Download as pdf or txt

You might also like

- Aryaduta JakartaDocument3 pagesAryaduta JakartaDeny Saputra0% (1)

- Sol. Man. Chapter 6 Consolidated Fs Part 3 Acctg For Bus. CombinationsDocument13 pagesSol. Man. Chapter 6 Consolidated Fs Part 3 Acctg For Bus. CombinationsFery Ann100% (5)

- NipeX JQS Application Form v11Document1 pageNipeX JQS Application Form v11Pelican Subsea100% (2)

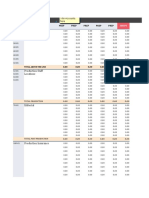

- StudioBinder Film Production Cashflow - PO LogDocument8 pagesStudioBinder Film Production Cashflow - PO Logjeetendra kumarNo ratings yet

- S20 TX ROM Sample AnswersDocument8 pagesS20 TX ROM Sample AnswersKAH MENG KAMNo ratings yet

- F6rom - 2010 - Dec - A ACCADocument10 pagesF6rom - 2010 - Dec - A ACCAgeorgetacaprarescuNo ratings yet

- 2017 Dec Ans-6Document1 page2017 Dec Ans-6何健珩No ratings yet

- F6ROM - 2012 - Dec - A ACCADocument9 pagesF6ROM - 2012 - Dec - A ACCAgeorgetacaprarescuNo ratings yet

- F6rom 2009 Jun ADocument13 pagesF6rom 2009 Jun AInga ȚîgaiNo ratings yet

- TXCHN 2018 Jun ADocument7 pagesTXCHN 2018 Jun AALEX TRANNo ratings yet

- TEST 3 SolutionDocument3 pagesTEST 3 SolutionlusandasithembeloNo ratings yet

- 2015 Dec Ans-8Document1 page2015 Dec Ans-8何健珩No ratings yet

- F6RUS AnsDocument9 pagesF6RUS AnsСветлана КозловаNo ratings yet

- S20 TX POL Sample AnswersDocument6 pagesS20 TX POL Sample AnswersKAH MENG KAMNo ratings yet

- DipIFR 2009 Dec ADocument10 pagesDipIFR 2009 Dec ANitin ChaudharyNo ratings yet

- AnswersDocument5 pagesAnswershfdghdhNo ratings yet

- MODULE 19 - Group Statements - Chapter 5 (Class Question 2 - SS)Document5 pagesMODULE 19 - Group Statements - Chapter 5 (Class Question 2 - SS)Zwivhuya MaimelaNo ratings yet

- F7irl 2008 Dec ADocument10 pagesF7irl 2008 Dec Awaseemhasan85No ratings yet

- TXPOL 2019 Dec ADocument8 pagesTXPOL 2019 Dec AKAH MENG KAMNo ratings yet

- Trs 2020 Sept ADocument9 pagesTrs 2020 Sept ADipesh MagratiNo ratings yet

- Jobb Internet AdvertisingDocument2 pagesJobb Internet Advertisingrethaxaba82No ratings yet

- F6zwe 2015 Dec ADocument8 pagesF6zwe 2015 Dec APhebieon MukwenhaNo ratings yet

- Iluted Arnings Er SDocument2 pagesIluted Arnings Er Ssuhasshinde88No ratings yet

- 2016 Dec Ans-6Document1 page2016 Dec Ans-6何健珩No ratings yet

- AnswersDocument7 pagesAnswersMlambo ConnieNo ratings yet

- TXZAF 2019 Dec ADocument8 pagesTXZAF 2019 Dec AKAH MENG KAMNo ratings yet

- AR Ali 102Document1 pageAR Ali 102Lieder CLNo ratings yet

- Test 1 Suggested SolutionDocument9 pagesTest 1 Suggested SolutionJames MutarauswaNo ratings yet

- Final CMADocument6 pagesFinal CMAManjari AgrawalNo ratings yet

- Cash Flow Illustrations: Exhibit 9.2 Project Cash FlowsDocument14 pagesCash Flow Illustrations: Exhibit 9.2 Project Cash FlowsSchone CoolbearNo ratings yet

- F6rom - 2011 - Jun - A ACCADocument10 pagesF6rom - 2011 - Jun - A ACCAgeorgetacaprarescuNo ratings yet

- MJ17 - Hybrids - P6UK - AMENDED AnswersDocument12 pagesMJ17 - Hybrids - P6UK - AMENDED AnswersHassan jalilNo ratings yet

- 2019 Jun Ans-8Document1 page2019 Jun Ans-8何健珩No ratings yet

- TXUK 2019 SepDec - ADocument10 pagesTXUK 2019 SepDec - AmdNo ratings yet

- F6PKN 2014 Dec ADocument13 pagesF6PKN 2014 Dec ARihamNo ratings yet

- 2015 Jun Ans-8Document1 page2015 Jun Ans-8何健珩No ratings yet

- Financial Statement Analysis - AssignmentDocument6 pagesFinancial Statement Analysis - AssignmentJennifer JosephNo ratings yet

- F6PKN 2014 Jun ADocument14 pagesF6PKN 2014 Jun ARihamNo ratings yet

- 2018 Dec Ans-6-7Document2 pages2018 Dec Ans-6-7何健珩No ratings yet

- F6SGP 2015 Jun AnsDocument9 pagesF6SGP 2015 Jun AnsDrift SirNo ratings yet

- 6int 2008 Dec ADocument6 pages6int 2008 Dec ACharles_Leong_3417No ratings yet

- Peregrine CNC Decision CaseDocument6 pagesPeregrine CNC Decision CaseAsadMughalNo ratings yet

- F6mys 2012 Dec ADocument7 pagesF6mys 2012 Dec AMohd IrfanNo ratings yet

- PrepzFy - LBO - VemptyDocument3 pagesPrepzFy - LBO - VemptykouakouNo ratings yet

- Draft ReportDocument8 pagesDraft Report0264192238No ratings yet

- Discontinued Operations (Disclosure Practice)Document5 pagesDiscontinued Operations (Disclosure Practice)Shaheryar ShahidNo ratings yet

- June 2019 ADocument8 pagesJune 2019 ARohan AbhyankarNo ratings yet

- 2016 Jun Ans-5-6Document2 pages2016 Jun Ans-5-6何健珩No ratings yet

- Txmwi 2018 Jun ADocument6 pagesTxmwi 2018 Jun AangaNo ratings yet

- CH 2 TAXATION ON INDIVIDUALS Slide 43 71Document8 pagesCH 2 TAXATION ON INDIVIDUALS Slide 43 71Casandra Nicole AldecoaNo ratings yet

- p7sgp 2011 Dec QDocument10 pagesp7sgp 2011 Dec QamNo ratings yet

- F6rom - 2011 - Dec - A ACCADocument11 pagesF6rom - 2011 - Dec - A ACCAgeorgetacaprarescuNo ratings yet

- Income Taxes - Crax LTD MemoDocument8 pagesIncome Taxes - Crax LTD Memoandiswa zuluNo ratings yet

- Tax Calculator For Individual Tax Payer: Data Tax Calculation Old Regime New RegimeDocument3 pagesTax Calculator For Individual Tax Payer: Data Tax Calculation Old Regime New RegimeDevi PrasannaNo ratings yet

- Less: Municipal Taxes Paid by Mr. Raj: © The Institute of Chartered Accountants of IndiaDocument11 pagesLess: Municipal Taxes Paid by Mr. Raj: © The Institute of Chartered Accountants of IndiaKetan DedhaNo ratings yet

- Tutorial 2 (3) 3 (E)Document2 pagesTutorial 2 (3) 3 (E)Shan JeefNo ratings yet

- 06 JUNE AnswersDocument13 pages06 JUNE AnswerskhengmaiNo ratings yet

- 2019 Dec Ans-5-6Document2 pages2019 Dec Ans-5-6何健珩No ratings yet

- Flux Net de Lichid Din Activ - de FinantareDocument3 pagesFlux Net de Lichid Din Activ - de FinantareatezorNo ratings yet

- CGG Announces q1 2022 ResultsDocument15 pagesCGG Announces q1 2022 ResultsCa WilNo ratings yet

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryFrom EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Securities Brokerage Revenues World Summary: Market Values & Financials by CountryFrom EverandSecurities Brokerage Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- f6vnm 2016 Dec QDocument10 pagesf6vnm 2016 Dec QHuyền NguyễnNo ratings yet

- Taxation (Vietnam) : Thursday 7 December 2017Document12 pagesTaxation (Vietnam) : Thursday 7 December 2017Huyền NguyễnNo ratings yet

- f6vnm 2017 Dec ADocument6 pagesf6vnm 2017 Dec AHuyền NguyễnNo ratings yet

- f6vnm 2017 Jun ADocument6 pagesf6vnm 2017 Jun AHuyền NguyễnNo ratings yet

- TXVNM 2018 Jun ADocument6 pagesTXVNM 2018 Jun AHuyền NguyễnNo ratings yet

- Reception - DAILY TASK (Training Checklist)Document4 pagesReception - DAILY TASK (Training Checklist)geoff0814No ratings yet

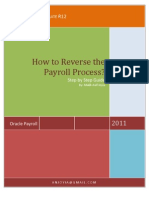

- How To Reverse The Payroll Process?: O E-B S R12Document6 pagesHow To Reverse The Payroll Process?: O E-B S R12Malik Asif Joyia100% (2)

- Penawaran ECU VolvoDocument1 pagePenawaran ECU VolvoAndy TeknikaNo ratings yet

- Income From Other Sources IllustrationDocument5 pagesIncome From Other Sources IllustrationSarvar PathanNo ratings yet

- GENMATHS Financial MathsDocument3 pagesGENMATHS Financial MathsAli HaidarNo ratings yet

- Acct Statement - XX2950 - 08012022Document56 pagesAcct Statement - XX2950 - 08012022shanthi pothuriNo ratings yet

- Flight TicketDocument1 pageFlight TicketnathisonsNo ratings yet

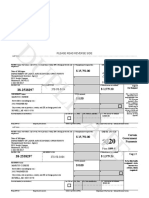

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)umair BaigNo ratings yet

- Form 1099GDocument2 pagesForm 1099GMarcus KreseNo ratings yet

- ACH Quick Guide 0914Document5 pagesACH Quick Guide 0914aplawNo ratings yet

- Benefits Received by Employees SeparatedDocument2 pagesBenefits Received by Employees Separatedrian.lee.b.tiangcoNo ratings yet

- FBB BrochureDocument2 pagesFBB BrochureDevdutta MajiNo ratings yet

- 76-78 Case Digest-TaxDocument8 pages76-78 Case Digest-TaxMique VillanuevaNo ratings yet

- Solution Responsibility Accounting Pratice ProblemDocument3 pagesSolution Responsibility Accounting Pratice ProblemBeomiNo ratings yet

- Voucher Jan Dec16Document4 pagesVoucher Jan Dec16Lovely Eulin FulgarNo ratings yet

- PDF - 2669819112.schedule of Service Charges FinacleDocument15 pagesPDF - 2669819112.schedule of Service Charges FinacleNirmal singhNo ratings yet

- Display Organization: 10172, Role FI CustomerDocument1 pageDisplay Organization: 10172, Role FI CustomerFarahNo ratings yet

- Abayao-Worwor Furniture ShopDocument4 pagesAbayao-Worwor Furniture ShopBen Carlo RamosNo ratings yet

- Gondwana Collection Namibia Terms and ConditionsDocument2 pagesGondwana Collection Namibia Terms and ConditionsAnton LungameniNo ratings yet

- How I Was Forced Into IncestDocument2 pagesHow I Was Forced Into IncestDebolina DeyNo ratings yet

- A Crash Course In: Classical MusicDocument4 pagesA Crash Course In: Classical Musicapi-210427398No ratings yet

- Chapter 7 - Banking Monies RevceivedDocument21 pagesChapter 7 - Banking Monies Revceivedshemida100% (3)

- Western Leyte College of Ormoc, Inc. Prelim Exam in Taxation I October 10, 2020Document2 pagesWestern Leyte College of Ormoc, Inc. Prelim Exam in Taxation I October 10, 2020Marc William SorianoNo ratings yet

- 1PZ2U8Document1 page1PZ2U8algumhyNo ratings yet

- Econmics SyllabusDocument3 pagesEconmics SyllabusjimmyNo ratings yet

- Up White Paper On Tax and GST Gas MarketDocument16 pagesUp White Paper On Tax and GST Gas MarketSunny KhavleNo ratings yet

- 0245 (22-23) (Harshpriya)Document1 page0245 (22-23) (Harshpriya)Ravikant MishraNo ratings yet