Download as pdf or txt

You might also like

- Bank of BarodaDocument2 pagesBank of BarodaAdventurous Freak50% (2)

- Series 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)From EverandSeries 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)No ratings yet

- AC Sample Paper 3 Unsolved-1Document10 pagesAC Sample Paper 3 Unsolved-1Appharnha Rs0% (1)

- Mg2451 Engineering Economics and Cost Analysis Questions and AnswersDocument11 pagesMg2451 Engineering Economics and Cost Analysis Questions and AnswersSenthil Kumar100% (1)

- Accountancy QP TEST-1Document11 pagesAccountancy QP TEST-1SomeoneNo ratings yet

- Class 12 EnglishDocument15 pagesClass 12 EnglishKhushi GoyalNo ratings yet

- Prelim Answer KeyDocument13 pagesPrelim Answer KeyLONE WOLF TECHNo ratings yet

- Mycbseguide: Class 12 - Accountancy Sample Paper 01Document15 pagesMycbseguide: Class 12 - Accountancy Sample Paper 01Rohan RughaniNo ratings yet

- PRE-BOARD - 2 (2023-2024) : Grade: XII Marks: 80 Subject: Accountancy Time: 3 HrsDocument8 pagesPRE-BOARD - 2 (2023-2024) : Grade: XII Marks: 80 Subject: Accountancy Time: 3 HrsKaustav DasNo ratings yet

- Mycbseguide: Class 12 - Accountancy Sample Paper 07Document15 pagesMycbseguide: Class 12 - Accountancy Sample Paper 07sneha muralidharanNo ratings yet

- QP Xii Accs PB 1Document7 pagesQP Xii Accs PB 1ansabroxx02No ratings yet

- Free Sample PaperDocument30 pagesFree Sample PapervanshpmlNo ratings yet

- CDEEDocument10 pagesCDEEአዲሱ ዞላNo ratings yet

- 2accountancy Qp-Xii (1) - 230328 - 201201Document11 pages2accountancy Qp-Xii (1) - 230328 - 201201jiya.mehra.2306No ratings yet

- 12 Accountancy QP Prep T1 21Document9 pages12 Accountancy QP Prep T1 21mitaliNo ratings yet

- MOCK PAPER Final 23 24Document16 pagesMOCK PAPER Final 23 24k74pqnqdtcNo ratings yet

- SP Term 1 XII - AcctsDocument14 pagesSP Term 1 XII - AcctsSakshi NagotkarNo ratings yet

- Question 1288284Document11 pagesQuestion 1288284groverpankaj04No ratings yet

- 12 Accountancy PDFDocument7 pages12 Accountancy PDFGaurang AgarwalNo ratings yet

- Answer Key Is Available Only On Grewal Conceptual Learning App' (Available On Playstore and Appstore)Document19 pagesAnswer Key Is Available Only On Grewal Conceptual Learning App' (Available On Playstore and Appstore)Madhumithaa SvNo ratings yet

- 12 Accountancy sp04Document26 pages12 Accountancy sp04vivekdaiv55No ratings yet

- Mycbseguide: Class 12 - Accountancy Sample Paper 03Document15 pagesMycbseguide: Class 12 - Accountancy Sample Paper 03sneha muralidharanNo ratings yet

- Accountancy Sample PaperDocument24 pagesAccountancy Sample PaperJutishmita SaikiaNo ratings yet

- QP Accountancy XIIDocument9 pagesQP Accountancy XIISahil RaikwarNo ratings yet

- ACC 2024 Pre Board PDFDocument12 pagesACC 2024 Pre Board PDFKeshvi.No ratings yet

- Abm 2 Summative TestDocument1 pageAbm 2 Summative TestSarah Mae Aventurado100% (1)

- Sample Paper 2Document15 pagesSample Paper 2TrostingNo ratings yet

- Sample Paper Class 12Document13 pagesSample Paper Class 12akshatbarnwal124No ratings yet

- Accountancy-SQP 23-24Document12 pagesAccountancy-SQP 23-24Ashutosh SinghNo ratings yet

- Class XII - AccountancyDocument11 pagesClass XII - Accountancyumangchh2306No ratings yet

- Xii Accountancy-Practice Paper-2Document16 pagesXii Accountancy-Practice Paper-2sneha muralidharanNo ratings yet

- De CV62 S NX QSB Tetgkk WaDocument24 pagesDe CV62 S NX QSB Tetgkk WaShabanaNo ratings yet

- Accountancy SQPDocument13 pagesAccountancy SQPDeepak Kr. VishwakarmaNo ratings yet

- SQP Accountancy 11Document12 pagesSQP Accountancy 11mamta.bdvrrmaNo ratings yet

- Class XI Accountancy Importaint Questions Sample PaperDocument32 pagesClass XI Accountancy Importaint Questions Sample Papergehlotneeraj11No ratings yet

- Xii Mid Term Exam LJ Acc LJ2021 22Document9 pagesXii Mid Term Exam LJ Acc LJ2021 22Tûshar ThakúrNo ratings yet

- FASD CLASS XII ACCOUNTANCY QPTerm I Pre Board 2021-22Document13 pagesFASD CLASS XII ACCOUNTANCY QPTerm I Pre Board 2021-22aaaaaaffffgNo ratings yet

- Financial Accounting 7Th Edition Harrison Test Bank Full Chapter PDFDocument51 pagesFinancial Accounting 7Th Edition Harrison Test Bank Full Chapter PDFMichaelMurrayewrsd100% (14)

- Financial Accounting 7th Edition Harrison Test BankDocument30 pagesFinancial Accounting 7th Edition Harrison Test Bankxaviadaniela75xv5100% (37)

- 12 Accountancy sp04 230604 170905Document27 pages12 Accountancy sp04 230604 170905RishiNo ratings yet

- QP Accountancy XIIDocument9 pagesQP Accountancy XIITûshar ThakúrNo ratings yet

- Accountancy 1Document12 pagesAccountancy 1sarathsivadamNo ratings yet

- Reg. No 20UCO3CC5 Jamal Mohamed College (Autonomous) Tiruchirappalli - 620 020 Commerce Third Semester Core: Time: Three Hours Maximum: 75 MarksDocument12 pagesReg. No 20UCO3CC5 Jamal Mohamed College (Autonomous) Tiruchirappalli - 620 020 Commerce Third Semester Core: Time: Three Hours Maximum: 75 MarksMuhammad ThanveerNo ratings yet

- Pre-Board Papers With MS AccountancyDocument183 pagesPre-Board Papers With MS Accountancydevanshitandon06No ratings yet

- 12 Acc SP 04aDocument26 pages12 Acc SP 04aठाकुर रुद्र प्रताप सिंहNo ratings yet

- Paper 2 Accountancy 2 2pb QP Set 2Document9 pagesPaper 2 Accountancy 2 2pb QP Set 2Harini NarayananNo ratings yet

- To Buy Recommended Term 1 Book Based On This CBSE Sample Paper, Click HereDocument10 pagesTo Buy Recommended Term 1 Book Based On This CBSE Sample Paper, Click Heresanskriti singhNo ratings yet

- ATS march-2020-insight-part-IIDocument104 pagesATS march-2020-insight-part-IIAromasodun Omobolanle IswatNo ratings yet

- 588c69bdc763b - Sample Paper Accountancy - 230102 - 185610Document7 pages588c69bdc763b - Sample Paper Accountancy - 230102 - 185610sanchitchaudhary431No ratings yet

- Cbleacpu 07Document10 pagesCbleacpu 07sarathsivadamNo ratings yet

- Question Bank - XII Accounts MCQDocument192 pagesQuestion Bank - XII Accounts MCQHarshal KaramchandaniNo ratings yet

- Class 12th Accounts Mock 2Document8 pagesClass 12th Accounts Mock 2Tushar AswaniNo ratings yet

- 12 Accountancy Sp02Document15 pages12 Accountancy Sp02Rahul PareekNo ratings yet

- KVS Jaipur XII ACC QP & MS (2nd PB) 23-24 (SET-3) - 1-9Document9 pagesKVS Jaipur XII ACC QP & MS (2nd PB) 23-24 (SET-3) - 1-9im subbing to everyone subbing to meNo ratings yet

- Model Test Paper-5Document26 pagesModel Test Paper-5Lavagreat The greatNo ratings yet

- Cbleacpu 08Document10 pagesCbleacpu 08Agastya KarnwalNo ratings yet

- 12 Accountancy sp07Document26 pages12 Accountancy sp07vivekdaiv55No ratings yet

- Term I - Class Xii - AccountancyDocument6 pagesTerm I - Class Xii - AccountancyPriyanshu PalNo ratings yet

- 5846SP 2Document10 pages5846SP 2grramyarajaNo ratings yet

- Ac SP 10Document11 pagesAc SP 10komal barotNo ratings yet

- Issue and Redemption of DebenturesDocument21 pagesIssue and Redemption of DebenturesMohammad Tariq AnsariNo ratings yet

- Sample Paper - 1: Book Recommended - Ultimate Book of Accountancy Class 12Document14 pagesSample Paper - 1: Book Recommended - Ultimate Book of Accountancy Class 12TrostingNo ratings yet

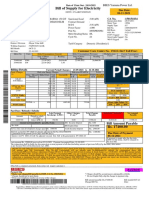

- Bill of Supply For Electricity: Due Date: 06-11-2021Document1 pageBill of Supply For Electricity: Due Date: 06-11-2021dev sharmaNo ratings yet

- 12th Maths Preboard-1 2021Document7 pages12th Maths Preboard-1 2021dev sharmaNo ratings yet

- Revision Test-Mock-1 - XIIDocument7 pagesRevision Test-Mock-1 - XIIdev sharmaNo ratings yet

- Final Guidlies For ExaminationDocument3 pagesFinal Guidlies For Examinationdev sharmaNo ratings yet

- Maths Pre BoardDocument6 pagesMaths Pre Boarddev sharmaNo ratings yet

- Health Ensure Floater - Policy Schedule: Proposer DetailsDocument3 pagesHealth Ensure Floater - Policy Schedule: Proposer DetailsValand NileshNo ratings yet

- Oehmke Opp - A Theory of Socially Responsible InvestmentDocument44 pagesOehmke Opp - A Theory of Socially Responsible InvestmentTimotheos MavropoulosNo ratings yet

- Pillar 2 CompleteDocument278 pagesPillar 2 CompleteAnshul SinghNo ratings yet

- Dealing With COVID-19 - Best Business Practices 180320Document2 pagesDealing With COVID-19 - Best Business Practices 180320Jane SadakaNo ratings yet

- Corporate Finance Ross 10th Edition Solutions ManualDocument14 pagesCorporate Finance Ross 10th Edition Solutions ManualCatherineJohnsonabpg100% (44)

- Taller 4 ActDocument3 pagesTaller 4 ActGabriela BarbosaNo ratings yet

- Wayside Compensation FinalDocument3 pagesWayside Compensation FinalpherlpmilferNo ratings yet

- Joint Stock CompanyDocument2 pagesJoint Stock CompanybijuNo ratings yet

- ND-Developers-Company Profile PDFDocument11 pagesND-Developers-Company Profile PDFÃvíňâšh Ř ŔäťhőďNo ratings yet

- AssignmentDocument4 pagesAssignmentrvkrd4k69jNo ratings yet

- EC3314 Spring PSet 4 SolutionsDocument6 pagesEC3314 Spring PSet 4 Solutionschristina0107No ratings yet

- 1-Technical Appraisal of Infrastructure Development ProjectDocument40 pages1-Technical Appraisal of Infrastructure Development ProjectKhawaja Kashif QadeerNo ratings yet

- Manisha Fincare StatementsDocument2 pagesManisha Fincare Statementsprem yadavNo ratings yet

- Acct Statement - XX5423 - 25102023Document37 pagesAcct Statement - XX5423 - 25102023Praveen SainiNo ratings yet

- ABE Level 5 Diploma in Business ManagementDocument3 pagesABE Level 5 Diploma in Business ManagementS.L.L.CNo ratings yet

- Capm 1Document65 pagesCapm 1api-3814557No ratings yet

- Course Syllabus - Investment ManagementDocument4 pagesCourse Syllabus - Investment ManagementDJ Gonzales100% (1)

- Barrier Options PrimerDocument4 pagesBarrier Options PrimeryukiyurikiNo ratings yet

- CGS Dumanjug 1119-002Document1 pageCGS Dumanjug 1119-002Jona Jane VerdidaNo ratings yet

- 112380-237973 20190331 PDFDocument5 pages112380-237973 20190331 PDFKutty KausyNo ratings yet

- Strategy Tester - TAIGUNDocument90 pagesStrategy Tester - TAIGUNTeamJunTradeezNo ratings yet

- Tendernotice 1 PDFDocument4 pagesTendernotice 1 PDFChit ChitrarasanNo ratings yet

- Loan Agreement TemplateDocument4 pagesLoan Agreement TemplateElisa DahotoyNo ratings yet

- History of Banking in The PhilippinesDocument18 pagesHistory of Banking in The PhilippinesJohn Carmelo Apilado100% (10)

- Business Plan OutlineDocument4 pagesBusiness Plan OutlineMd Jihadul Islam 1911024630No ratings yet

- Pram An Are Tail BankingDocument10 pagesPram An Are Tail BankingDr.I.SelvamaniNo ratings yet

- ReinsurnaceDocument25 pagesReinsurnaceJohn MichaelNo ratings yet

- Financial Advisor PDFDocument7 pagesFinancial Advisor PDFapi-338161039No ratings yet