Employment Benefit

Employment Benefit

You might also like

- 2303 Certificate of RegistrationDocument4 pages2303 Certificate of RegistrationLeo EstabilloNo ratings yet

- Conceptual Framework: & Accounting StandardsDocument61 pagesConceptual Framework: & Accounting StandardsAmie Jane Miranda100% (1)

- Establish and Maintain A Payroll SystemDocument16 pagesEstablish and Maintain A Payroll SystemMagarsaa Hirphaa100% (3)

- Chapter 4 - Accounting For Other Liabilities: A. Post Employment BenefitsDocument50 pagesChapter 4 - Accounting For Other Liabilities: A. Post Employment BenefitsLovely AbadianoNo ratings yet

- Post-Employment BenefitsDocument2 pagesPost-Employment BenefitsJustz LimNo ratings yet

- Employee Benefits P201Document18 pagesEmployee Benefits P201krisha milloNo ratings yet

- Employee Benefits: PAS 19, PAS 20, PAS 23, and PAS 24 Philippine Accounting Standards 19 (PAS 19)Document10 pagesEmployee Benefits: PAS 19, PAS 20, PAS 23, and PAS 24 Philippine Accounting Standards 19 (PAS 19)Mica DelaCruzNo ratings yet

- Accounting For Employee BenefitsDocument35 pagesAccounting For Employee BenefitsOnwuchekwa Chidi CalebNo ratings yet

- Discussion Problems: Manila Cavite Laguna Cebu Cagayan de Oro DavaoDocument5 pagesDiscussion Problems: Manila Cavite Laguna Cebu Cagayan de Oro DavaoTatianaNo ratings yet

- IAS-19 Employee BenefitsDocument49 pagesIAS-19 Employee BenefitsmalikjawadNo ratings yet

- Employee Benefits P201Document17 pagesEmployee Benefits P201krisha milloNo ratings yet

- IA2 10 01 Employee Benefits PDFDocument17 pagesIA2 10 01 Employee Benefits PDFAzaria MatiasNo ratings yet

- PAS 19 Employee BenefitsDocument62 pagesPAS 19 Employee BenefitsBenj FloresNo ratings yet

- IAS 19 NotesDocument16 pagesIAS 19 NotesArsalan AliNo ratings yet

- FAR.2932 - Employee Benefits.Document6 pagesFAR.2932 - Employee Benefits.Edmark LuspeNo ratings yet

- Pre Review 1 SEM S.Y. 2011-2012 Practical Accounting 1 / Theory of AccountsDocument11 pagesPre Review 1 SEM S.Y. 2011-2012 Practical Accounting 1 / Theory of AccountsKristine JarinaNo ratings yet

- Post Employment BenefitsDocument31 pagesPost Employment BenefitsSky SoronoiNo ratings yet

- Chapter 21 - Employee Benefits IFRS (IAS 19) and Then ASPE (Section 3462), Minor Difference Flashcards - QuizletDocument1 pageChapter 21 - Employee Benefits IFRS (IAS 19) and Then ASPE (Section 3462), Minor Difference Flashcards - QuizletcathNo ratings yet

- Pas 19Document5 pagesPas 19elle friasNo ratings yet

- MODULE Midterm FAR 3 EmpBenefitsDocument15 pagesMODULE Midterm FAR 3 EmpBenefitsJohn Mark FernandoNo ratings yet

- IAS19Document1 pageIAS19Chamil SureshNo ratings yet

- Postemployment BenefitsDocument3 pagesPostemployment BenefitsChristian John PardoNo ratings yet

- FAR.2832 Employee Benefits YT PDFDocument4 pagesFAR.2832 Employee Benefits YT PDFJames ScoldNo ratings yet

- Dependents or Insurance Companies.: Sharing, Paid Annual Leave, Paid Sick Leave, Non Monetary Benefits)Document3 pagesDependents or Insurance Companies.: Sharing, Paid Annual Leave, Paid Sick Leave, Non Monetary Benefits)Niranjan JainNo ratings yet

- MODULE Midterm FAR 3 EmpBenefitsDocument15 pagesMODULE Midterm FAR 3 EmpBenefitsKezNo ratings yet

- As 15Document12 pagesAs 15abhishekkapse654No ratings yet

- Lecture Outline: Part A: The Nature of Pension PlansDocument6 pagesLecture Outline: Part A: The Nature of Pension PlansDivine CuasayNo ratings yet

- IAS 19 NotesDocument15 pagesIAS 19 NotesArsalan AliNo ratings yet

- Or Defined Benefit Plans - Such May Be Contributory or NoncontributoryDocument7 pagesOr Defined Benefit Plans - Such May Be Contributory or NoncontributoryGirl Lang AkoNo ratings yet

- Q A Employees Benefits 2Document2 pagesQ A Employees Benefits 2Norlailah AmanollahNo ratings yet

- IAS 19 Employee Benefits StudentDocument40 pagesIAS 19 Employee Benefits StudentYI WEI CHANGNo ratings yet

- Objectives: Chapter 5 - Employee Benefits - Ias 19Document82 pagesObjectives: Chapter 5 - Employee Benefits - Ias 19Tram NguyenNo ratings yet

- 1 IAS 19 EMPLOYEE BENEFITS With Suggested Answers As of 11 10Document13 pages1 IAS 19 EMPLOYEE BENEFITS With Suggested Answers As of 11 10Kimberly IgnacioNo ratings yet

- Module 1 - Employee BenefitsDocument38 pagesModule 1 - Employee BenefitsMitchie Faustino100% (1)

- FAR SU11 Core Concepts PDFDocument3 pagesFAR SU11 Core Concepts PDFkoti kebeleNo ratings yet

- Chap. 20Document45 pagesChap. 20Nguyễn Lê ThủyNo ratings yet

- Employee BenefitsDocument9 pagesEmployee BenefitstinydmpNo ratings yet

- Employee BenefitsDocument18 pagesEmployee BenefitsLavillaNo ratings yet

- Employee Benefits: September 21, 2020Document18 pagesEmployee Benefits: September 21, 2020Andrea BaldonadoNo ratings yet

- Lecture - Post Employment Benefits - Defined Benefit PlanDocument5 pagesLecture - Post Employment Benefits - Defined Benefit PlanKatrina MarzanNo ratings yet

- Employee BenefitsDocument3 pagesEmployee BenefitsJAY AUBREY PINEDANo ratings yet

- QQ Employees Benefit 4Document2 pagesQQ Employees Benefit 4Norlailah AmanollahNo ratings yet

- Ind AS On Employee BenefitDocument81 pagesInd AS On Employee BenefitSanjay GohilNo ratings yet

- Employee Benefit PlanDocument8 pagesEmployee Benefit PlantinydmpNo ratings yet

- Pas 19 Employee BenefitsDocument14 pagesPas 19 Employee BenefitsKelzarineah FludgeNo ratings yet

- IAS 19 Employee Benefits (2021)Document6 pagesIAS 19 Employee Benefits (2021)Tawanda Tatenda Herbert100% (1)

- 02 Ias19Document8 pages02 Ias19AANo ratings yet

- Employee Benefits: PAS 19 Corpuz, Mary Lorie Anne ODocument38 pagesEmployee Benefits: PAS 19 Corpuz, Mary Lorie Anne OMarylorieanne CorpuzNo ratings yet

- Accounting For Employee BenefitsDocument29 pagesAccounting For Employee BenefitsnuggsNo ratings yet

- SBR - Chapter 5Document6 pagesSBR - Chapter 5Jason KumarNo ratings yet

- Lecture # 11: Employee Benefits IAS-19Document3 pagesLecture # 11: Employee Benefits IAS-19ali hassnainNo ratings yet

- Accounting V Tax TreatmentDocument3 pagesAccounting V Tax TreatmentReena MaNo ratings yet

- IAS 19 - Employee Benefits v2Document53 pagesIAS 19 - Employee Benefits v2Emil John SughuNo ratings yet

- Module 3 Packet: College of CommerceDocument21 pagesModule 3 Packet: College of CommerceDexie Jane MayoNo ratings yet

- Unit 7 E-Tutor PresentationDocument18 pagesUnit 7 E-Tutor PresentationKatrina EustaceNo ratings yet

- Cfas Pas 19Document4 pagesCfas Pas 19Zyribelle Anne JAPSONNo ratings yet

- CFAS NotesDocument27 pagesCFAS NotesMikasa AckermanNo ratings yet

- Cfas Finals ReviewerDocument5 pagesCfas Finals ReviewerKim Nicole BantolaNo ratings yet

- IAS 19 - Employee Benefits Supplementary NotesDocument19 pagesIAS 19 - Employee Benefits Supplementary NotesPASTORYNo ratings yet

- Unit 03Document9 pagesUnit 03bobo tangaNo ratings yet

- Cost Volume Profit AnalysisDocument6 pagesCost Volume Profit AnalysisSrabon BaruaNo ratings yet

- Financial Accounting For Manager End SemDocument13 pagesFinancial Accounting For Manager End SemSrabon BaruaNo ratings yet

- Fin Accounting Preparation For MidtermDocument89 pagesFin Accounting Preparation For MidtermSrabon BaruaNo ratings yet

- Economic EB EndtermDocument24 pagesEconomic EB EndtermSrabon BaruaNo ratings yet

- Ratio Analysis 1Document2 pagesRatio Analysis 1Srabon BaruaNo ratings yet

- Final Sem Theory AnswerDocument11 pagesFinal Sem Theory AnswerSrabon BaruaNo ratings yet

- Study Mart Statistics Course OutlineDocument2 pagesStudy Mart Statistics Course OutlineSrabon BaruaNo ratings yet

- Cost and Management Accounting Midsem PrepDocument25 pagesCost and Management Accounting Midsem PrepSrabon BaruaNo ratings yet

- Operating SegmentDocument15 pagesOperating SegmentSrabon BaruaNo ratings yet

- Cost and Management Accounting AssignmentDocument3 pagesCost and Management Accounting AssignmentSrabon BaruaNo ratings yet

- Economic Environment of BusinessDocument6 pagesEconomic Environment of BusinessSrabon BaruaNo ratings yet

- Cost DJB - ICAI Mat Additional QuestionsDocument29 pagesCost DJB - ICAI Mat Additional QuestionsSrabon BaruaNo ratings yet

- Accounting For InventoriesDocument40 pagesAccounting For InventoriesSrabon BaruaNo ratings yet

- IAS 12 - Income Tax: Prepared By: Sir Hamza Abdul HaqDocument33 pagesIAS 12 - Income Tax: Prepared By: Sir Hamza Abdul HaqSrabon BaruaNo ratings yet

- Basic ConsolidationDocument33 pagesBasic ConsolidationSrabon BaruaNo ratings yet

- Value Added Tax VAT - in View of Bangladesh PDFDocument11 pagesValue Added Tax VAT - in View of Bangladesh PDFSrabon BaruaNo ratings yet

- Audit PDFDocument31 pagesAudit PDFSrabon BaruaNo ratings yet

- Impairment of AssetDocument27 pagesImpairment of AssetSrabon BaruaNo ratings yet

- Presentation of Financial StatementDocument14 pagesPresentation of Financial StatementSrabon BaruaNo ratings yet

- Analysis & Interpretation: Prepared By: Sir Hamza Abdul HaqDocument10 pagesAnalysis & Interpretation: Prepared By: Sir Hamza Abdul HaqSrabon BaruaNo ratings yet

- Provision, Ca and CLDocument17 pagesProvision, Ca and CLSrabon BaruaNo ratings yet

- Framework: Prepared By: Sir Hamza Abdul HaqDocument11 pagesFramework: Prepared By: Sir Hamza Abdul HaqSrabon BaruaNo ratings yet

- Guaranteed Income PDS PDFDocument48 pagesGuaranteed Income PDS PDFIlyah JaucianNo ratings yet

- Accounting For Government and Not-For-Profit Organizations: ACCO 30033Document24 pagesAccounting For Government and Not-For-Profit Organizations: ACCO 30033hehehedontmind me100% (1)

- Document p3b United Arab Emirates (New) enDocument25 pagesDocument p3b United Arab Emirates (New) enmelsyNo ratings yet

- Payslip For The Month of June, 2023: Toyota Kirloskar Motor PVT LTDDocument2 pagesPayslip For The Month of June, 2023: Toyota Kirloskar Motor PVT LTDevilghostevilghost666No ratings yet

- TRADITIONAL LIFE REVIEWER - Intermediary ExamDocument27 pagesTRADITIONAL LIFE REVIEWER - Intermediary ExamJohn Michael FernandezNo ratings yet

- form-w2-Ramona-Crawford 2Document9 pagesform-w2-Ramona-Crawford 2Nicole CarutherNo ratings yet

- Second Copy Company Income Tax Return Report - Mohid2017 - Copy 1Document6 pagesSecond Copy Company Income Tax Return Report - Mohid2017 - Copy 1fatima khurramNo ratings yet

- Chapter 10 Compensation ManagementDocument23 pagesChapter 10 Compensation ManagementvarunNo ratings yet

- BrioHR Payroll Guide Malaysia 2020Document29 pagesBrioHR Payroll Guide Malaysia 2020Chiaw MeiNo ratings yet

- Chapter - 18 PFPDocument4 pagesChapter - 18 PFPaliNo ratings yet

- 15 043 IBFD International Tax Glossary 7th Edition Final WebDocument20 pages15 043 IBFD International Tax Glossary 7th Edition Final WebDaisy AnitaNo ratings yet

- Anil Khanna Appt - LetterDocument5 pagesAnil Khanna Appt - Lettertestengine701921No ratings yet

- DeductionsDocument31 pagesDeductionsJane Tuazon50% (2)

- Identify and Discuss Direct TaxDocument7 pagesIdentify and Discuss Direct Taxsamuel asefaNo ratings yet

- Income Tax Law and Accounts: Ruchi Mehta Assistant Professor Department of Commerce St. Mary's College ThrissurDocument13 pagesIncome Tax Law and Accounts: Ruchi Mehta Assistant Professor Department of Commerce St. Mary's College ThrissurAnju ShajuNo ratings yet

- Investment Environment & Securities MarketDocument28 pagesInvestment Environment & Securities MarketProf. Suyog ChachadNo ratings yet

- Republic of The Philippines Bulacan State University City of Malolos, Bulacan Office of The Dean of InstructionDocument8 pagesRepublic of The Philippines Bulacan State University City of Malolos, Bulacan Office of The Dean of InstructionTheresa RoqueNo ratings yet

- D2fin ExamDocument17 pagesD2fin Examjeffleeter100% (1)

- Assignment 2Document4 pagesAssignment 2Ahmed AhmedNo ratings yet

- Accounting For The Payroll System in An Ethiopian ContextDocument11 pagesAccounting For The Payroll System in An Ethiopian Contextalemayehu100% (1)

- Financial Statements of Insurance CompaniesDocument30 pagesFinancial Statements of Insurance CompaniesHarikrishnaNo ratings yet

- UNIT 2 Income From SalaryDocument146 pagesUNIT 2 Income From Salaryeasy mailNo ratings yet

- A Study On Perception of Investors Investing in Life InsuranceDocument57 pagesA Study On Perception of Investors Investing in Life InsuranceDigvijay ParmarNo ratings yet

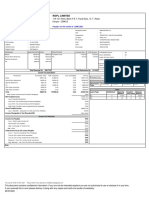

- RSPL Limited: Payslip For The Month of JUNE 2021Document1 pageRSPL Limited: Payslip For The Month of JUNE 2021Manju ManjappaNo ratings yet

- Detailed Study of General Insurance in IndiaDocument49 pagesDetailed Study of General Insurance in IndiaSimone RodriguesNo ratings yet

- Income Tax and GSTDocument207 pagesIncome Tax and GSTTERZO IncNo ratings yet

- Annual Report 1982-83Document139 pagesAnnual Report 1982-83dr.estab.iiftNo ratings yet

- PF & Esi 16.10.21Document13 pagesPF & Esi 16.10.21JatinNo ratings yet

Download as pdf or txt

You might also like

- 2303 Certificate of RegistrationDocument4 pages2303 Certificate of RegistrationLeo EstabilloNo ratings yet

- Conceptual Framework: & Accounting StandardsDocument61 pagesConceptual Framework: & Accounting StandardsAmie Jane Miranda100% (1)

- Establish and Maintain A Payroll SystemDocument16 pagesEstablish and Maintain A Payroll SystemMagarsaa Hirphaa100% (3)

- Chapter 4 - Accounting For Other Liabilities: A. Post Employment BenefitsDocument50 pagesChapter 4 - Accounting For Other Liabilities: A. Post Employment BenefitsLovely AbadianoNo ratings yet

- Post-Employment BenefitsDocument2 pagesPost-Employment BenefitsJustz LimNo ratings yet

- Employee Benefits P201Document18 pagesEmployee Benefits P201krisha milloNo ratings yet

- Employee Benefits: PAS 19, PAS 20, PAS 23, and PAS 24 Philippine Accounting Standards 19 (PAS 19)Document10 pagesEmployee Benefits: PAS 19, PAS 20, PAS 23, and PAS 24 Philippine Accounting Standards 19 (PAS 19)Mica DelaCruzNo ratings yet

- Accounting For Employee BenefitsDocument35 pagesAccounting For Employee BenefitsOnwuchekwa Chidi CalebNo ratings yet

- Discussion Problems: Manila Cavite Laguna Cebu Cagayan de Oro DavaoDocument5 pagesDiscussion Problems: Manila Cavite Laguna Cebu Cagayan de Oro DavaoTatianaNo ratings yet

- IAS-19 Employee BenefitsDocument49 pagesIAS-19 Employee BenefitsmalikjawadNo ratings yet

- Employee Benefits P201Document17 pagesEmployee Benefits P201krisha milloNo ratings yet

- IA2 10 01 Employee Benefits PDFDocument17 pagesIA2 10 01 Employee Benefits PDFAzaria MatiasNo ratings yet

- PAS 19 Employee BenefitsDocument62 pagesPAS 19 Employee BenefitsBenj FloresNo ratings yet

- IAS 19 NotesDocument16 pagesIAS 19 NotesArsalan AliNo ratings yet

- FAR.2932 - Employee Benefits.Document6 pagesFAR.2932 - Employee Benefits.Edmark LuspeNo ratings yet

- Pre Review 1 SEM S.Y. 2011-2012 Practical Accounting 1 / Theory of AccountsDocument11 pagesPre Review 1 SEM S.Y. 2011-2012 Practical Accounting 1 / Theory of AccountsKristine JarinaNo ratings yet

- Post Employment BenefitsDocument31 pagesPost Employment BenefitsSky SoronoiNo ratings yet

- Chapter 21 - Employee Benefits IFRS (IAS 19) and Then ASPE (Section 3462), Minor Difference Flashcards - QuizletDocument1 pageChapter 21 - Employee Benefits IFRS (IAS 19) and Then ASPE (Section 3462), Minor Difference Flashcards - QuizletcathNo ratings yet

- Pas 19Document5 pagesPas 19elle friasNo ratings yet

- MODULE Midterm FAR 3 EmpBenefitsDocument15 pagesMODULE Midterm FAR 3 EmpBenefitsJohn Mark FernandoNo ratings yet

- IAS19Document1 pageIAS19Chamil SureshNo ratings yet

- Postemployment BenefitsDocument3 pagesPostemployment BenefitsChristian John PardoNo ratings yet

- FAR.2832 Employee Benefits YT PDFDocument4 pagesFAR.2832 Employee Benefits YT PDFJames ScoldNo ratings yet

- Dependents or Insurance Companies.: Sharing, Paid Annual Leave, Paid Sick Leave, Non Monetary Benefits)Document3 pagesDependents or Insurance Companies.: Sharing, Paid Annual Leave, Paid Sick Leave, Non Monetary Benefits)Niranjan JainNo ratings yet

- MODULE Midterm FAR 3 EmpBenefitsDocument15 pagesMODULE Midterm FAR 3 EmpBenefitsKezNo ratings yet

- As 15Document12 pagesAs 15abhishekkapse654No ratings yet

- Lecture Outline: Part A: The Nature of Pension PlansDocument6 pagesLecture Outline: Part A: The Nature of Pension PlansDivine CuasayNo ratings yet

- IAS 19 NotesDocument15 pagesIAS 19 NotesArsalan AliNo ratings yet

- Or Defined Benefit Plans - Such May Be Contributory or NoncontributoryDocument7 pagesOr Defined Benefit Plans - Such May Be Contributory or NoncontributoryGirl Lang AkoNo ratings yet

- Q A Employees Benefits 2Document2 pagesQ A Employees Benefits 2Norlailah AmanollahNo ratings yet

- IAS 19 Employee Benefits StudentDocument40 pagesIAS 19 Employee Benefits StudentYI WEI CHANGNo ratings yet

- Objectives: Chapter 5 - Employee Benefits - Ias 19Document82 pagesObjectives: Chapter 5 - Employee Benefits - Ias 19Tram NguyenNo ratings yet

- 1 IAS 19 EMPLOYEE BENEFITS With Suggested Answers As of 11 10Document13 pages1 IAS 19 EMPLOYEE BENEFITS With Suggested Answers As of 11 10Kimberly IgnacioNo ratings yet

- Module 1 - Employee BenefitsDocument38 pagesModule 1 - Employee BenefitsMitchie Faustino100% (1)

- FAR SU11 Core Concepts PDFDocument3 pagesFAR SU11 Core Concepts PDFkoti kebeleNo ratings yet

- Chap. 20Document45 pagesChap. 20Nguyễn Lê ThủyNo ratings yet

- Employee BenefitsDocument9 pagesEmployee BenefitstinydmpNo ratings yet

- Employee BenefitsDocument18 pagesEmployee BenefitsLavillaNo ratings yet

- Employee Benefits: September 21, 2020Document18 pagesEmployee Benefits: September 21, 2020Andrea BaldonadoNo ratings yet

- Lecture - Post Employment Benefits - Defined Benefit PlanDocument5 pagesLecture - Post Employment Benefits - Defined Benefit PlanKatrina MarzanNo ratings yet

- Employee BenefitsDocument3 pagesEmployee BenefitsJAY AUBREY PINEDANo ratings yet

- QQ Employees Benefit 4Document2 pagesQQ Employees Benefit 4Norlailah AmanollahNo ratings yet

- Ind AS On Employee BenefitDocument81 pagesInd AS On Employee BenefitSanjay GohilNo ratings yet

- Employee Benefit PlanDocument8 pagesEmployee Benefit PlantinydmpNo ratings yet

- Pas 19 Employee BenefitsDocument14 pagesPas 19 Employee BenefitsKelzarineah FludgeNo ratings yet

- IAS 19 Employee Benefits (2021)Document6 pagesIAS 19 Employee Benefits (2021)Tawanda Tatenda Herbert100% (1)

- 02 Ias19Document8 pages02 Ias19AANo ratings yet

- Employee Benefits: PAS 19 Corpuz, Mary Lorie Anne ODocument38 pagesEmployee Benefits: PAS 19 Corpuz, Mary Lorie Anne OMarylorieanne CorpuzNo ratings yet

- Accounting For Employee BenefitsDocument29 pagesAccounting For Employee BenefitsnuggsNo ratings yet

- SBR - Chapter 5Document6 pagesSBR - Chapter 5Jason KumarNo ratings yet

- Lecture # 11: Employee Benefits IAS-19Document3 pagesLecture # 11: Employee Benefits IAS-19ali hassnainNo ratings yet

- Accounting V Tax TreatmentDocument3 pagesAccounting V Tax TreatmentReena MaNo ratings yet

- IAS 19 - Employee Benefits v2Document53 pagesIAS 19 - Employee Benefits v2Emil John SughuNo ratings yet

- Module 3 Packet: College of CommerceDocument21 pagesModule 3 Packet: College of CommerceDexie Jane MayoNo ratings yet

- Unit 7 E-Tutor PresentationDocument18 pagesUnit 7 E-Tutor PresentationKatrina EustaceNo ratings yet

- Cfas Pas 19Document4 pagesCfas Pas 19Zyribelle Anne JAPSONNo ratings yet

- CFAS NotesDocument27 pagesCFAS NotesMikasa AckermanNo ratings yet

- Cfas Finals ReviewerDocument5 pagesCfas Finals ReviewerKim Nicole BantolaNo ratings yet

- IAS 19 - Employee Benefits Supplementary NotesDocument19 pagesIAS 19 - Employee Benefits Supplementary NotesPASTORYNo ratings yet

- Unit 03Document9 pagesUnit 03bobo tangaNo ratings yet

- Cost Volume Profit AnalysisDocument6 pagesCost Volume Profit AnalysisSrabon BaruaNo ratings yet

- Financial Accounting For Manager End SemDocument13 pagesFinancial Accounting For Manager End SemSrabon BaruaNo ratings yet

- Fin Accounting Preparation For MidtermDocument89 pagesFin Accounting Preparation For MidtermSrabon BaruaNo ratings yet

- Economic EB EndtermDocument24 pagesEconomic EB EndtermSrabon BaruaNo ratings yet

- Ratio Analysis 1Document2 pagesRatio Analysis 1Srabon BaruaNo ratings yet

- Final Sem Theory AnswerDocument11 pagesFinal Sem Theory AnswerSrabon BaruaNo ratings yet

- Study Mart Statistics Course OutlineDocument2 pagesStudy Mart Statistics Course OutlineSrabon BaruaNo ratings yet

- Cost and Management Accounting Midsem PrepDocument25 pagesCost and Management Accounting Midsem PrepSrabon BaruaNo ratings yet

- Operating SegmentDocument15 pagesOperating SegmentSrabon BaruaNo ratings yet

- Cost and Management Accounting AssignmentDocument3 pagesCost and Management Accounting AssignmentSrabon BaruaNo ratings yet

- Economic Environment of BusinessDocument6 pagesEconomic Environment of BusinessSrabon BaruaNo ratings yet

- Cost DJB - ICAI Mat Additional QuestionsDocument29 pagesCost DJB - ICAI Mat Additional QuestionsSrabon BaruaNo ratings yet

- Accounting For InventoriesDocument40 pagesAccounting For InventoriesSrabon BaruaNo ratings yet

- IAS 12 - Income Tax: Prepared By: Sir Hamza Abdul HaqDocument33 pagesIAS 12 - Income Tax: Prepared By: Sir Hamza Abdul HaqSrabon BaruaNo ratings yet

- Basic ConsolidationDocument33 pagesBasic ConsolidationSrabon BaruaNo ratings yet

- Value Added Tax VAT - in View of Bangladesh PDFDocument11 pagesValue Added Tax VAT - in View of Bangladesh PDFSrabon BaruaNo ratings yet

- Audit PDFDocument31 pagesAudit PDFSrabon BaruaNo ratings yet

- Impairment of AssetDocument27 pagesImpairment of AssetSrabon BaruaNo ratings yet

- Presentation of Financial StatementDocument14 pagesPresentation of Financial StatementSrabon BaruaNo ratings yet

- Analysis & Interpretation: Prepared By: Sir Hamza Abdul HaqDocument10 pagesAnalysis & Interpretation: Prepared By: Sir Hamza Abdul HaqSrabon BaruaNo ratings yet

- Provision, Ca and CLDocument17 pagesProvision, Ca and CLSrabon BaruaNo ratings yet

- Framework: Prepared By: Sir Hamza Abdul HaqDocument11 pagesFramework: Prepared By: Sir Hamza Abdul HaqSrabon BaruaNo ratings yet

- Guaranteed Income PDS PDFDocument48 pagesGuaranteed Income PDS PDFIlyah JaucianNo ratings yet

- Accounting For Government and Not-For-Profit Organizations: ACCO 30033Document24 pagesAccounting For Government and Not-For-Profit Organizations: ACCO 30033hehehedontmind me100% (1)

- Document p3b United Arab Emirates (New) enDocument25 pagesDocument p3b United Arab Emirates (New) enmelsyNo ratings yet

- Payslip For The Month of June, 2023: Toyota Kirloskar Motor PVT LTDDocument2 pagesPayslip For The Month of June, 2023: Toyota Kirloskar Motor PVT LTDevilghostevilghost666No ratings yet

- TRADITIONAL LIFE REVIEWER - Intermediary ExamDocument27 pagesTRADITIONAL LIFE REVIEWER - Intermediary ExamJohn Michael FernandezNo ratings yet

- form-w2-Ramona-Crawford 2Document9 pagesform-w2-Ramona-Crawford 2Nicole CarutherNo ratings yet

- Second Copy Company Income Tax Return Report - Mohid2017 - Copy 1Document6 pagesSecond Copy Company Income Tax Return Report - Mohid2017 - Copy 1fatima khurramNo ratings yet

- Chapter 10 Compensation ManagementDocument23 pagesChapter 10 Compensation ManagementvarunNo ratings yet

- BrioHR Payroll Guide Malaysia 2020Document29 pagesBrioHR Payroll Guide Malaysia 2020Chiaw MeiNo ratings yet

- Chapter - 18 PFPDocument4 pagesChapter - 18 PFPaliNo ratings yet

- 15 043 IBFD International Tax Glossary 7th Edition Final WebDocument20 pages15 043 IBFD International Tax Glossary 7th Edition Final WebDaisy AnitaNo ratings yet

- Anil Khanna Appt - LetterDocument5 pagesAnil Khanna Appt - Lettertestengine701921No ratings yet

- DeductionsDocument31 pagesDeductionsJane Tuazon50% (2)

- Identify and Discuss Direct TaxDocument7 pagesIdentify and Discuss Direct Taxsamuel asefaNo ratings yet

- Income Tax Law and Accounts: Ruchi Mehta Assistant Professor Department of Commerce St. Mary's College ThrissurDocument13 pagesIncome Tax Law and Accounts: Ruchi Mehta Assistant Professor Department of Commerce St. Mary's College ThrissurAnju ShajuNo ratings yet

- Investment Environment & Securities MarketDocument28 pagesInvestment Environment & Securities MarketProf. Suyog ChachadNo ratings yet

- Republic of The Philippines Bulacan State University City of Malolos, Bulacan Office of The Dean of InstructionDocument8 pagesRepublic of The Philippines Bulacan State University City of Malolos, Bulacan Office of The Dean of InstructionTheresa RoqueNo ratings yet

- D2fin ExamDocument17 pagesD2fin Examjeffleeter100% (1)

- Assignment 2Document4 pagesAssignment 2Ahmed AhmedNo ratings yet

- Accounting For The Payroll System in An Ethiopian ContextDocument11 pagesAccounting For The Payroll System in An Ethiopian Contextalemayehu100% (1)

- Financial Statements of Insurance CompaniesDocument30 pagesFinancial Statements of Insurance CompaniesHarikrishnaNo ratings yet

- UNIT 2 Income From SalaryDocument146 pagesUNIT 2 Income From Salaryeasy mailNo ratings yet

- A Study On Perception of Investors Investing in Life InsuranceDocument57 pagesA Study On Perception of Investors Investing in Life InsuranceDigvijay ParmarNo ratings yet

- RSPL Limited: Payslip For The Month of JUNE 2021Document1 pageRSPL Limited: Payslip For The Month of JUNE 2021Manju ManjappaNo ratings yet

- Detailed Study of General Insurance in IndiaDocument49 pagesDetailed Study of General Insurance in IndiaSimone RodriguesNo ratings yet

- Income Tax and GSTDocument207 pagesIncome Tax and GSTTERZO IncNo ratings yet

- Annual Report 1982-83Document139 pagesAnnual Report 1982-83dr.estab.iiftNo ratings yet

- PF & Esi 16.10.21Document13 pagesPF & Esi 16.10.21JatinNo ratings yet