Solution 2009

Solution 2009

You might also like

- Essentials of Investments 11th Edition Bodie Solutions ManualDocument7 pagesEssentials of Investments 11th Edition Bodie Solutions ManualDavidWilliamsxwdgs94% (18)

- Financial Reporting and AnalysisDocument50 pagesFinancial Reporting and AnalysisGeorge Shevtsov83% (6)

- Multiple Choice: Principles of Accounting, Volume 2: Managerial AccountingDocument46 pagesMultiple Choice: Principles of Accounting, Volume 2: Managerial Accountingquanghuymc100% (2)

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- Responsibility AccountingDocument10 pagesResponsibility AccountingCheny MabiniNo ratings yet

- MCS SumsDocument29 pagesMCS SumsRahul GargNo ratings yet

- Segment and Intrim Reporting HandoutDocument7 pagesSegment and Intrim Reporting HandoutMulugeta NiguseNo ratings yet

- ACCTG 7 Chapter 14 Exercises 56Document2 pagesACCTG 7 Chapter 14 Exercises 56freaann03No ratings yet

- SD17 Hybrid F5 Section C Answers Clean Proof PDFDocument12 pagesSD17 Hybrid F5 Section C Answers Clean Proof PDFShaksham SharmaNo ratings yet

- Cost ST - 1 2018 (Solu)Document6 pagesCost ST - 1 2018 (Solu)chitkarashellyNo ratings yet

- Capital Budgeting IiiDocument25 pagesCapital Budgeting IiiRanu AgrawalNo ratings yet

- PM EdcDocument10 pagesPM EdcAlbee Koh Jia YeeNo ratings yet

- Chapter 14 Answer PDF FreeDocument24 pagesChapter 14 Answer PDF FreeAang GrandeNo ratings yet

- ORBITA - Relevant Costing ActivityDocument3 pagesORBITA - Relevant Costing ActivityCarmellae OrbitaNo ratings yet

- Chapter 24Document28 pagesChapter 24Shahaleel Alboridi0% (2)

- CVP MC 1920 W KeyDocument6 pagesCVP MC 1920 W KeyGale RasNo ratings yet

- EXERCISE 12-2 (15 Minutes)Document9 pagesEXERCISE 12-2 (15 Minutes)Mari Louis Noriell MejiaNo ratings yet

- Book-Responsibility Actg-SolMan PDFDocument18 pagesBook-Responsibility Actg-SolMan PDFLordson RamosNo ratings yet

- Chapter 14 - Answer PDFDocument18 pagesChapter 14 - Answer PDFAldrin ZlmdNo ratings yet

- Chapter 14Document18 pagesChapter 14RenNo ratings yet

- Return On InvestmentDocument5 pagesReturn On Investmentela kikay100% (1)

- Cost Classification: Total Product/ ServiceDocument21 pagesCost Classification: Total Product/ ServiceThureinNo ratings yet

- Responsibility Acctg Transfer Pricing GP Analysis PDFDocument21 pagesResponsibility Acctg Transfer Pricing GP Analysis PDFma quenaNo ratings yet

- PERMALINO - Learning Activity 19. Working Capital ManagementDocument3 pagesPERMALINO - Learning Activity 19. Working Capital ManagementAra Joyce PermalinoNo ratings yet

- Statemen of Comprehensive IncomeDocument2 pagesStatemen of Comprehensive IncomeAnne Marieline Buenaventura0% (1)

- FAR Material-2Document8 pagesFAR Material-2Blessy Zedlav LacbainNo ratings yet

- Solution Class 12 - Accountancy Half Syllabus: For Admission Contact 1 / 10Document10 pagesSolution Class 12 - Accountancy Half Syllabus: For Admission Contact 1 / 10Shaindra SinghNo ratings yet

- Responsibility Acctg Transfer Pricing GP AnalysisDocument21 pagesResponsibility Acctg Transfer Pricing GP AnalysisMoon LightNo ratings yet

- Responsibility Acctg, Transfer Pricing & GP AnalysisDocument21 pagesResponsibility Acctg, Transfer Pricing & GP AnalysisGelyn CruzNo ratings yet

- Lecture 27Document34 pagesLecture 27Riaz Baloch NotezaiNo ratings yet

- MCS University Ques. Paper 2001-2009Document19 pagesMCS University Ques. Paper 2001-2009hepatbya50% (2)

- Corporate Finance JUNE 2022Document7 pagesCorporate Finance JUNE 2022Rajni KumariNo ratings yet

- MAS Final Preboard QuestionsDocument12 pagesMAS Final Preboard QuestionsVillanueva, Mariella De VeraNo ratings yet

- Mock CPA Board Examinations (Mas)Document8 pagesMock CPA Board Examinations (Mas)Lara Lewis Achilles100% (1)

- Solutions Additional ExercisesDocument87 pagesSolutions Additional Exercisesapi-3767414No ratings yet

- Cost Accounting & Financial Management Solved Paper Nov 2009, Chartered AccountancyDocument16 pagesCost Accounting & Financial Management Solved Paper Nov 2009, Chartered AccountancyAnkit2020No ratings yet

- FinalexamDocument12 pagesFinalexamJoshua GibsonNo ratings yet

- 28 Solved PCC Cost FM Nov09Document16 pages28 Solved PCC Cost FM Nov09Karan Joshi100% (1)

- ISV Managerial Accounting, 4e: Final Exam: Chapters 1-14Document85 pagesISV Managerial Accounting, 4e: Final Exam: Chapters 1-14Mikaela SeminianoNo ratings yet

- Managerial Accounting PDFDocument6 pagesManagerial Accounting PDFProsenJit KarmakarNo ratings yet

- PROBLEM 4 (Evaluation of Performance) : TotalDocument3 pagesPROBLEM 4 (Evaluation of Performance) : TotalArt IslandNo ratings yet

- MS-1stPB 10.22Document12 pagesMS-1stPB 10.22Harold Dan Acebedo0% (1)

- CH 5 Flexible Budget-7Document23 pagesCH 5 Flexible Budget-7ed tuNo ratings yet

- Suggested Answer of November 2019 ExamDocument21 pagesSuggested Answer of November 2019 ExamRakshitha VarshaNo ratings yet

- Take Home Examination Bbma3203Document6 pagesTake Home Examination Bbma3203Sufian Abd RahimNo ratings yet

- Exercises Responsibility Accounting AnswersDocument6 pagesExercises Responsibility Accounting AnswersAlexis Jaina Tinaan100% (1)

- 92 08 DeductionsDocument18 pages92 08 DeductionsNikkoNo ratings yet

- 06 - Responsibility Accounting - LectureDocument7 pages06 - Responsibility Accounting - LecturedumpyforhimNo ratings yet

- CH 5 Flexible BudgetDocument23 pagesCH 5 Flexible Budgettamirat tadeseNo ratings yet

- Responsibility Acctg Transfer Pricing GP Analysis 1Document21 pagesResponsibility Acctg Transfer Pricing GP Analysis 1John Bryan100% (1)

- Cup-Management Advisory ServicesDocument7 pagesCup-Management Advisory ServicesJerauld BucolNo ratings yet

- Mas Cup 21 - QuestionsDocument4 pagesMas Cup 21 - QuestionsPhilip CastroNo ratings yet

- Revaluation Gain On Sale and ImpairmentDocument5 pagesRevaluation Gain On Sale and ImpairmentDyno Laurence Karl GallogoNo ratings yet

- Management Advisory Services: Responsibility Accounting & Transfer PricingDocument9 pagesManagement Advisory Services: Responsibility Accounting & Transfer PricingVanessa Arizo ValenciaNo ratings yet

- Answer Key Week 4Document10 pagesAnswer Key Week 4Chin FiguraNo ratings yet

- Responsibility AccountingDocument21 pagesResponsibility AccountingMicaella GrandeNo ratings yet

- Wiley CMAexcel Learning System Exam Review 2017: Part 1, Financial Reporting, Planning, Performance, and Control (1-year access)From EverandWiley CMAexcel Learning System Exam Review 2017: Part 1, Financial Reporting, Planning, Performance, and Control (1-year access)No ratings yet

- The Entrepreneur’S Dictionary of Business and Financial TermsFrom EverandThe Entrepreneur’S Dictionary of Business and Financial TermsNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Beyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkFrom EverandBeyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkNo ratings yet

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Kelvion India Private Limited 10-06-2021Document18 pagesKelvion India Private Limited 10-06-2021suresh sivadasanNo ratings yet

- Caap Practice Manual Executive ProgDocument483 pagesCaap Practice Manual Executive Progsalaarbhai2322No ratings yet

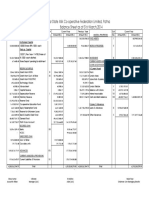

- Bihar State Milk Co-Operative Federation Limited, Patna Balance Sheet As at 31st March, 2014Document1 pageBihar State Milk Co-Operative Federation Limited, Patna Balance Sheet As at 31st March, 2014SATYAM KUMARNo ratings yet

- Excel 2Document8 pagesExcel 2Vignesh BalachandarNo ratings yet

- Poa FormatDocument4 pagesPoa FormatSumithaNo ratings yet

- 159 Milan DumreDocument46 pages159 Milan Dumre02 - CM Ankita AdamNo ratings yet

- Business Plan Pre Final ExamDocument4 pagesBusiness Plan Pre Final ExamRenan De GuzmanNo ratings yet

- Account Types in ConsolidationDocument5 pagesAccount Types in ConsolidationKrishna GBNo ratings yet

- Conceptual Frame WorrkDocument10 pagesConceptual Frame WorrkChota H MpukuNo ratings yet

- SEC 17-Q (1st QRTR 31 March 2014)Document49 pagesSEC 17-Q (1st QRTR 31 March 2014)RCCruzNo ratings yet

- Conceptual Framework and Accounting StandardsDocument11 pagesConceptual Framework and Accounting StandardsAngela TalastasNo ratings yet

- P4 Taxation New Suggested CA Inter May 18Document27 pagesP4 Taxation New Suggested CA Inter May 18Durgadevi BaskaranNo ratings yet

- Accounting For Non-Current AssetsDocument4 pagesAccounting For Non-Current AssetsPrinceNo ratings yet

- ExmDocument18 pagesExmRoy Mitz Bautista0% (2)

- Derivatives Market FinalDocument19 pagesDerivatives Market FinalRohit ChellaniNo ratings yet

- Introduction To Transfer TaxationDocument6 pagesIntroduction To Transfer TaxationHazel Jane EsclamadaNo ratings yet

- Chap 008Document66 pagesChap 008dsementsova100% (1)

- Cash Flow StatementDocument46 pagesCash Flow StatementSiraj Siddiqui100% (1)

- CapitalisationDocument9 pagesCapitalisationselvakrishnaNo ratings yet

- Group 3 - BUSINESS PLANDocument16 pagesGroup 3 - BUSINESS PLANShuu SaiharaNo ratings yet

- EduX.F3A 1 01-CAIXINDocument10 pagesEduX.F3A 1 01-CAIXINvetNo ratings yet

- Section 3 and 4Document6 pagesSection 3 and 4Alaine DobleNo ratings yet

- Dey's Sample Paper-05 - Accountancy-XII - 2023Document8 pagesDey's Sample Paper-05 - Accountancy-XII - 2023Akshat RajeshNo ratings yet

- اختبار أنماط الشخصية لمايرز وبريجزDocument22 pagesاختبار أنماط الشخصية لمايرز وبريجزakeelahNo ratings yet

- Manual Asset Revaluation PDFDocument4 pagesManual Asset Revaluation PDFrajiwani100% (1)

- Accounting Fundamentals II: Lesson 4 (Printer-Friendly Version)Document7 pagesAccounting Fundamentals II: Lesson 4 (Printer-Friendly Version)gretatamaraNo ratings yet

- Financial StatementDocument13 pagesFinancial StatementkeyurNo ratings yet

Download as pdf or txt

You might also like

- Essentials of Investments 11th Edition Bodie Solutions ManualDocument7 pagesEssentials of Investments 11th Edition Bodie Solutions ManualDavidWilliamsxwdgs94% (18)

- Financial Reporting and AnalysisDocument50 pagesFinancial Reporting and AnalysisGeorge Shevtsov83% (6)

- Multiple Choice: Principles of Accounting, Volume 2: Managerial AccountingDocument46 pagesMultiple Choice: Principles of Accounting, Volume 2: Managerial Accountingquanghuymc100% (2)

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- Responsibility AccountingDocument10 pagesResponsibility AccountingCheny MabiniNo ratings yet

- MCS SumsDocument29 pagesMCS SumsRahul GargNo ratings yet

- Segment and Intrim Reporting HandoutDocument7 pagesSegment and Intrim Reporting HandoutMulugeta NiguseNo ratings yet

- ACCTG 7 Chapter 14 Exercises 56Document2 pagesACCTG 7 Chapter 14 Exercises 56freaann03No ratings yet

- SD17 Hybrid F5 Section C Answers Clean Proof PDFDocument12 pagesSD17 Hybrid F5 Section C Answers Clean Proof PDFShaksham SharmaNo ratings yet

- Cost ST - 1 2018 (Solu)Document6 pagesCost ST - 1 2018 (Solu)chitkarashellyNo ratings yet

- Capital Budgeting IiiDocument25 pagesCapital Budgeting IiiRanu AgrawalNo ratings yet

- PM EdcDocument10 pagesPM EdcAlbee Koh Jia YeeNo ratings yet

- Chapter 14 Answer PDF FreeDocument24 pagesChapter 14 Answer PDF FreeAang GrandeNo ratings yet

- ORBITA - Relevant Costing ActivityDocument3 pagesORBITA - Relevant Costing ActivityCarmellae OrbitaNo ratings yet

- Chapter 24Document28 pagesChapter 24Shahaleel Alboridi0% (2)

- CVP MC 1920 W KeyDocument6 pagesCVP MC 1920 W KeyGale RasNo ratings yet

- EXERCISE 12-2 (15 Minutes)Document9 pagesEXERCISE 12-2 (15 Minutes)Mari Louis Noriell MejiaNo ratings yet

- Book-Responsibility Actg-SolMan PDFDocument18 pagesBook-Responsibility Actg-SolMan PDFLordson RamosNo ratings yet

- Chapter 14 - Answer PDFDocument18 pagesChapter 14 - Answer PDFAldrin ZlmdNo ratings yet

- Chapter 14Document18 pagesChapter 14RenNo ratings yet

- Return On InvestmentDocument5 pagesReturn On Investmentela kikay100% (1)

- Cost Classification: Total Product/ ServiceDocument21 pagesCost Classification: Total Product/ ServiceThureinNo ratings yet

- Responsibility Acctg Transfer Pricing GP Analysis PDFDocument21 pagesResponsibility Acctg Transfer Pricing GP Analysis PDFma quenaNo ratings yet

- PERMALINO - Learning Activity 19. Working Capital ManagementDocument3 pagesPERMALINO - Learning Activity 19. Working Capital ManagementAra Joyce PermalinoNo ratings yet

- Statemen of Comprehensive IncomeDocument2 pagesStatemen of Comprehensive IncomeAnne Marieline Buenaventura0% (1)

- FAR Material-2Document8 pagesFAR Material-2Blessy Zedlav LacbainNo ratings yet

- Solution Class 12 - Accountancy Half Syllabus: For Admission Contact 1 / 10Document10 pagesSolution Class 12 - Accountancy Half Syllabus: For Admission Contact 1 / 10Shaindra SinghNo ratings yet

- Responsibility Acctg Transfer Pricing GP AnalysisDocument21 pagesResponsibility Acctg Transfer Pricing GP AnalysisMoon LightNo ratings yet

- Responsibility Acctg, Transfer Pricing & GP AnalysisDocument21 pagesResponsibility Acctg, Transfer Pricing & GP AnalysisGelyn CruzNo ratings yet

- Lecture 27Document34 pagesLecture 27Riaz Baloch NotezaiNo ratings yet

- MCS University Ques. Paper 2001-2009Document19 pagesMCS University Ques. Paper 2001-2009hepatbya50% (2)

- Corporate Finance JUNE 2022Document7 pagesCorporate Finance JUNE 2022Rajni KumariNo ratings yet

- MAS Final Preboard QuestionsDocument12 pagesMAS Final Preboard QuestionsVillanueva, Mariella De VeraNo ratings yet

- Mock CPA Board Examinations (Mas)Document8 pagesMock CPA Board Examinations (Mas)Lara Lewis Achilles100% (1)

- Solutions Additional ExercisesDocument87 pagesSolutions Additional Exercisesapi-3767414No ratings yet

- Cost Accounting & Financial Management Solved Paper Nov 2009, Chartered AccountancyDocument16 pagesCost Accounting & Financial Management Solved Paper Nov 2009, Chartered AccountancyAnkit2020No ratings yet

- FinalexamDocument12 pagesFinalexamJoshua GibsonNo ratings yet

- 28 Solved PCC Cost FM Nov09Document16 pages28 Solved PCC Cost FM Nov09Karan Joshi100% (1)

- ISV Managerial Accounting, 4e: Final Exam: Chapters 1-14Document85 pagesISV Managerial Accounting, 4e: Final Exam: Chapters 1-14Mikaela SeminianoNo ratings yet

- Managerial Accounting PDFDocument6 pagesManagerial Accounting PDFProsenJit KarmakarNo ratings yet

- PROBLEM 4 (Evaluation of Performance) : TotalDocument3 pagesPROBLEM 4 (Evaluation of Performance) : TotalArt IslandNo ratings yet

- MS-1stPB 10.22Document12 pagesMS-1stPB 10.22Harold Dan Acebedo0% (1)

- CH 5 Flexible Budget-7Document23 pagesCH 5 Flexible Budget-7ed tuNo ratings yet

- Suggested Answer of November 2019 ExamDocument21 pagesSuggested Answer of November 2019 ExamRakshitha VarshaNo ratings yet

- Take Home Examination Bbma3203Document6 pagesTake Home Examination Bbma3203Sufian Abd RahimNo ratings yet

- Exercises Responsibility Accounting AnswersDocument6 pagesExercises Responsibility Accounting AnswersAlexis Jaina Tinaan100% (1)

- 92 08 DeductionsDocument18 pages92 08 DeductionsNikkoNo ratings yet

- 06 - Responsibility Accounting - LectureDocument7 pages06 - Responsibility Accounting - LecturedumpyforhimNo ratings yet

- CH 5 Flexible BudgetDocument23 pagesCH 5 Flexible Budgettamirat tadeseNo ratings yet

- Responsibility Acctg Transfer Pricing GP Analysis 1Document21 pagesResponsibility Acctg Transfer Pricing GP Analysis 1John Bryan100% (1)

- Cup-Management Advisory ServicesDocument7 pagesCup-Management Advisory ServicesJerauld BucolNo ratings yet

- Mas Cup 21 - QuestionsDocument4 pagesMas Cup 21 - QuestionsPhilip CastroNo ratings yet

- Revaluation Gain On Sale and ImpairmentDocument5 pagesRevaluation Gain On Sale and ImpairmentDyno Laurence Karl GallogoNo ratings yet

- Management Advisory Services: Responsibility Accounting & Transfer PricingDocument9 pagesManagement Advisory Services: Responsibility Accounting & Transfer PricingVanessa Arizo ValenciaNo ratings yet

- Answer Key Week 4Document10 pagesAnswer Key Week 4Chin FiguraNo ratings yet

- Responsibility AccountingDocument21 pagesResponsibility AccountingMicaella GrandeNo ratings yet

- Wiley CMAexcel Learning System Exam Review 2017: Part 1, Financial Reporting, Planning, Performance, and Control (1-year access)From EverandWiley CMAexcel Learning System Exam Review 2017: Part 1, Financial Reporting, Planning, Performance, and Control (1-year access)No ratings yet

- The Entrepreneur’S Dictionary of Business and Financial TermsFrom EverandThe Entrepreneur’S Dictionary of Business and Financial TermsNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Beyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkFrom EverandBeyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkNo ratings yet

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Kelvion India Private Limited 10-06-2021Document18 pagesKelvion India Private Limited 10-06-2021suresh sivadasanNo ratings yet

- Caap Practice Manual Executive ProgDocument483 pagesCaap Practice Manual Executive Progsalaarbhai2322No ratings yet

- Bihar State Milk Co-Operative Federation Limited, Patna Balance Sheet As at 31st March, 2014Document1 pageBihar State Milk Co-Operative Federation Limited, Patna Balance Sheet As at 31st March, 2014SATYAM KUMARNo ratings yet

- Excel 2Document8 pagesExcel 2Vignesh BalachandarNo ratings yet

- Poa FormatDocument4 pagesPoa FormatSumithaNo ratings yet

- 159 Milan DumreDocument46 pages159 Milan Dumre02 - CM Ankita AdamNo ratings yet

- Business Plan Pre Final ExamDocument4 pagesBusiness Plan Pre Final ExamRenan De GuzmanNo ratings yet

- Account Types in ConsolidationDocument5 pagesAccount Types in ConsolidationKrishna GBNo ratings yet

- Conceptual Frame WorrkDocument10 pagesConceptual Frame WorrkChota H MpukuNo ratings yet

- SEC 17-Q (1st QRTR 31 March 2014)Document49 pagesSEC 17-Q (1st QRTR 31 March 2014)RCCruzNo ratings yet

- Conceptual Framework and Accounting StandardsDocument11 pagesConceptual Framework and Accounting StandardsAngela TalastasNo ratings yet

- P4 Taxation New Suggested CA Inter May 18Document27 pagesP4 Taxation New Suggested CA Inter May 18Durgadevi BaskaranNo ratings yet

- Accounting For Non-Current AssetsDocument4 pagesAccounting For Non-Current AssetsPrinceNo ratings yet

- ExmDocument18 pagesExmRoy Mitz Bautista0% (2)

- Derivatives Market FinalDocument19 pagesDerivatives Market FinalRohit ChellaniNo ratings yet

- Introduction To Transfer TaxationDocument6 pagesIntroduction To Transfer TaxationHazel Jane EsclamadaNo ratings yet

- Chap 008Document66 pagesChap 008dsementsova100% (1)

- Cash Flow StatementDocument46 pagesCash Flow StatementSiraj Siddiqui100% (1)

- CapitalisationDocument9 pagesCapitalisationselvakrishnaNo ratings yet

- Group 3 - BUSINESS PLANDocument16 pagesGroup 3 - BUSINESS PLANShuu SaiharaNo ratings yet

- EduX.F3A 1 01-CAIXINDocument10 pagesEduX.F3A 1 01-CAIXINvetNo ratings yet

- Section 3 and 4Document6 pagesSection 3 and 4Alaine DobleNo ratings yet

- Dey's Sample Paper-05 - Accountancy-XII - 2023Document8 pagesDey's Sample Paper-05 - Accountancy-XII - 2023Akshat RajeshNo ratings yet

- اختبار أنماط الشخصية لمايرز وبريجزDocument22 pagesاختبار أنماط الشخصية لمايرز وبريجزakeelahNo ratings yet

- Manual Asset Revaluation PDFDocument4 pagesManual Asset Revaluation PDFrajiwani100% (1)

- Accounting Fundamentals II: Lesson 4 (Printer-Friendly Version)Document7 pagesAccounting Fundamentals II: Lesson 4 (Printer-Friendly Version)gretatamaraNo ratings yet

- Financial StatementDocument13 pagesFinancial StatementkeyurNo ratings yet