Download as pdf or txt

You might also like

- Mckinsey Presentation On Managing The DownturnDocument16 pagesMckinsey Presentation On Managing The DownturnRehan FariasNo ratings yet

- Bulletin - CPI December 2021.Document11 pagesBulletin - CPI December 2021.kingsleyNo ratings yet

- August 2021 August 2021: Bank of Tanzania Bank of TanzaniaDocument30 pagesAugust 2021 August 2021: Bank of Tanzania Bank of TanzaniaArden Muhumuza KitomariNo ratings yet

- Monthly Chartbook 6 Jan 23Document53 pagesMonthly Chartbook 6 Jan 23avinash sharmaNo ratings yet

- SP 500 Eps EstDocument65 pagesSP 500 Eps EsteoaffxNo ratings yet

- TV Ad Volumes Insights:: The Mid-Year AnalysisDocument13 pagesTV Ad Volumes Insights:: The Mid-Year AnalysisNishtha ChaurasiaNo ratings yet

- India TV Ad Volumes Insights - The Mid-Year Analysis 2021Document13 pagesIndia TV Ad Volumes Insights - The Mid-Year Analysis 2021Poornima Shettigar UpletawalaNo ratings yet

- CS Lviii 33 19082023Document2 pagesCS Lviii 33 19082023ram917722No ratings yet

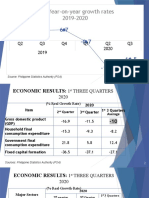

- Blemishing GDP Quarterly ResultsDocument4 pagesBlemishing GDP Quarterly ResultsCritiNo ratings yet

- Indian Economy Website Sep 3 2019Document1 pageIndian Economy Website Sep 3 2019nipun sharmaNo ratings yet

- MER February 2022Document29 pagesMER February 2022Arden Muhumuza KitomariNo ratings yet

- US-China Trade War Tariffs: An Up-to-Date Chart: Updated On December 19, 2019Document1 pageUS-China Trade War Tariffs: An Up-to-Date Chart: Updated On December 19, 2019Asha Si AchaNo ratings yet

- NBFC Tracker 2023Document10 pagesNBFC Tracker 2023jigihereNo ratings yet

- Naukri Jobspeak: Hiring Trends by City, Industry, Functional Area and ExperienceDocument10 pagesNaukri Jobspeak: Hiring Trends by City, Industry, Functional Area and ExperienceMeMyKTNo ratings yet

- Bank of Tanzania: AaaaaDocument30 pagesBank of Tanzania: AaaaaaureliaNo ratings yet

- CRFB The Fiscal Outlook After The Debt Limit DealDocument31 pagesCRFB The Fiscal Outlook After The Debt Limit DealjordanNo ratings yet

- Economic Highlights - Vietnam: Economic Data Showing Signs of Weakness in July - 30/07/2010Document4 pagesEconomic Highlights - Vietnam: Economic Data Showing Signs of Weakness in July - 30/07/2010Rhb InvestNo ratings yet

- Economy: IndiaDocument8 pagesEconomy: IndiaRavichandra BNo ratings yet

- Economic Highlights - Vietnam: Economic Activities Held Up Relatively Well in September - 29/09/2010Document4 pagesEconomic Highlights - Vietnam: Economic Activities Held Up Relatively Well in September - 29/09/2010Rhb InvestNo ratings yet

- July 2021 MerDocument32 pagesJuly 2021 MerArden Muhumuza KitomariNo ratings yet

- China - Should We Worry About The Falling FDIDocument8 pagesChina - Should We Worry About The Falling FDISumanth GururajNo ratings yet

- State Budget Analysis KA 2020-21 FinalDocument7 pagesState Budget Analysis KA 2020-21 Finalmohdahmed12345No ratings yet

- IEP Presentation June 2023 MacroDocument15 pagesIEP Presentation June 2023 MacroBona Christanto SiahaanNo ratings yet

- MOLS Ecoscpe 3 Jan 2019Document8 pagesMOLS Ecoscpe 3 Jan 2019rchawdhry123No ratings yet

- Argentina Economy - GDP, Inflation, CPI and Interest Rate PDFDocument3 pagesArgentina Economy - GDP, Inflation, CPI and Interest Rate PDFRoberto ManNo ratings yet

- Bank of Tanzania: AaaaaDocument33 pagesBank of Tanzania: AaaaaWilliam MuhomiNo ratings yet

- Indian Economy - Website - Aug 9 2022Document1 pageIndian Economy - Website - Aug 9 2022vinay jodNo ratings yet

- CS Lviii 24 17062023Document3 pagesCS Lviii 24 17062023leo lokeshNo ratings yet

- Fs Idxindust Per 2022 03Document3 pagesFs Idxindust Per 2022 03Rizki FebariNo ratings yet

- ETF Newsletter - February - 23Document20 pagesETF Newsletter - February - 23Chuck CookNo ratings yet

- The Richest 20 Percent Facing More Inflation Than The Poorest 20 PercentDocument4 pagesThe Richest 20 Percent Facing More Inflation Than The Poorest 20 PercentUttiya RoyNo ratings yet

- Macroscope: Nov18 Trade Result Could Trigger (Another) Front-Loaded Rate HikeDocument5 pagesMacroscope: Nov18 Trade Result Could Trigger (Another) Front-Loaded Rate HikeKurnia NindyoNo ratings yet

- IIFL - D-Mart - FY22 AR Analysis - 20220727Document15 pagesIIFL - D-Mart - FY22 AR Analysis - 20220727Bhav Bhagwan HaiNo ratings yet

- LFS202020 Employed - 02dec2020 - Final1Document1 pageLFS202020 Employed - 02dec2020 - Final1alvin.requieroNo ratings yet

- Arrow - Dry Bulk Outlook - Apr-20Document22 pagesArrow - Dry Bulk Outlook - Apr-20Sahil FarazNo ratings yet

- NAMC Food Price Monitor May 2023Document16 pagesNAMC Food Price Monitor May 2023xolaneNo ratings yet

- Economic Outlook - July 2020Document8 pagesEconomic Outlook - July 2020KaraNo ratings yet

- Us China Trade War TariffsDocument11 pagesUs China Trade War TariffsazmykiranovaaNo ratings yet

- Economic - 200709 - May IPI - ADBSDocument4 pagesEconomic - 200709 - May IPI - ADBSAhmadZulkhairiNo ratings yet

- India International Trade Investment Website June 2022Document18 pagesIndia International Trade Investment Website June 2022vinay jodNo ratings yet

- Real GDPTracking SlidesDocument5 pagesReal GDPTracking SlidesmbidNo ratings yet

- Pick of The Week Ongc LTDDocument4 pagesPick of The Week Ongc LTDAnkit JagetiaNo ratings yet

- Summary of Economic and Financial Data May 2023Document16 pagesSummary of Economic and Financial Data May 2023Asare AmoabengNo ratings yet

- Sinking Deeper: Lockdowns and Restrictions Have Hit Harder Than ExpectedDocument6 pagesSinking Deeper: Lockdowns and Restrictions Have Hit Harder Than Expectedabhinavsingh4uNo ratings yet

- Macroeconomic Update 2020Document22 pagesMacroeconomic Update 2020Fuhad AhmedNo ratings yet

- 202003261100349638864web Final Industry Consumption Report February 2020 PDFDocument17 pages202003261100349638864web Final Industry Consumption Report February 2020 PDFpraful s.gNo ratings yet

- Talk Shop Asia - As of 24 Nov 2020Document9 pagesTalk Shop Asia - As of 24 Nov 2020Jonathan AguilarNo ratings yet

- Q4 Fy21 GDPDocument7 pagesQ4 Fy21 GDPsksaha1976No ratings yet

- Nomura - India InsuranceDocument10 pagesNomura - India Insuranceudhaya kumarNo ratings yet

- Africa Day Presentation VDefDocument30 pagesAfrica Day Presentation VDefBernard BiboumNo ratings yet

- TDRIDocument26 pagesTDRIChatis HerabutNo ratings yet

- Section 1 General Economic and Financial OutlookDocument8 pagesSection 1 General Economic and Financial OutlookMicheal SamaanNo ratings yet

- Monthly Economic Review - Jun 2022Document30 pagesMonthly Economic Review - Jun 2022Dan FordNo ratings yet

- JPM Retail Trading Radar - Dec 8 2022Document26 pagesJPM Retail Trading Radar - Dec 8 2022LuanNo ratings yet

- Comprehensive Report On Indian Metal Cutting Machine Tool Industry - 2019Document73 pagesComprehensive Report On Indian Metal Cutting Machine Tool Industry - 2019Dr-Prashanth GowdaNo ratings yet

- The Macroeconomic and Social Impact of COVID-19 in Ethiopia and Suggested Directions For Policy ResponseDocument51 pagesThe Macroeconomic and Social Impact of COVID-19 in Ethiopia and Suggested Directions For Policy ResponseGetachew HussenNo ratings yet

- Monthly Economic Review - Jan 2021Document32 pagesMonthly Economic Review - Jan 2021Carl RossNo ratings yet

- Revision Notes On Economy of J&K by Vidhya Tutorials.Document7 pagesRevision Notes On Economy of J&K by Vidhya Tutorials.MuzaFar100% (1)

- ReQ Real Estate Quarterly HighlightsDocument8 pagesReQ Real Estate Quarterly HighlightsVaibhav RaghuvanshiNo ratings yet

- Technological Innovation for Agricultural Statistics: Special Supplement to Key Indicators for Asia and the Pacific 2018From EverandTechnological Innovation for Agricultural Statistics: Special Supplement to Key Indicators for Asia and the Pacific 2018No ratings yet

- Infostat: Data Collection PlatformDocument40 pagesInfostat: Data Collection PlatformAli KalemNo ratings yet

- VA21P033V01 Researcher IP2 IKAM PRS ViennaDocument4 pagesVA21P033V01 Researcher IP2 IKAM PRS ViennaAli KalemNo ratings yet

- VA21P133V01 - Job - Profile - Project - Manager (Irregular Migration and Return) - LP3 - WBTR - AnkaraDocument5 pagesVA21P133V01 - Job - Profile - Project - Manager (Irregular Migration and Return) - LP3 - WBTR - AnkaraAli KalemNo ratings yet

- ICMPD Job Profile Project Manager (IBM4TR) : Organisational SettingDocument4 pagesICMPD Job Profile Project Manager (IBM4TR) : Organisational SettingAli KalemNo ratings yet

- VA21P138V01 Job Profile Project Officer (IBM4TR) LP2 WBTR AnkaraDocument3 pagesVA21P138V01 Job Profile Project Officer (IBM4TR) LP2 WBTR AnkaraAli KalemNo ratings yet

- UnemploymentDocument7 pagesUnemploymentAli KalemNo ratings yet

- Donors TaxDocument4 pagesDonors TaxRo-Anne LozadaNo ratings yet

- Unit Iii Consumption FunctionDocument16 pagesUnit Iii Consumption FunctionMaster 003No ratings yet

- c4g The Impact of Covid 19 On African Smmes Operations OnlineDocument20 pagesc4g The Impact of Covid 19 On African Smmes Operations OnlineOlerato MothibediNo ratings yet

- P6-18 Unrealized Profit On Upstream SalesDocument4 pagesP6-18 Unrealized Profit On Upstream Salesw3n123No ratings yet

- Module 4 - Commodities Derivatives TradingDocument71 pagesModule 4 - Commodities Derivatives TradingLMT indiaNo ratings yet

- Il&fs FraudDocument10 pagesIl&fs FraudkrupaNo ratings yet

- Standard Ceramic Dividend PolicyDocument23 pagesStandard Ceramic Dividend PolicyEmon HossainNo ratings yet

- 7 - Exotic OptionsDocument39 pages7 - Exotic OptionsAman Kumar SharanNo ratings yet

- Cboec e 2021 02297Document3 pagesCboec e 2021 02297RatanaRoulNo ratings yet

- Analysis of The Courier Industry DTDCDocument31 pagesAnalysis of The Courier Industry DTDCMrinalini NagNo ratings yet

- Financial Economics Bocconi Lecture5Document20 pagesFinancial Economics Bocconi Lecture5Elisa CarnevaleNo ratings yet

- Make-Up & Beauty Salon: Guruji EnterprisesDocument1 pageMake-Up & Beauty Salon: Guruji EnterprisesAMITNo ratings yet

- Kế Hoạch Học PMPDocument4 pagesKế Hoạch Học PMPKhacNam NguyễnNo ratings yet

- AMEX - Glossary (ENG-SPA) - 1686735355Document8 pagesAMEX - Glossary (ENG-SPA) - 1686735355RAUL RAMIREZNo ratings yet

- Six Sigma: High Quality Can Lower Costs and Raise Customer SatisfactionDocument5 pagesSix Sigma: High Quality Can Lower Costs and Raise Customer SatisfactionsukhpreetbachhalNo ratings yet

- International Marketing Project ReportDocument85 pagesInternational Marketing Project ReportMohit AgarwalNo ratings yet

- Quiz Box 2 - QuestionnairesDocument13 pagesQuiz Box 2 - QuestionnairesCamila Mae AlduezaNo ratings yet

- Last Writing1Document2 pagesLast Writing11997elyasinNo ratings yet

- Mitrank Final Research ReportDocument71 pagesMitrank Final Research ReportMitrank ShuklaNo ratings yet

- Terms and Conditions: Atria Convergence Technologies Limited, Due Date: 15/11/2020Document2 pagesTerms and Conditions: Atria Convergence Technologies Limited, Due Date: 15/11/2020MaayaBimbamNo ratings yet

- Southern Innovator Magazine From 2011 To 2012: A Compilation of Documents From The Magazine's Early YearsDocument25 pagesSouthern Innovator Magazine From 2011 To 2012: A Compilation of Documents From The Magazine's Early YearsDavid SouthNo ratings yet

- Green HR Management (Chat GPT)Document2 pagesGreen HR Management (Chat GPT)esa arimbawaNo ratings yet

- Session1 Problem SetDocument1 pageSession1 Problem SetPattyNo ratings yet

- Kieni Dairy Brief Company Profile 2023Document2 pagesKieni Dairy Brief Company Profile 2023Solomon MainaNo ratings yet

- Connectivity Within Agricultural Supply ChainsDocument5 pagesConnectivity Within Agricultural Supply ChainsadelabdelaalNo ratings yet

- Tailoring UnitDocument8 pagesTailoring UnitSuresh sureshNo ratings yet

- BEST ICHIMOKU STRATEGY For QUICK PROFITS For BITFINEX - BTCUSD by Tradingstrategyguides - TradingViewDocument3 pagesBEST ICHIMOKU STRATEGY For QUICK PROFITS For BITFINEX - BTCUSD by Tradingstrategyguides - TradingViewhenrykayode40% (2)

- Bamboo Value Chain Story of Himalica Myanmar and Future Perspectives by DR Wah Wah HtunDocument17 pagesBamboo Value Chain Story of Himalica Myanmar and Future Perspectives by DR Wah Wah HtunAyeChan AungNo ratings yet

- International Journal of Research in Management & Social Science Volume 3, Issue 2 (II) April To June 2015 ISSN: 2322-0899Document111 pagesInternational Journal of Research in Management & Social Science Volume 3, Issue 2 (II) April To June 2015 ISSN: 2322-0899empyrealNo ratings yet

- Eurekahedge Asian Hedge Fund Awards 2010: WinnersDocument9 pagesEurekahedge Asian Hedge Fund Awards 2010: WinnersEurekahedgeNo ratings yet