Download as pdf or txt

You might also like

- Sample Notes To Financial Statements For Single ProprietorDocument6 pagesSample Notes To Financial Statements For Single ProprietorLost Student100% (3)

- Intermediate Accounting 1: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 1: a QuickStudy Digital Reference GuideNo ratings yet

- Acct 3021 Quizzes For Exam I IDocument4 pagesAcct 3021 Quizzes For Exam I IMelissa BrownNo ratings yet

- Bilant in EnglezaDocument6 pagesBilant in EnglezaBiancaDoloNo ratings yet

- Activity 3-4 SB CompensationDocument3 pagesActivity 3-4 SB CompensationNhel Alvaro0% (1)

- ACC 108 QuizDocument11 pagesACC 108 QuizAllian CastroNo ratings yet

- MIDTERMDocument14 pagesMIDTERMSoremn PotatoheadNo ratings yet

- ch7 (1) Becker CPA Chapter 7Document9 pagesch7 (1) Becker CPA Chapter 7VaeNo ratings yet

- MC and Problems-AE221 (Quiz 2)Document6 pagesMC and Problems-AE221 (Quiz 2)Nhel AlvaroNo ratings yet

- Summary PASDocument7 pagesSummary PASRemie Rose BarcebalNo ratings yet

- IFRS - IAS19 - Employee BenefitsDocument16 pagesIFRS - IAS19 - Employee BenefitsFendy YamiNo ratings yet

- IFRS - IAS19 - Employee BenefitsDocument16 pagesIFRS - IAS19 - Employee BenefitsPramita RoyNo ratings yet

- Mohammed Bilal Choudhary (Ju2021Mba14574) Activity - 1 Fsra 1Document4 pagesMohammed Bilal Choudhary (Ju2021Mba14574) Activity - 1 Fsra 1Md BilalNo ratings yet

- IFRS For Small and Medium-Sized Entities: Pocket Guide 2009Document8 pagesIFRS For Small and Medium-Sized Entities: Pocket Guide 2009Robin SicatNo ratings yet

- FAR560 - Interim ReportingDocument18 pagesFAR560 - Interim ReportingSiti AqilahNo ratings yet

- Assignment Discussions On Interim Financial ReportingDocument3 pagesAssignment Discussions On Interim Financial ReportingAllysa Jane FajilagmagoNo ratings yet

- Take Home Activity 3Document6 pagesTake Home Activity 3Justine CruzNo ratings yet

- Employer Benefit - Part 2Document9 pagesEmployer Benefit - Part 2Julian Adam PagalNo ratings yet

- Assam Financial Corporation (1) Accounting PoliciesDocument27 pagesAssam Financial Corporation (1) Accounting PoliciesChinmoy DasNo ratings yet

- Interim Financial ReportingDocument4 pagesInterim Financial ReportingBea ChristineNo ratings yet

- 221 ExamsDocument10 pages221 ExamsElla Mae AgoniaNo ratings yet

- Ifrs VS Us - GaapDocument20 pagesIfrs VS Us - Gaapalokshri25No ratings yet

- REVISED EMPLOYEES BENIFITS IAS 19 and IFRS 2Document8 pagesREVISED EMPLOYEES BENIFITS IAS 19 and IFRS 2It'z Pragmatic IbrahimNo ratings yet

- Ifrs Indian GAPP Cost V/s Fair Value: Components of Financial StatementsDocument8 pagesIfrs Indian GAPP Cost V/s Fair Value: Components of Financial Statementsnagendra2007No ratings yet

- IAS and IFRS Standards For F7FR ACCA ExamDocument9 pagesIAS and IFRS Standards For F7FR ACCA ExamTushar VoiceNo ratings yet

- Ias 16Document4 pagesIas 16Alloysius ParilNo ratings yet

- GIPS Summary PDFDocument4 pagesGIPS Summary PDFrooptejaNo ratings yet

- IFRS AND IAS of AuditDocument11 pagesIFRS AND IAS of AuditAvinash KumarNo ratings yet

- Unit 3 - Interim Reporting - 1484598619Document14 pagesUnit 3 - Interim Reporting - 1484598619Charmaine CañeteNo ratings yet

- Ias 19 Employee BenefitsDocument43 pagesIas 19 Employee BenefitsHasan Ali BokhariNo ratings yet

- Exercise 1. History, Development, and Functions of The Standard-Setting BodiesDocument14 pagesExercise 1. History, Development, and Functions of The Standard-Setting BodiesHershey GalvezNo ratings yet

- The Same As It Would Have Been If The Original Payment Had Been Debited Initially To An Expense AccountDocument37 pagesThe Same As It Would Have Been If The Original Payment Had Been Debited Initially To An Expense AccountNolyne Faith O. VendiolaNo ratings yet

- Accounting Questions: 1 PointDocument4 pagesAccounting Questions: 1 PointxaxaNo ratings yet

- Guidelines For ValuationDocument6 pagesGuidelines For ValuationparikhkashishNo ratings yet

- FARAP-4519Document4 pagesFARAP-4519Accounting StuffNo ratings yet

- 7 Benchmarking Mercer 2010 MethodologyDocument17 pages7 Benchmarking Mercer 2010 MethodologyAdelina Ade100% (2)

- PAS 19 Practice GuideDocument4 pagesPAS 19 Practice GuideEllaine Montojo MirandaNo ratings yet

- Operating Segments PDFDocument4 pagesOperating Segments PDFAvi MartinezNo ratings yet

- Ias 19Document9 pagesIas 19Hammad SarwarNo ratings yet

- IFRS 8 Operating SegmentsDocument6 pagesIFRS 8 Operating SegmentsPratima SeedheeyanNo ratings yet

- JAIBB Accounting 2016Document8 pagesJAIBB Accounting 2016Ahsan ZamanNo ratings yet

- IFRS For Small and Medium-Sized Entities: Pocket Guide 2009Document9 pagesIFRS For Small and Medium-Sized Entities: Pocket Guide 2009Robin SicatNo ratings yet

- Analysis of Finanacing ActivitiesDocument48 pagesAnalysis of Finanacing ActivitiesPrateek SinglaNo ratings yet

- Mas All ExamsDocument192 pagesMas All ExamsJohn Mark VerarNo ratings yet

- Acctg 311N - First Trinal 1Document11 pagesAcctg 311N - First Trinal 1Raenessa FranciscoNo ratings yet

- Description of The Account Based On The San Miguel CorporationDocument5 pagesDescription of The Account Based On The San Miguel CorporationMARRIETTE JOY ABADNo ratings yet

- AE211 Final ExamDocument10 pagesAE211 Final ExamMariette Alex AgbanlogNo ratings yet

- ACC803 Advanced Financial Reporting: Week 2: Financial Statement Preparation and PresentationDocument21 pagesACC803 Advanced Financial Reporting: Week 2: Financial Statement Preparation and PresentationRavinesh PrasadNo ratings yet

- Prof 3 (Final) : If The Partnership Agreement Provides For The Division of Losses Only. Profits Should Be DividedDocument22 pagesProf 3 (Final) : If The Partnership Agreement Provides For The Division of Losses Only. Profits Should Be DividedTifanny MallariNo ratings yet

- Activity 4-Post EbDocument7 pagesActivity 4-Post EbNhel AlvaroNo ratings yet

- SEC Simplifies Financial Reporting For Small Entities: April 4, 2018Document9 pagesSEC Simplifies Financial Reporting For Small Entities: April 4, 2018AndriaNo ratings yet

- Chapter 5Document43 pagesChapter 5Sajid AliNo ratings yet

- Taxation of Unincorporated Business Part 1 - The New BusinessDocument10 pagesTaxation of Unincorporated Business Part 1 - The New BusinessRaja Zahoor ArifNo ratings yet

- 09-OVP2020 Part1-Notes To FSDocument24 pages09-OVP2020 Part1-Notes To FSRuffus ToqueroNo ratings yet

- HDFC Annual Interval FundDocument7 pagesHDFC Annual Interval Fundsandeepkumar404No ratings yet

- Accounting LalaDocument2 pagesAccounting LalaPaw PaladanNo ratings yet

- Aspe Vs IfrsDocument49 pagesAspe Vs IfrsafaiziNo ratings yet

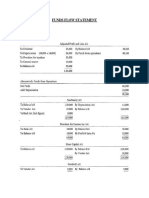

- Funds Flow Statement: Numerical 1Document4 pagesFunds Flow Statement: Numerical 1Neelu AhluwaliaNo ratings yet

- PSAK 56 - Earnings Per Share PDFDocument34 pagesPSAK 56 - Earnings Per Share PDFFendi WijayaNo ratings yet

- Final MF0003 2nd AssigDocument6 pagesFinal MF0003 2nd Assignigistwold5192No ratings yet

- Finance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersFrom EverandFinance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersNo ratings yet

- Financial Statement Fraud IndicatorsDocument5 pagesFinancial Statement Fraud IndicatorsMir Tebrak HossainNo ratings yet

- Annual Report 2019-20 FRLDocument179 pagesAnnual Report 2019-20 FRLBhavin KariaNo ratings yet

- Chapter 9 SolutionsDocument6 pagesChapter 9 SolutionsmackkshellNo ratings yet

- Income Statement and Balance Sheet (LV & Parda)Document30 pagesIncome Statement and Balance Sheet (LV & Parda)Pallavi KalraNo ratings yet

- Clothing Business PlanDocument30 pagesClothing Business PlanBabmani Mani50% (2)

- CORRECTION OF ERRORS Theories PDFDocument7 pagesCORRECTION OF ERRORS Theories PDFJoy Miraflor AlinoodNo ratings yet

- Business Plan by Group 8Document24 pagesBusiness Plan by Group 8Hades RiegoNo ratings yet

- Spending Plans Info Sheet 2 2 5 f1Document4 pagesSpending Plans Info Sheet 2 2 5 f1api-296018213No ratings yet

- Valuation of Keya Cosmetics Ltd.Document74 pagesValuation of Keya Cosmetics Ltd.Anwar Hossain JewelNo ratings yet

- Assurance Services and The Integrity of Financial Reporting, 8 Edition William C. Boynton Raymond N. JohnsonDocument27 pagesAssurance Services and The Integrity of Financial Reporting, 8 Edition William C. Boynton Raymond N. JohnsonDewi Agus SukowatiNo ratings yet

- Project ReportDocument20 pagesProject ReportSrihari Babu100% (1)

- Xiao Enterprise Payslip Mar15Document5 pagesXiao Enterprise Payslip Mar15D Jay ApostelloNo ratings yet

- ENG-21-22 - UB - FEE - ADE-ECO - ACCOUNTING 1st Course - B I - U 4Document39 pagesENG-21-22 - UB - FEE - ADE-ECO - ACCOUNTING 1st Course - B I - U 4Irina FerrerNo ratings yet

- Application For Permit and Recognition of Private SchoolsDocument5 pagesApplication For Permit and Recognition of Private SchoolsajeanismsNo ratings yet

- BCF Annual Report 2014 R1Document15 pagesBCF Annual Report 2014 R1Anonymous UpWci5No ratings yet

- Ind As BookDocument122 pagesInd As BookanupNo ratings yet

- Module - Principless of Accounting IDocument205 pagesModule - Principless of Accounting Iወሬ ነጋሪ- oduu himaaNo ratings yet

- Chapter 2 ActivityDocument10 pagesChapter 2 ActivityBELARMINO LOUIE A.No ratings yet

- ACCA F7 Course NotesDocument272 pagesACCA F7 Course NotesNagendra Krishnamurthy50% (4)

- Chapter 05 XLSolDocument7 pagesChapter 05 XLSolZachary Thomas CarneyNo ratings yet

- Prac One Final Pre BoardDocument7 pagesPrac One Final Pre BoardJose Stanley B. MendozaNo ratings yet

- Chap 1Document18 pagesChap 1Tran Pham Quoc ThuyNo ratings yet

- Fisher Sand GravelDocument46 pagesFisher Sand GravelinforumdocsNo ratings yet

- Acknowledgement Number 272322460110821Document38 pagesAcknowledgement Number 272322460110821Sourabh PunshiNo ratings yet

- Written Report Special Treatment of Fringe Benefits FINAL....Document13 pagesWritten Report Special Treatment of Fringe Benefits FINAL....SANTIAGO CHESKAMAE OQUIANo ratings yet

- 3 Autonomi Dan AkauntabilitiDocument85 pages3 Autonomi Dan AkauntabilitiDhiahVersatil100% (1)

- EthicsDocument2 pagesEthicsjanicasia100% (5)

- W10 Building MaintenanceDocument47 pagesW10 Building MaintenanceMuhammad AizatNo ratings yet

- Reshma Chauhan - PGFC1927 (BOCA)Document9 pagesReshma Chauhan - PGFC1927 (BOCA)Surbhî GuptaNo ratings yet