Methodology For Market Analysis

Methodology For Market Analysis

You might also like

- The Survival Guide to EU Medical Device RegulationsFrom EverandThe Survival Guide to EU Medical Device RegulationsRating: 5 out of 5 stars5/5 (1)

- Network neutrality: From policy to law to regulationFrom EverandNetwork neutrality: From policy to law to regulationNo ratings yet

- Com2011 0772en01Document97 pagesCom2011 0772en01ipliprensNo ratings yet

- EN EN: European CommissionDocument44 pagesEN EN: European CommissionSlaven DžindoNo ratings yet

- EN EN: European CommissionDocument25 pagesEN EN: European CommissionSoniaNo ratings yet

- NIST Special Publication 951 A Guide To EU Standards and Conformity AssessmentDocument36 pagesNIST Special Publication 951 A Guide To EU Standards and Conformity Assessmentrehan107No ratings yet

- TP 2007 DirectiveDocument13 pagesTP 2007 DirectiveBruegelNo ratings yet

- Celex PDFDocument26 pagesCelex PDFsamuelNo ratings yet

- Gd1 - General Guidance To The Allocation MethodologyDocument37 pagesGd1 - General Guidance To The Allocation MethodologyAbhay PrakashNo ratings yet

- 1 EN ACT Part1 v8Document144 pages1 EN ACT Part1 v8ana silvaNo ratings yet

- Ergeg 2005-07-2005 Gas Balancing Public ConsultationDocument47 pagesErgeg 2005-07-2005 Gas Balancing Public Consultationmselim197499No ratings yet

- EHDOTUS CPD REVISIO CPRproposal Com2008 311Document61 pagesEHDOTUS CPD REVISIO CPRproposal Com2008 311harri.sauvalaNo ratings yet

- Blue Book For CE MarkDocument114 pagesBlue Book For CE Marksks27974No ratings yet

- Principles of MetrologyDocument7 pagesPrinciples of MetrologysptbalaNo ratings yet

- Competition Enforcement EU LawsDocument38 pagesCompetition Enforcement EU Lawspayalhansaria2001No ratings yet

- Cs66 MartinoDocument20 pagesCs66 MartinoMohamed SaadNo ratings yet

- Commission of The European Communities: Brussels, 9.8.2002 COM (2002) 460 Final 2001/0117 (COD)Document64 pagesCommission of The European Communities: Brussels, 9.8.2002 COM (2002) 460 Final 2001/0117 (COD)Bosko SofijanovNo ratings yet

- Regulation (EU) No 1025 - 2012Document22 pagesRegulation (EU) No 1025 - 2012RNo ratings yet

- EU Code of Conduct - JTPFDocument7 pagesEU Code of Conduct - JTPFGeorg ProkschNo ratings yet

- The Leniency ProgramDocument11 pagesThe Leniency ProgramFelixDelux2023roNo ratings yet

- DG Markt G2 MET/OT/acg D (2010) 768690: Egislation On Legal Certainty of Securities Holding and DispositionsDocument37 pagesDG Markt G2 MET/OT/acg D (2010) 768690: Egislation On Legal Certainty of Securities Holding and DispositionspisterboneNo ratings yet

- EU Conveyancing MarketDocument37 pagesEU Conveyancing Market張漢斌No ratings yet

- Propuesta de Ley de La Comisión Europea para La Regulación Del EURIBOR y Del LIBOR Proposed European Commission Act To Regulate The EURIBOR and LIBORDocument81 pagesPropuesta de Ley de La Comisión Europea para La Regulación Del EURIBOR y Del LIBOR Proposed European Commission Act To Regulate The EURIBOR and LIBORGregorio AbascalNo ratings yet

- An Assessment of Telecommunications Regulation Performance in The European UnionDocument39 pagesAn Assessment of Telecommunications Regulation Performance in The European UnionCarlos de LegarretaNo ratings yet

- Full Report Part1Document110 pagesFull Report Part1Luiza DraghiciNo ratings yet

- European Banking Authority Opinion On Debt Based Crowdfunding March 2015Document40 pagesEuropean Banking Authority Opinion On Debt Based Crowdfunding March 2015CrowdfundInsiderNo ratings yet

- European Cooperation in Legal Metrology Welmec: Corinne LAGAUTERIE WELMEC Vice ChairpersonDocument18 pagesEuropean Cooperation in Legal Metrology Welmec: Corinne LAGAUTERIE WELMEC Vice ChairpersonazitaggNo ratings yet

- 0000welmec Oiml 2007Document18 pages0000welmec Oiml 2007azitaggNo ratings yet

- COM_2013_0075_FIN_EN_TXTDocument64 pagesCOM_2013_0075_FIN_EN_TXTsasaregent2No ratings yet

- ECRB Dispute ResolutionDocument52 pagesECRB Dispute ResolutionDivyanshu BaraiyaNo ratings yet

- Celex 52012PC0073 enDocument101 pagesCelex 52012PC0073 envaish2u6263No ratings yet

- Public Procurment GuidanceDocument37 pagesPublic Procurment GuidanceRoxi RoxanaNo ratings yet

- Business Law CaseDocument6 pagesBusiness Law CaseMdeme CleptoNo ratings yet

- EU Benchmark Regulations CELEX - 32016R1011 - EN - TXTDocument65 pagesEU Benchmark Regulations CELEX - 32016R1011 - EN - TXTdpageNo ratings yet

- Regulation 765 2008Document18 pagesRegulation 765 2008hoyipleong1326No ratings yet

- 13ercl239 PDFDocument17 pages13ercl239 PDFTran Ngoc Bao TramNo ratings yet

- EU New MDR White Paper EMERGODocument28 pagesEU New MDR White Paper EMERGOFrancisco100% (2)

- Position Paper: 19 August 2020Document7 pagesPosition Paper: 19 August 2020Εύη ΣαλταNo ratings yet

- Achilles Brief Guide To Utilities Eu Procurement LegislationDocument16 pagesAchilles Brief Guide To Utilities Eu Procurement LegislationDavid WoodhouseNo ratings yet

- European Union Regulation of in Vitro Diagnostic Medical DevicesDocument26 pagesEuropean Union Regulation of in Vitro Diagnostic Medical DevicesLuis Arístides Torres SánchezNo ratings yet

- Provisional EU Directive On Auditing November 2011Document28 pagesProvisional EU Directive On Auditing November 2011Irl_tax_expertNo ratings yet

- Council of The European Union Brussels, 9 July 2013 (OR. En) 12101/13Document168 pagesCouncil of The European Union Brussels, 9 July 2013 (OR. En) 12101/13ProkopNo ratings yet

- EA-2 17 2009 - EA Guidance On The Horizontal Requirements For The Accreditation of Conformity Assessment Bodies For Notification PurposesDocument40 pagesEA-2 17 2009 - EA Guidance On The Horizontal Requirements For The Accreditation of Conformity Assessment Bodies For Notification PurposesMin Gul100% (1)

- Impact Effectiveness EU Public Procurement 201106Document207 pagesImpact Effectiveness EU Public Procurement 201106Emmanuel MorelNo ratings yet

- Mitchell Working Paper Series: Europa InstituteDocument19 pagesMitchell Working Paper Series: Europa InstituteRevekka TheodorouNo ratings yet

- 021-11pas EngDocument8 pages021-11pas Engjennypenny035No ratings yet

- The European Commission's Proposed Construction Products RegulationDocument30 pagesThe European Commission's Proposed Construction Products Regulationdcd1980No ratings yet

- ECRB 042019 Recommendation NEMODocument21 pagesECRB 042019 Recommendation NEMOpetar.krstevski1No ratings yet

- IRG-Rail 2021 9 - Paper On Market Segmentation Mark-UpsDocument32 pagesIRG-Rail 2021 9 - Paper On Market Segmentation Mark-UpsAFUECABNo ratings yet

- Ucpd Report enDocument31 pagesUcpd Report ennikubejNo ratings yet

- 2019 EP SEPS and The Internet of Things (Report For JURI Committee)Document36 pages2019 EP SEPS and The Internet of Things (Report For JURI Committee)mugui84No ratings yet

- Eu Customs Code EPRS STU (2018) 621854 enDocument64 pagesEu Customs Code EPRS STU (2018) 621854 enaibotNo ratings yet

- Policy Memo 21 v2 APDocument25 pagesPolicy Memo 21 v2 APStoian DragosNo ratings yet

- JRC Assessment Framework Final v2Document26 pagesJRC Assessment Framework Final v2Jerome PercepiedNo ratings yet

- Executive Summary Impact Assessment EMFA eCPL8l5LECc21EAEChijuNp0 89594Document4 pagesExecutive Summary Impact Assessment EMFA eCPL8l5LECc21EAEChijuNp0 89594Fernando Rivera LazoNo ratings yet

- Consultation PaperDocument57 pagesConsultation PaperMarketsWikiNo ratings yet

- PHD Thesis Liyang HouDocument365 pagesPHD Thesis Liyang HoumarianopinnaNo ratings yet

- Electrical Equipment Designed For Use Within Certain Voltage LimitsDocument5 pagesElectrical Equipment Designed For Use Within Certain Voltage Limitsmon tailNo ratings yet

- Acts Adopted Under The EC Treaty/Euratom Treaty Whose Publication Is ObligatoryDocument14 pagesActs Adopted Under The EC Treaty/Euratom Treaty Whose Publication Is ObligatorybrillachielNo ratings yet

- ENTSO-E Grid Planning Modelling Showcase for China: Joint Statement Report Series, #4From EverandENTSO-E Grid Planning Modelling Showcase for China: Joint Statement Report Series, #4No ratings yet

- Foreign PolicyDocument10 pagesForeign PolicyMuhammad HaseebNo ratings yet

- Company Stats EuropeDocument375 pagesCompany Stats Europesourabh6chakrabort-1No ratings yet

- Lumang Pera NG PilipinasDocument2 pagesLumang Pera NG PilipinasYeng100% (1)

- Mock Exam 1 - Chapters 1 - 4Document8 pagesMock Exam 1 - Chapters 1 - 4Thomas Matheny100% (1)

- Proforma Invoice For ScalesDocument1 pageProforma Invoice For ScalespaulwengardNo ratings yet

- Analisis Titik Pulang ModalDocument3 pagesAnalisis Titik Pulang ModalAzimun HalimNo ratings yet

- Model Question 2Document88 pagesModel Question 2Hamal PrachandaNo ratings yet

- Government BudgetDocument13 pagesGovernment BudgetsarikaNo ratings yet

- Premier Cement PDFDocument183 pagesPremier Cement PDFSor O RityNo ratings yet

- 02 Cash Cash EquivalentDocument5 pages02 Cash Cash EquivalentalteregoNo ratings yet

- StadiumStudyUrbanDesignAnalysisPresentation PDFDocument65 pagesStadiumStudyUrbanDesignAnalysisPresentation PDFsanamNo ratings yet

- BBS-Safety MomentDocument24 pagesBBS-Safety MomentbabjihanumanthuNo ratings yet

- facturaEDK1511 Andy OttenoDocument1 pagefacturaEDK1511 Andy OttenoJoseph OttenoNo ratings yet

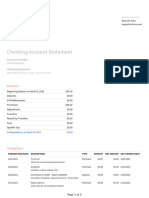

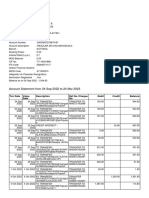

- Checking Account StatementDocument3 pagesChecking Account Statementandyspeers0No ratings yet

- Murphy and Nagel The Myth of Ownership PDFDocument239 pagesMurphy and Nagel The Myth of Ownership PDFDaisy Anita SusiloNo ratings yet

- Coal Sector in IndiaDocument8 pagesCoal Sector in IndiaJEFY JEAN ANo ratings yet

- A Study On Guest Touch Point at The Front Office - Vivanta by Taj Holiday Village GoaDocument27 pagesA Study On Guest Touch Point at The Front Office - Vivanta by Taj Holiday Village GoaJoel Dias0% (1)

- Draft Case AnalysisDocument2 pagesDraft Case AnalysisaaaaaNo ratings yet

- Muchhala Poly Staff PresentationDocument3 pagesMuchhala Poly Staff PresentationSuryakant NawleNo ratings yet

- Cash Inadequacy and Cash Insolvency-4Document21 pagesCash Inadequacy and Cash Insolvency-4Girish KumarNo ratings yet

- BladeRunner Trading MethodDocument5 pagesBladeRunner Trading MethodSelfia ThabibahNo ratings yet

- Six Sigma Lean Leads.Document2 pagesSix Sigma Lean Leads.TMDWARNo ratings yet

- Exploring The Continuum of Social and Financial Returns: Kathy BrozekDocument11 pagesExploring The Continuum of Social and Financial Returns: Kathy BrozekScott OrnNo ratings yet

- 10 Ways To Improve Trading Strategy enDocument56 pages10 Ways To Improve Trading Strategy enMaqbool KhalidNo ratings yet

- B.A (H) Eco - Sem 2 - Introductory MacroeconomicsDocument4 pagesB.A (H) Eco - Sem 2 - Introductory Macroeconomicsanshuyadav620344No ratings yet

- Case Analysis: 1. Hewlett-Packard-Compaq: The Merger Decision 2. Hewlett-Packard: Culture in Changing TimesDocument8 pagesCase Analysis: 1. Hewlett-Packard-Compaq: The Merger Decision 2. Hewlett-Packard: Culture in Changing TimesAmbujTripathiNo ratings yet

- Cooperative Development Authority of The PhilippinesDocument32 pagesCooperative Development Authority of The PhilippinesJyedmark Reconalla MoreteNo ratings yet

- SESm 1 B 0 y LMNHTM1 ZDocument15 pagesSESm 1 B 0 y LMNHTM1 ZJithuHashMiNo ratings yet

- Partnership ActDocument12 pagesPartnership ActAusaf Ali JokhioNo ratings yet

- Five Forces AnalysisDocument5 pagesFive Forces Analysiswonderland123No ratings yet

Download as pdf or txt

You might also like

- The Survival Guide to EU Medical Device RegulationsFrom EverandThe Survival Guide to EU Medical Device RegulationsRating: 5 out of 5 stars5/5 (1)

- Network neutrality: From policy to law to regulationFrom EverandNetwork neutrality: From policy to law to regulationNo ratings yet

- Com2011 0772en01Document97 pagesCom2011 0772en01ipliprensNo ratings yet

- EN EN: European CommissionDocument44 pagesEN EN: European CommissionSlaven DžindoNo ratings yet

- EN EN: European CommissionDocument25 pagesEN EN: European CommissionSoniaNo ratings yet

- NIST Special Publication 951 A Guide To EU Standards and Conformity AssessmentDocument36 pagesNIST Special Publication 951 A Guide To EU Standards and Conformity Assessmentrehan107No ratings yet

- TP 2007 DirectiveDocument13 pagesTP 2007 DirectiveBruegelNo ratings yet

- Celex PDFDocument26 pagesCelex PDFsamuelNo ratings yet

- Gd1 - General Guidance To The Allocation MethodologyDocument37 pagesGd1 - General Guidance To The Allocation MethodologyAbhay PrakashNo ratings yet

- 1 EN ACT Part1 v8Document144 pages1 EN ACT Part1 v8ana silvaNo ratings yet

- Ergeg 2005-07-2005 Gas Balancing Public ConsultationDocument47 pagesErgeg 2005-07-2005 Gas Balancing Public Consultationmselim197499No ratings yet

- EHDOTUS CPD REVISIO CPRproposal Com2008 311Document61 pagesEHDOTUS CPD REVISIO CPRproposal Com2008 311harri.sauvalaNo ratings yet

- Blue Book For CE MarkDocument114 pagesBlue Book For CE Marksks27974No ratings yet

- Principles of MetrologyDocument7 pagesPrinciples of MetrologysptbalaNo ratings yet

- Competition Enforcement EU LawsDocument38 pagesCompetition Enforcement EU Lawspayalhansaria2001No ratings yet

- Cs66 MartinoDocument20 pagesCs66 MartinoMohamed SaadNo ratings yet

- Commission of The European Communities: Brussels, 9.8.2002 COM (2002) 460 Final 2001/0117 (COD)Document64 pagesCommission of The European Communities: Brussels, 9.8.2002 COM (2002) 460 Final 2001/0117 (COD)Bosko SofijanovNo ratings yet

- Regulation (EU) No 1025 - 2012Document22 pagesRegulation (EU) No 1025 - 2012RNo ratings yet

- EU Code of Conduct - JTPFDocument7 pagesEU Code of Conduct - JTPFGeorg ProkschNo ratings yet

- The Leniency ProgramDocument11 pagesThe Leniency ProgramFelixDelux2023roNo ratings yet

- DG Markt G2 MET/OT/acg D (2010) 768690: Egislation On Legal Certainty of Securities Holding and DispositionsDocument37 pagesDG Markt G2 MET/OT/acg D (2010) 768690: Egislation On Legal Certainty of Securities Holding and DispositionspisterboneNo ratings yet

- EU Conveyancing MarketDocument37 pagesEU Conveyancing Market張漢斌No ratings yet

- Propuesta de Ley de La Comisión Europea para La Regulación Del EURIBOR y Del LIBOR Proposed European Commission Act To Regulate The EURIBOR and LIBORDocument81 pagesPropuesta de Ley de La Comisión Europea para La Regulación Del EURIBOR y Del LIBOR Proposed European Commission Act To Regulate The EURIBOR and LIBORGregorio AbascalNo ratings yet

- An Assessment of Telecommunications Regulation Performance in The European UnionDocument39 pagesAn Assessment of Telecommunications Regulation Performance in The European UnionCarlos de LegarretaNo ratings yet

- Full Report Part1Document110 pagesFull Report Part1Luiza DraghiciNo ratings yet

- European Banking Authority Opinion On Debt Based Crowdfunding March 2015Document40 pagesEuropean Banking Authority Opinion On Debt Based Crowdfunding March 2015CrowdfundInsiderNo ratings yet

- European Cooperation in Legal Metrology Welmec: Corinne LAGAUTERIE WELMEC Vice ChairpersonDocument18 pagesEuropean Cooperation in Legal Metrology Welmec: Corinne LAGAUTERIE WELMEC Vice ChairpersonazitaggNo ratings yet

- 0000welmec Oiml 2007Document18 pages0000welmec Oiml 2007azitaggNo ratings yet

- COM_2013_0075_FIN_EN_TXTDocument64 pagesCOM_2013_0075_FIN_EN_TXTsasaregent2No ratings yet

- ECRB Dispute ResolutionDocument52 pagesECRB Dispute ResolutionDivyanshu BaraiyaNo ratings yet

- Celex 52012PC0073 enDocument101 pagesCelex 52012PC0073 envaish2u6263No ratings yet

- Public Procurment GuidanceDocument37 pagesPublic Procurment GuidanceRoxi RoxanaNo ratings yet

- Business Law CaseDocument6 pagesBusiness Law CaseMdeme CleptoNo ratings yet

- EU Benchmark Regulations CELEX - 32016R1011 - EN - TXTDocument65 pagesEU Benchmark Regulations CELEX - 32016R1011 - EN - TXTdpageNo ratings yet

- Regulation 765 2008Document18 pagesRegulation 765 2008hoyipleong1326No ratings yet

- 13ercl239 PDFDocument17 pages13ercl239 PDFTran Ngoc Bao TramNo ratings yet

- EU New MDR White Paper EMERGODocument28 pagesEU New MDR White Paper EMERGOFrancisco100% (2)

- Position Paper: 19 August 2020Document7 pagesPosition Paper: 19 August 2020Εύη ΣαλταNo ratings yet

- Achilles Brief Guide To Utilities Eu Procurement LegislationDocument16 pagesAchilles Brief Guide To Utilities Eu Procurement LegislationDavid WoodhouseNo ratings yet

- European Union Regulation of in Vitro Diagnostic Medical DevicesDocument26 pagesEuropean Union Regulation of in Vitro Diagnostic Medical DevicesLuis Arístides Torres SánchezNo ratings yet

- Provisional EU Directive On Auditing November 2011Document28 pagesProvisional EU Directive On Auditing November 2011Irl_tax_expertNo ratings yet

- Council of The European Union Brussels, 9 July 2013 (OR. En) 12101/13Document168 pagesCouncil of The European Union Brussels, 9 July 2013 (OR. En) 12101/13ProkopNo ratings yet

- EA-2 17 2009 - EA Guidance On The Horizontal Requirements For The Accreditation of Conformity Assessment Bodies For Notification PurposesDocument40 pagesEA-2 17 2009 - EA Guidance On The Horizontal Requirements For The Accreditation of Conformity Assessment Bodies For Notification PurposesMin Gul100% (1)

- Impact Effectiveness EU Public Procurement 201106Document207 pagesImpact Effectiveness EU Public Procurement 201106Emmanuel MorelNo ratings yet

- Mitchell Working Paper Series: Europa InstituteDocument19 pagesMitchell Working Paper Series: Europa InstituteRevekka TheodorouNo ratings yet

- 021-11pas EngDocument8 pages021-11pas Engjennypenny035No ratings yet

- The European Commission's Proposed Construction Products RegulationDocument30 pagesThe European Commission's Proposed Construction Products Regulationdcd1980No ratings yet

- ECRB 042019 Recommendation NEMODocument21 pagesECRB 042019 Recommendation NEMOpetar.krstevski1No ratings yet

- IRG-Rail 2021 9 - Paper On Market Segmentation Mark-UpsDocument32 pagesIRG-Rail 2021 9 - Paper On Market Segmentation Mark-UpsAFUECABNo ratings yet

- Ucpd Report enDocument31 pagesUcpd Report ennikubejNo ratings yet

- 2019 EP SEPS and The Internet of Things (Report For JURI Committee)Document36 pages2019 EP SEPS and The Internet of Things (Report For JURI Committee)mugui84No ratings yet

- Eu Customs Code EPRS STU (2018) 621854 enDocument64 pagesEu Customs Code EPRS STU (2018) 621854 enaibotNo ratings yet

- Policy Memo 21 v2 APDocument25 pagesPolicy Memo 21 v2 APStoian DragosNo ratings yet

- JRC Assessment Framework Final v2Document26 pagesJRC Assessment Framework Final v2Jerome PercepiedNo ratings yet

- Executive Summary Impact Assessment EMFA eCPL8l5LECc21EAEChijuNp0 89594Document4 pagesExecutive Summary Impact Assessment EMFA eCPL8l5LECc21EAEChijuNp0 89594Fernando Rivera LazoNo ratings yet

- Consultation PaperDocument57 pagesConsultation PaperMarketsWikiNo ratings yet

- PHD Thesis Liyang HouDocument365 pagesPHD Thesis Liyang HoumarianopinnaNo ratings yet

- Electrical Equipment Designed For Use Within Certain Voltage LimitsDocument5 pagesElectrical Equipment Designed For Use Within Certain Voltage Limitsmon tailNo ratings yet

- Acts Adopted Under The EC Treaty/Euratom Treaty Whose Publication Is ObligatoryDocument14 pagesActs Adopted Under The EC Treaty/Euratom Treaty Whose Publication Is ObligatorybrillachielNo ratings yet

- ENTSO-E Grid Planning Modelling Showcase for China: Joint Statement Report Series, #4From EverandENTSO-E Grid Planning Modelling Showcase for China: Joint Statement Report Series, #4No ratings yet

- Foreign PolicyDocument10 pagesForeign PolicyMuhammad HaseebNo ratings yet

- Company Stats EuropeDocument375 pagesCompany Stats Europesourabh6chakrabort-1No ratings yet

- Lumang Pera NG PilipinasDocument2 pagesLumang Pera NG PilipinasYeng100% (1)

- Mock Exam 1 - Chapters 1 - 4Document8 pagesMock Exam 1 - Chapters 1 - 4Thomas Matheny100% (1)

- Proforma Invoice For ScalesDocument1 pageProforma Invoice For ScalespaulwengardNo ratings yet

- Analisis Titik Pulang ModalDocument3 pagesAnalisis Titik Pulang ModalAzimun HalimNo ratings yet

- Model Question 2Document88 pagesModel Question 2Hamal PrachandaNo ratings yet

- Government BudgetDocument13 pagesGovernment BudgetsarikaNo ratings yet

- Premier Cement PDFDocument183 pagesPremier Cement PDFSor O RityNo ratings yet

- 02 Cash Cash EquivalentDocument5 pages02 Cash Cash EquivalentalteregoNo ratings yet

- StadiumStudyUrbanDesignAnalysisPresentation PDFDocument65 pagesStadiumStudyUrbanDesignAnalysisPresentation PDFsanamNo ratings yet

- BBS-Safety MomentDocument24 pagesBBS-Safety MomentbabjihanumanthuNo ratings yet

- facturaEDK1511 Andy OttenoDocument1 pagefacturaEDK1511 Andy OttenoJoseph OttenoNo ratings yet

- Checking Account StatementDocument3 pagesChecking Account Statementandyspeers0No ratings yet

- Murphy and Nagel The Myth of Ownership PDFDocument239 pagesMurphy and Nagel The Myth of Ownership PDFDaisy Anita SusiloNo ratings yet

- Coal Sector in IndiaDocument8 pagesCoal Sector in IndiaJEFY JEAN ANo ratings yet

- A Study On Guest Touch Point at The Front Office - Vivanta by Taj Holiday Village GoaDocument27 pagesA Study On Guest Touch Point at The Front Office - Vivanta by Taj Holiday Village GoaJoel Dias0% (1)

- Draft Case AnalysisDocument2 pagesDraft Case AnalysisaaaaaNo ratings yet

- Muchhala Poly Staff PresentationDocument3 pagesMuchhala Poly Staff PresentationSuryakant NawleNo ratings yet

- Cash Inadequacy and Cash Insolvency-4Document21 pagesCash Inadequacy and Cash Insolvency-4Girish KumarNo ratings yet

- BladeRunner Trading MethodDocument5 pagesBladeRunner Trading MethodSelfia ThabibahNo ratings yet

- Six Sigma Lean Leads.Document2 pagesSix Sigma Lean Leads.TMDWARNo ratings yet

- Exploring The Continuum of Social and Financial Returns: Kathy BrozekDocument11 pagesExploring The Continuum of Social and Financial Returns: Kathy BrozekScott OrnNo ratings yet

- 10 Ways To Improve Trading Strategy enDocument56 pages10 Ways To Improve Trading Strategy enMaqbool KhalidNo ratings yet

- B.A (H) Eco - Sem 2 - Introductory MacroeconomicsDocument4 pagesB.A (H) Eco - Sem 2 - Introductory Macroeconomicsanshuyadav620344No ratings yet

- Case Analysis: 1. Hewlett-Packard-Compaq: The Merger Decision 2. Hewlett-Packard: Culture in Changing TimesDocument8 pagesCase Analysis: 1. Hewlett-Packard-Compaq: The Merger Decision 2. Hewlett-Packard: Culture in Changing TimesAmbujTripathiNo ratings yet

- Cooperative Development Authority of The PhilippinesDocument32 pagesCooperative Development Authority of The PhilippinesJyedmark Reconalla MoreteNo ratings yet

- SESm 1 B 0 y LMNHTM1 ZDocument15 pagesSESm 1 B 0 y LMNHTM1 ZJithuHashMiNo ratings yet

- Partnership ActDocument12 pagesPartnership ActAusaf Ali JokhioNo ratings yet

- Five Forces AnalysisDocument5 pagesFive Forces Analysiswonderland123No ratings yet