Download as pdf or txt

You might also like

- Case Write Up 1Document4 pagesCase Write Up 1E learningNo ratings yet

- Crash of The Titans by Greg Farrell - ExcerptDocument41 pagesCrash of The Titans by Greg Farrell - ExcerptCrown Publishing Group37% (19)

- SheDocument12 pagesSheMark Anthony Tibule80% (5)

- Journal Entry GSTDocument8 pagesJournal Entry GSTSimardeep SalujaNo ratings yet

- CRC Ace Mas First PBDocument10 pagesCRC Ace Mas First PBJohn Philip Castro100% (2)

- Beda MemAid PPSADocument5 pagesBeda MemAid PPSAJeremiah Ruaro100% (3)

- Adobe Scan 04 Sep 2023Document13 pagesAdobe Scan 04 Sep 2023Devendra ChaudhariNo ratings yet

- Unit 1 O XTR Pra Tice: - TourDocument2 pagesUnit 1 O XTR Pra Tice: - Tourdane gaoNo ratings yet

- Computer TallyDocument15 pagesComputer Tallysadaf khanNo ratings yet

- Book 8 Feb 2024Document5 pagesBook 8 Feb 2024hemachandra.karlapudi2021No ratings yet

- Pension DocumentDocument2 pagesPension DocumentSusovan SirNo ratings yet

- Lec 7Document33 pagesLec 7Ali RajaNo ratings yet

- Mech Exp - No.5,6Document10 pagesMech Exp - No.5,6vanixbot750No ratings yet

- Federalism Notes Feb 8, 2023Document13 pagesFederalism Notes Feb 8, 2023Shubhada ChanfaneNo ratings yet

- Adobe Scan 06 Apr 2021Document3 pagesAdobe Scan 06 Apr 2021ZAHRA ARINTA BASUKINo ratings yet

- O Dduw Rhanath Fendithion (John RUTTER)Document5 pagesO Dduw Rhanath Fendithion (John RUTTER)Yamila GaunaNo ratings yet

- Awpo FeedbackDocument4 pagesAwpo Feedback28xytpfsb5No ratings yet

- NC44 45 GauravDocument2 pagesNC44 45 GauravRavichandran DNo ratings yet

- Adobe Scan 6 Feb 2024Document2 pagesAdobe Scan 6 Feb 2024kohinoorcheema06No ratings yet

- Polarimeter Phy PracDocument6 pagesPolarimeter Phy Pracsingh19.09shristiNo ratings yet

- Adobe Scan 16 Jul 2022Document23 pagesAdobe Scan 16 Jul 2022Vanakkam Tamil Valga TamilNo ratings yet

- Adobe Scan 13 Fév. 2023 PDFDocument1 pageAdobe Scan 13 Fév. 2023 PDFMostafa AmimiNo ratings yet

- Unit No 3 Plane Table SurveyingDocument12 pagesUnit No 3 Plane Table SurveyinggomatesgNo ratings yet

- Gener : AcrsDocument2 pagesGener : AcrsEldhoThomasNo ratings yet

- Adobe Scan Mar 25, 2021Document1 pageAdobe Scan Mar 25, 2021Wilson BrueNo ratings yet

- PlantDocument5 pagesPlantKinjalNo ratings yet

- Solid State Viva QuestionsDocument7 pagesSolid State Viva QuestionsAnanya SNo ratings yet

- Learning Activity 21Document12 pagesLearning Activity 21tiana.jonesy99No ratings yet

- PhysicsDocument25 pagesPhysicsNilaksh Jha 9DNo ratings yet

- Shrinking CoreDocument4 pagesShrinking Core22mt0153No ratings yet

- M CuttingDocument6 pagesM Cuttingksonu99555No ratings yet

- Circular July 2011 - BOT TollDocument1 pageCircular July 2011 - BOT TollPANKIT PATELNo ratings yet

- Basic Problems of An EconomyDocument5 pagesBasic Problems of An Economy01 shashant AlamchandaniNo ratings yet

- B . T. (.FRP: For Instructions, See Back Form Dr-SfaDocument1 pageB . T. (.FRP: For Instructions, See Back Form Dr-SfaZach EdwardsNo ratings yet

- Capital and Revenue ExpenditureDocument1 pageCapital and Revenue ExpenditureJohn Sue HanNo ratings yet

- For Prioduct Put On QA HoldDocument1 pageFor Prioduct Put On QA Holdgbernall30No ratings yet

- Gpo 36 Tests and Inspections Routine P 5039Document1 pageGpo 36 Tests and Inspections Routine P 5039Theodor EikeNo ratings yet

- Seconds Pointing L Descri-Dec Y. Date A: 10 L Direction Pi Main Out.Document6 pagesSeconds Pointing L Descri-Dec Y. Date A: 10 L Direction Pi Main Out.Nur AgustinusNo ratings yet

- Key - Quiz 2 Asignment Session 2Document6 pagesKey - Quiz 2 Asignment Session 2khizar abbasNo ratings yet

- Abhi JournalDocument16 pagesAbhi JournalAnkit Jerome FargoseNo ratings yet

- PR19940066 CasingandCementingReportDocument23 pagesPR19940066 CasingandCementingReportsd186551No ratings yet

- Inglés CI - Sectors of The EconomyDocument7 pagesInglés CI - Sectors of The EconomyMajetnoNo ratings yet

- Economics Unit 3Document17 pagesEconomics Unit 3mgmtNo ratings yet

- QC Lab ProgramDocument2 pagesQC Lab ProgramsanjayNo ratings yet

- C/y/ (VI: AGM S Not HeDocument1 pageC/y/ (VI: AGM S Not HeCOLLA NOTENo ratings yet

- bài tập cb83 4 MDQH PDFDocument4 pagesbài tập cb83 4 MDQH PDFTuệ Mãng NguyễnNo ratings yet

- Norek Bendahara SalutDocument1 pageNorek Bendahara SalutNur HusniansyahNo ratings yet

- Thermal 8Document1 pageThermal 8Clash GodNo ratings yet

- Tests 1Document6 pagesTests 1Dolly NarisNo ratings yet

- Ma旧Ao Harbor Administration Corp: Technical Documentat!On Front SheetDocument14 pagesMa旧Ao Harbor Administration Corp: Technical Documentat!On Front SheetmanthoexNo ratings yet

- Biochem Oct 30 2021Document11 pagesBiochem Oct 30 2021Denise CedeñoNo ratings yet

- M-3 Specification For Installation of Piping System in Engine RoomDocument9 pagesM-3 Specification For Installation of Piping System in Engine RoomHuy HùynhNo ratings yet

- Activite 4 GestionDocument5 pagesActivite 4 GestionMohamed TaouilNo ratings yet

- 03 - Ahmad Din Fahrizzy Latuconsina - Mindmap2Document1 page03 - Ahmad Din Fahrizzy Latuconsina - Mindmap2Ahmad Din Fahrizzy LatuconsinaNo ratings yet

- Agricultural Engineering Soil MechanicsDocument298 pagesAgricultural Engineering Soil Mechanicsseunghee choiNo ratings yet

- Adobe Scan 20 Сент. 2020 г.Document13 pagesAdobe Scan 20 Сент. 2020 г.Petr IschenkoNo ratings yet

- Csec Math p1 1993 To 2023Document388 pagesCsec Math p1 1993 To 2023lillyannsam88No ratings yet

- Organic Chemistry NotesDocument4 pagesOrganic Chemistry NotesAbhinav KumarNo ratings yet

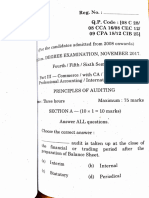

- Principles of Auditing 2017Document4 pagesPrinciples of Auditing 2017rajeshwarsagaNo ratings yet

- ML Unit 2Document18 pagesML Unit 2gowrishankar nayanaNo ratings yet

- Adobe Scan Jan 30, 2021Document25 pagesAdobe Scan Jan 30, 2021Spina ShilNo ratings yet

- D.E. 555 Is D.E. 101 5.10.2017 - Order Settin Trial, 5.10.17Document6 pagesD.E. 555 Is D.E. 101 5.10.2017 - Order Settin Trial, 5.10.17larry-612445No ratings yet

- Repo RateDocument5 pagesRepo RateSweta SinghNo ratings yet

- MCQS On Financial Management p2Document3 pagesMCQS On Financial Management p2Sweta SinghNo ratings yet

- Lime 13 Case Submission of Sunsilk BrandDocument1 pageLime 13 Case Submission of Sunsilk BrandSweta SinghNo ratings yet

- Indian Commodity MarketDocument9 pagesIndian Commodity MarketSweta SinghNo ratings yet

- Certificate of DepositsDocument8 pagesCertificate of DepositsSweta SinghNo ratings yet

- Impact of Covid-19Document11 pagesImpact of Covid-19Sweta SinghNo ratings yet

- HUL LIME 13 Case Submission FormatDocument1 pageHUL LIME 13 Case Submission FormatSweta SinghNo ratings yet

- HUL Post Mid TermDocument13 pagesHUL Post Mid TermSweta SinghNo ratings yet

- BRM Project Chart AnalysisDocument8 pagesBRM Project Chart AnalysisSweta SinghNo ratings yet

- Partnership: AdmissionDocument7 pagesPartnership: AdmissionSweta SinghNo ratings yet

- Meaning of Stock ExchangeDocument4 pagesMeaning of Stock ExchangeShruti BhatiaNo ratings yet

- Chapter 8Document3 pagesChapter 8kish MishNo ratings yet

- Cycles - Research - Institute - GANN - Docx Filename UTF-8''Cycles Research Institute GANNDocument3 pagesCycles - Research - Institute - GANN - Docx Filename UTF-8''Cycles Research Institute GANNrajeshrraikarNo ratings yet

- Identification and Evaluation of Factors of Dividend PolicyDocument17 pagesIdentification and Evaluation of Factors of Dividend PolicyFarhana DibagelenNo ratings yet

- Dividend Policy and Retained Earnings: Foundations of Financial ManagementDocument38 pagesDividend Policy and Retained Earnings: Foundations of Financial ManagementBlack UnicornNo ratings yet

- HO4Document2 pagesHO4Emily Dela CruzNo ratings yet

- Wealth Educator Magazine 01Document92 pagesWealth Educator Magazine 01Rafael AlemanNo ratings yet

- The Mechanics of Day Trading Are Crucial To BeginnersDocument3 pagesThe Mechanics of Day Trading Are Crucial To BeginnershariramNo ratings yet

- Bonner Family Wealth BlueprintDocument7 pagesBonner Family Wealth Blueprintmary welch100% (3)

- List of 30 Highest Dividend Paying Stocks in IndiaDocument5 pagesList of 30 Highest Dividend Paying Stocks in IndiaPankajNo ratings yet

- Equity List 01 Feb 2022Document35 pagesEquity List 01 Feb 2022Akhil HussainNo ratings yet

- Distribution To ShareholdersDocument47 pagesDistribution To Shareholderszyra liam stylesNo ratings yet

- Section 5 Reflection EssayDocument2 pagesSection 5 Reflection Essayapi-302636671100% (1)

- FAR-06 Earnings Per ShareDocument4 pagesFAR-06 Earnings Per ShareKim Cristian Maaño50% (2)

- Chapter 6Document56 pagesChapter 6Ilyes LouatiNo ratings yet

- DIS Investment ReportDocument1 pageDIS Investment ReportHyperNo ratings yet

- Profit From The PanicDocument202 pagesProfit From The PanicLau Wai KentNo ratings yet

- Literature Review On Equity InvestmentDocument5 pagesLiterature Review On Equity Investmentafmzrdqrzfasnj100% (1)

- College Internship ReportDocument43 pagesCollege Internship ReportGopi Krishnan.n50% (2)

- BCG - Dealing With Investors Expectations PDFDocument76 pagesBCG - Dealing With Investors Expectations PDFLouis C. MartinNo ratings yet

- SEVENTH. That The Authorized Capital Stock of The Corporation Is ONE BILLION PESOSDocument2 pagesSEVENTH. That The Authorized Capital Stock of The Corporation Is ONE BILLION PESOSReysel Adeza MuliNo ratings yet

- Chapter 2 - Financial Markets: Learning OutcomesDocument9 pagesChapter 2 - Financial Markets: Learning OutcomesIanna Kyla BatomalaqueNo ratings yet

- The Problematic of Financing Small and Medium Sized Enterprise in MoroccoDocument13 pagesThe Problematic of Financing Small and Medium Sized Enterprise in MoroccoHAMED JamalNo ratings yet

- Unit 2 Objectives VipulDocument7 pagesUnit 2 Objectives Vipulamrutapillai06No ratings yet

- Calculating The Cost of Capital: Team Eddie'sDocument37 pagesCalculating The Cost of Capital: Team Eddie'sMarilou AguilarNo ratings yet

- Equity Market Definition of 'Equity Market': Stocks Shares Securities Stock ExchangeDocument15 pagesEquity Market Definition of 'Equity Market': Stocks Shares Securities Stock ExchangeYogesh DevmoreNo ratings yet

- APC Ch9sol PDFDocument7 pagesAPC Ch9sol PDFBaymadNo ratings yet