Download as pdf or txt

You might also like

- Comparison of Sbi Yono With Other Banking AppsDocument16 pagesComparison of Sbi Yono With Other Banking AppsgaganpreetNo ratings yet

- Day To Day Banking Companion Booklet - Scotiabank PDFDocument74 pagesDay To Day Banking Companion Booklet - Scotiabank PDFNhân MaximusNo ratings yet

- Market Research and Product Development: Citi Global Consumer BankDocument4 pagesMarket Research and Product Development: Citi Global Consumer BankAnil Kumar ShahNo ratings yet

- Mobile BankingDocument17 pagesMobile Bankingankitaneema87% (15)

- A Research Study On Awareness of Fin-Tech Among MillennialDocument10 pagesA Research Study On Awareness of Fin-Tech Among MillennialresearchparksNo ratings yet

- Digital Banking: A Mini Project Report OnDocument22 pagesDigital Banking: A Mini Project Report Onvinayak mishraNo ratings yet

- Black Book ProjectDocument23 pagesBlack Book ProjectAtharv KoyandeNo ratings yet

- Project e BankingDocument88 pagesProject e BankingAbhijit MohantyNo ratings yet

- A Descriptive Study On Growth of Mobile Banking & Insurance in India During Covid-19Document69 pagesA Descriptive Study On Growth of Mobile Banking & Insurance in India During Covid-19UPENDRA NISHADNo ratings yet

- Customer Perception Towards Internet Banking PDFDocument17 pagesCustomer Perception Towards Internet Banking PDFarpita waruleNo ratings yet

- Technology in BankingDocument92 pagesTechnology in BankingJason Amaral100% (2)

- Mobile BankingDocument42 pagesMobile BankingGLOBAL INFO-TECH KUMBAKONAMNo ratings yet

- E-Banking in IndiaDocument43 pagesE-Banking in Indiakpalanivel123No ratings yet

- Review of LiteratureDocument4 pagesReview of Literaturemaha lakshmiNo ratings yet

- Internet Banking in SBI - Preeti Pawar 357358Document90 pagesInternet Banking in SBI - Preeti Pawar 357358pawarprateek100% (3)

- Digital Payment by S.SDocument10 pagesDigital Payment by S.SMr David SarkarNo ratings yet

- The Impact of Digitalisation On Indian Banking SectorDocument5 pagesThe Impact of Digitalisation On Indian Banking SectorEditor IJTSRDNo ratings yet

- Technology in BankingDocument98 pagesTechnology in BankingkarenNo ratings yet

- Role of IT in BankingDocument11 pagesRole of IT in BankingManjrekar RohanNo ratings yet

- Mohammad Fazal-1Document81 pagesMohammad Fazal-1Norma SanfordNo ratings yet

- E BankingDocument77 pagesE BankingDEEPAKNo ratings yet

- Mobile BankingDocument97 pagesMobile BankingsspmNo ratings yet

- Chapter-One: E-Banking in Bangladesh: Present Scenario and ProspectsDocument9 pagesChapter-One: E-Banking in Bangladesh: Present Scenario and ProspectsFahad AminNo ratings yet

- Consumer Behaviour On Mobile Banking - A Behavioural Reasoning TheoryDocument12 pagesConsumer Behaviour On Mobile Banking - A Behavioural Reasoning Theory02Mmr 02No ratings yet

- Project Report On e Banking PDFDocument88 pagesProject Report On e Banking PDFSagarNo ratings yet

- e Banking ReportDocument40 pagese Banking Reportleeshee351No ratings yet

- Consumer Behaviour Towards E-Banking - Final ReportDocument68 pagesConsumer Behaviour Towards E-Banking - Final ReportVivek Rana33% (9)

- Diksha Blackbook Mobile BankingDocument52 pagesDiksha Blackbook Mobile BankingDiksha YNo ratings yet

- IntroductionDocument3 pagesIntroduction3037 Vishva RNo ratings yet

- Assainment of Online BankingDocument21 pagesAssainment of Online BankingMOHAMMAD SAIFUL ISLAM100% (1)

- E Banking Consumer BehaviourDocument116 pagesE Banking Consumer Behaviourrevahykrish93No ratings yet

- HDFC Core BankingDocument32 pagesHDFC Core Bankingakashshah1069100% (1)

- A Study On Adoption of Digital Payment Through Mobile Payment Application With Reference To Gujarat StateDocument6 pagesA Study On Adoption of Digital Payment Through Mobile Payment Application With Reference To Gujarat StateEditor IJTSRDNo ratings yet

- Mobile Banking NewDocument33 pagesMobile Banking NewHimanshu MehraNo ratings yet

- A Study of Digital Payment in India and Perspective of Consumer AdoptionDocument2 pagesA Study of Digital Payment in India and Perspective of Consumer Adoptionmahbobullah rahmani0% (1)

- Commercial Bank ManagementDocument11 pagesCommercial Bank ManagementAbhishek Chopra0% (1)

- Digital Payments For Rural India - Challenges and OpportunitiesDocument8 pagesDigital Payments For Rural India - Challenges and OpportunitiesIJOPAAR JOURNALNo ratings yet

- An Article On Digital Innovations in BanksDocument4 pagesAn Article On Digital Innovations in BanksKadar mohideen ANo ratings yet

- Fintech and Financial InclusionDocument22 pagesFintech and Financial InclusionHabiba KausarNo ratings yet

- A Study of Digitalization Impact On Bank of Maharastra PDFDocument85 pagesA Study of Digitalization Impact On Bank of Maharastra PDFwarghade academyNo ratings yet

- ProjectDocument50 pagesProjectkomalpreetdhirNo ratings yet

- Literature Review: Digital Payment System in IndiaDocument8 pagesLiterature Review: Digital Payment System in IndiaAkshay Thampi0% (1)

- Project On UPIDocument17 pagesProject On UPIpallavimishra1109No ratings yet

- The Impact of E Banking On The Use of Banking Services and Customers SatisfactionDocument4 pagesThe Impact of E Banking On The Use of Banking Services and Customers SatisfactionEditor IJTSRDNo ratings yet

- Mid Term - A Study of Consumer Perception Towards Mobile Wallet in Delhi NCRDocument35 pagesMid Term - A Study of Consumer Perception Towards Mobile Wallet in Delhi NCRamanNo ratings yet

- 03.impact of Digital Banking On Profitability of Public & Private Sector Banks in IndiaDocument9 pages03.impact of Digital Banking On Profitability of Public & Private Sector Banks in IndiaNilesh MotwaniNo ratings yet

- A Study On Customer Attitude Towards Mobile Banking With Special Reference To Erode DistrictDocument6 pagesA Study On Customer Attitude Towards Mobile Banking With Special Reference To Erode DistrictEditor IJTSRDNo ratings yet

- Innovation in Banking SectorDocument21 pagesInnovation in Banking Sectoruma2k10No ratings yet

- Final Final BlackbookDocument105 pagesFinal Final BlackbookIsha PednekarNo ratings yet

- Banking 3Document2 pagesBanking 3Manju MessiNo ratings yet

- Impact of Digitalisation On Bank Performance: A Study of Indian BanksDocument15 pagesImpact of Digitalisation On Bank Performance: A Study of Indian BanksHardik MistryNo ratings yet

- Review of Literature:: Definition of Electronic Payment SystemsDocument3 pagesReview of Literature:: Definition of Electronic Payment SystemsAvula Shravan YadavNo ratings yet

- A Study On Role of Technology in Banking SectorDocument6 pagesA Study On Role of Technology in Banking SectorEditor IJTSRD50% (2)

- Digital Payment System 2018Document12 pagesDigital Payment System 2018wong wai hongNo ratings yet

- A Study of Usage Security of The Mobile Payments Services in IndiaDocument62 pagesA Study of Usage Security of The Mobile Payments Services in IndiaPinak DuttaNo ratings yet

- Digital Banking SystemDocument22 pagesDigital Banking SystemAvijit Manna100% (1)

- NTCC Banking System in IndiaDocument23 pagesNTCC Banking System in IndiaPriyanka RajNo ratings yet

- Challenges Faced by Fintechs in IndiaDocument2 pagesChallenges Faced by Fintechs in IndiaSRISHTI NARANGNo ratings yet

- SBI Mobile BankingDocument64 pagesSBI Mobile Bankingankit161019893980No ratings yet

- Mobile Banking - Project ReportDocument33 pagesMobile Banking - Project ReportAlpha GamingNo ratings yet

- Top Ten Banking EmergencyDocument5 pagesTop Ten Banking EmergencyDPC GymNo ratings yet

- Punjab College of Technical Education Mba-2C Indian Ethos Project AssignmentDocument17 pagesPunjab College of Technical Education Mba-2C Indian Ethos Project AssignmentHIMANSHU RAWATNo ratings yet

- Anureet Economics ProjectDocument9 pagesAnureet Economics ProjectHIMANSHU RAWATNo ratings yet

- Coffee Chain India11Document5 pagesCoffee Chain India11HIMANSHU RAWATNo ratings yet

- PCTE Group of Institutes, Ludhiana: Mba Semester 2Document6 pagesPCTE Group of Institutes, Ludhiana: Mba Semester 2HIMANSHU RAWATNo ratings yet

- PCTE Group of Institutes, Ludhiana: Human Resource Management, Sem-2Document3 pagesPCTE Group of Institutes, Ludhiana: Human Resource Management, Sem-2HIMANSHU RAWATNo ratings yet

- G.A.M.E Video AnalysisDocument2 pagesG.A.M.E Video AnalysisHIMANSHU RAWATNo ratings yet

- PCTE Group of Institutes, Ludhiana: Human Resource Management, Sem-2Document6 pagesPCTE Group of Institutes, Ludhiana: Human Resource Management, Sem-2HIMANSHU RAWATNo ratings yet

- Synopsis Crompton Greaves Consumer Electrical Ltd.Document4 pagesSynopsis Crompton Greaves Consumer Electrical Ltd.HIMANSHU RAWATNo ratings yet

- PCTE Group of Institutes, Ludhiana: Human Resource Management, Sem-2Document4 pagesPCTE Group of Institutes, Ludhiana: Human Resource Management, Sem-2HIMANSHU RAWATNo ratings yet

- Himanshu Rawat - Jashanpreet Singh - Coffee ChainDocument17 pagesHimanshu Rawat - Jashanpreet Singh - Coffee ChainHIMANSHU RAWATNo ratings yet

- Submitted By: Himanshu Rawat Submitted To:Dr. Pallavi DawraDocument16 pagesSubmitted By: Himanshu Rawat Submitted To:Dr. Pallavi DawraHIMANSHU RAWATNo ratings yet

- Marico Limited - Investor Presentation - February 2019Document65 pagesMarico Limited - Investor Presentation - February 2019HIMANSHU RAWATNo ratings yet

- PerformanceAGlance 10 YearsDocument1 pagePerformanceAGlance 10 YearsHIMANSHU RAWATNo ratings yet

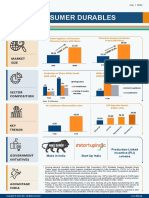

- Consumer Durables Infographic July 2021Document1 pageConsumer Durables Infographic July 2021HIMANSHU RAWATNo ratings yet

- Rishab Garg Major ProjrctDocument10 pagesRishab Garg Major ProjrctHIMANSHU RAWATNo ratings yet

- GroupDocument48 pagesGroupHIMANSHU RAWATNo ratings yet

- Project Report Cycle PartsDocument142 pagesProject Report Cycle PartsHIMANSHU RAWATNo ratings yet

- Jindal Steels & Power LimitedDocument10 pagesJindal Steels & Power LimitedHIMANSHU RAWATNo ratings yet

- Ratio Analysis: Chaksh Sharma, Assistant Professor, PCTEDocument25 pagesRatio Analysis: Chaksh Sharma, Assistant Professor, PCTEHIMANSHU RAWATNo ratings yet

- Historical Phases of CSRDocument12 pagesHistorical Phases of CSRHIMANSHU RAWATNo ratings yet

- Business Environment: Topic - Middle EastDocument12 pagesBusiness Environment: Topic - Middle EastHIMANSHU RAWATNo ratings yet

- Historical Phases of CSRDocument12 pagesHistorical Phases of CSRHIMANSHU RAWATNo ratings yet

- Investment Valuation RatiosDocument3 pagesInvestment Valuation RatiosHIMANSHU RAWATNo ratings yet

- Himanshu Rawat & Rishab Garg Marico ProjectDocument12 pagesHimanshu Rawat & Rishab Garg Marico ProjectHIMANSHU RAWATNo ratings yet

- MAHINDRA & MAHINDRA... FinalDocument32 pagesMAHINDRA & MAHINDRA... FinalHIMANSHU RAWAT100% (1)

- Assignment 1 Chapter /topic: Foreign Exchange Market InstructionDocument3 pagesAssignment 1 Chapter /topic: Foreign Exchange Market InstructionDeveraj Muniandy ThevarNo ratings yet

- d424 HlsummaryDocument16 pagesd424 HlsummaryNathalie NaniNo ratings yet

- PRJP - 1653Document9 pagesPRJP - 1653PraKhar PandeNo ratings yet

- Secured Transactions and Collateral Registries A Global PerspectiveDocument36 pagesSecured Transactions and Collateral Registries A Global PerspectiveADBI EventsNo ratings yet

- 716 Bob StatementDocument10 pages716 Bob Statementअभिषेक मिश्राNo ratings yet

- Moneylion StatementDocument1 pageMoneylion StatementrolphcourtenayNo ratings yet

- سوبرماركت سمى �PHEKAN SAHDocument1 pageسوبرماركت سمى �PHEKAN SAHmohamad syrNo ratings yet

- 86d7fd13-a6d8-461f-9c4c-a5c1ab5ec0ffDocument2 pages86d7fd13-a6d8-461f-9c4c-a5c1ab5ec0ffnavid kamrava100% (1)

- SBI Financial InclusionDocument6 pagesSBI Financial Inclusionmanideep111100% (1)

- Final ScamDocument5 pagesFinal ScamSanju ReddyNo ratings yet

- Correspondent BanksDocument4 pagesCorrespondent BankscharrisedelarosaNo ratings yet

- Reserve Requirement/Deposit Expansion AND BANK BALANCE SHEET PRACTICE Questions - Show Your Work and Answer in The Space ProvidedDocument6 pagesReserve Requirement/Deposit Expansion AND BANK BALANCE SHEET PRACTICE Questions - Show Your Work and Answer in The Space ProvidedRingle JobNo ratings yet

- PPT On NpaDocument20 pagesPPT On NpaNoor Preet KaurNo ratings yet

- Khatabook Customer Transactions 08.04.2024 07.24.41.PMDocument11 pagesKhatabook Customer Transactions 08.04.2024 07.24.41.PMfaizancscmailNo ratings yet

- 93c3 Document 3Document14 pages93c3 Document 3NONON NICOLASNo ratings yet

- Financial Products in Kotak Mahiindra Bank and Its CompetitorsDocument93 pagesFinancial Products in Kotak Mahiindra Bank and Its CompetitorsShobhit GoswamiNo ratings yet

- Hidayatullah National Law University: Mortgage and Its Various TypesDocument16 pagesHidayatullah National Law University: Mortgage and Its Various TypesSirshenduNo ratings yet

- Promissory Note: Co-Makers' StatementDocument1 pagePromissory Note: Co-Makers' Statementjunna lyn sanchezNo ratings yet

- Personal and Household FinanceDocument5 pagesPersonal and Household FinanceMuhammad SamhanNo ratings yet

- Global Direct Selling CompanyDocument3 pagesGlobal Direct Selling Companyjayesh lokhandeNo ratings yet

- PhonePe PulseDocument49 pagesPhonePe PulseAbcd123411No ratings yet

- Sales ReportDocument2 pagesSales ReportJames RodriguezNo ratings yet

- Agats & Merauke (IDR)Document2 pagesAgats & Merauke (IDR)Mandiri TBANo ratings yet

- Axis Saving Ac Opening FormDocument4 pagesAxis Saving Ac Opening Formashish.rac6053No ratings yet

- AUDITING - PRELIM - For PrintingDocument4 pagesAUDITING - PRELIM - For PrintingAndreiu Mark EsmeleNo ratings yet

- Paper Manajemen Risiko: Disusun Oleh: DAMA AZIIZ PRAYOGO (1805056014) Kelas Manajemen A7Document8 pagesPaper Manajemen Risiko: Disusun Oleh: DAMA AZIIZ PRAYOGO (1805056014) Kelas Manajemen A7blazerpria kerenNo ratings yet

- GST Invoice: Perfect SoftconDocument1 pageGST Invoice: Perfect SoftconpiyushjainpcNo ratings yet

- Mishkin 6ce TB Ch12Document37 pagesMishkin 6ce TB Ch12JaeDukAndrewSeoNo ratings yet