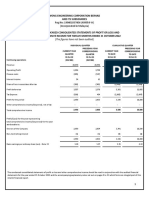

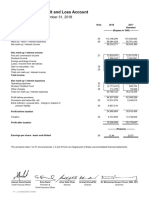

Statement of Profit and Loss: Particulars Notes For The Year Ending On 31st March 2020

Statement of Profit and Loss: Particulars Notes For The Year Ending On 31st March 2020

You might also like

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- FINA 4383 QuizzesDocument10 pagesFINA 4383 QuizzesSamantha Luna100% (1)

- Quizzes - Chapter 2 - Statement of Comprehensive IncomeDocument6 pagesQuizzes - Chapter 2 - Statement of Comprehensive IncomeAmie Jane Miranda100% (3)

- Analysis of Financial State MentDocument13 pagesAnalysis of Financial State MentAbdul RehmanNo ratings yet

- Standalone Profit LossDocument1 pageStandalone Profit LossrahulNo ratings yet

- ITC-Profit-Loss 2017 PDFDocument1 pageITC-Profit-Loss 2017 PDFShristi GutgutiaNo ratings yet

- Extracted Pages From PVR LTD - 20Document1 pageExtracted Pages From PVR LTD - 20jadgugNo ratings yet

- ITC Report and Accounts 2023 185Document1 pageITC Report and Accounts 2023 185Nishith RanjanNo ratings yet

- InfoEdge Annual Report 2023 1Document1 pageInfoEdge Annual Report 2023 1Aditya RoyNo ratings yet

- CA Inter - Advanced Accoounting - Chapter 8 & 9 - AKDocument4 pagesCA Inter - Advanced Accoounting - Chapter 8 & 9 - AKSaraswathi ShanmugarajaNo ratings yet

- Statement of Profit and LossDocument1 pageStatement of Profit and LossAjit singhNo ratings yet

- 20 03 12 Financial Statements of RWE AG 2019Document66 pages20 03 12 Financial Statements of RWE AG 2019HoangNo ratings yet

- AR Ali 102Document1 pageAR Ali 102Lieder CLNo ratings yet

- Reliance Capital Limited: Vu VM of ' ('Document4 pagesReliance Capital Limited: Vu VM of ' ('Moneylife Foundation100% (1)

- cpr03 Lesechos 16165 964001 Consolidated Financial Statements SE 2020Document66 pagescpr03 Lesechos 16165 964001 Consolidated Financial Statements SE 2020kjbewdjNo ratings yet

- Profit and LossDocument1 pageProfit and LossYagika Jagnani100% (1)

- Consolidated Balance Sheet For Hindustan Unilever LTDDocument11 pagesConsolidated Balance Sheet For Hindustan Unilever LTDMohit ChughNo ratings yet

- AFM Project Sec J Group 10Document32 pagesAFM Project Sec J Group 10J40Santhosh KrishnaNo ratings yet

- UBA - June2021 FN StatementsDocument2 pagesUBA - June2021 FN StatementsFuaad DodooNo ratings yet

- Consolidated Financial Statements As of December 31 2020Document86 pagesConsolidated Financial Statements As of December 31 2020Raka AryawanNo ratings yet

- Vicom 1Document10 pagesVicom 1johnsolarpanelsNo ratings yet

- Statemnt of Profit and LossDocument1 pageStatemnt of Profit and LossRutuja shindeNo ratings yet

- AFM Project 86 - 87 1Document20 pagesAFM Project 86 - 87 1Rohan ShekarNo ratings yet

- Supplementary Accounting Statement ECPLDocument15 pagesSupplementary Accounting Statement ECPLdeepNo ratings yet

- Plaquette Annuelle 31 Decembre 2022 EN VdefsDocument80 pagesPlaquette Annuelle 31 Decembre 2022 EN VdefsAbdcNo ratings yet

- FinalDocument20 pagesFinalMuhammad Aminul HoqueNo ratings yet

- 7050 Wong QR 2022-10-31 Wecfrq4fy2022 - 2122247081Document13 pages7050 Wong QR 2022-10-31 Wecfrq4fy2022 - 2122247081Quint WongNo ratings yet

- Financial Statements Kodak Q3 2022Document3 pagesFinancial Statements Kodak Q3 2022GARCÍA GUTIERREZ NOEMINo ratings yet

- JHM 1Qtr21 Financial Report (Amendment)Document13 pagesJHM 1Qtr21 Financial Report (Amendment)Ooi Gim SengNo ratings yet

- Statement of Profit and Loss For The Year Ended 31St March 2017Document1 pageStatement of Profit and Loss For The Year Ended 31St March 2017Himanshu DuttaNo ratings yet

- Directors Report FY20Document49 pagesDirectors Report FY20Rajeshwari ShuklaNo ratings yet

- Selecta Group - Q1 2023 Financial StatementsDocument22 pagesSelecta Group - Q1 2023 Financial StatementsJean Claude HechtNo ratings yet

- Plaquette Annuelle 31 Decembre 2021 ENDocument85 pagesPlaquette Annuelle 31 Decembre 2021 ENHari ShankarNo ratings yet

- Indigo Income STMT 1Document1 pageIndigo Income STMT 1deepzNo ratings yet

- Consolidated Statement of Profit and LossDocument9 pagesConsolidated Statement of Profit and LossHrushikesh DahaleNo ratings yet

- KIL Result June-2022Document3 pagesKIL Result June-2022akshay kausaleNo ratings yet

- Aji 202206 Q1Document4 pagesAji 202206 Q1Al TanNo ratings yet

- Choo Bee Metal Industries Berhad (10587-A)Document18 pagesChoo Bee Metal Industries Berhad (10587-A)Iqbal YusufNo ratings yet

- Statement of Profit and Loss: For The Year Ended 31st March, 2021Document2 pagesStatement of Profit and Loss: For The Year Ended 31st March, 2021Only For StudyNo ratings yet

- Statement of Profit and LossDocument1 pageStatement of Profit and LossAbhilash JackNo ratings yet

- Report Q1 2010Document24 pagesReport Q1 2010Frode HaukenesNo ratings yet

- Kering V2Document6 pagesKering V2Pranav HansonNo ratings yet

- Exhibit 1: BALANCE SHEET of VIP Industries As at March 31Document2 pagesExhibit 1: BALANCE SHEET of VIP Industries As at March 31Neelu AggrawalNo ratings yet

- Indian Oil (CFS) Profit and Loss - 2023Document1 pageIndian Oil (CFS) Profit and Loss - 2023kavyagarg8542No ratings yet

- Integrated Report and Annual Accounts 2016-17-175 175Document1 pageIntegrated Report and Annual Accounts 2016-17-175 175Sanju VisuNo ratings yet

- Raymond Limited Financial StatementsDocument85 pagesRaymond Limited Financial StatementsVinay KukrejaNo ratings yet

- MMFSL Fin Results Q1 F2019 LODR Clause 33 FianlDocument2 pagesMMFSL Fin Results Q1 F2019 LODR Clause 33 FianlIMAM JAVOORNo ratings yet

- Consolidated Fi Nancial Statements and Notes To The Consolidated Fi Nancial StatementsDocument5 pagesConsolidated Fi Nancial Statements and Notes To The Consolidated Fi Nancial Statementsria septiani putriNo ratings yet

- 4 Years of Financial Data - v4Document25 pages4 Years of Financial Data - v4khusus downloadNo ratings yet

- 6 Supplementary Accounting StatementDocument16 pages6 Supplementary Accounting Statementshrianand0248No ratings yet

- Statement of Income and ExpenditureDocument2 pagesStatement of Income and Expenditureyogendra kumarNo ratings yet

- Financial StatementsDocument92 pagesFinancial StatementsJaspreet KaurNo ratings yet

- Extracted Pages From PVR LTD - 20Document2 pagesExtracted Pages From PVR LTD - 20jadgugNo ratings yet

- UBL Annual Report 2018-76Document1 pageUBL Annual Report 2018-76IFRS LabNo ratings yet

- 2 Worked ExamplesDocument20 pages2 Worked ExamplesJester LabanNo ratings yet

- Impce Bs m23 For SignDocument15 pagesImpce Bs m23 For SignauditNo ratings yet

- FCMB Group PLC - Quarter 1 - Financial Statement For 2024 Financial Statements April 2024Document49 pagesFCMB Group PLC - Quarter 1 - Financial Statement For 2024 Financial Statements April 2024frederick aivborayeNo ratings yet

- DPL Annual Report 2022 23 Pages 2Document1 pageDPL Annual Report 2022 23 Pages 2workf17hoursformeNo ratings yet

- 15 March Worksheet - Cash FlowDocument7 pages15 March Worksheet - Cash FlowkeithsimphiweNo ratings yet

- Fs Credo Ye 2017Document38 pagesFs Credo Ye 2017AzerNo ratings yet

- Ratio Analysis of Lanka Ashok Leyland PLCDocument6 pagesRatio Analysis of Lanka Ashok Leyland PLCThe MutantzNo ratings yet

- Audited Consolidated-Statements - PAL 2022Document10 pagesAudited Consolidated-Statements - PAL 2022P patelNo ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Himadri: Himadri Speciality Chemical LTDDocument16 pagesHimadri: Himadri Speciality Chemical LTDdineshkumar1234No ratings yet

- Dirac Precision Instumentation: Make - SKF, NTN, Fag, Koyo, JapanDocument9 pagesDirac Precision Instumentation: Make - SKF, NTN, Fag, Koyo, Japandineshkumar1234No ratings yet

- Pipe DesignDocument48 pagesPipe Designdineshkumar1234No ratings yet

- Design Basis Rev 0 - Static EqptDocument57 pagesDesign Basis Rev 0 - Static Eqptdineshkumar1234100% (1)

- Humanitarian Voice in The Poems of Jayanta MahapatraDocument6 pagesHumanitarian Voice in The Poems of Jayanta Mahapatradineshkumar1234No ratings yet

- 2 & 3 B H K Sector 144, NoidaDocument9 pages2 & 3 B H K Sector 144, Noidadineshkumar1234No ratings yet

- Global Transfer PricesDocument285 pagesGlobal Transfer PricesDiana AlexandraNo ratings yet

- Balance Sheet StartUpDocument1 pageBalance Sheet StartUpHercule P OirotNo ratings yet

- Diagnostic Exam Accounting 1.1 AKDocument14 pagesDiagnostic Exam Accounting 1.1 AKRobert CastilloNo ratings yet

- QP XI AccountancyDocument13 pagesQP XI AccountancySanjay Panicker100% (1)

- Mercury Mining Investment LTD - Audited Reports For 2022Document16 pagesMercury Mining Investment LTD - Audited Reports For 2022tankodanjumacNo ratings yet

- 5.0 Financial Plan: Chapter FiveDocument6 pages5.0 Financial Plan: Chapter FiveJane WangariNo ratings yet

- Q & A Marathon DT Question Bank Part 1Document181 pagesQ & A Marathon DT Question Bank Part 1Gagan SahuNo ratings yet

- Unit 5Document43 pagesUnit 5sujal mundhraNo ratings yet

- CF02 TaskDocument7 pagesCF02 TaskScribdTranslationsNo ratings yet

- Union Budget - 2023-24 - Direct Tax Proposals (K&Co)Document54 pagesUnion Budget - 2023-24 - Direct Tax Proposals (K&Co)Charul ChhajerNo ratings yet

- Axis Bank LTD Payslip For The Month of May - 2021Document2 pagesAxis Bank LTD Payslip For The Month of May - 2021Suman DasNo ratings yet

- Assignment # 2 MBA Financial and Managerial AccountingDocument7 pagesAssignment # 2 MBA Financial and Managerial AccountingSelamawit MekonnenNo ratings yet

- FAR 1 AssetsDocument15 pagesFAR 1 AssetsSky LeeNo ratings yet

- Assignment 1 FS BORJAL, Mary Ymanuella S.Document2 pagesAssignment 1 FS BORJAL, Mary Ymanuella S.Mary Ymanuella BorjalNo ratings yet

- Furnmart Ltd. (FURNMART-BW) - Interim Report For Period End 31-Jan-2018 (English) PDFDocument1 pageFurnmart Ltd. (FURNMART-BW) - Interim Report For Period End 31-Jan-2018 (English) PDFmisterbeNo ratings yet

- AC59 - Final ExamDocument16 pagesAC59 - Final ExamFlorie May HizoNo ratings yet

- FBS 112 Exam 2019Document10 pagesFBS 112 Exam 2019siyoliseworkNo ratings yet

- Spotify Case Fsa BusinessDocument3 pagesSpotify Case Fsa Businessjuan.amoros.ja65No ratings yet

- Tax CalculatorDocument1 pageTax CalculatorLovish VatwaniNo ratings yet

- Rhombus Energy v. CIRDocument2 pagesRhombus Energy v. CIRBernadette RacadioNo ratings yet

- Daftar Nama Akun PT JayatamaDocument2 pagesDaftar Nama Akun PT Jayatamastriii906No ratings yet

- CLWTAXN MODULE 5 Income Taxation of Individuals Notes v022023-1-1Document7 pagesCLWTAXN MODULE 5 Income Taxation of Individuals Notes v022023-1-1kdcngan162No ratings yet

- Market X Ls FunctionsDocument73 pagesMarket X Ls FunctionsNaresh KumarNo ratings yet

- Tax Card TY 2022Document8 pagesTax Card TY 2022princecharming14No ratings yet

- Advanced Accounting 12th Edition Beams Test Bank 1Document31 pagesAdvanced Accounting 12th Edition Beams Test Bank 1leslieNo ratings yet

- Form 16-2021-2022Document12 pagesForm 16-2021-2022Kunal BansodeNo ratings yet

- Concept of Tax Planning and Specific Management Decisions: CHANIKA GOEL (1886532) RITIKA SACHDEVA (1886586)Document34 pagesConcept of Tax Planning and Specific Management Decisions: CHANIKA GOEL (1886532) RITIKA SACHDEVA (1886586)parvati anilkumarNo ratings yet

Download as pdf or txt

You might also like

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- FINA 4383 QuizzesDocument10 pagesFINA 4383 QuizzesSamantha Luna100% (1)

- Quizzes - Chapter 2 - Statement of Comprehensive IncomeDocument6 pagesQuizzes - Chapter 2 - Statement of Comprehensive IncomeAmie Jane Miranda100% (3)

- Analysis of Financial State MentDocument13 pagesAnalysis of Financial State MentAbdul RehmanNo ratings yet

- Standalone Profit LossDocument1 pageStandalone Profit LossrahulNo ratings yet

- ITC-Profit-Loss 2017 PDFDocument1 pageITC-Profit-Loss 2017 PDFShristi GutgutiaNo ratings yet

- Extracted Pages From PVR LTD - 20Document1 pageExtracted Pages From PVR LTD - 20jadgugNo ratings yet

- ITC Report and Accounts 2023 185Document1 pageITC Report and Accounts 2023 185Nishith RanjanNo ratings yet

- InfoEdge Annual Report 2023 1Document1 pageInfoEdge Annual Report 2023 1Aditya RoyNo ratings yet

- CA Inter - Advanced Accoounting - Chapter 8 & 9 - AKDocument4 pagesCA Inter - Advanced Accoounting - Chapter 8 & 9 - AKSaraswathi ShanmugarajaNo ratings yet

- Statement of Profit and LossDocument1 pageStatement of Profit and LossAjit singhNo ratings yet

- 20 03 12 Financial Statements of RWE AG 2019Document66 pages20 03 12 Financial Statements of RWE AG 2019HoangNo ratings yet

- AR Ali 102Document1 pageAR Ali 102Lieder CLNo ratings yet

- Reliance Capital Limited: Vu VM of ' ('Document4 pagesReliance Capital Limited: Vu VM of ' ('Moneylife Foundation100% (1)

- cpr03 Lesechos 16165 964001 Consolidated Financial Statements SE 2020Document66 pagescpr03 Lesechos 16165 964001 Consolidated Financial Statements SE 2020kjbewdjNo ratings yet

- Profit and LossDocument1 pageProfit and LossYagika Jagnani100% (1)

- Consolidated Balance Sheet For Hindustan Unilever LTDDocument11 pagesConsolidated Balance Sheet For Hindustan Unilever LTDMohit ChughNo ratings yet

- AFM Project Sec J Group 10Document32 pagesAFM Project Sec J Group 10J40Santhosh KrishnaNo ratings yet

- UBA - June2021 FN StatementsDocument2 pagesUBA - June2021 FN StatementsFuaad DodooNo ratings yet

- Consolidated Financial Statements As of December 31 2020Document86 pagesConsolidated Financial Statements As of December 31 2020Raka AryawanNo ratings yet

- Vicom 1Document10 pagesVicom 1johnsolarpanelsNo ratings yet

- Statemnt of Profit and LossDocument1 pageStatemnt of Profit and LossRutuja shindeNo ratings yet

- AFM Project 86 - 87 1Document20 pagesAFM Project 86 - 87 1Rohan ShekarNo ratings yet

- Supplementary Accounting Statement ECPLDocument15 pagesSupplementary Accounting Statement ECPLdeepNo ratings yet

- Plaquette Annuelle 31 Decembre 2022 EN VdefsDocument80 pagesPlaquette Annuelle 31 Decembre 2022 EN VdefsAbdcNo ratings yet

- FinalDocument20 pagesFinalMuhammad Aminul HoqueNo ratings yet

- 7050 Wong QR 2022-10-31 Wecfrq4fy2022 - 2122247081Document13 pages7050 Wong QR 2022-10-31 Wecfrq4fy2022 - 2122247081Quint WongNo ratings yet

- Financial Statements Kodak Q3 2022Document3 pagesFinancial Statements Kodak Q3 2022GARCÍA GUTIERREZ NOEMINo ratings yet

- JHM 1Qtr21 Financial Report (Amendment)Document13 pagesJHM 1Qtr21 Financial Report (Amendment)Ooi Gim SengNo ratings yet

- Statement of Profit and Loss For The Year Ended 31St March 2017Document1 pageStatement of Profit and Loss For The Year Ended 31St March 2017Himanshu DuttaNo ratings yet

- Directors Report FY20Document49 pagesDirectors Report FY20Rajeshwari ShuklaNo ratings yet

- Selecta Group - Q1 2023 Financial StatementsDocument22 pagesSelecta Group - Q1 2023 Financial StatementsJean Claude HechtNo ratings yet

- Plaquette Annuelle 31 Decembre 2021 ENDocument85 pagesPlaquette Annuelle 31 Decembre 2021 ENHari ShankarNo ratings yet

- Indigo Income STMT 1Document1 pageIndigo Income STMT 1deepzNo ratings yet

- Consolidated Statement of Profit and LossDocument9 pagesConsolidated Statement of Profit and LossHrushikesh DahaleNo ratings yet

- KIL Result June-2022Document3 pagesKIL Result June-2022akshay kausaleNo ratings yet

- Aji 202206 Q1Document4 pagesAji 202206 Q1Al TanNo ratings yet

- Choo Bee Metal Industries Berhad (10587-A)Document18 pagesChoo Bee Metal Industries Berhad (10587-A)Iqbal YusufNo ratings yet

- Statement of Profit and Loss: For The Year Ended 31st March, 2021Document2 pagesStatement of Profit and Loss: For The Year Ended 31st March, 2021Only For StudyNo ratings yet

- Statement of Profit and LossDocument1 pageStatement of Profit and LossAbhilash JackNo ratings yet

- Report Q1 2010Document24 pagesReport Q1 2010Frode HaukenesNo ratings yet

- Kering V2Document6 pagesKering V2Pranav HansonNo ratings yet

- Exhibit 1: BALANCE SHEET of VIP Industries As at March 31Document2 pagesExhibit 1: BALANCE SHEET of VIP Industries As at March 31Neelu AggrawalNo ratings yet

- Indian Oil (CFS) Profit and Loss - 2023Document1 pageIndian Oil (CFS) Profit and Loss - 2023kavyagarg8542No ratings yet

- Integrated Report and Annual Accounts 2016-17-175 175Document1 pageIntegrated Report and Annual Accounts 2016-17-175 175Sanju VisuNo ratings yet

- Raymond Limited Financial StatementsDocument85 pagesRaymond Limited Financial StatementsVinay KukrejaNo ratings yet

- MMFSL Fin Results Q1 F2019 LODR Clause 33 FianlDocument2 pagesMMFSL Fin Results Q1 F2019 LODR Clause 33 FianlIMAM JAVOORNo ratings yet

- Consolidated Fi Nancial Statements and Notes To The Consolidated Fi Nancial StatementsDocument5 pagesConsolidated Fi Nancial Statements and Notes To The Consolidated Fi Nancial Statementsria septiani putriNo ratings yet

- 4 Years of Financial Data - v4Document25 pages4 Years of Financial Data - v4khusus downloadNo ratings yet

- 6 Supplementary Accounting StatementDocument16 pages6 Supplementary Accounting Statementshrianand0248No ratings yet

- Statement of Income and ExpenditureDocument2 pagesStatement of Income and Expenditureyogendra kumarNo ratings yet

- Financial StatementsDocument92 pagesFinancial StatementsJaspreet KaurNo ratings yet

- Extracted Pages From PVR LTD - 20Document2 pagesExtracted Pages From PVR LTD - 20jadgugNo ratings yet

- UBL Annual Report 2018-76Document1 pageUBL Annual Report 2018-76IFRS LabNo ratings yet

- 2 Worked ExamplesDocument20 pages2 Worked ExamplesJester LabanNo ratings yet

- Impce Bs m23 For SignDocument15 pagesImpce Bs m23 For SignauditNo ratings yet

- FCMB Group PLC - Quarter 1 - Financial Statement For 2024 Financial Statements April 2024Document49 pagesFCMB Group PLC - Quarter 1 - Financial Statement For 2024 Financial Statements April 2024frederick aivborayeNo ratings yet

- DPL Annual Report 2022 23 Pages 2Document1 pageDPL Annual Report 2022 23 Pages 2workf17hoursformeNo ratings yet

- 15 March Worksheet - Cash FlowDocument7 pages15 March Worksheet - Cash FlowkeithsimphiweNo ratings yet

- Fs Credo Ye 2017Document38 pagesFs Credo Ye 2017AzerNo ratings yet

- Ratio Analysis of Lanka Ashok Leyland PLCDocument6 pagesRatio Analysis of Lanka Ashok Leyland PLCThe MutantzNo ratings yet

- Audited Consolidated-Statements - PAL 2022Document10 pagesAudited Consolidated-Statements - PAL 2022P patelNo ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Himadri: Himadri Speciality Chemical LTDDocument16 pagesHimadri: Himadri Speciality Chemical LTDdineshkumar1234No ratings yet

- Dirac Precision Instumentation: Make - SKF, NTN, Fag, Koyo, JapanDocument9 pagesDirac Precision Instumentation: Make - SKF, NTN, Fag, Koyo, Japandineshkumar1234No ratings yet

- Pipe DesignDocument48 pagesPipe Designdineshkumar1234No ratings yet

- Design Basis Rev 0 - Static EqptDocument57 pagesDesign Basis Rev 0 - Static Eqptdineshkumar1234100% (1)

- Humanitarian Voice in The Poems of Jayanta MahapatraDocument6 pagesHumanitarian Voice in The Poems of Jayanta Mahapatradineshkumar1234No ratings yet

- 2 & 3 B H K Sector 144, NoidaDocument9 pages2 & 3 B H K Sector 144, Noidadineshkumar1234No ratings yet

- Global Transfer PricesDocument285 pagesGlobal Transfer PricesDiana AlexandraNo ratings yet

- Balance Sheet StartUpDocument1 pageBalance Sheet StartUpHercule P OirotNo ratings yet

- Diagnostic Exam Accounting 1.1 AKDocument14 pagesDiagnostic Exam Accounting 1.1 AKRobert CastilloNo ratings yet

- QP XI AccountancyDocument13 pagesQP XI AccountancySanjay Panicker100% (1)

- Mercury Mining Investment LTD - Audited Reports For 2022Document16 pagesMercury Mining Investment LTD - Audited Reports For 2022tankodanjumacNo ratings yet

- 5.0 Financial Plan: Chapter FiveDocument6 pages5.0 Financial Plan: Chapter FiveJane WangariNo ratings yet

- Q & A Marathon DT Question Bank Part 1Document181 pagesQ & A Marathon DT Question Bank Part 1Gagan SahuNo ratings yet

- Unit 5Document43 pagesUnit 5sujal mundhraNo ratings yet

- CF02 TaskDocument7 pagesCF02 TaskScribdTranslationsNo ratings yet

- Union Budget - 2023-24 - Direct Tax Proposals (K&Co)Document54 pagesUnion Budget - 2023-24 - Direct Tax Proposals (K&Co)Charul ChhajerNo ratings yet

- Axis Bank LTD Payslip For The Month of May - 2021Document2 pagesAxis Bank LTD Payslip For The Month of May - 2021Suman DasNo ratings yet

- Assignment # 2 MBA Financial and Managerial AccountingDocument7 pagesAssignment # 2 MBA Financial and Managerial AccountingSelamawit MekonnenNo ratings yet

- FAR 1 AssetsDocument15 pagesFAR 1 AssetsSky LeeNo ratings yet

- Assignment 1 FS BORJAL, Mary Ymanuella S.Document2 pagesAssignment 1 FS BORJAL, Mary Ymanuella S.Mary Ymanuella BorjalNo ratings yet

- Furnmart Ltd. (FURNMART-BW) - Interim Report For Period End 31-Jan-2018 (English) PDFDocument1 pageFurnmart Ltd. (FURNMART-BW) - Interim Report For Period End 31-Jan-2018 (English) PDFmisterbeNo ratings yet

- AC59 - Final ExamDocument16 pagesAC59 - Final ExamFlorie May HizoNo ratings yet

- FBS 112 Exam 2019Document10 pagesFBS 112 Exam 2019siyoliseworkNo ratings yet

- Spotify Case Fsa BusinessDocument3 pagesSpotify Case Fsa Businessjuan.amoros.ja65No ratings yet

- Tax CalculatorDocument1 pageTax CalculatorLovish VatwaniNo ratings yet

- Rhombus Energy v. CIRDocument2 pagesRhombus Energy v. CIRBernadette RacadioNo ratings yet

- Daftar Nama Akun PT JayatamaDocument2 pagesDaftar Nama Akun PT Jayatamastriii906No ratings yet

- CLWTAXN MODULE 5 Income Taxation of Individuals Notes v022023-1-1Document7 pagesCLWTAXN MODULE 5 Income Taxation of Individuals Notes v022023-1-1kdcngan162No ratings yet

- Market X Ls FunctionsDocument73 pagesMarket X Ls FunctionsNaresh KumarNo ratings yet

- Tax Card TY 2022Document8 pagesTax Card TY 2022princecharming14No ratings yet

- Advanced Accounting 12th Edition Beams Test Bank 1Document31 pagesAdvanced Accounting 12th Edition Beams Test Bank 1leslieNo ratings yet

- Form 16-2021-2022Document12 pagesForm 16-2021-2022Kunal BansodeNo ratings yet

- Concept of Tax Planning and Specific Management Decisions: CHANIKA GOEL (1886532) RITIKA SACHDEVA (1886586)Document34 pagesConcept of Tax Planning and Specific Management Decisions: CHANIKA GOEL (1886532) RITIKA SACHDEVA (1886586)parvati anilkumarNo ratings yet