Download as pdf or txt

You might also like

- Equirus Securities Initiating Coverage GAEX 08.01.2018-Gujarat Ambuja ExportsDocument41 pagesEquirus Securities Initiating Coverage GAEX 08.01.2018-Gujarat Ambuja Exportsrchawdhry123100% (2)

- Strama Research PaperDocument17 pagesStrama Research PaperKLD C100% (1)

- NILKAMAL LTD Detail ReportDocument14 pagesNILKAMAL LTD Detail Report5309 HARSH MAKADIYANo ratings yet

- Britannia Industries LTD: Index DetailsDocument13 pagesBritannia Industries LTD: Index DetailsÀbhîñáy Sîñgh RâjpôôtNo ratings yet

- Raymond LTD Detail ReportDocument13 pagesRaymond LTD Detail ReportShivana GuruNo ratings yet

- Seya Industries LTD Detail ReportDocument15 pagesSeya Industries LTD Detail ReportvishnuNo ratings yet

- Zuari Agro Chemicals Limited: Index DetailsDocument10 pagesZuari Agro Chemicals Limited: Index DetailsHarshita KumariNo ratings yet

- JAIN IRRIGATION SYSTEMS LTD Detail ReportDocument13 pagesJAIN IRRIGATION SYSTEMS LTD Detail ReportRishabh RanaNo ratings yet

- The Phoenix Mills LTD Detail ReportDocument13 pagesThe Phoenix Mills LTD Detail ReportdarshanmaldeNo ratings yet

- Rubfila International LTD: Sector BSE Code Face Value 52wk. High / Low (RS.) Volume (2wk. Avg.) Market Cap (Rs. in MN.)Document11 pagesRubfila International LTD: Sector BSE Code Face Value 52wk. High / Low (RS.) Volume (2wk. Avg.) Market Cap (Rs. in MN.)Reena ShahNo ratings yet

- Mphasis LTD: Index DetailsDocument11 pagesMphasis LTD: Index DetailsAshokNo ratings yet

- Shemaroo Entertainment LTD: Index DetailsDocument14 pagesShemaroo Entertainment LTD: Index DetailsAshokNo ratings yet

- KUANTUM PAPERS 30aug17 Research ReportDocument12 pagesKUANTUM PAPERS 30aug17 Research ReportSantosh KadamNo ratings yet

- Mastek LTD: Index DetailsDocument12 pagesMastek LTD: Index DetailsAshokNo ratings yet

- Swaraj Engines LTD: Index DetailsDocument11 pagesSwaraj Engines LTD: Index DetailsTavi SharmaNo ratings yet

- Supreme Industries.madhavanDocument16 pagesSupreme Industries.madhavanAbishek RNo ratings yet

- Seshasayee Paper Boards LTD Detail ReportDocument11 pagesSeshasayee Paper Boards LTD Detail ReportKarthikNo ratings yet

- Escorts LTD: Index DetailsDocument15 pagesEscorts LTD: Index DetailsVivek MavillaNo ratings yet

- L.g.balakrishnan Bros - LTD Detail ReportDocument11 pagesL.g.balakrishnan Bros - LTD Detail Reportsai venkatNo ratings yet

- Precision Wires India LTD Detail ReportDocument11 pagesPrecision Wires India LTD Detail ReportTILAK PATELNo ratings yet

- Gulf Oil Lubricants India LTD: Index DetailsDocument13 pagesGulf Oil Lubricants India LTD: Index DetailsADNo ratings yet

- Avenue Supermarts LTDDocument11 pagesAvenue Supermarts LTDashok yadavNo ratings yet

- Corporate Performance Q3 FY19Document12 pagesCorporate Performance Q3 FY19Gautam MehtaNo ratings yet

- DFM Foods LTD: Index DetailsDocument11 pagesDFM Foods LTD: Index DetailsAshokNo ratings yet

- Berger Paints India LTD Detail Report PDFDocument12 pagesBerger Paints India LTD Detail Report PDFSahil GargNo ratings yet

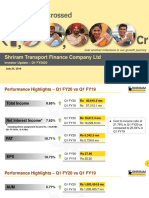

- Shriram Transport Finance Co. LTD: Index DetailsDocument11 pagesShriram Transport Finance Co. LTD: Index DetailsBapi KumarNo ratings yet

- ITC Limited: Resilient Quarter Amidst Weak Industry DemandDocument5 pagesITC Limited: Resilient Quarter Amidst Weak Industry DemandGeebeeNo ratings yet

- Simbhaoli Sugars LTD.: Stakeholders Empowerment ServicesDocument9 pagesSimbhaoli Sugars LTD.: Stakeholders Empowerment ServicesvishalNo ratings yet

- Simbhaoli Sugars LTD.: Stakeholders Empowerment ServicesDocument9 pagesSimbhaoli Sugars LTD.: Stakeholders Empowerment ServicesvishalNo ratings yet

- Aarti Industries LTDDocument5 pagesAarti Industries LTDViju K GNo ratings yet

- Result Presentation For December 31, 2016 (Result)Document30 pagesResult Presentation For December 31, 2016 (Result)Shyam SunderNo ratings yet

- Avenue Supermarts Sell: Result UpdateDocument6 pagesAvenue Supermarts Sell: Result UpdateAshokNo ratings yet

- Care Ratings - Q4FY19 - Call Closure - 13062019 - 14-06-2019 - 09Document4 pagesCare Ratings - Q4FY19 - Call Closure - 13062019 - 14-06-2019 - 09Jai SinghNo ratings yet

- L&T Equity ResearchDocument4 pagesL&T Equity ResearchMegha ThakurNo ratings yet

- Investor Presentation (Company Update)Document24 pagesInvestor Presentation (Company Update)Shyam SunderNo ratings yet

- VRL L L (VRL) : Ogistics TDDocument6 pagesVRL L L (VRL) : Ogistics TDjagadish madiwalarNo ratings yet

- Indsec ABFRL Q1 FY'21Document9 pagesIndsec ABFRL Q1 FY'21PriyankaNo ratings yet

- Security Analysis and Investment Management: Army Institute of Management & TechnologyDocument10 pagesSecurity Analysis and Investment Management: Army Institute of Management & TechnologyArjun BhosaleNo ratings yet

- Glaxosmithkline Pharmaceuticals LTD: Revenue De-GrowthDocument7 pagesGlaxosmithkline Pharmaceuticals LTD: Revenue De-GrowthGuarachandar ChandNo ratings yet

- Reliance by Motilal OswalDocument34 pagesReliance by Motilal OswalQUALITY12No ratings yet

- Varun BeveragesDocument7 pagesVarun Beverages869jshh52hNo ratings yet

- Aarti Industries - 3QFY20 Result - RsecDocument7 pagesAarti Industries - 3QFY20 Result - RsecdarshanmaldeNo ratings yet

- Shilpi Cable Technologies LTD - Firstcall - 070715Document10 pagesShilpi Cable Technologies LTD - Firstcall - 070715Lokesh BhatiNo ratings yet

- SML Isuzu ReportDocument7 pagesSML Isuzu ReportShivani KelvalkarNo ratings yet

- Research Report ITC LTD PDFDocument8 pagesResearch Report ITC LTD PDFPriyanashi JainNo ratings yet

- Shriram Transport Q1 FY20 PresentationDocument18 pagesShriram Transport Q1 FY20 PresentationVenkata Reddy KNo ratings yet

- Analyst Briefing 2019 CBSDocument11 pagesAnalyst Briefing 2019 CBSshussayn82No ratings yet

- Estados Financieros 2018 2019 SubaruDocument26 pagesEstados Financieros 2018 2019 SubaruManuel Eduardo Herrera AguilaNo ratings yet

- Aarti Industries - 1QFY19 RU - KR ChokseyDocument7 pagesAarti Industries - 1QFY19 RU - KR ChokseydarshanmaldeNo ratings yet

- Hero Motocorp: CMP: Inr3,707 TP: Inr3,818 (+3%)Document12 pagesHero Motocorp: CMP: Inr3,707 TP: Inr3,818 (+3%)SAHIL SHARMANo ratings yet

- Assignment I - Ashapura Minechem LimitedDocument8 pagesAssignment I - Ashapura Minechem LimitedSibika GadiaNo ratings yet

- Bharat Petroleum Corporation Limited: BPCL Income Statement 2018-19Document3 pagesBharat Petroleum Corporation Limited: BPCL Income Statement 2018-19RuchikaNo ratings yet

- Bhel (Bhel In) : Q4FY19 Result UpdateDocument6 pagesBhel (Bhel In) : Q4FY19 Result Updatesaran21No ratings yet

- Bajaj-Consumer-Care-Limited 827 CompanyUpdate PDFDocument11 pagesBajaj-Consumer-Care-Limited 827 CompanyUpdate PDFhamsNo ratings yet

- Jain Irrigation Systems LTD: AccumulateDocument6 pagesJain Irrigation Systems LTD: Accumulatesaran21No ratings yet

- EarningsReleaseQ1 FY19Document5 pagesEarningsReleaseQ1 FY19osama aboualamNo ratings yet

- FY2019 2nd Quarter Consolidated Financial Results (IFRS) (April 1, 2018 Through September 30, 2018)Document7 pagesFY2019 2nd Quarter Consolidated Financial Results (IFRS) (April 1, 2018 Through September 30, 2018)Papa Ekow ArmahNo ratings yet

- Sanghi Industries - Q1FY20 - Market Impact-201908291229582531348 PDFDocument3 pagesSanghi Industries - Q1FY20 - Market Impact-201908291229582531348 PDFSabyasachi BangalNo ratings yet

- Mitra Adiperkasa: Indonesia Company GuideDocument14 pagesMitra Adiperkasa: Indonesia Company GuideAshokNo ratings yet

- Final Report ACC 406Document14 pagesFinal Report ACC 406Mahmud TuhinNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- Solutions - Chapter 7 Non-Current Operating Assets Solutions - Chapter 7 Non-Current Operating AssetsDocument9 pagesSolutions - Chapter 7 Non-Current Operating Assets Solutions - Chapter 7 Non-Current Operating AssetsJohanna VidadNo ratings yet

- Chapter 25Document4 pagesChapter 25Xynith Nicole RamosNo ratings yet

- REVISION Qs FADocument12 pagesREVISION Qs FAhannah ispandiNo ratings yet

- Mid CORFINDocument16 pagesMid CORFINRichard LazaroNo ratings yet

- Pakistan Synthetics Limited: Condensed Interim Balance Sheet (Unaudited)Document8 pagesPakistan Synthetics Limited: Condensed Interim Balance Sheet (Unaudited)mohammadtalhaNo ratings yet

- Odoo Erp SolutionDocument53 pagesOdoo Erp SolutionDiana Rosa GonzálezNo ratings yet

- Oracle Item AttributesDocument10 pagesOracle Item AttributesSwarna Lata DebbarmaNo ratings yet

- Dutch Lady: Financial Statement AnalysisDocument17 pagesDutch Lady: Financial Statement AnalysisNurqasrina AisyahNo ratings yet

- The Expenditure Cycle Part II: Payroll Processing and Fixed Asset ProcedureDocument42 pagesThe Expenditure Cycle Part II: Payroll Processing and Fixed Asset ProcedureNicah AcojonNo ratings yet

- MGT 201 Chapter 9Document41 pagesMGT 201 Chapter 9lupi99No ratings yet

- Discussion 1 Second Sem PDFDocument11 pagesDiscussion 1 Second Sem PDFRNo ratings yet

- BKT PDFDocument28 pagesBKT PDFnikhilNo ratings yet

- Long AlignTechnologyDocument14 pagesLong AlignTechnologyMichael RousselNo ratings yet

- Financial Accounting: Long-Term Investments and The Time Value of MoneyDocument68 pagesFinancial Accounting: Long-Term Investments and The Time Value of Moneygizem akçaNo ratings yet

- Summer Project Report - Format - MmsDocument47 pagesSummer Project Report - Format - MmsVaishnavi khotNo ratings yet

- Sir. Shabir Ahmad Tariq Aziz: Supervised byDocument52 pagesSir. Shabir Ahmad Tariq Aziz: Supervised byMohib Ullah YousafzaiNo ratings yet

- Britannia Industries: PrintDocument1 pageBritannia Industries: PrintTejaswiniNo ratings yet

- Bus Com 12Document3 pagesBus Com 12Chabelita MijaresNo ratings yet

- Benjamin Graham S Net Current Asset Value Approach PDFDocument6 pagesBenjamin Graham S Net Current Asset Value Approach PDFBimal MaheshNo ratings yet

- Hoyle Advanced Accounting Powerpoint Slides Chapter 3Document37 pagesHoyle Advanced Accounting Powerpoint Slides Chapter 3Sean75% (4)

- CH 10Document74 pagesCH 10Satria WijayaNo ratings yet

- IRRI AR 2013 Audited Financial StatementsDocument62 pagesIRRI AR 2013 Audited Financial StatementsIRRI_resourcesNo ratings yet

- Asset Information Management - Part 1 - The Case For Developing An AIM StrategyDocument28 pagesAsset Information Management - Part 1 - The Case For Developing An AIM StrategyhanhdoducNo ratings yet

- Aarti Industries LTDDocument8 pagesAarti Industries LTDAkash MathewsNo ratings yet

- Intermediate Accounting 1 FinalDocument5 pagesIntermediate Accounting 1 FinalCix SorcheNo ratings yet

- Companies (Auditors' Report) Order, 2015 (CARO) : Requirements of Sec 143 Requirements of CARODocument28 pagesCompanies (Auditors' Report) Order, 2015 (CARO) : Requirements of Sec 143 Requirements of CAROCA Rishabh DaiyaNo ratings yet

- Cloudpoint Technology Berhad IPO Prospectus 9 May 2023 Part 2Document154 pagesCloudpoint Technology Berhad IPO Prospectus 9 May 2023 Part 2Oliver Oscar100% (1)

- Partnership MyDocument13 pagesPartnership MyHoneylyne PlazaNo ratings yet

- ACCO-20093 - INTERMEDIATE-ACCOUNTING-2 - Module - Non - Current Assets Held For SaleDocument4 pagesACCO-20093 - INTERMEDIATE-ACCOUNTING-2 - Module - Non - Current Assets Held For SalePamela Ledesma SusonNo ratings yet