Download as pdf or txt

You might also like

- Federal Income Tax 1040 Activity PDFDocument14 pagesFederal Income Tax 1040 Activity PDFRobert Brant100% (1)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- SMChap004 PDFDocument57 pagesSMChap004 PDFhshNo ratings yet

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- WSJ+ Tax-Guide 2020 Updated PDFDocument58 pagesWSJ+ Tax-Guide 2020 Updated PDFLan NguyenNo ratings yet

- US Internal Revenue Service: f8615 - 2003Document1 pageUS Internal Revenue Service: f8615 - 2003IRSNo ratings yet

- US Internal Revenue Service: f8615 - 2002Document1 pageUS Internal Revenue Service: f8615 - 2002IRSNo ratings yet

- US Internal Revenue Service: f8615 - 1997Document2 pagesUS Internal Revenue Service: f8615 - 1997IRSNo ratings yet

- US Internal Revenue Service: f8615 - 1993Document2 pagesUS Internal Revenue Service: f8615 - 1993IRSNo ratings yet

- US Internal Revenue Service: f8615 - 1992Document2 pagesUS Internal Revenue Service: f8615 - 1992IRSNo ratings yet

- US Internal Revenue Service: f8814 - 1997Document2 pagesUS Internal Revenue Service: f8814 - 1997IRSNo ratings yet

- US Internal Revenue Service: f8814 - 2000Document2 pagesUS Internal Revenue Service: f8814 - 2000IRSNo ratings yet

- US Internal Revenue Service: f8814 - 1995Document2 pagesUS Internal Revenue Service: f8814 - 1995IRSNo ratings yet

- US Internal Revenue Service: f8814 - 2001Document2 pagesUS Internal Revenue Service: f8814 - 2001IRSNo ratings yet

- US Internal Revenue Service: f8814 - 1998Document2 pagesUS Internal Revenue Service: f8814 - 1998IRSNo ratings yet

- US Internal Revenue Service: f8814 - 1996Document2 pagesUS Internal Revenue Service: f8814 - 1996IRSNo ratings yet

- US Internal Revenue Service: f8814 - 1993Document2 pagesUS Internal Revenue Service: f8814 - 1993IRSNo ratings yet

- Child Tax Credit WorksheetDocument2 pagesChild Tax Credit Worksheetcam.guerreNo ratings yet

- Additional Child Tax Credit: Schedule 8812Document1 pageAdditional Child Tax Credit: Schedule 8812Jack MiguelNo ratings yet

- US Internal Revenue Service: f8814 - 2004Document3 pagesUS Internal Revenue Service: f8814 - 2004IRSNo ratings yet

- Earned Income Credit-WorksheetDocument1 pageEarned Income Credit-Worksheetcam.guerreNo ratings yet

- US Internal Revenue Service: f8814 - 2005Document3 pagesUS Internal Revenue Service: f8814 - 2005IRSNo ratings yet

- f1099msc 2019Document8 pagesf1099msc 2019pyatetsky100% (1)

- US Internal Revenue Service: F1040ez - 1992Document2 pagesUS Internal Revenue Service: F1040ez - 1992IRSNo ratings yet

- US Internal Revenue Service: f8812 - 2001Document2 pagesUS Internal Revenue Service: f8812 - 2001IRSNo ratings yet

- Child Tax Credit: (For Individuals Sent Here From The Form 1040 or 1040A Instructions)Document12 pagesChild Tax Credit: (For Individuals Sent Here From The Form 1040 or 1040A Instructions)IRSNo ratings yet

- AdamDocument2 pagesAdamtnt4101No ratings yet

- US Internal Revenue Service: fw4s - 2005Document2 pagesUS Internal Revenue Service: fw4s - 2005IRSNo ratings yet

- US Internal Revenue Service: f8812 - 1999Document2 pagesUS Internal Revenue Service: f8812 - 1999IRSNo ratings yet

- US Internal Revenue Service: I8841 - 1993Document2 pagesUS Internal Revenue Service: I8841 - 1993IRSNo ratings yet

- Solution Manual For Concepts in Federal Taxation 2018 25th Edition Murphy, HigginsDocument2 pagesSolution Manual For Concepts in Federal Taxation 2018 25th Edition Murphy, Higginsa882650259No ratings yet

- Documents (942,202212311058, F99NEE)Document2 pagesDocuments (942,202212311058, F99NEE)LertoraNo ratings yet

- Income Tax Return For Single and Joint Filers With No DependentsDocument2 pagesIncome Tax Return For Single and Joint Filers With No DependentsmarahmaneNo ratings yet

- Employer's Annual Federal Unemployment (FUTA) Tax ReturnDocument4 pagesEmployer's Annual Federal Unemployment (FUTA) Tax ReturnFrank LamNo ratings yet

- US Internal Revenue Service: f8815 - 1996Document2 pagesUS Internal Revenue Service: f8815 - 1996IRSNo ratings yet

- Employer's Annual Federal Unemployment (FUTA) Tax ReturnDocument4 pagesEmployer's Annual Federal Unemployment (FUTA) Tax ReturnKaradi KuttiNo ratings yet

- Limitation On Business LossesDocument1 pageLimitation On Business Lossesdouglas jonesNo ratings yet

- US Internal Revenue Service: f2210f - 1995Document2 pagesUS Internal Revenue Service: f2210f - 1995IRSNo ratings yet

- US Internal Revenue Service: f8815 - 1994Document2 pagesUS Internal Revenue Service: f8815 - 1994IRSNo ratings yet

- Form 1040-V: What Is Form 1040-V and Do You Have To Use It? How To Send in Your 2009 Tax Return, Payment, and Form 1040-VDocument2 pagesForm 1040-V: What Is Form 1040-V and Do You Have To Use It? How To Send in Your 2009 Tax Return, Payment, and Form 1040-Vapi-26236657No ratings yet

- US Internal Revenue Service: f8839 - 2004Document2 pagesUS Internal Revenue Service: f8839 - 2004IRSNo ratings yet

- 2011 Irs Tax Form 1040 A Individual Income Tax ReturnDocument3 pages2011 Irs Tax Form 1040 A Individual Income Tax ReturnscribddownloadedNo ratings yet

- F1040ez PDFDocument2 pagesF1040ez PDFjc75aNo ratings yet

- Additional Child Tax Credit: Schedule 8812Document1 pageAdditional Child Tax Credit: Schedule 8812Ishfaq Ali KhanNo ratings yet

- Attention:: WWW - Irs.gov/form1099Document8 pagesAttention:: WWW - Irs.gov/form1099kmufti7No ratings yet

- US Internal Revenue Service: fw4s - 1994Document2 pagesUS Internal Revenue Service: fw4s - 1994IRSNo ratings yet

- F1040ez 2008Document2 pagesF1040ez 2008jonathandeauxNo ratings yet

- US Internal Revenue Service: p967 - 1996Document5 pagesUS Internal Revenue Service: p967 - 1996IRSNo ratings yet

- US Internal Revenue Service: fw4s - 1995Document2 pagesUS Internal Revenue Service: fw4s - 1995IRSNo ratings yet

- US Internal Revenue Service: p967 - 1998Document6 pagesUS Internal Revenue Service: p967 - 1998IRSNo ratings yet

- US Internal Revenue Service: f4137 - 1999Document2 pagesUS Internal Revenue Service: f4137 - 1999IRSNo ratings yet

- 2021 - 1099-NEC - GreenWay Waste & Recycling of Indiana LLC - 11367636 - Sol PinedaDocument3 pages2021 - 1099-NEC - GreenWay Waste & Recycling of Indiana LLC - 11367636 - Sol PinedaRolando Pineda100% (1)

- Income Averaging For Farmers and Fishermen: Schedule J (Form 1040) 20Document1 pageIncome Averaging For Farmers and Fishermen: Schedule J (Form 1040) 20IRSNo ratings yet

- 2014 Alabama Possible 990Document39 pages2014 Alabama Possible 990Alabama PossibleNo ratings yet

- Monica L Lindo Tax FormDocument2 pagesMonica L Lindo Tax Formapi-299234513No ratings yet

- US Internal Revenue Service: F1040as2 - 1994Document2 pagesUS Internal Revenue Service: F1040as2 - 1994IRSNo ratings yet

- US Internal Revenue Service: fw4s07 AccessibleDocument2 pagesUS Internal Revenue Service: fw4s07 AccessibleIRSNo ratings yet

- US Internal Revenue Service: f8863 - 2002Document3 pagesUS Internal Revenue Service: f8863 - 2002IRSNo ratings yet

- 2012 Federal ReturnDocument1 page2012 Federal Return24male86No ratings yet

- US Internal Revenue Service: p967 - 1997Document5 pagesUS Internal Revenue Service: p967 - 1997IRSNo ratings yet

- US Internal Revenue Service: f8812 - 2005Document2 pagesUS Internal Revenue Service: f8812 - 2005IRSNo ratings yet

- 1040 Exam Prep: Module I: The Form 1040 FormulaFrom Everand1040 Exam Prep: Module I: The Form 1040 FormulaRating: 1 out of 5 stars1/5 (3)

- 1040 Exam Prep: Module II - Basic Tax ConceptsFrom Everand1040 Exam Prep: Module II - Basic Tax ConceptsRating: 1.5 out of 5 stars1.5/5 (2)

- Doing Your Own Taxes is as Easy as 1, 2, 3.From EverandDoing Your Own Taxes is as Easy as 1, 2, 3.Rating: 1 out of 5 stars1/5 (1)

- Next Level Tax Course: The only book a newbie needs for a foundation of the tax industryFrom EverandNext Level Tax Course: The only book a newbie needs for a foundation of the tax industryNo ratings yet

- 2008 Credit Card Bulk Provider RequirementsDocument112 pages2008 Credit Card Bulk Provider RequirementsIRSNo ratings yet

- 2008 Data DictionaryDocument260 pages2008 Data DictionaryIRSNo ratings yet

- US Internal Revenue Service: 2290rulesty2007v4 0Document6 pagesUS Internal Revenue Service: 2290rulesty2007v4 0IRSNo ratings yet

- 2008 Objectives Report To Congress v2Document153 pages2008 Objectives Report To Congress v2IRSNo ratings yet

- Request For Photocopy of Missouri Income Tax Return or Property Tax Credit ClaimDocument1 pageRequest For Photocopy of Missouri Income Tax Return or Property Tax Credit ClaimAsjsjsjsNo ratings yet

- 2017W2 PDFDocument2 pages2017W2 PDFSeadevil0No ratings yet

- North Carolina Individual Income Tax Instructions: EfileDocument24 pagesNorth Carolina Individual Income Tax Instructions: EfileQunariNo ratings yet

- I1040tt DFTDocument16 pagesI1040tt DFTVictor Hugo Padilla-VazquezNo ratings yet

- REVENUE MEMORANDUM CIRCULAR NO. 21-2018 Issued On April 5, 2018Document1 pageREVENUE MEMORANDUM CIRCULAR NO. 21-2018 Issued On April 5, 2018Hansel Jake B. PampiloNo ratings yet

- True The Vote v. IRS Consent Order - Jan 21, 2018Document14 pagesTrue The Vote v. IRS Consent Order - Jan 21, 2018Catherine Engelbrecht100% (1)

- Form IL-W-4 Illinois Withholding Allowance Certificate and InstructionsDocument2 pagesForm IL-W-4 Illinois Withholding Allowance Certificate and Instructionspuyang48No ratings yet

- Instructions For Form 8962Document18 pagesInstructions For Form 8962jim1234uNo ratings yet

- Wage and Tax StatementDocument4 pagesWage and Tax StatementMark OasayNo ratings yet

- F 1040 SeDocument2 pagesF 1040 SeseihnNo ratings yet

- An Important Update: Benefit Information IRS Form: What You Need To DoDocument8 pagesAn Important Update: Benefit Information IRS Form: What You Need To DoYordis RamirezNo ratings yet

- Home TestDocument22 pagesHome TestSelina ChenNo ratings yet

- Bigstock 2018 Tax Form PDFDocument1 pageBigstock 2018 Tax Form PDFBalint RoxanaNo ratings yet

- f1040 2018 PDFDocument3 pagesf1040 2018 PDFSara HeadrickNo ratings yet

- Food Stamp Budget WorksheetDocument2 pagesFood Stamp Budget WorksheetZachary CollinsNo ratings yet

- 2014-2015 Verification Worksheet-Dependent Student IDOCDocument4 pages2014-2015 Verification Worksheet-Dependent Student IDOCJoshChukwubudikeBarnesNo ratings yet

- ACC 317 Homework CH 23Document2 pagesACC 317 Homework CH 23leelee0302No ratings yet

- Electronic Filing Instructions For Your 2019 Federal Tax ReturnDocument6 pagesElectronic Filing Instructions For Your 2019 Federal Tax ReturnSindy Cruz100% (1)

- Arizona Form 2018 Arizona Corporation Income Tax Return 120: General InstructionsDocument19 pagesArizona Form 2018 Arizona Corporation Income Tax Return 120: General InstructionsUlii PntNo ratings yet

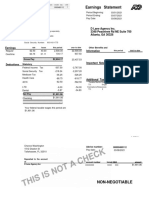

- Earnings Statement: D Lane Agency Inc. 3348 Peachtree RD NE Suite 700 Atlanta, GA 30326Document1 pageEarnings Statement: D Lane Agency Inc. 3348 Peachtree RD NE Suite 700 Atlanta, GA 30326Muhammad AdeelNo ratings yet

- 2020 W-4 FormDocument4 pages2020 W-4 FormFOX Business100% (8)

- 1040 NR EzDocument2 pages1040 NR EzElena Alexandra CărăvanNo ratings yet

- US Treasury Address Puerto RicoDocument1 pageUS Treasury Address Puerto RicoFreeman Lawyer86% (7)

- 1.4 IRS Form 1040VDocument1 page1.4 IRS Form 1040VBenne James100% (1)

- W-2 Wage and Tax Statement: I I I IDocument1 pageW-2 Wage and Tax Statement: I I I Imichelle analieNo ratings yet

- 2019 TSP Catch-Up Contributions and Effective Date ChartDocument1 page2019 TSP Catch-Up Contributions and Effective Date ChartRayNo ratings yet

- Eddie Salazar PDFDocument11 pagesEddie Salazar PDFsloweddie salazar0% (1)