ratings yet

- Momo Operating Report 2022 Q4Document5 pagesMomo Operating Report 2022 Q4Harris ChengNo ratings yet

- Earnings Presentation: Bse Code: 524558 - Nse Symbol: Neulandlab - Bloomberg: Nll:In - Reuters: Neul - NsDocument34 pagesEarnings Presentation: Bse Code: 524558 - Nse Symbol: Neulandlab - Bloomberg: Nll:In - Reuters: Neul - Nssunil.dasarath jadhavNo ratings yet

- q2 Investor Forum 2017 2Document15 pagesq2 Investor Forum 2017 2Nisal Nuwan SenarathnaNo ratings yet

- Godrej Consumer Products Result Update - Q1FY23Document4 pagesGodrej Consumer Products Result Update - Q1FY23Prity KumariNo ratings yet

- Earnings Call Q4 2014 17 Feb 2015Document22 pagesEarnings Call Q4 2014 17 Feb 2015vanessa karmadjayaNo ratings yet

- Vertical Analysis Tabung HajiDocument6 pagesVertical Analysis Tabung HajiRyuzanna JubaidiNo ratings yet

- Year 2018 2019 2020: Task 1Document9 pagesYear 2018 2019 2020: Task 1Prateek ChandnaNo ratings yet

- Dwnload Full Fundamentals of Corporate Finance 4th Edition Berk Solutions Manual PDFDocument35 pagesDwnload Full Fundamentals of Corporate Finance 4th Edition Berk Solutions Manual PDFbrumfieldridleyvip100% (13)

- Pertamina 1H 2021 PerformanceDocument18 pagesPertamina 1H 2021 PerformanceMuhamad Luthfi azizNo ratings yet

- Phiroze Jeejeebhoy Towers Dalal Street Mumbai - 400 001Document5 pagesPhiroze Jeejeebhoy Towers Dalal Street Mumbai - 400 001Namrata ShahNo ratings yet

- Danone Year Results 2022Document12 pagesDanone Year Results 2022celinemaillard65No ratings yet

- SailashreeChakraborty 13600921093 FM401Document12 pagesSailashreeChakraborty 13600921093 FM401Sailashree ChakrabortyNo ratings yet

- (CL Logistics) 3Q23IR - ENG - VFDocument20 pages(CL Logistics) 3Q23IR - ENG - VFAyee 217No ratings yet

- 2.valuation - TDM - WITHOUT - SOLUTIONS Slim FinalDocument55 pages2.valuation - TDM - WITHOUT - SOLUTIONS Slim FinalMeriam HaouesNo ratings yet

- Adidias Ar21 - En-3-150Document148 pagesAdidias Ar21 - En-3-150Abdourahamane DialloNo ratings yet

- Sansera-Engineering 30052024 ICICI-SecuritiesDocument5 pagesSansera-Engineering 30052024 ICICI-SecuritiesgreyistariNo ratings yet

- Chevron Lubricants Lanka PLC: Hold For Dividends Lack of Long Term Growth Prospects Limit Price UpsideDocument3 pagesChevron Lubricants Lanka PLC: Hold For Dividends Lack of Long Term Growth Prospects Limit Price UpsidejdNo ratings yet

- Sha, Da Lill, Ited: CropchemDocument25 pagesSha, Da Lill, Ited: Cropchemaditig2301No ratings yet

- Financial Results Briefing Material For FY2019: April 1, 2018 To March 31, 2019Document30 pagesFinancial Results Briefing Material For FY2019: April 1, 2018 To March 31, 2019choiand1No ratings yet

- Kirk Fulford - AASB PresentationDocument33 pagesKirk Fulford - AASB PresentationTrisha Powell CrainNo ratings yet

- Page Industries: Revenue Growth Improves While Margins DeclineDocument8 pagesPage Industries: Revenue Growth Improves While Margins DeclinePuneet367No ratings yet

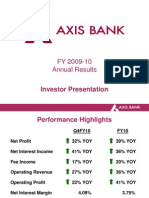

- FY 2009-10 Annual Results: Investor PresentationDocument34 pagesFY 2009-10 Annual Results: Investor PresentationDujesh KardamNo ratings yet

- Constellation Software IncDocument6 pagesConstellation Software IncSugar RayNo ratings yet

- Q3 & 9M FY21 - Results Presentation: February 2021Document29 pagesQ3 & 9M FY21 - Results Presentation: February 2021Richa CNo ratings yet

- Earnings Estimates Answer q3 2021Document1 pageEarnings Estimates Answer q3 2021LT COL VIKRAM SINGH EPGDIB 2021-22No ratings yet

- Sub: Raymond Limited - Investor Presentation: Rakesh Muljibh Ai DarjiDocument64 pagesSub: Raymond Limited - Investor Presentation: Rakesh Muljibh Ai DarjiSathwik PadamNo ratings yet

- 1Q21 Profit Up 78.1% Q/Q But Outlook Remains Uncertain: SM Prime Holdings, IncDocument9 pages1Q21 Profit Up 78.1% Q/Q But Outlook Remains Uncertain: SM Prime Holdings, IncJajahinaNo ratings yet

- Bwcu Htsqwn00sorvupdk.3Document22 pagesBwcu Htsqwn00sorvupdk.3JoshKernNo ratings yet

- Earnings Presentation - InRetail - Q4'21Document26 pagesEarnings Presentation - InRetail - Q4'21Cecilia Campos VelascoNo ratings yet

- 3Q17 Net Income Down 39.2% Y/y, Outlook Remains Poor: Universal Robina CorporationDocument8 pages3Q17 Net Income Down 39.2% Y/y, Outlook Remains Poor: Universal Robina Corporationherrewt rewterwNo ratings yet

- Assignment Fin420 - Individual & Group EditDocument58 pagesAssignment Fin420 - Individual & Group EditHakim SantiagoNo ratings yet

- Q1FY22 Result Update City Union Bank LTD: Beat On Operational Front Due To Lower Credit CostDocument12 pagesQ1FY22 Result Update City Union Bank LTD: Beat On Operational Front Due To Lower Credit Costforgi mistyNo ratings yet

- V-Guard-Industries - Q4 FY21-Results-PresentationDocument17 pagesV-Guard-Industries - Q4 FY21-Results-PresentationanooppattazhyNo ratings yet

- Fin 440 ReportDocument40 pagesFin 440 Reportsayed.mahmud7No ratings yet

- Accounting Project 2Document8 pagesAccounting Project 2api-661554832No ratings yet

- Dixon InvestorPresentationJan2022Document12 pagesDixon InvestorPresentationJan2022raguramrNo ratings yet

- RLX Technology Inc.: Earnings Presentation Q3 2021Document21 pagesRLX Technology Inc.: Earnings Presentation Q3 2021Faris RahmanNo ratings yet

- Iifl Wealth & Asset Management: Q4 and Full Year FY21 Performance UpdateDocument21 pagesIifl Wealth & Asset Management: Q4 and Full Year FY21 Performance UpdateRohan RautelaNo ratings yet

- Dupont Analysis of Adani Power: Particulars 2021 2020Document3 pagesDupont Analysis of Adani Power: Particulars 2021 2020Ananthasankar SNairNo ratings yet

- Acount ExpensesDocument1 pageAcount ExpenseshxNo ratings yet

- 2022 10 20 PH S CNVRGDocument7 pages2022 10 20 PH S CNVRGValiente RandzNo ratings yet

- TCS Ashish Ranjan: 2.TCS Balance Sheet AnalysisDocument7 pagesTCS Ashish Ranjan: 2.TCS Balance Sheet Analysissnigdha sahayNo ratings yet

- Manappuram Finance Investor PresentationDocument43 pagesManappuram Finance Investor PresentationabmahendruNo ratings yet

- Long Awaited China Revenues Get Booked But FV Reduced As Restrictions TightenDocument8 pagesLong Awaited China Revenues Get Booked But FV Reduced As Restrictions TightenJajahinaNo ratings yet

- My Life at 6ft BelowDocument1 pageMy Life at 6ft Belowvasquez.jabezraphael308129No ratings yet

- Financial DepartmentDocument27 pagesFinancial DepartmentPiyu VyasNo ratings yet

- Earnings Estimates Answer q1 2021Document1 pageEarnings Estimates Answer q1 2021rdtuf ddkdkdNo ratings yet

- Task 1 BigTech TemplateDocument5 pagesTask 1 BigTech Templatedaniyalansari.8425No ratings yet

- Varma Capitals - Modeling TestDocument6 pagesVarma Capitals - Modeling TestSuper FreakNo ratings yet

- Internal Forces G, HDocument6 pagesInternal Forces G, HRui JiaNo ratings yet

- Basic Concepts: Maxfort School-Rohini Chapter - RevenueDocument7 pagesBasic Concepts: Maxfort School-Rohini Chapter - Revenuepiyush rohiraNo ratings yet

- Maxfort School-Rohini Worksheet 1 - Organisation of Data Q1Document3 pagesMaxfort School-Rohini Worksheet 1 - Organisation of Data Q1piyush rohiraNo ratings yet

- The Bmu Mba: A InitiativeDocument19 pagesThe Bmu Mba: A Initiativepiyush rohiraNo ratings yet

- Receipt: Reference No.: 573119 Date:September 16, 2021Document1 pageReceipt: Reference No.: 573119 Date:September 16, 2021piyush rohiraNo ratings yet

- Economics by Piyush Rohira (9999794302) : Om Sai RamDocument7 pagesEconomics by Piyush Rohira (9999794302) : Om Sai Rampiyush rohiraNo ratings yet

- Economics DepreciationDocument3 pagesEconomics DepreciationGeodetic Engineering FilesNo ratings yet

- Module 13 - BusCom - Forex. - StudentsDocument13 pagesModule 13 - BusCom - Forex. - StudentsLuisito CorreaNo ratings yet

- Accounting 3 4 Module 5bDocument2 pagesAccounting 3 4 Module 5bMariel Ann RebancosNo ratings yet

- Risk Management in Banks00001Document52 pagesRisk Management in Banks00001Neha DhuriNo ratings yet

- RLX 4Q23 PresentationDocument26 pagesRLX 4Q23 PresentationrdtrinyNo ratings yet

- Module 3Document47 pagesModule 3Harrold HarryNo ratings yet

- Case Hansson Private LabelDocument15 pagesCase Hansson Private Labelpaul57% (7)

- Lat 7 Knight&lesserDocument5 pagesLat 7 Knight&lesserNadratul Hasanah LubisNo ratings yet

- Laporan Tahunan 2013Document152 pagesLaporan Tahunan 2013NadineNo ratings yet

- Law - Insider - Exlservice Holdings Inc - Merger Agreement by and Among Exlservice Holdings - Filed - 06 06 2011 - ContractDocument89 pagesLaw - Insider - Exlservice Holdings Inc - Merger Agreement by and Among Exlservice Holdings - Filed - 06 06 2011 - ContractSean JJ IntiomaleNo ratings yet

- BEFA Ece, Eee, Eie and Me ReccDocument9 pagesBEFA Ece, Eee, Eie and Me Reccprasad babuNo ratings yet

- Budget Management System User Manual: Department of Treasury and FinanceDocument60 pagesBudget Management System User Manual: Department of Treasury and FinanceChelle P. TenorioNo ratings yet

- Cat OneDocument2 pagesCat Onegerrad cortezNo ratings yet

- MBA 468 2 Credits Objective: F 3 - Management of Banks and Financial InstitutionsDocument3 pagesMBA 468 2 Credits Objective: F 3 - Management of Banks and Financial Institutions05550No ratings yet

- LEAP - Business Finance - Q3 W3 W4Document9 pagesLEAP - Business Finance - Q3 W3 W4Jade MonteverosNo ratings yet

- Financial Accounting (1st Year)Document18 pagesFinancial Accounting (1st Year)RohitNo ratings yet

- Abc Chapter 2Document22 pagesAbc Chapter 2ZNo ratings yet

- Presenatation On Fund Flow Statement: BY: Weena Yancey Kyrmen Singleman DipjoytiDocument22 pagesPresenatation On Fund Flow Statement: BY: Weena Yancey Kyrmen Singleman DipjoytiKuladeepa KrNo ratings yet

- Annual Report 2020Document444 pagesAnnual Report 2020haseen ullahNo ratings yet

- Choice 1-1Document17 pagesChoice 1-1Dagnachew WeldegebrielNo ratings yet

- TML Standalone Results Sept 2023 1Document5 pagesTML Standalone Results Sept 2023 1NagendranNo ratings yet

- Tesla Inc Financial Statements (Extract)Document10 pagesTesla Inc Financial Statements (Extract)Abhishek BatraNo ratings yet

- Actg 5 - Intermediate Accounting 3Document69 pagesActg 5 - Intermediate Accounting 3Christian N Magsino50% (2)

- Partnership Liquidation QuizDocument4 pagesPartnership Liquidation QuizMark Francis Solante100% (1)

- Sample Thesis Financial Performance AnalysisDocument4 pagesSample Thesis Financial Performance Analysissandraahnwashington100% (2)

Download as pdf or txt

You might also like

- The Basics of Public Budgeting and Financial Management: A Handbook for Academics and PractitionersFrom EverandThe Basics of Public Budgeting and Financial Management: A Handbook for Academics and PractitionersNo ratings yet

- Ezz Steel Financial AnalysisDocument31 pagesEzz Steel Financial Analysismohamed ashorNo ratings yet

- Week 1 - Partnership Formation and Partnership OperationDocument10 pagesWeek 1 - Partnership Formation and Partnership OperationJanna Mari Frias100% (1)

- BIR Audit ManualDocument89 pagesBIR Audit ManualRivera RwlrNo ratings yet

- Car Wash Business PlanDocument26 pagesCar Wash Business PlanAmi BangladeshiNo ratings yet

- Chapter 13Document75 pagesChapter 13Anonymous rh4M7A100% (2)

- AnalysisDocument7 pagesAnalysisrajibzzamanibcsNo ratings yet

- 1Q21 Profit in Line With Estimates: SM Investments CorporationDocument8 pages1Q21 Profit in Line With Estimates: SM Investments CorporationJajahinaNo ratings yet

- Tech Mahindra Valuation Report FY21 Equity Inv CIA3Document5 pagesTech Mahindra Valuation Report FY21 Equity Inv CIA3safwan hosainNo ratings yet

- Retail Industry Retail Industry Retail IndustryDocument8 pagesRetail Industry Retail Industry Retail IndustryTanmay PokaleNo ratings yet

- Quarterly Update Q4FY20: Visaka Industries LTDDocument10 pagesQuarterly Update Q4FY20: Visaka Industries LTDsherwinmitraNo ratings yet

- Telenor Group: First Quarter 2021Document37 pagesTelenor Group: First Quarter 2021Jawwad ZakiNo ratings yet

- H AnhDocument8 pagesH AnhVăn ĐứcNo ratings yet

- Madhuvanthi Raja-Accounts Minor 2Document11 pagesMadhuvanthi Raja-Accounts Minor 2madhuvanthi.rajaaNo ratings yet

- Momo Operating Report 2022 Q4Document5 pagesMomo Operating Report 2022 Q4Harris ChengNo ratings yet

- Earnings Presentation: Bse Code: 524558 - Nse Symbol: Neulandlab - Bloomberg: Nll:In - Reuters: Neul - NsDocument34 pagesEarnings Presentation: Bse Code: 524558 - Nse Symbol: Neulandlab - Bloomberg: Nll:In - Reuters: Neul - Nssunil.dasarath jadhavNo ratings yet

- q2 Investor Forum 2017 2Document15 pagesq2 Investor Forum 2017 2Nisal Nuwan SenarathnaNo ratings yet

- Godrej Consumer Products Result Update - Q1FY23Document4 pagesGodrej Consumer Products Result Update - Q1FY23Prity KumariNo ratings yet

- Earnings Call Q4 2014 17 Feb 2015Document22 pagesEarnings Call Q4 2014 17 Feb 2015vanessa karmadjayaNo ratings yet

- Vertical Analysis Tabung HajiDocument6 pagesVertical Analysis Tabung HajiRyuzanna JubaidiNo ratings yet

- Year 2018 2019 2020: Task 1Document9 pagesYear 2018 2019 2020: Task 1Prateek ChandnaNo ratings yet

- Dwnload Full Fundamentals of Corporate Finance 4th Edition Berk Solutions Manual PDFDocument35 pagesDwnload Full Fundamentals of Corporate Finance 4th Edition Berk Solutions Manual PDFbrumfieldridleyvip100% (13)

- Pertamina 1H 2021 PerformanceDocument18 pagesPertamina 1H 2021 PerformanceMuhamad Luthfi azizNo ratings yet

- Phiroze Jeejeebhoy Towers Dalal Street Mumbai - 400 001Document5 pagesPhiroze Jeejeebhoy Towers Dalal Street Mumbai - 400 001Namrata ShahNo ratings yet

- Danone Year Results 2022Document12 pagesDanone Year Results 2022celinemaillard65No ratings yet

- SailashreeChakraborty 13600921093 FM401Document12 pagesSailashreeChakraborty 13600921093 FM401Sailashree ChakrabortyNo ratings yet

- (CL Logistics) 3Q23IR - ENG - VFDocument20 pages(CL Logistics) 3Q23IR - ENG - VFAyee 217No ratings yet

- 2.valuation - TDM - WITHOUT - SOLUTIONS Slim FinalDocument55 pages2.valuation - TDM - WITHOUT - SOLUTIONS Slim FinalMeriam HaouesNo ratings yet

- Adidias Ar21 - En-3-150Document148 pagesAdidias Ar21 - En-3-150Abdourahamane DialloNo ratings yet

- Sansera-Engineering 30052024 ICICI-SecuritiesDocument5 pagesSansera-Engineering 30052024 ICICI-SecuritiesgreyistariNo ratings yet

- Chevron Lubricants Lanka PLC: Hold For Dividends Lack of Long Term Growth Prospects Limit Price UpsideDocument3 pagesChevron Lubricants Lanka PLC: Hold For Dividends Lack of Long Term Growth Prospects Limit Price UpsidejdNo ratings yet

- Sha, Da Lill, Ited: CropchemDocument25 pagesSha, Da Lill, Ited: Cropchemaditig2301No ratings yet

- Financial Results Briefing Material For FY2019: April 1, 2018 To March 31, 2019Document30 pagesFinancial Results Briefing Material For FY2019: April 1, 2018 To March 31, 2019choiand1No ratings yet

- Kirk Fulford - AASB PresentationDocument33 pagesKirk Fulford - AASB PresentationTrisha Powell CrainNo ratings yet

- Page Industries: Revenue Growth Improves While Margins DeclineDocument8 pagesPage Industries: Revenue Growth Improves While Margins DeclinePuneet367No ratings yet

- FY 2009-10 Annual Results: Investor PresentationDocument34 pagesFY 2009-10 Annual Results: Investor PresentationDujesh KardamNo ratings yet

- Constellation Software IncDocument6 pagesConstellation Software IncSugar RayNo ratings yet

- Q3 & 9M FY21 - Results Presentation: February 2021Document29 pagesQ3 & 9M FY21 - Results Presentation: February 2021Richa CNo ratings yet

- Earnings Estimates Answer q3 2021Document1 pageEarnings Estimates Answer q3 2021LT COL VIKRAM SINGH EPGDIB 2021-22No ratings yet

- Sub: Raymond Limited - Investor Presentation: Rakesh Muljibh Ai DarjiDocument64 pagesSub: Raymond Limited - Investor Presentation: Rakesh Muljibh Ai DarjiSathwik PadamNo ratings yet

- 1Q21 Profit Up 78.1% Q/Q But Outlook Remains Uncertain: SM Prime Holdings, IncDocument9 pages1Q21 Profit Up 78.1% Q/Q But Outlook Remains Uncertain: SM Prime Holdings, IncJajahinaNo ratings yet

- Bwcu Htsqwn00sorvupdk.3Document22 pagesBwcu Htsqwn00sorvupdk.3JoshKernNo ratings yet

- Earnings Presentation - InRetail - Q4'21Document26 pagesEarnings Presentation - InRetail - Q4'21Cecilia Campos VelascoNo ratings yet

- 3Q17 Net Income Down 39.2% Y/y, Outlook Remains Poor: Universal Robina CorporationDocument8 pages3Q17 Net Income Down 39.2% Y/y, Outlook Remains Poor: Universal Robina Corporationherrewt rewterwNo ratings yet

- Assignment Fin420 - Individual & Group EditDocument58 pagesAssignment Fin420 - Individual & Group EditHakim SantiagoNo ratings yet

- Q1FY22 Result Update City Union Bank LTD: Beat On Operational Front Due To Lower Credit CostDocument12 pagesQ1FY22 Result Update City Union Bank LTD: Beat On Operational Front Due To Lower Credit Costforgi mistyNo ratings yet

- V-Guard-Industries - Q4 FY21-Results-PresentationDocument17 pagesV-Guard-Industries - Q4 FY21-Results-PresentationanooppattazhyNo ratings yet

- Fin 440 ReportDocument40 pagesFin 440 Reportsayed.mahmud7No ratings yet

- Accounting Project 2Document8 pagesAccounting Project 2api-661554832No ratings yet

- Dixon InvestorPresentationJan2022Document12 pagesDixon InvestorPresentationJan2022raguramrNo ratings yet

- RLX Technology Inc.: Earnings Presentation Q3 2021Document21 pagesRLX Technology Inc.: Earnings Presentation Q3 2021Faris RahmanNo ratings yet

- Iifl Wealth & Asset Management: Q4 and Full Year FY21 Performance UpdateDocument21 pagesIifl Wealth & Asset Management: Q4 and Full Year FY21 Performance UpdateRohan RautelaNo ratings yet

- Dupont Analysis of Adani Power: Particulars 2021 2020Document3 pagesDupont Analysis of Adani Power: Particulars 2021 2020Ananthasankar SNairNo ratings yet

- Acount ExpensesDocument1 pageAcount ExpenseshxNo ratings yet

- 2022 10 20 PH S CNVRGDocument7 pages2022 10 20 PH S CNVRGValiente RandzNo ratings yet

- TCS Ashish Ranjan: 2.TCS Balance Sheet AnalysisDocument7 pagesTCS Ashish Ranjan: 2.TCS Balance Sheet Analysissnigdha sahayNo ratings yet

- Manappuram Finance Investor PresentationDocument43 pagesManappuram Finance Investor PresentationabmahendruNo ratings yet

- Long Awaited China Revenues Get Booked But FV Reduced As Restrictions TightenDocument8 pagesLong Awaited China Revenues Get Booked But FV Reduced As Restrictions TightenJajahinaNo ratings yet

- My Life at 6ft BelowDocument1 pageMy Life at 6ft Belowvasquez.jabezraphael308129No ratings yet

- Financial DepartmentDocument27 pagesFinancial DepartmentPiyu VyasNo ratings yet

- Earnings Estimates Answer q1 2021Document1 pageEarnings Estimates Answer q1 2021rdtuf ddkdkdNo ratings yet

- Task 1 BigTech TemplateDocument5 pagesTask 1 BigTech Templatedaniyalansari.8425No ratings yet

- Varma Capitals - Modeling TestDocument6 pagesVarma Capitals - Modeling TestSuper FreakNo ratings yet

- Internal Forces G, HDocument6 pagesInternal Forces G, HRui JiaNo ratings yet

- Basic Concepts: Maxfort School-Rohini Chapter - RevenueDocument7 pagesBasic Concepts: Maxfort School-Rohini Chapter - Revenuepiyush rohiraNo ratings yet

- Maxfort School-Rohini Worksheet 1 - Organisation of Data Q1Document3 pagesMaxfort School-Rohini Worksheet 1 - Organisation of Data Q1piyush rohiraNo ratings yet

- The Bmu Mba: A InitiativeDocument19 pagesThe Bmu Mba: A Initiativepiyush rohiraNo ratings yet

- Receipt: Reference No.: 573119 Date:September 16, 2021Document1 pageReceipt: Reference No.: 573119 Date:September 16, 2021piyush rohiraNo ratings yet

- Economics by Piyush Rohira (9999794302) : Om Sai RamDocument7 pagesEconomics by Piyush Rohira (9999794302) : Om Sai Rampiyush rohiraNo ratings yet

- Economics DepreciationDocument3 pagesEconomics DepreciationGeodetic Engineering FilesNo ratings yet

- Module 13 - BusCom - Forex. - StudentsDocument13 pagesModule 13 - BusCom - Forex. - StudentsLuisito CorreaNo ratings yet

- Accounting 3 4 Module 5bDocument2 pagesAccounting 3 4 Module 5bMariel Ann RebancosNo ratings yet

- Risk Management in Banks00001Document52 pagesRisk Management in Banks00001Neha DhuriNo ratings yet

- RLX 4Q23 PresentationDocument26 pagesRLX 4Q23 PresentationrdtrinyNo ratings yet

- Module 3Document47 pagesModule 3Harrold HarryNo ratings yet

- Case Hansson Private LabelDocument15 pagesCase Hansson Private Labelpaul57% (7)

- Lat 7 Knight&lesserDocument5 pagesLat 7 Knight&lesserNadratul Hasanah LubisNo ratings yet

- Laporan Tahunan 2013Document152 pagesLaporan Tahunan 2013NadineNo ratings yet

- Law - Insider - Exlservice Holdings Inc - Merger Agreement by and Among Exlservice Holdings - Filed - 06 06 2011 - ContractDocument89 pagesLaw - Insider - Exlservice Holdings Inc - Merger Agreement by and Among Exlservice Holdings - Filed - 06 06 2011 - ContractSean JJ IntiomaleNo ratings yet

- BEFA Ece, Eee, Eie and Me ReccDocument9 pagesBEFA Ece, Eee, Eie and Me Reccprasad babuNo ratings yet

- Budget Management System User Manual: Department of Treasury and FinanceDocument60 pagesBudget Management System User Manual: Department of Treasury and FinanceChelle P. TenorioNo ratings yet

- Cat OneDocument2 pagesCat Onegerrad cortezNo ratings yet

- MBA 468 2 Credits Objective: F 3 - Management of Banks and Financial InstitutionsDocument3 pagesMBA 468 2 Credits Objective: F 3 - Management of Banks and Financial Institutions05550No ratings yet

- LEAP - Business Finance - Q3 W3 W4Document9 pagesLEAP - Business Finance - Q3 W3 W4Jade MonteverosNo ratings yet

- Financial Accounting (1st Year)Document18 pagesFinancial Accounting (1st Year)RohitNo ratings yet

- Abc Chapter 2Document22 pagesAbc Chapter 2ZNo ratings yet

- Presenatation On Fund Flow Statement: BY: Weena Yancey Kyrmen Singleman DipjoytiDocument22 pagesPresenatation On Fund Flow Statement: BY: Weena Yancey Kyrmen Singleman DipjoytiKuladeepa KrNo ratings yet

- Annual Report 2020Document444 pagesAnnual Report 2020haseen ullahNo ratings yet

- Choice 1-1Document17 pagesChoice 1-1Dagnachew WeldegebrielNo ratings yet

- TML Standalone Results Sept 2023 1Document5 pagesTML Standalone Results Sept 2023 1NagendranNo ratings yet

- Tesla Inc Financial Statements (Extract)Document10 pagesTesla Inc Financial Statements (Extract)Abhishek BatraNo ratings yet

- Actg 5 - Intermediate Accounting 3Document69 pagesActg 5 - Intermediate Accounting 3Christian N Magsino50% (2)

- Partnership Liquidation QuizDocument4 pagesPartnership Liquidation QuizMark Francis Solante100% (1)

- Sample Thesis Financial Performance AnalysisDocument4 pagesSample Thesis Financial Performance Analysissandraahnwashington100% (2)