Download as pdf or txt

You might also like

- For The Period Ending October 05, 2020: Summary of Your AccountDocument1 pageFor The Period Ending October 05, 2020: Summary of Your AccountKrista Schlosser0% (1)

- PPM 158-QP PDFDocument3 pagesPPM 158-QP PDFAnanditaKarNo ratings yet

- Banking Law AssignmentDocument7 pagesBanking Law AssignmentSangeetha RoyNo ratings yet

- Banking and NI Case AnalysisDocument30 pagesBanking and NI Case AnalysisKandarpNo ratings yet

- National Consumer Disputes Redressal Commission's JudgmentDocument13 pagesNational Consumer Disputes Redressal Commission's JudgmentLatest Laws TeamNo ratings yet

- Corp. Bank Vs GowdaDocument7 pagesCorp. Bank Vs GowdaArjun KanadiNo ratings yet

- In The Supreme Court of India Civil Appellate Jurisdiction: Judgment L. Nageswara Rao, JDocument22 pagesIn The Supreme Court of India Civil Appellate Jurisdiction: Judgment L. Nageswara Rao, JsamsthenimmaneNo ratings yet

- In The National Company Law Tribunal Mumbai Bench: Per: Bhaskara Pantula Mohan, Member (J)Document12 pagesIn The National Company Law Tribunal Mumbai Bench: Per: Bhaskara Pantula Mohan, Member (J)saurabhNo ratings yet

- SHDocument231 pagesSHyuvasree talapaneniNo ratings yet

- 9.1 Banking and Financial Laws (Question Paper)Document2 pages9.1 Banking and Financial Laws (Question Paper)Medha DwivediNo ratings yet

- RSPDocument18 pagesRSPRISHI SHARMANo ratings yet

- Bankers To An IssueDocument3 pagesBankers To An IssueNaveen SehrawatNo ratings yet

- Banking Law AssignmentDocument18 pagesBanking Law AssignmentDivya RaoNo ratings yet

- SARFAESI Rulings: Prachi Narayan 7 January, 2014Document5 pagesSARFAESI Rulings: Prachi Narayan 7 January, 2014AASHISH GUPTANo ratings yet

- In The High Court of Karnataka at BangalkoreDocument14 pagesIn The High Court of Karnataka at BangalkoreGanti Santosh KumarNo ratings yet

- 05-Banking & Insur 2016Document34 pages05-Banking & Insur 2016ishikaNo ratings yet

- Amal Peterson Vs The Authorised OfficerDocument14 pagesAmal Peterson Vs The Authorised OfficermshantanuthakurNo ratings yet

- Neeraj Malhotra Vs Deustche Post Bank Home FinancCO100001COM466165Document153 pagesNeeraj Malhotra Vs Deustche Post Bank Home FinancCO100001COM466165urvashiNo ratings yet

- Himalayan Reply CONTINUING (1) - 1Document13 pagesHimalayan Reply CONTINUING (1) - 1Gaurav KumarNo ratings yet

- Bank of India Ltd. Vs Ahmedabad Manufacturing & CalicoDocument6 pagesBank of India Ltd. Vs Ahmedabad Manufacturing & CalicoSaurabh JainNo ratings yet

- 2022 6 1507 39466 Judgement 04-Nov-2022Document20 pages2022 6 1507 39466 Judgement 04-Nov-2022Shivam Shiddharth SinghNo ratings yet

- 431,437,444,447,448,463 - Banking LawDocument10 pages431,437,444,447,448,463 - Banking LawIpkshita SinghNo ratings yet

- Defence-docs-witness-refusal-G V Aswathanarayana Vs Central Bank of India by Chairman On 28 May 2003Document15 pagesDefence-docs-witness-refusal-G V Aswathanarayana Vs Central Bank of India by Chairman On 28 May 2003anwa1No ratings yet

- Notes On The DHFL SCAM AT A GLANCE: FROM THE PERSPECTIVES OF AILING FD HOLDERSDocument16 pagesNotes On The DHFL SCAM AT A GLANCE: FROM THE PERSPECTIVES OF AILING FD HOLDERSDebaprasad BandyopadhyayNo ratings yet

- J 2021 SCC OnLine Kar 12934 AIR 2021 Kar 155 2021 4 AI 20221109 095745 1 8Document8 pagesJ 2021 SCC OnLine Kar 12934 AIR 2021 Kar 155 2021 4 AI 20221109 095745 1 8SAI SUVEDHYA RNo ratings yet

- SARFAESIDocument14 pagesSARFAESIaravind100305No ratings yet

- Lotus Pay Solutions (P) Ltd. v. Union of India, (2022) 5 HCC (Del) 525Document16 pagesLotus Pay Solutions (P) Ltd. v. Union of India, (2022) 5 HCC (Del) 525ayushi agrawalNo ratings yet

- Sarfaesi (1,2)Document15 pagesSarfaesi (1,2)aravind100305No ratings yet

- Pearson Drums Barrels Pvt. Ltd. Vs General Manager High Court CalcuttaDocument14 pagesPearson Drums Barrels Pvt. Ltd. Vs General Manager High Court CalcuttaratnakumariNo ratings yet

- Equivalent Citation: AIR2010SC3534, 2010 (6) ALD29 (SC), 2010Document21 pagesEquivalent Citation: AIR2010SC3534, 2010 (6) ALD29 (SC), 2010Pradeep YadavNo ratings yet

- Before The Divisional Joint Registrar, Co-Operative Societies Mumbai at Navi Mumbai Revision Application No. 55 of 2017Document5 pagesBefore The Divisional Joint Registrar, Co-Operative Societies Mumbai at Navi Mumbai Revision Application No. 55 of 2017Sachin MantriNo ratings yet

- Bank of Baroda Vs Dr. Kamal Gupta & 4 Ors. On 20 December, 2019Document6 pagesBank of Baroda Vs Dr. Kamal Gupta & 4 Ors. On 20 December, 2019Rajan SinghNo ratings yet

- Signature Not VerifiedDocument19 pagesSignature Not VerifiedChandra Sekhar Kakarla100% (1)

- Guidelines On Fair Practices Code For LendersDocument5 pagesGuidelines On Fair Practices Code For LendersAKHI9No ratings yet

- Circular Judgments 13.11.2015Document8 pagesCircular Judgments 13.11.2015g9769916102No ratings yet

- Jindal Saxena Financial Services Pvt. Ltd. v. Mayfair Capital Pvt. LTD., 2017 SCC OnLine NCLT 182Document3 pagesJindal Saxena Financial Services Pvt. Ltd. v. Mayfair Capital Pvt. LTD., 2017 SCC OnLine NCLT 182kavyareddyNo ratings yet

- Order Against M/s Sai Praksah Properties Development Ltd. and Its Directors/promotersDocument22 pagesOrder Against M/s Sai Praksah Properties Development Ltd. and Its Directors/promotersShyam SunderNo ratings yet

- Banking Law - Shivansh Ahuja - 18010126147Document12 pagesBanking Law - Shivansh Ahuja - 18010126147Albatross AhujaNo ratings yet

- A Study of The Customer - Docx Shreya - Docx 1Document49 pagesA Study of The Customer - Docx Shreya - Docx 1Shreya ChavanNo ratings yet

- Judgment D.B. CIVIL SPECIAL APPEAL (W) NO.2021/2011Document11 pagesJudgment D.B. CIVIL SPECIAL APPEAL (W) NO.2021/2011SAKETSHOURAVNo ratings yet

- Vimal Chapter7Document54 pagesVimal Chapter7MitheleshDevarajNo ratings yet

- IBC Case LawDocument3 pagesIBC Case LawPrashant SinghNo ratings yet

- Islamic Finance As An Alternative For Supplementary Loans in Commercial Banks (A Descriptive and Analytical Study of Alternatives)Document13 pagesIslamic Finance As An Alternative For Supplementary Loans in Commercial Banks (A Descriptive and Analytical Study of Alternatives)guadie workuNo ratings yet

- Renaissance University, Indore Proforma of First Page of PresentationsDocument7 pagesRenaissance University, Indore Proforma of First Page of PresentationsMudit MaheshwariNo ratings yet

- Sale of CD Assets Shown As OTS 1711599186Document8 pagesSale of CD Assets Shown As OTS 1711599186advsakthinathanNo ratings yet

- N. Raghavender v. State of A.P.Document19 pagesN. Raghavender v. State of A.P.Manushi SaxenaNo ratings yet

- 430 Late SubmissionDocument16 pages430 Late SubmissionIpkshita SinghNo ratings yet

- Hassad Food Company Q.S.C. v. Bank of India, 2019 SCC OnLine Del 10647Document7 pagesHassad Food Company Q.S.C. v. Bank of India, 2019 SCC OnLine Del 10647tanyaNo ratings yet

- Bikki Raveendra Babu, Member (J)Document16 pagesBikki Raveendra Babu, Member (J)veer vikramNo ratings yet

- Reportable in The Supreme Court of India Civil Appellate Jurisdiction Civil Appeal No.1650 of 2020Document73 pagesReportable in The Supreme Court of India Civil Appellate Jurisdiction Civil Appeal No.1650 of 2020Anirudh PNo ratings yet

- Interim Order Cum Show Cause Notice in The Matter of Bhabiswajyoti Infrastructure India LimitedDocument16 pagesInterim Order Cum Show Cause Notice in The Matter of Bhabiswajyoti Infrastructure India LimitedShyam SunderNo ratings yet

- BoiDocument162 pagesBoiHirakSCNo ratings yet

- 673 Kotak Mahindra Bank Limited V Kew Precision Parts PVT LTD 5 Aug 2022 430323Document15 pages673 Kotak Mahindra Bank Limited V Kew Precision Parts PVT LTD 5 Aug 2022 430323samsthenimmaneNo ratings yet

- 12 - Chapter 6, Mergers and Acquisitions in The Indian Banking SectorDocument6 pages12 - Chapter 6, Mergers and Acquisitions in The Indian Banking SectorRakesh Prabhakar ShrivastavaNo ratings yet

- Case SummaryDocument8 pagesCase SummaryMano FelixNo ratings yet

- Fair Practice CodepdfDocument8 pagesFair Practice CodepdfBharat SolankiNo ratings yet

- 2e9b1the Consumer Protection ActDocument9 pages2e9b1the Consumer Protection ActSidharth KapoorNo ratings yet

- Case Analysis Islamic Banking TakafulDocument11 pagesCase Analysis Islamic Banking Takafulshukri ahmad ikramNo ratings yet

- Sanjay - LabDocument8 pagesSanjay - LabArun VaananNo ratings yet

- 2022 Livelaw (SC) 496: in The Supreme Court of IndiaDocument9 pages2022 Livelaw (SC) 496: in The Supreme Court of IndiaKailash KhaliNo ratings yet

- Competition Law (Optional Paper)Document6 pagesCompetition Law (Optional Paper)Kamal NaraniyaNo ratings yet

- Air and Space Law (Optional Paper)Document3 pagesAir and Space Law (Optional Paper)Kamal NaraniyaNo ratings yet

- Contribution Guidelines (A) Aim of The Journal: Editors@ijal - inDocument3 pagesContribution Guidelines (A) Aim of The Journal: Editors@ijal - inKamal NaraniyaNo ratings yet

- Apple S Notice of Opposition V Super Healthy Kids IncDocument548 pagesApple S Notice of Opposition V Super Healthy Kids IncKamal NaraniyaNo ratings yet

- Assignment of SarthiDocument27 pagesAssignment of SarthiKamal NaraniyaNo ratings yet

- Book Review by Mrs. Jayashree Thakre: GM Momin Women's College, Bhiwandi, Maharashtra, IndiaDocument5 pagesBook Review by Mrs. Jayashree Thakre: GM Momin Women's College, Bhiwandi, Maharashtra, IndiaKamal NaraniyaNo ratings yet

- Case A Large Bench of 7 Judge Was: SP Sampath Kumar v. UOI 1987 SCR (3) 233. L. Chandra Kumar v. UOI (1977) 3 SCC 261Document6 pagesCase A Large Bench of 7 Judge Was: SP Sampath Kumar v. UOI 1987 SCR (3) 233. L. Chandra Kumar v. UOI (1977) 3 SCC 261Kamal NaraniyaNo ratings yet

- Against StateDocument18 pagesAgainst StateKamal NaraniyaNo ratings yet

- Ringkasan Saham-20210723Document90 pagesRingkasan Saham-20210723IrwanNo ratings yet

- FV-Lump Sum PV-Lump Sum PV-Different Interest Rates Time To Double A Lump Sum TVM Comparisons Growth Rate FV-Ordinary Annuity FV-Annuity DueDocument10 pagesFV-Lump Sum PV-Lump Sum PV-Different Interest Rates Time To Double A Lump Sum TVM Comparisons Growth Rate FV-Ordinary Annuity FV-Annuity Duehoangyen260803No ratings yet

- Roadside Assistance: Tax InvoiceDocument2 pagesRoadside Assistance: Tax InvoiceBessNo ratings yet

- WellsFargoDocument4 pagesWellsFargofathyNo ratings yet

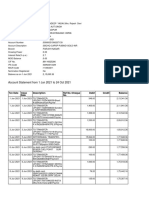

- Account Statement From 1 Jun 2021 To 24 Oct 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument7 pagesAccount Statement From 1 Jun 2021 To 24 Oct 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceProxyNo ratings yet

- Final Exam ANT FINANCIAL CASE QuestionsDocument4 pagesFinal Exam ANT FINANCIAL CASE Questionsfideliadwiksa krisensiaNo ratings yet

- PayingDocument16 pagesPayingNhư NgọcNo ratings yet

- Business Model of Nagad and Surjopay - Com.bd.Document17 pagesBusiness Model of Nagad and Surjopay - Com.bd.Golam ZelaniNo ratings yet

- Chapter - Dissolution of Partnership PDFDocument5 pagesChapter - Dissolution of Partnership PDFBHUMIKA JAINNo ratings yet

- Secretary's Certificate For LandbankDocument2 pagesSecretary's Certificate For LandbankMarriane SapitanNo ratings yet

- Third Space Learning Compound Interest GCSE Worksheet 1Document12 pagesThird Space Learning Compound Interest GCSE Worksheet 1erin zietsmanNo ratings yet

- Commercial Bank Platinum Credit CardDocument2 pagesCommercial Bank Platinum Credit Cardsaraju_felixNo ratings yet

- Detailed Procedure To Register A Vehicle in Luxembourg - May 2017Document4 pagesDetailed Procedure To Register A Vehicle in Luxembourg - May 2017Ting ohnNo ratings yet

- CritDocument4 pagesCritMikhail Ayman MasturaNo ratings yet

- Green Banking ActivitiesDocument37 pagesGreen Banking ActivitiesShoumik MahmudNo ratings yet

- Banking CompaniesDocument18 pagesBanking CompaniesSunanda SharmaNo ratings yet

- Chapter 1 Introduction To Financial ManagementDocument30 pagesChapter 1 Introduction To Financial ManagementMark DavidNo ratings yet

- The Indian Payments Handbook 2021 2026Document34 pagesThe Indian Payments Handbook 2021 2026scienceplexNo ratings yet

- Online Banking DownloadDocument4 pagesOnline Banking DownloadANDREW STRUGNELLNo ratings yet

- International TakeoverDocument38 pagesInternational TakeoverHector Quispe CruzNo ratings yet

- CA Inter Advanced Account - Regular Course by CA P S BeniwalDocument346 pagesCA Inter Advanced Account - Regular Course by CA P S BeniwalHarry PotterNo ratings yet

- Study On Consumer Durable Loans and GoodsDocument73 pagesStudy On Consumer Durable Loans and GoodsRoshan Ghatge RG100% (1)

- Geschaeftsbericht UCB AG Bericht 2021 ENGLISCHDocument152 pagesGeschaeftsbericht UCB AG Bericht 2021 ENGLISCHCHIARA DI MARTINONo ratings yet

- ACI Godrej Agrovet Private Limited Account StatementDocument7 pagesACI Godrej Agrovet Private Limited Account StatementMd Al Mamun RintuNo ratings yet

- Sagar R: Account StatementDocument6 pagesSagar R: Account Statementsagar R RaoNo ratings yet

- ICICI Bank Launches ICICI STACK For Corporates To Offer Ecosystem BankingDocument3 pagesICICI Bank Launches ICICI STACK For Corporates To Offer Ecosystem BankingRam CharanNo ratings yet

- Junta Rulebook-2 PDFDocument6 pagesJunta Rulebook-2 PDFHenrique AndradeNo ratings yet

- Altman (2020)Document28 pagesAltman (2020)Juan PerezNo ratings yet

- Banking on IP_UKIPODocument224 pagesBanking on IP_UKIPOraniNo ratings yet