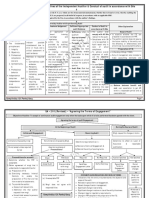

Amendments For May 2021: Chapter 1: Quality Control and Engagement Standards

Amendments For May 2021: Chapter 1: Quality Control and Engagement Standards

You might also like

- CA Final Audit RISK ASSESSMENT AND INTERNAL CONTROL NotesDocument21 pagesCA Final Audit RISK ASSESSMENT AND INTERNAL CONTROL NotesSARASWATHI S100% (1)

- Jamaica Producers Group FITDocument47 pagesJamaica Producers Group FITGerron Thomas100% (1)

- WW SS-4Document3 pagesWW SS-4cstocksg1100% (7)

- Solution To QB QuestionsDocument3 pagesSolution To QB QuestionsSurabhi Suman100% (1)

- Risk Assessment and Internal Control - E-NotesDocument55 pagesRisk Assessment and Internal Control - E-NotesManavNo ratings yet

- ACCA F8知识要点汇总 (上)Document37 pagesACCA F8知识要点汇总 (上)Freya SunNo ratings yet

- Reviewer AuditDocument9 pagesReviewer AuditElisha BascoNo ratings yet

- Identifying and Assessing Risks of Material MisstatementsDocument2 pagesIdentifying and Assessing Risks of Material MisstatementsCattleyaNo ratings yet

- Chapter 3 - : - Risk Assessment and Internal ControlDocument26 pagesChapter 3 - : - Risk Assessment and Internal ControlTamanna AroraNo ratings yet

- 74937bos60526-Cp4 UnlockedDocument72 pages74937bos60526-Cp4 Unlockedhrudaya boysNo ratings yet

- Caua 3752 - Auditing 1B: Topic and Reference: Auditing NotesDocument42 pagesCaua 3752 - Auditing 1B: Topic and Reference: Auditing NotesMoniqueNo ratings yet

- Control RiskDocument19 pagesControl RiskAnonymous HBzUFPliGsNo ratings yet

- Auditing Theory Salosagcol SummaryDocument32 pagesAuditing Theory Salosagcol Summarylily andrew0% (1)

- Risk and MaterialityDocument4 pagesRisk and MaterialitymsyllNo ratings yet

- Ca Inter Audit Paper July - 2021 Paper Review by CA Kapil GoyalDocument13 pagesCa Inter Audit Paper July - 2021 Paper Review by CA Kapil GoyalEdwin MartinNo ratings yet

- Psa 200: Overall Objectives of The Independent Auditor and The Conduct of AuditDocument3 pagesPsa 200: Overall Objectives of The Independent Auditor and The Conduct of AuditDaren Dame Jodi RentasidaNo ratings yet

- ISA 315 SummaryDocument7 pagesISA 315 SummaryTeam R12-01 Cotabato ProvinceNo ratings yet

- CH 4 - Risk AssessmentDocument35 pagesCH 4 - Risk AssessmentSUMIT SINGHNo ratings yet

- Lecture 6-Audit RiksDocument6 pagesLecture 6-Audit Riksakii ramNo ratings yet

- Risk-Based Approach To Conducting A Quality AuditDocument55 pagesRisk-Based Approach To Conducting A Quality AuditKyla Marie MojicoNo ratings yet

- Risk Assesment & Internal ControlDocument56 pagesRisk Assesment & Internal Controlkaran kapadiaNo ratings yet

- Chapter 19 ReportDocument16 pagesChapter 19 ReportAmira SawadjaanNo ratings yet

- Aud339 Audit Planning Part 2Document26 pagesAud339 Audit Planning Part 2Nur IzzahNo ratings yet

- CA Final Audit AmendmentsDocument39 pagesCA Final Audit AmendmentsAkshit WaliaNo ratings yet

- Referencer For Quick Revision: Intermediate Course Paper-6: Auditing and AssuranceDocument32 pagesReferencer For Quick Revision: Intermediate Course Paper-6: Auditing and AssuranceCutfit HardNo ratings yet

- Referencer For Quick Revision: Intermediate Course Paper-6: Auditing and AssuranceDocument29 pagesReferencer For Quick Revision: Intermediate Course Paper-6: Auditing and AssuranceRamNo ratings yet

- Kitcb D01.nhóm 7Document44 pagesKitcb D01.nhóm 7Mạnh hưng LêNo ratings yet

- AT 4 Audit Risk and MaterialityDocument6 pagesAT 4 Audit Risk and MaterialityLhea ClomaNo ratings yet

- CH 5Document2 pagesCH 5Scholastica DaniaNo ratings yet

- TOPIC 3e - Risk and MaterialityDocument33 pagesTOPIC 3e - Risk and MaterialityLANGITBIRUNo ratings yet

- Chapter 6 Risk Assessment (PART 1)Document9 pagesChapter 6 Risk Assessment (PART 1)Aravinthan INSAF SmartClassNo ratings yet

- Chapter 3: Process of Assurance: Planning The AssignmentDocument12 pagesChapter 3: Process of Assurance: Planning The AssignmentShahid MahmudNo ratings yet

- PBEPIII Inherent Risk PDFDocument5 pagesPBEPIII Inherent Risk PDFkim romanoNo ratings yet

- Adobe Scan Oct 24, 2022Document14 pagesAdobe Scan Oct 24, 2022Emmanuel PenullarNo ratings yet

- Content - 2023 Global PWC Audit Guide - Isas - Isa 315 Revised 2019 Identifying and Assessing The Risks of Material MisstatementDocument95 pagesContent - 2023 Global PWC Audit Guide - Isas - Isa 315 Revised 2019 Identifying and Assessing The Risks of Material MisstatementCường Trần MinhNo ratings yet

- Multiple Choice Questions PDFDocument6 pagesMultiple Choice Questions PDFabdul majid khawajaNo ratings yet

- Financial Statements, Deals With An External Auditor's Responsibilities However, Both Internal andDocument11 pagesFinancial Statements, Deals With An External Auditor's Responsibilities However, Both Internal andDanisa NdhlovuNo ratings yet

- ISA 315 Revised 2019 Updated 2022Document228 pagesISA 315 Revised 2019 Updated 2022Lâm Nguyễn TiếnNo ratings yet

- Interactive Training On Overall Audit Process and DocumentationDocument19 pagesInteractive Training On Overall Audit Process and DocumentationAmenu AdagneNo ratings yet

- Risk Based Audit of FSDocument1 pageRisk Based Audit of FSNavsNo ratings yet

- 4 Audit RiskDocument10 pages4 Audit RiskHussain MustunNo ratings yet

- Audit Quick Review PDFDocument41 pagesAudit Quick Review PDFChunnu ChamkilaNo ratings yet

- Audit Risk and Materiality Week Ending 19 April 2024Document96 pagesAudit Risk and Materiality Week Ending 19 April 2024masilelaemmaculateNo ratings yet

- This Study Resource WasDocument3 pagesThis Study Resource WasYuliana rahayuNo ratings yet

- Overview of AuditingDocument5 pagesOverview of AuditingMylene Sunga AbergasNo ratings yet

- Unit 3 - Internal Control - NotesDocument14 pagesUnit 3 - Internal Control - NotesNabhan JafferNo ratings yet

- Types of Audits: Audit - An OverviewDocument31 pagesTypes of Audits: Audit - An OverviewRanel Clark D. TabiosNo ratings yet

- Chapter 4 Risk Assessment and Internal Control - ScannerDocument64 pagesChapter 4 Risk Assessment and Internal Control - ScannerRanjisi chimbanguNo ratings yet

- AUD Flashcards Flashcards - QuizletDocument16 pagesAUD Flashcards Flashcards - QuizletDieter LudwigNo ratings yet

- Internal Control DocumentationDocument42 pagesInternal Control DocumentationJhoe Marie Balintag100% (1)

- 4 5850471109056532138Document39 pages4 5850471109056532138Yehualashet MulugetaNo ratings yet

- What Is Audit RiskDocument7 pagesWhat Is Audit RiskHoang Ngoc ToNo ratings yet

- Arens AAS17 sm 05筆記版Document20 pagesArens AAS17 sm 05筆記版林芷瑜No ratings yet

- Q1 - Bon GarageDocument5 pagesQ1 - Bon GaragefatihahNo ratings yet

- School of Business, Economics and Management Bps430: Audit Practice and Performance Review Chapter 4: The Theory of AuditingDocument73 pagesSchool of Business, Economics and Management Bps430: Audit Practice and Performance Review Chapter 4: The Theory of AuditingChibwe ChinyamaNo ratings yet

- Audit Standards Summary Compiled With Q & ADocument86 pagesAudit Standards Summary Compiled With Q & Asantosh pandeyNo ratings yet

- SA Flowcharts 2Document33 pagesSA Flowcharts 2partymonger71% (7)

- (MA 4221) - Notes Extern Audit RequirementsDocument3 pages(MA 4221) - Notes Extern Audit RequirementsMichael Tom BucalonNo ratings yet

- Chapter 2 - Lesson Outline - StudentDocument14 pagesChapter 2 - Lesson Outline - StudentKim Heok ChuaNo ratings yet

- AA - Chapter 2Document5 pagesAA - Chapter 2Jacqueline Kanesha JamesNo ratings yet

- Risk Rating The Audit UniverseDocument10 pagesRisk Rating The Audit Universecajitendergupta100% (2)

- Chapter 3 Risk Assement & Internal ControlDocument54 pagesChapter 3 Risk Assement & Internal ControlRohit Kumar SantukaNo ratings yet

- Finance Research Paper Topics ListDocument5 pagesFinance Research Paper Topics Listfzgzygnp100% (1)

- EC3314 Spring PSet 4 SolutionsDocument6 pagesEC3314 Spring PSet 4 Solutionschristina0107No ratings yet

- AmlqDocument3 pagesAmlqtejasrawalNo ratings yet

- Dressen Abridged) (A)Document13 pagesDressen Abridged) (A)mithileshagrawalNo ratings yet

- Topic 3 4 5 6 7 Cash Flow Analysis CFO CFI CFFDocument22 pagesTopic 3 4 5 6 7 Cash Flow Analysis CFO CFI CFFYadu Priya DeviNo ratings yet

- Contract of IndemnificationDocument12 pagesContract of IndemnificationMayank AgrawalNo ratings yet

- CE2402-Estimation and Quantity SurveyingDocument12 pagesCE2402-Estimation and Quantity Surveyingసురేంద్ర కారంపూడిNo ratings yet

- Pledge Case: Pactum CommissoriumDocument2 pagesPledge Case: Pactum CommissoriumSusie VanguardiaNo ratings yet

- Cost of Capital at AmeritradeDocument3 pagesCost of Capital at AmeritradeAnkur JainNo ratings yet

- Tendernotice 1 PDFDocument4 pagesTendernotice 1 PDFChit ChitrarasanNo ratings yet

- Monthly Review August 2023Document17 pagesMonthly Review August 2023Md. Razin Hossain 2021148630No ratings yet

- UFI ProspectusDocument17 pagesUFI ProspectusAlvin Rejano TanNo ratings yet

- User Id 012439461813 - DSL Telephonenumber 01244823150Document6 pagesUser Id 012439461813 - DSL Telephonenumber 01244823150NAVEEN SLNo ratings yet

- Syllabus - Certificate Course in Digital BankingDocument3 pagesSyllabus - Certificate Course in Digital Bankinglekshmi priyaNo ratings yet

- ABA Format File DetailsDocument7 pagesABA Format File DetailsAbbas MohamedNo ratings yet

- 1 RR 7-2009Document5 pages1 RR 7-2009JoyceNo ratings yet

- Etf PDFDocument14 pagesEtf PDFYash MeelNo ratings yet

- 74736bos60488 m2 cp8Document40 pages74736bos60488 m2 cp8Vignesh VigneshNo ratings yet

- Statement 600606 35438479 2 11 2022 1 12 2022Document1 pageStatement 600606 35438479 2 11 2022 1 12 2022Orhan DagdelenNo ratings yet

- Quiz 6Document6 pagesQuiz 6Jyasmine Aura V. AgustinNo ratings yet

- Contact Sushant Kumar Add Sushant Kumar To Your NetworkDocument2 pagesContact Sushant Kumar Add Sushant Kumar To Your NetworkJaspreet Singh SahaniNo ratings yet

- Article On HR Score CardDocument8 pagesArticle On HR Score CardPratibha Sesham100% (1)

- Capital Budgeting NotesDocument5 pagesCapital Budgeting NotesDipin LohiyaNo ratings yet

- Premier Cement Mills Limited-RbDocument1 pagePremier Cement Mills Limited-Rbmr9_apeceNo ratings yet

- Quick and Dirty Interpretation of RatiosDocument4 pagesQuick and Dirty Interpretation of RatiosGauravNo ratings yet

- Exercises For Chapter 23 EFA2Document13 pagesExercises For Chapter 23 EFA2tuananh leNo ratings yet

- Carpentry Pro Plan v1664134062229Document30 pagesCarpentry Pro Plan v1664134062229jweremaNo ratings yet

Download as pdf or txt

You might also like

- CA Final Audit RISK ASSESSMENT AND INTERNAL CONTROL NotesDocument21 pagesCA Final Audit RISK ASSESSMENT AND INTERNAL CONTROL NotesSARASWATHI S100% (1)

- Jamaica Producers Group FITDocument47 pagesJamaica Producers Group FITGerron Thomas100% (1)

- WW SS-4Document3 pagesWW SS-4cstocksg1100% (7)

- Solution To QB QuestionsDocument3 pagesSolution To QB QuestionsSurabhi Suman100% (1)

- Risk Assessment and Internal Control - E-NotesDocument55 pagesRisk Assessment and Internal Control - E-NotesManavNo ratings yet

- ACCA F8知识要点汇总 (上)Document37 pagesACCA F8知识要点汇总 (上)Freya SunNo ratings yet

- Reviewer AuditDocument9 pagesReviewer AuditElisha BascoNo ratings yet

- Identifying and Assessing Risks of Material MisstatementsDocument2 pagesIdentifying and Assessing Risks of Material MisstatementsCattleyaNo ratings yet

- Chapter 3 - : - Risk Assessment and Internal ControlDocument26 pagesChapter 3 - : - Risk Assessment and Internal ControlTamanna AroraNo ratings yet

- 74937bos60526-Cp4 UnlockedDocument72 pages74937bos60526-Cp4 Unlockedhrudaya boysNo ratings yet

- Caua 3752 - Auditing 1B: Topic and Reference: Auditing NotesDocument42 pagesCaua 3752 - Auditing 1B: Topic and Reference: Auditing NotesMoniqueNo ratings yet

- Control RiskDocument19 pagesControl RiskAnonymous HBzUFPliGsNo ratings yet

- Auditing Theory Salosagcol SummaryDocument32 pagesAuditing Theory Salosagcol Summarylily andrew0% (1)

- Risk and MaterialityDocument4 pagesRisk and MaterialitymsyllNo ratings yet

- Ca Inter Audit Paper July - 2021 Paper Review by CA Kapil GoyalDocument13 pagesCa Inter Audit Paper July - 2021 Paper Review by CA Kapil GoyalEdwin MartinNo ratings yet

- Psa 200: Overall Objectives of The Independent Auditor and The Conduct of AuditDocument3 pagesPsa 200: Overall Objectives of The Independent Auditor and The Conduct of AuditDaren Dame Jodi RentasidaNo ratings yet

- ISA 315 SummaryDocument7 pagesISA 315 SummaryTeam R12-01 Cotabato ProvinceNo ratings yet

- CH 4 - Risk AssessmentDocument35 pagesCH 4 - Risk AssessmentSUMIT SINGHNo ratings yet

- Lecture 6-Audit RiksDocument6 pagesLecture 6-Audit Riksakii ramNo ratings yet

- Risk-Based Approach To Conducting A Quality AuditDocument55 pagesRisk-Based Approach To Conducting A Quality AuditKyla Marie MojicoNo ratings yet

- Risk Assesment & Internal ControlDocument56 pagesRisk Assesment & Internal Controlkaran kapadiaNo ratings yet

- Chapter 19 ReportDocument16 pagesChapter 19 ReportAmira SawadjaanNo ratings yet

- Aud339 Audit Planning Part 2Document26 pagesAud339 Audit Planning Part 2Nur IzzahNo ratings yet

- CA Final Audit AmendmentsDocument39 pagesCA Final Audit AmendmentsAkshit WaliaNo ratings yet

- Referencer For Quick Revision: Intermediate Course Paper-6: Auditing and AssuranceDocument32 pagesReferencer For Quick Revision: Intermediate Course Paper-6: Auditing and AssuranceCutfit HardNo ratings yet

- Referencer For Quick Revision: Intermediate Course Paper-6: Auditing and AssuranceDocument29 pagesReferencer For Quick Revision: Intermediate Course Paper-6: Auditing and AssuranceRamNo ratings yet

- Kitcb D01.nhóm 7Document44 pagesKitcb D01.nhóm 7Mạnh hưng LêNo ratings yet

- AT 4 Audit Risk and MaterialityDocument6 pagesAT 4 Audit Risk and MaterialityLhea ClomaNo ratings yet

- CH 5Document2 pagesCH 5Scholastica DaniaNo ratings yet

- TOPIC 3e - Risk and MaterialityDocument33 pagesTOPIC 3e - Risk and MaterialityLANGITBIRUNo ratings yet

- Chapter 6 Risk Assessment (PART 1)Document9 pagesChapter 6 Risk Assessment (PART 1)Aravinthan INSAF SmartClassNo ratings yet

- Chapter 3: Process of Assurance: Planning The AssignmentDocument12 pagesChapter 3: Process of Assurance: Planning The AssignmentShahid MahmudNo ratings yet

- PBEPIII Inherent Risk PDFDocument5 pagesPBEPIII Inherent Risk PDFkim romanoNo ratings yet

- Adobe Scan Oct 24, 2022Document14 pagesAdobe Scan Oct 24, 2022Emmanuel PenullarNo ratings yet

- Content - 2023 Global PWC Audit Guide - Isas - Isa 315 Revised 2019 Identifying and Assessing The Risks of Material MisstatementDocument95 pagesContent - 2023 Global PWC Audit Guide - Isas - Isa 315 Revised 2019 Identifying and Assessing The Risks of Material MisstatementCường Trần MinhNo ratings yet

- Multiple Choice Questions PDFDocument6 pagesMultiple Choice Questions PDFabdul majid khawajaNo ratings yet

- Financial Statements, Deals With An External Auditor's Responsibilities However, Both Internal andDocument11 pagesFinancial Statements, Deals With An External Auditor's Responsibilities However, Both Internal andDanisa NdhlovuNo ratings yet

- ISA 315 Revised 2019 Updated 2022Document228 pagesISA 315 Revised 2019 Updated 2022Lâm Nguyễn TiếnNo ratings yet

- Interactive Training On Overall Audit Process and DocumentationDocument19 pagesInteractive Training On Overall Audit Process and DocumentationAmenu AdagneNo ratings yet

- Risk Based Audit of FSDocument1 pageRisk Based Audit of FSNavsNo ratings yet

- 4 Audit RiskDocument10 pages4 Audit RiskHussain MustunNo ratings yet

- Audit Quick Review PDFDocument41 pagesAudit Quick Review PDFChunnu ChamkilaNo ratings yet

- Audit Risk and Materiality Week Ending 19 April 2024Document96 pagesAudit Risk and Materiality Week Ending 19 April 2024masilelaemmaculateNo ratings yet

- This Study Resource WasDocument3 pagesThis Study Resource WasYuliana rahayuNo ratings yet

- Overview of AuditingDocument5 pagesOverview of AuditingMylene Sunga AbergasNo ratings yet

- Unit 3 - Internal Control - NotesDocument14 pagesUnit 3 - Internal Control - NotesNabhan JafferNo ratings yet

- Types of Audits: Audit - An OverviewDocument31 pagesTypes of Audits: Audit - An OverviewRanel Clark D. TabiosNo ratings yet

- Chapter 4 Risk Assessment and Internal Control - ScannerDocument64 pagesChapter 4 Risk Assessment and Internal Control - ScannerRanjisi chimbanguNo ratings yet

- AUD Flashcards Flashcards - QuizletDocument16 pagesAUD Flashcards Flashcards - QuizletDieter LudwigNo ratings yet

- Internal Control DocumentationDocument42 pagesInternal Control DocumentationJhoe Marie Balintag100% (1)

- 4 5850471109056532138Document39 pages4 5850471109056532138Yehualashet MulugetaNo ratings yet

- What Is Audit RiskDocument7 pagesWhat Is Audit RiskHoang Ngoc ToNo ratings yet

- Arens AAS17 sm 05筆記版Document20 pagesArens AAS17 sm 05筆記版林芷瑜No ratings yet

- Q1 - Bon GarageDocument5 pagesQ1 - Bon GaragefatihahNo ratings yet

- School of Business, Economics and Management Bps430: Audit Practice and Performance Review Chapter 4: The Theory of AuditingDocument73 pagesSchool of Business, Economics and Management Bps430: Audit Practice and Performance Review Chapter 4: The Theory of AuditingChibwe ChinyamaNo ratings yet

- Audit Standards Summary Compiled With Q & ADocument86 pagesAudit Standards Summary Compiled With Q & Asantosh pandeyNo ratings yet

- SA Flowcharts 2Document33 pagesSA Flowcharts 2partymonger71% (7)

- (MA 4221) - Notes Extern Audit RequirementsDocument3 pages(MA 4221) - Notes Extern Audit RequirementsMichael Tom BucalonNo ratings yet

- Chapter 2 - Lesson Outline - StudentDocument14 pagesChapter 2 - Lesson Outline - StudentKim Heok ChuaNo ratings yet

- AA - Chapter 2Document5 pagesAA - Chapter 2Jacqueline Kanesha JamesNo ratings yet

- Risk Rating The Audit UniverseDocument10 pagesRisk Rating The Audit Universecajitendergupta100% (2)

- Chapter 3 Risk Assement & Internal ControlDocument54 pagesChapter 3 Risk Assement & Internal ControlRohit Kumar SantukaNo ratings yet

- Finance Research Paper Topics ListDocument5 pagesFinance Research Paper Topics Listfzgzygnp100% (1)

- EC3314 Spring PSet 4 SolutionsDocument6 pagesEC3314 Spring PSet 4 Solutionschristina0107No ratings yet

- AmlqDocument3 pagesAmlqtejasrawalNo ratings yet

- Dressen Abridged) (A)Document13 pagesDressen Abridged) (A)mithileshagrawalNo ratings yet

- Topic 3 4 5 6 7 Cash Flow Analysis CFO CFI CFFDocument22 pagesTopic 3 4 5 6 7 Cash Flow Analysis CFO CFI CFFYadu Priya DeviNo ratings yet

- Contract of IndemnificationDocument12 pagesContract of IndemnificationMayank AgrawalNo ratings yet

- CE2402-Estimation and Quantity SurveyingDocument12 pagesCE2402-Estimation and Quantity Surveyingసురేంద్ర కారంపూడిNo ratings yet

- Pledge Case: Pactum CommissoriumDocument2 pagesPledge Case: Pactum CommissoriumSusie VanguardiaNo ratings yet

- Cost of Capital at AmeritradeDocument3 pagesCost of Capital at AmeritradeAnkur JainNo ratings yet

- Tendernotice 1 PDFDocument4 pagesTendernotice 1 PDFChit ChitrarasanNo ratings yet

- Monthly Review August 2023Document17 pagesMonthly Review August 2023Md. Razin Hossain 2021148630No ratings yet

- UFI ProspectusDocument17 pagesUFI ProspectusAlvin Rejano TanNo ratings yet

- User Id 012439461813 - DSL Telephonenumber 01244823150Document6 pagesUser Id 012439461813 - DSL Telephonenumber 01244823150NAVEEN SLNo ratings yet

- Syllabus - Certificate Course in Digital BankingDocument3 pagesSyllabus - Certificate Course in Digital Bankinglekshmi priyaNo ratings yet

- ABA Format File DetailsDocument7 pagesABA Format File DetailsAbbas MohamedNo ratings yet

- 1 RR 7-2009Document5 pages1 RR 7-2009JoyceNo ratings yet

- Etf PDFDocument14 pagesEtf PDFYash MeelNo ratings yet

- 74736bos60488 m2 cp8Document40 pages74736bos60488 m2 cp8Vignesh VigneshNo ratings yet

- Statement 600606 35438479 2 11 2022 1 12 2022Document1 pageStatement 600606 35438479 2 11 2022 1 12 2022Orhan DagdelenNo ratings yet

- Quiz 6Document6 pagesQuiz 6Jyasmine Aura V. AgustinNo ratings yet

- Contact Sushant Kumar Add Sushant Kumar To Your NetworkDocument2 pagesContact Sushant Kumar Add Sushant Kumar To Your NetworkJaspreet Singh SahaniNo ratings yet

- Article On HR Score CardDocument8 pagesArticle On HR Score CardPratibha Sesham100% (1)

- Capital Budgeting NotesDocument5 pagesCapital Budgeting NotesDipin LohiyaNo ratings yet

- Premier Cement Mills Limited-RbDocument1 pagePremier Cement Mills Limited-Rbmr9_apeceNo ratings yet

- Quick and Dirty Interpretation of RatiosDocument4 pagesQuick and Dirty Interpretation of RatiosGauravNo ratings yet

- Exercises For Chapter 23 EFA2Document13 pagesExercises For Chapter 23 EFA2tuananh leNo ratings yet

- Carpentry Pro Plan v1664134062229Document30 pagesCarpentry Pro Plan v1664134062229jweremaNo ratings yet