Download as pdf or txt

You might also like

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- My MBA ProjectDocument93 pagesMy MBA ProjectVivek Nambiar70% (10)

- Mahindra Case StudyDocument19 pagesMahindra Case Studymeena_manju1No ratings yet

- Shareholder's Instructions For Schedule K-1 (Form 1120S) : Internal Revenue ServiceDocument8 pagesShareholder's Instructions For Schedule K-1 (Form 1120S) : Internal Revenue ServiceIRSNo ratings yet

- Shareholder's Instructions For Schedule K-1 (Form 1120S)Document8 pagesShareholder's Instructions For Schedule K-1 (Form 1120S)IRSNo ratings yet

- Shareholder's Instructions For Schedule K-1 (Form 1120S)Document8 pagesShareholder's Instructions For Schedule K-1 (Form 1120S)IRSNo ratings yet

- Shareholder's Instructions For Schedule K-1 (Form 1120S)Document8 pagesShareholder's Instructions For Schedule K-1 (Form 1120S)IRSNo ratings yet

- Shareholder's Instructions For Schedule K-1 (Form 1120S) : Pager/SgmlDocument8 pagesShareholder's Instructions For Schedule K-1 (Form 1120S) : Pager/SgmlIRSNo ratings yet

- Shareholder's Instructions For Schedule K-1 (Form 1120S) : Internal Revenue ServiceDocument8 pagesShareholder's Instructions For Schedule K-1 (Form 1120S) : Internal Revenue ServiceIRSNo ratings yet

- Shareholder's Instructions For Schedule K-1 (Form 1120S) : Pager/SgmlDocument14 pagesShareholder's Instructions For Schedule K-1 (Form 1120S) : Pager/SgmlIRSNo ratings yet

- Partner's Instructions For Schedule K-1 (Form 1065)Document15 pagesPartner's Instructions For Schedule K-1 (Form 1065)Mario LaflammeNo ratings yet

- US Internal Revenue Service: I1065bsk - 2001Document10 pagesUS Internal Revenue Service: I1065bsk - 2001IRSNo ratings yet

- US Internal Revenue Service: I1065sk1 - 2003Document12 pagesUS Internal Revenue Service: I1065sk1 - 2003IRSNo ratings yet

- Partner's Instructions For Schedule K-1 (Form 1065) : Internal Revenue ServiceDocument10 pagesPartner's Instructions For Schedule K-1 (Form 1065) : Internal Revenue ServiceIRSNo ratings yet

- Shareholder's Instructions For Schedule K-1 (Form 1120S) : Pager/SgmlDocument8 pagesShareholder's Instructions For Schedule K-1 (Form 1120S) : Pager/SgmlIRSNo ratings yet

- US Internal Revenue Service: I1065sk1 - 2002Document11 pagesUS Internal Revenue Service: I1065sk1 - 2002IRSNo ratings yet

- Partner's Instructions For Schedule K-1 (Form 1065) : Internal Revenue ServiceDocument10 pagesPartner's Instructions For Schedule K-1 (Form 1065) : Internal Revenue ServiceIRSNo ratings yet

- Partner's Instructions For Schedule K-1 (Form 1065) : Internal Revenue ServiceDocument10 pagesPartner's Instructions For Schedule K-1 (Form 1065) : Internal Revenue ServiceIRSNo ratings yet

- US Internal Revenue Service: I1065sk1Document13 pagesUS Internal Revenue Service: I1065sk1IRS100% (1)

- US Internal Revenue Service: I1065sk1 - 2004Document12 pagesUS Internal Revenue Service: I1065sk1 - 2004IRSNo ratings yet

- US Internal Revenue Service: I1065bsk - 2002Document10 pagesUS Internal Revenue Service: I1065bsk - 2002IRSNo ratings yet

- Partner's Instructions For Schedule K-1 (Form 1065) : Internal Revenue ServiceDocument10 pagesPartner's Instructions For Schedule K-1 (Form 1065) : Internal Revenue ServiceIRSNo ratings yet

- Partner's Instructions For Schedule K-1 (Form 1065) : Internal Revenue ServiceDocument10 pagesPartner's Instructions For Schedule K-1 (Form 1065) : Internal Revenue ServiceIRSNo ratings yet

- US Internal Revenue Service: I1065bsk - 2003Document10 pagesUS Internal Revenue Service: I1065bsk - 2003IRSNo ratings yet

- US Internal Revenue Service: I1065bsk - 2004Document10 pagesUS Internal Revenue Service: I1065bsk - 2004IRSNo ratings yet

- US Internal Revenue Service: I1065bsk - 2005Document10 pagesUS Internal Revenue Service: I1065bsk - 2005IRSNo ratings yet

- US Internal Revenue Service: I1065bskDocument11 pagesUS Internal Revenue Service: I1065bskIRSNo ratings yet

- Instructions For Form 1045 (2021) - Internal Revenue ServiceDocument36 pagesInstructions For Form 1045 (2021) - Internal Revenue ServiceDr. Varah SiedleckiNo ratings yet

- Partner's Instructions For Schedule K-1 (Form 1065)Document15 pagesPartner's Instructions For Schedule K-1 (Form 1065)jeroenbosmaNo ratings yet

- US Internal Revenue Service: I1099div - 2002Document2 pagesUS Internal Revenue Service: I1099div - 2002IRSNo ratings yet

- US Internal Revenue Service: f2210f - 1996Document2 pagesUS Internal Revenue Service: f2210f - 1996IRSNo ratings yet

- Instructions For Form 982: (Rev. March 2018)Document4 pagesInstructions For Form 982: (Rev. March 2018)eagle12No ratings yet

- 2021 Instructions For Schedule E: Supplemental Income and LossDocument12 pages2021 Instructions For Schedule E: Supplemental Income and Lossjyoti06ranjanNo ratings yet

- IRS f982 Goes With The 1099-CDocument5 pagesIRS f982 Goes With The 1099-Cexousiallc100% (3)

- F 5452Document4 pagesF 5452IRSNo ratings yet

- Instructions For Form 2220: Underpayment of Estimated Tax by CorporationsDocument4 pagesInstructions For Form 2220: Underpayment of Estimated Tax by CorporationsIRSNo ratings yet

- IRS Form 982 Reduction of Attributes Due To Discharge of IndebtednessDocument5 pagesIRS Form 982 Reduction of Attributes Due To Discharge of IndebtednessDebe MaxwellNo ratings yet

- Instructions For Form N-20: Partnership Return of IncomeDocument8 pagesInstructions For Form N-20: Partnership Return of IncomedaveyNo ratings yet

- US Internal Revenue Service: I1040sf - 2004Document6 pagesUS Internal Revenue Service: I1040sf - 2004IRSNo ratings yet

- Instructions For Form 990-T: Internal Revenue ServiceDocument15 pagesInstructions For Form 990-T: Internal Revenue ServiceIRSNo ratings yet

- US Internal Revenue Service: I2220 - 1996Document4 pagesUS Internal Revenue Service: I2220 - 1996IRSNo ratings yet

- US Internal Revenue Service: I1040sf - 2001Document6 pagesUS Internal Revenue Service: I1040sf - 2001IRSNo ratings yet

- US Internal Revenue Service: I6251 - 1994Document7 pagesUS Internal Revenue Service: I6251 - 1994IRSNo ratings yet

- Partner's Instructions For Schedule K-1 (Form 1065) : RemindersDocument22 pagesPartner's Instructions For Schedule K-1 (Form 1065) : RemindersAl medranoNo ratings yet

- US Internal Revenue Service: F1040esn - 2001Document5 pagesUS Internal Revenue Service: F1040esn - 2001IRSNo ratings yet

- Explanatory Notes Formct1Document15 pagesExplanatory Notes Formct1lockon31No ratings yet

- 2012 Instructions For Schedule F: Profit or Loss From FarmingDocument20 pages2012 Instructions For Schedule F: Profit or Loss From FarmingRonnie QuimioNo ratings yet

- US Internal Revenue Service: I1099div 07Document3 pagesUS Internal Revenue Service: I1099div 07IRSNo ratings yet

- Instructions For Form 990-T: Internal Revenue ServiceDocument16 pagesInstructions For Form 990-T: Internal Revenue ServiceIRSNo ratings yet

- 2015 Instructions For Schedule E (Form 1040) : Supplemental Income and LossDocument12 pages2015 Instructions For Schedule E (Form 1040) : Supplemental Income and LossManish KotharyNo ratings yet

- US Internal Revenue Service: I1099div - 2006Document3 pagesUS Internal Revenue Service: I1099div - 2006IRSNo ratings yet

- Trang 248Document4 pagesTrang 248Tran Hoang Dong AnhNo ratings yet

- Interest Charge On DISC-Related Deferred Tax Liability: Sign HereDocument2 pagesInterest Charge On DISC-Related Deferred Tax Liability: Sign HereInternational Tax Magazine; David Greenberg PhD, MSA, EA, CPA; Tax Group International; 646-705-2910No ratings yet

- Income Analysis WorksheetDocument11 pagesIncome Analysis WorksheetRajasekhar Reddy AnekalluNo ratings yet

- US Internal Revenue Service: I1040sf - 2000Document6 pagesUS Internal Revenue Service: I1040sf - 2000IRSNo ratings yet

- 2019 W-2 Gregorio MartinezDocument2 pages2019 W-2 Gregorio Martinezporhj perraNo ratings yet

- US Internal Revenue Service: I1040sf - 2003Document6 pagesUS Internal Revenue Service: I1040sf - 2003IRSNo ratings yet

- US Internal Revenue Service: I2220 - 1992Document4 pagesUS Internal Revenue Service: I2220 - 1992IRSNo ratings yet

- US Internal Revenue Service: I1120icd - 1992Document15 pagesUS Internal Revenue Service: I1120icd - 1992IRSNo ratings yet

- Purchases + Carriage Inwards + Other Expenses Incurred On Purchase of Materials - Closing Inventory of MaterialsDocument4 pagesPurchases + Carriage Inwards + Other Expenses Incurred On Purchase of Materials - Closing Inventory of MaterialsSiva SankariNo ratings yet

- 1040 Exam Prep: Module I: The Form 1040 FormulaFrom Everand1040 Exam Prep: Module I: The Form 1040 FormulaRating: 1 out of 5 stars1/5 (3)

- US Internal Revenue Service: 2290rulesty2007v4 0Document6 pagesUS Internal Revenue Service: 2290rulesty2007v4 0IRSNo ratings yet

- 2008 Data DictionaryDocument260 pages2008 Data DictionaryIRSNo ratings yet

- 2008 Credit Card Bulk Provider RequirementsDocument112 pages2008 Credit Card Bulk Provider RequirementsIRSNo ratings yet

- 2008 Objectives Report To Congress v2Document153 pages2008 Objectives Report To Congress v2IRSNo ratings yet

- The Study of Dividend Policies of Indian CompaniesDocument41 pagesThe Study of Dividend Policies of Indian CompaniesKushaal Chaudhary67% (3)

- Assignment - Loan Amortisation ScheduleDocument12 pagesAssignment - Loan Amortisation Scheduleangie_nimmoNo ratings yet

- FME520 Practice QuestionsDocument3 pagesFME520 Practice QuestionsMatende SimionNo ratings yet

- Lecture 1 - Financial Analysis PDFDocument84 pagesLecture 1 - Financial Analysis PDFReymark De veraNo ratings yet

- Rural Development Programmes and Externalities: A Study of Seven Villages in Tamil NaduDocument155 pagesRural Development Programmes and Externalities: A Study of Seven Villages in Tamil NaduSathish BabuNo ratings yet

- Risk Management Surveillance at Ludhiana Stock ExchangeDocument99 pagesRisk Management Surveillance at Ludhiana Stock Exchangepritpal singhNo ratings yet

- Statement of Cash Flows - ProblemsDocument2 pagesStatement of Cash Flows - ProblemsMiladanica Barcelona BarracaNo ratings yet

- Far Eastern University: Bonds Are Classified Into Four Main TypesDocument7 pagesFar Eastern University: Bonds Are Classified Into Four Main TypesAleah Jehan AbuatNo ratings yet

- J Parmar - D Gilmartin O&M PaperDocument14 pagesJ Parmar - D Gilmartin O&M PaperjparmarNo ratings yet

- Peter LynchDocument6 pagesPeter LynchIntan SawalNo ratings yet

- Guidelines For Implementing HR ScoreCardDocument15 pagesGuidelines For Implementing HR ScoreCardparioor95No ratings yet

- Rex Offer Document (Clean)Document732 pagesRex Offer Document (Clean)Invest StockNo ratings yet

- Money Growth and InflationDocument30 pagesMoney Growth and InflationopshoraNo ratings yet

- 15-Minute Retirement Plan FINALDocument23 pages15-Minute Retirement Plan FINALUmar FarooqNo ratings yet

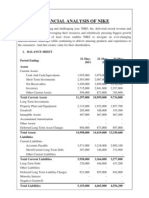

- Financial Analysis of NikeDocument5 pagesFinancial Analysis of NikenimmymathewpkkthlNo ratings yet

- Bank Rec MarkingDocument20 pagesBank Rec MarkingHftc SamNo ratings yet

- Retail Collection PolicyDocument3 pagesRetail Collection PolicyGarimaNo ratings yet

- Sec Memorandum Circular No. 16-02Document6 pagesSec Memorandum Circular No. 16-02Nash Ortiz LuisNo ratings yet

- Effect of Demonetisation On IS-LM Curve.: Money Market EquilibriumDocument5 pagesEffect of Demonetisation On IS-LM Curve.: Money Market EquilibriumswagatikaNo ratings yet

- BankesaddaDocument100 pagesBankesaddamss_sikarwar3812No ratings yet

- Project DatasetDocument201 pagesProject Datasetapi-350428425No ratings yet

- Cochrane On PortfolioDocument86 pagesCochrane On PortfolioecrcauNo ratings yet

- Bivins V Rogers Florida Attorney Ashley Crispin and Attorney Brian O'Connell Guilty of Breaching Fiduciary Duty in This Case.Document18 pagesBivins V Rogers Florida Attorney Ashley Crispin and Attorney Brian O'Connell Guilty of Breaching Fiduciary Duty in This Case.Crystal CoxNo ratings yet

- Genisis of UTI ScamDocument18 pagesGenisis of UTI ScamManish NashaNo ratings yet

- QuizzDocument57 pagesQuizzvitza1No ratings yet

- November 15Document16 pagesNovember 15MLastTryNo ratings yet

- Adobe Inc.Document117 pagesAdobe Inc.Jose AntonioNo ratings yet

- Process Selection and Capacity PlanningDocument18 pagesProcess Selection and Capacity PlanningMarivic TorresNo ratings yet