Download as pdf or txt

You might also like

- Your Final Bill.: Account Balance Your Payment Is Due NowDocument3 pagesYour Final Bill.: Account Balance Your Payment Is Due NowJaktron71% (7)

- Instant Download Ebook PDF Fundamentals of Corporate Finance Third Canadian 3rd Edition PDF ScribdDocument42 pagesInstant Download Ebook PDF Fundamentals of Corporate Finance Third Canadian 3rd Edition PDF Scribdwalter.herbert733100% (49)

- Working Capital QuestionsDocument10 pagesWorking Capital QuestionsVaishnavi VenkatesanNo ratings yet

- Chapter 16 AssignmentDocument4 pagesChapter 16 Assignmentsam broughtonNo ratings yet

- All Sums CostingDocument14 pagesAll Sums Costingshankarinadar100% (1)

- Financial Management PROBLEMS FROM UNIT - 2Document14 pagesFinancial Management PROBLEMS FROM UNIT - 2jeganrajrajNo ratings yet

- PDF To DocsDocument72 pagesPDF To Docs777priyankaNo ratings yet

- URP Income Tax Part SolutionsDocument127 pagesURP Income Tax Part SolutionsSushant MaskeyNo ratings yet

- Leverage: Prepared By:-Priyanka GohilDocument23 pagesLeverage: Prepared By:-Priyanka GohilSunil PillaiNo ratings yet

- FFM Updated AnswersDocument79 pagesFFM Updated AnswersSrikrishnan S100% (1)

- Techniques of Capital Budgeting SumsDocument15 pagesTechniques of Capital Budgeting Sumshardika jadavNo ratings yet

- Leverages ProblemsDocument4 pagesLeverages Problemsk,hbibk,n50% (2)

- Financial Management - PROBLEMS FROM UNIT - 4Document5 pagesFinancial Management - PROBLEMS FROM UNIT - 4jeganrajraj100% (1)

- Problems LeverageDocument20 pagesProblems LeverageMadhav RajbanshiNo ratings yet

- Chapter 4 Overhead ProblemsDocument5 pagesChapter 4 Overhead Problemsthiluvnddi100% (2)

- CA Ipcc Costing Suggested Answers For Nov 20161Document12 pagesCA Ipcc Costing Suggested Answers For Nov 20161Sai Kumar SandralaNo ratings yet

- 1 From The Following Information Prepare A Statement Showing The Working CapitalDocument4 pages1 From The Following Information Prepare A Statement Showing The Working CapitalHarihara PuthiranNo ratings yet

- Cost AccountingDocument6 pagesCost Accountingchirag shahNo ratings yet

- CH 8 LeverageDocument51 pagesCH 8 LeverageNikita AggarwalNo ratings yet

- Chapter 10 - Dividend PolicyDocument37 pagesChapter 10 - Dividend PolicyShubhra Srivastava100% (1)

- 7891FinalGr1paper2ManagementAccountingandFinancilAnalys PDFDocument32 pages7891FinalGr1paper2ManagementAccountingandFinancilAnalys PDFPrasanna SharmaNo ratings yet

- Dividend PolicyDocument13 pagesDividend PolicyRakesh Gupta100% (2)

- Ratio Analysis Numerical QuestionsDocument9 pagesRatio Analysis Numerical Questionsnsrivastav1No ratings yet

- Cost DJB - MTP Oct21Document10 pagesCost DJB - MTP Oct21Bharath Krishna MVNo ratings yet

- Dividend DecisionDocument4 pagesDividend DecisionKhushi Rani100% (2)

- Receivable Management Llustration 1: A Company Has Prepared The Following Projections For A YearDocument6 pagesReceivable Management Llustration 1: A Company Has Prepared The Following Projections For A YearJC Del MundoNo ratings yet

- AS-19-LeasesDocument23 pagesAS-19-LeasesKrishna Jha0% (2)

- Financial Management: Unit 3Document47 pagesFinancial Management: Unit 3muralikarthik31No ratings yet

- 18415compsuggans PCC FM Chapter7Document13 pages18415compsuggans PCC FM Chapter7Mukunthan RBNo ratings yet

- Valuation of Fixed Income Securities Aims and ObjectivesDocument20 pagesValuation of Fixed Income Securities Aims and ObjectivesAyalew Taye100% (2)

- Unit 3: Cost of Capital Cost of DebtDocument11 pagesUnit 3: Cost of Capital Cost of DebtTaransh A100% (1)

- Cost Acc Nov06Document27 pagesCost Acc Nov06api-3825774100% (1)

- CAPITAL STRUCTURE Sums OnlinePGDMDocument6 pagesCAPITAL STRUCTURE Sums OnlinePGDMSoumendra RoyNo ratings yet

- Cost of Capital: Vivek College of CommerceDocument31 pagesCost of Capital: Vivek College of Commercekarthika kounderNo ratings yet

- L3-L4 CostsheetDocument30 pagesL3-L4 CostsheetDhawal RajNo ratings yet

- Dividend Policy - Sample Problems - ICAIDocument2 pagesDividend Policy - Sample Problems - ICAIgfahsgdahNo ratings yet

- Ca Ipcc Costing and Financial Management Suggested Answers May 2015Document20 pagesCa Ipcc Costing and Financial Management Suggested Answers May 2015Prasanna KumarNo ratings yet

- Marginal Costing and Its Application - ProblemsDocument5 pagesMarginal Costing and Its Application - ProblemsAAKASH BAIDNo ratings yet

- Bond Yield To Maturity (YTM) FormulasDocument2 pagesBond Yield To Maturity (YTM) FormulasIzzy BNo ratings yet

- Transfer Price Questuon Ca Final PDFDocument69 pagesTransfer Price Questuon Ca Final PDFCoc GamingNo ratings yet

- Answer 1 - Cost of CapitalDocument2 pagesAnswer 1 - Cost of Capitaljeganrajraj100% (1)

- Cost of Capital Solved Problems - Cost of Capital - Capital StructureDocument1 pageCost of Capital Solved Problems - Cost of Capital - Capital StructureAnonymous qOdzTznKE100% (1)

- BudgetDocument15 pagesBudgetJoydip DasguptaNo ratings yet

- 46793bosinter p8 Seca cp5 PDFDocument42 pages46793bosinter p8 Seca cp5 PDFIsavic AlsinaNo ratings yet

- LEVERAGE Online Problem SheetDocument6 pagesLEVERAGE Online Problem SheetSoumendra RoyNo ratings yet

- 7 Additional Solved Problems 6Document14 pages7 Additional Solved Problems 6Pranoy SarkarNo ratings yet

- Inancing Ecisions: Unit - I: Cost of Capital Answer Weighted Average Cost of CapitalDocument15 pagesInancing Ecisions: Unit - I: Cost of Capital Answer Weighted Average Cost of Capitalanon_672065362No ratings yet

- Unit - V Budget and Budgetary Control ProblemsDocument2 pagesUnit - V Budget and Budgetary Control ProblemsalexanderNo ratings yet

- Decision-Making Using Marginal Costing-IDocument11 pagesDecision-Making Using Marginal Costing-Iapi-27014089100% (3)

- Numericals On Capital BudgetingDocument3 pagesNumericals On Capital BudgetingRevati ShindeNo ratings yet

- Chapter - 5 Marginal CostingDocument9 pagesChapter - 5 Marginal CostingDipen AdhikariNo ratings yet

- Dividend Policy Gorden, Walter & MM Model Practice QuestionsDocument1 pageDividend Policy Gorden, Walter & MM Model Practice QuestionsAmjad AliNo ratings yet

- CH # 8 (By Product)Document10 pagesCH # 8 (By Product)Rooh Ullah KhanNo ratings yet

- EBIT EPS AnalysisDocument17 pagesEBIT EPS AnalysisAditya GuptaNo ratings yet

- 5.calculation of EPSDocument6 pages5.calculation of EPSVinitga100% (1)

- Cost Sheet Practice QuestionsDocument6 pagesCost Sheet Practice Questionsmeenagoyal995650% (2)

- Leasing Solution Ca-Final SFM (Full)Document32 pagesLeasing Solution Ca-Final SFM (Full)Pravinn_Mahajan80% (5)

- 19732ipcc CA Vol2 Cp3Document43 pages19732ipcc CA Vol2 Cp3PALADUGU MOUNIKANo ratings yet

- Operation Scheduling PDFDocument26 pagesOperation Scheduling PDFMd. Mahbub-ul- Huq Alvi, 170021144No ratings yet

- FM - Valuation of Bond and StocksDocument10 pagesFM - Valuation of Bond and StocksMaxine SantosNo ratings yet

- Lec 6 SlidesDocument29 pagesLec 6 Slidesc5y5f562y4No ratings yet

- Bond Valuation 1Document33 pagesBond Valuation 1bhaskkarNo ratings yet

- BFW1001 Foundations of Finance: Valuation of Fixed Income Securities: Updated April 28, 2020Document14 pagesBFW1001 Foundations of Finance: Valuation of Fixed Income Securities: Updated April 28, 2020Quoc Viet DuongNo ratings yet

- Basundhara Tala ThapDocument2 pagesBasundhara Tala ThapSushant MaskeyNo ratings yet

- Bbs 4Document55 pagesBbs 4Sushant MaskeyNo ratings yet

- MS Word: Marks AllocationDocument1 pageMS Word: Marks AllocationSushant MaskeyNo ratings yet

- Layout Er SuggestDocument1 pageLayout Er SuggestSushant MaskeyNo ratings yet

- Exam Date: 2079-11-26 (2023-03-10) : IT Training Passed Out Student The Institute of Chartered Accountants of NepalDocument1 pageExam Date: 2079-11-26 (2023-03-10) : IT Training Passed Out Student The Institute of Chartered Accountants of NepalSushant MaskeyNo ratings yet

- 500 Question SetDocument72 pages500 Question SetSushant MaskeyNo ratings yet

- IT ResultDocument1 pageIT ResultSushant MaskeyNo ratings yet

- UntitledDocument72 pagesUntitledSushant MaskeyNo ratings yet

- Exam Date: 2079-10-29 (2023-02-12) : IT Training Passed Out Student The Institute of Chartered Accountants of NepalDocument1 pageExam Date: 2079-10-29 (2023-02-12) : IT Training Passed Out Student The Institute of Chartered Accountants of NepalSushant MaskeyNo ratings yet

- Branch AccountingDocument51 pagesBranch AccountingSushant MaskeyNo ratings yet

- Cost of CapitalDocument37 pagesCost of CapitalSushant Maskey100% (1)

- Valn of CMN StockDocument18 pagesValn of CMN StockSushant Maskey0% (1)

- Budget AnswersDocument6 pagesBudget AnswersSushant MaskeyNo ratings yet

- Budget & Budgetary ControlDocument15 pagesBudget & Budgetary ControlSushant MaskeyNo ratings yet

- Chapter 4: LeverageDocument15 pagesChapter 4: LeverageSushant MaskeyNo ratings yet

- Overheads PracticalDocument37 pagesOverheads PracticalSushant Maskey100% (1)

- RD TReeqim RSFH XACz 0 W91617196460Document10 pagesRD TReeqim RSFH XACz 0 W91617196460Sushant MaskeyNo ratings yet

- Risk Return Basics/Portfolio Management: Learning Objective of The ChapterDocument34 pagesRisk Return Basics/Portfolio Management: Learning Objective of The ChapterSushant MaskeyNo ratings yet

- Chapter 4: LeverageDocument15 pagesChapter 4: LeverageSushant MaskeyNo ratings yet

- Capital StructureDocument31 pagesCapital StructureSushant Maskey100% (1)

- EDP Audit CIS Environment MeaningDocument7 pagesEDP Audit CIS Environment MeaningSushant MaskeyNo ratings yet

- NIOjid Akjc MDI9 L 5 Ulv I1617282937Document4 pagesNIOjid Akjc MDI9 L 5 Ulv I1617282937Sushant MaskeyNo ratings yet

- Govt AuditingDocument12 pagesGovt AuditingSushant MaskeyNo ratings yet

- CAPII Suggested Dec2015Document87 pagesCAPII Suggested Dec2015Sushant MaskeyNo ratings yet

- Labour/Employee Cost: Classification of Labor CostDocument9 pagesLabour/Employee Cost: Classification of Labor CostSushant MaskeyNo ratings yet

- Labour: (A) (B) (C) (D) (E)Document40 pagesLabour: (A) (B) (C) (D) (E)Sushant Maskey100% (1)

- Kieso Inter 13e Ch13Document67 pagesKieso Inter 13e Ch13mikeafriedmanNo ratings yet

- TUT 03 Time Value of MoneyDocument2 pagesTUT 03 Time Value of MoneyShubham NayakNo ratings yet

- Assigment 2 Spring 2013Document3 pagesAssigment 2 Spring 2013JustinNo ratings yet

- Case Study 2 - ReportDocument10 pagesCase Study 2 - ReportTomás TavaresNo ratings yet

- IMT 57 Financial Accounting M1Document4 pagesIMT 57 Financial Accounting M1solvedcareNo ratings yet

- Yield To Maturity Answer KeyDocument2 pagesYield To Maturity Answer KeyBrandon LumibaoNo ratings yet

- General Financial Literacy Student ChecklistDocument3 pagesGeneral Financial Literacy Student ChecklistKarsten Walker100% (1)

- Financial Statements - Tata Steel & JSW SteelDocument10 pagesFinancial Statements - Tata Steel & JSW Steelrohit5saoNo ratings yet

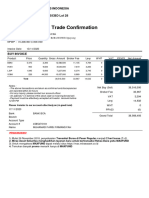

- Trade ConfirmationDocument1 pageTrade ConfirmationCKS CateringNo ratings yet

- Chapter 4 The Time Value of MoneyDocument39 pagesChapter 4 The Time Value of MoneyQuỳnh NguyễnNo ratings yet

- DCF SBI TemplateDocument7 pagesDCF SBI Templatekeya.bitsembryoNo ratings yet

- Yes Bank Failure Exposes India To Wider Credit Risk - Nomura - The Economic TimesDocument2 pagesYes Bank Failure Exposes India To Wider Credit Risk - Nomura - The Economic TimesTushar SharmaNo ratings yet

- GM Insights - Asymmetry - 9-20Document16 pagesGM Insights - Asymmetry - 9-20richardck61No ratings yet

- b2 AnsDocument13 pagesb2 AnsRashid AbeidNo ratings yet

- Assignment - Operating Lease & Direct Financing LeaseDocument8 pagesAssignment - Operating Lease & Direct Financing Leaseangelian bagadiongNo ratings yet

- Soco V MilitanteDocument4 pagesSoco V MilitanteAllen Windel BernabeNo ratings yet

- Niruword 3Document11 pagesNiruword 3Raju BhaiNo ratings yet

- What Is Fiscal PolicyDocument5 pagesWhat Is Fiscal PolicyJanhvi AroraNo ratings yet

- Bill of Supply For Electricity (Amended) Due Date: - : BSES Rajdhani Power LTDDocument1 pageBill of Supply For Electricity (Amended) Due Date: - : BSES Rajdhani Power LTDLalan ChaudharyNo ratings yet

- Words GigiDocument102 pagesWords GigiNguyen Ha QuanNo ratings yet

- JS Bank Second Quarter and Half Year Report June 30 2021 2Document104 pagesJS Bank Second Quarter and Half Year Report June 30 2021 2HassanNo ratings yet

- KsebBill 1155058024039Document1 pageKsebBill 1155058024039akkgptcktmNo ratings yet

- Module III: DerivativesDocument18 pagesModule III: Derivativessantucan1No ratings yet

- 愛升息特選理財壽險計劃 - 產品小冊子Document8 pages愛升息特選理財壽險計劃 - 產品小冊子TNo ratings yet

- Ifrs 1 First Time AdoptionDocument27 pagesIfrs 1 First Time Adoptionesulawyer2001No ratings yet

- Soft Drink CompanyDocument6 pagesSoft Drink Companymanish_mittalNo ratings yet

- Finance Project - KSFEDocument48 pagesFinance Project - KSFEDinesh77% (13)

- Development Financial Institution in India: Preeti SharmaDocument27 pagesDevelopment Financial Institution in India: Preeti Sharmahridesh21No ratings yet