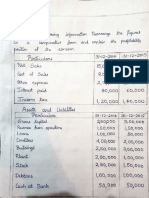

Horizontal and Vertical Analaysis: Karysse Arielle Noel Jalao Financial Management Bsac-2B

Horizontal and Vertical Analaysis: Karysse Arielle Noel Jalao Financial Management Bsac-2B

You might also like

- Magsino Hannah Florence Activity 5 Discounted Cash FlowsDocument36 pagesMagsino Hannah Florence Activity 5 Discounted Cash FlowsKathyrine Claire Edrolin100% (2)

- Keith J Cunningham - Financial LiteracyDocument5 pagesKeith J Cunningham - Financial Literacykoetjinsiong100% (4)

- Bharat Chemicals Ltd. SolnDocument4 pagesBharat Chemicals Ltd. SolnJayash KaushalNo ratings yet

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- Sep 27 - Practice Problems On ValuationDocument2 pagesSep 27 - Practice Problems On ValuationMost. Amina KhatunNo ratings yet

- Black BookDocument85 pagesBlack BookRamesh Yadav100% (1)

- Exercises FSDocument6 pagesExercises FSDIVINE GRACE ROSALESNo ratings yet

- Peoria COperation - Cash Flow StatementDocument8 pagesPeoria COperation - Cash Flow StatementcbarajNo ratings yet

- Analysis and Interpretation of FS-Part 1Document2 pagesAnalysis and Interpretation of FS-Part 1Rhea RamirezNo ratings yet

- Internal Test - 2 - FSA - QuestionDocument3 pagesInternal Test - 2 - FSA - QuestionSandeep Choudhary40% (5)

- Technical Analysis of Stocks Commodities 2018 No 07 PDFDocument64 pagesTechnical Analysis of Stocks Commodities 2018 No 07 PDFs9298100% (1)

- Fsa Questions and SolutionsDocument11 pagesFsa Questions and SolutionsAnjali Betala KothariNo ratings yet

- Comparative Income Statement of Star Company For 2016-2018 Star Company Comparative Income Statement December 31, 2016,2017 and 2018Document5 pagesComparative Income Statement of Star Company For 2016-2018 Star Company Comparative Income Statement December 31, 2016,2017 and 2018JonellNo ratings yet

- Top Down Ebit Tax Rate Nopat 6600: Net Sales 100,000Document2 pagesTop Down Ebit Tax Rate Nopat 6600: Net Sales 100,000Jayash KaushalNo ratings yet

- 201B 201A Peso Change % ChangeDocument4 pages201B 201A Peso Change % ChangeNin JahNo ratings yet

- Task Performance I. Horizontal AnalysisDocument3 pagesTask Performance I. Horizontal AnalysisarisuNo ratings yet

- Assignment N3Document12 pagesAssignment N3Maiko KopadzeNo ratings yet

- Homework N3Document24 pagesHomework N3Maiko KopadzeNo ratings yet

- Question No 1: A-Gross PayDocument6 pagesQuestion No 1: A-Gross PayArmaghan Ali MalikNo ratings yet

- Financial Statement: Balance SheetDocument2 pagesFinancial Statement: Balance SheetChara etangNo ratings yet

- Chapter Five Format and ExampleDocument8 pagesChapter Five Format and Examplechris mutungaNo ratings yet

- Inbound 578213835412696153Document2 pagesInbound 578213835412696153Joppel PrescoNo ratings yet

- 20201015012755Document57 pages20201015012755hasharawanNo ratings yet

- Assgnmnt 2 FIN658Document5 pagesAssgnmnt 2 FIN658markNo ratings yet

- Pricewell Single Entity Financial StatementsDocument6 pagesPricewell Single Entity Financial StatementsBig SmutNo ratings yet

- Cortez Exam in Business FinanceDocument4 pagesCortez Exam in Business FinanceFranchesca CortezNo ratings yet

- 8-9 Mecca Copy Budget Balance SheetDocument5 pages8-9 Mecca Copy Budget Balance SheetAli Hassan SukheraNo ratings yet

- 5110WA7 FinancialsDocument1 page5110WA7 FinancialsAhmed EzzNo ratings yet

- 5.ratio Analysis SumsDocument9 pages5.ratio Analysis Sumsvinay kumar nuwalNo ratings yet

- AFAR2 CH. 3 - Problem Quiz 1Document19 pagesAFAR2 CH. 3 - Problem Quiz 1Von Andrei MedinaNo ratings yet

- BTAXREV ACT 184 Week 3 Income Taxation - Tax ReturnsDocument21 pagesBTAXREV ACT 184 Week 3 Income Taxation - Tax ReturnsgatotkaNo ratings yet

- Intercompany Sale of PPE Problem 2: Requirement: January 1, 20x4Document31 pagesIntercompany Sale of PPE Problem 2: Requirement: January 1, 20x4Abegail LibreaNo ratings yet

- Model Scheme IS CFS Fcfe BS Irr Coc NPV/DCF Development ScheduleDocument11 pagesModel Scheme IS CFS Fcfe BS Irr Coc NPV/DCF Development ScheduleMilind VatsiNo ratings yet

- Horizontal and Vertical AnalysisDocument4 pagesHorizontal and Vertical AnalysisJasmine ActaNo ratings yet

- Quiz BusFinHVRJULIANA VILLANUEVA ABM201-1Document10 pagesQuiz BusFinHVRJULIANA VILLANUEVA ABM201-1Juliana Angela VillanuevaNo ratings yet

- Illustration For Financial Analysis Using RatioDocument2 pagesIllustration For Financial Analysis Using RatioamahaktNo ratings yet

- Financial Management Week 2 AssignmentDocument2 pagesFinancial Management Week 2 AssignmentAndrea Monique AlejagaNo ratings yet

- Cash Flow HomeworkDocument2 pagesCash Flow HomeworkMyron BrandwineNo ratings yet

- 5,655.00 Additional Investment Needed/financingDocument23 pages5,655.00 Additional Investment Needed/financingMPCINo ratings yet

- Analysis and Interpretation of Financial StatementsDocument24 pagesAnalysis and Interpretation of Financial StatementsMariel NatullaNo ratings yet

- P and L and BSDocument8 pagesP and L and BSgautam48128No ratings yet

- Võ Thành Thắng - 31211024016 - NFGDocument28 pagesVõ Thành Thắng - 31211024016 - NFGtungphan.31211023431No ratings yet

- Tut 8 - Management AccountingDocument29 pagesTut 8 - Management AccountingTao LoheNo ratings yet

- Bank A and B - Bank XDocument4 pagesBank A and B - Bank XSoleil SierraNo ratings yet

- Tugas 5 - InventoryDocument11 pagesTugas 5 - InventoryMuhammad RochimNo ratings yet

- Adam's Learning Centre, Lahore: Interpretation of Financial StatementsDocument10 pagesAdam's Learning Centre, Lahore: Interpretation of Financial StatementsMasood Ahmad AadamNo ratings yet

- Adam's Learning Centre, Lahore: Interpretation of Financial StatementsDocument10 pagesAdam's Learning Centre, Lahore: Interpretation of Financial StatementsMasood Ahmad AadamNo ratings yet

- Start-Up Costs Start-Up Assets: Emergency Funds MiscellaneousDocument4 pagesStart-Up Costs Start-Up Assets: Emergency Funds MiscellaneousJudith Atienza HugoNo ratings yet

- Financial Analysis LiquidityDocument22 pagesFinancial Analysis LiquidityRochelle ArpilledaNo ratings yet

- CONFRA2Document5 pagesCONFRA2Pia ChanNo ratings yet

- Far (Semestral Project)Document5 pagesFar (Semestral Project)Diana Rose RioNo ratings yet

- Activity-1 Unit 2 Financial Analysis 3BSA-1Document4 pagesActivity-1 Unit 2 Financial Analysis 3BSA-1JonellNo ratings yet

- Activity-1 Unit 2 Financial Analysis 3BSA-1Document4 pagesActivity-1 Unit 2 Financial Analysis 3BSA-1JonellNo ratings yet

- Assets 2018 2019 Forecast: Balance SheetDocument12 pagesAssets 2018 2019 Forecast: Balance SheetJosephAmparoNo ratings yet

- Horizonatal & Vertical Analysis and RatiosDocument6 pagesHorizonatal & Vertical Analysis and RatiosNicole AlexandraNo ratings yet

- Income Statement - Bells Manufacturing Year Ending December 31, 2015Document12 pagesIncome Statement - Bells Manufacturing Year Ending December 31, 2015Elif TuncaNo ratings yet

- Project PDA Conch Republic: Ebit 13,000,000 9,300,000Document4 pagesProject PDA Conch Republic: Ebit 13,000,000 9,300,000Harsya FitrioNo ratings yet

- Vertical Analysis SolutionsDocument5 pagesVertical Analysis SolutionsSamer IsmaelNo ratings yet

- DONE BA 118.3 Module 2 Quiz 1answer KeyDocument8 pagesDONE BA 118.3 Module 2 Quiz 1answer KeyRed Ashley De LeonNo ratings yet

- Comprehensive AccountingDocument5 pagesComprehensive AccountingAnn Kea GuillepaNo ratings yet

- Problem 1: P Company and Subsidiary Consolidated Working Paper Year Ended December 31, 2017Document6 pagesProblem 1: P Company and Subsidiary Consolidated Working Paper Year Ended December 31, 2017Vincent FrancoNo ratings yet

- Intl Business Machines Corp ComDocument6 pagesIntl Business Machines Corp Comluisa Fernanda PeñaNo ratings yet

- Intl Business Machines Corp ComDocument6 pagesIntl Business Machines Corp Comluisa Fernanda PeñaNo ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Micro (Scope Is On An Individual Level) and MacroDocument3 pagesMicro (Scope Is On An Individual Level) and MacroKarysse Arielle Noel JalaoNo ratings yet

- SW IV Answer Key PDFDocument4 pagesSW IV Answer Key PDFKarysse Arielle Noel JalaoNo ratings yet

- Managerial Econ LessonDocument14 pagesManagerial Econ LessonKarysse Arielle Noel JalaoNo ratings yet

- SD5 Financial Statement AnalysisDocument7 pagesSD5 Financial Statement AnalysisKarysse Arielle Noel JalaoNo ratings yet

- Reviewer PDFDocument9 pagesReviewer PDFKarysse Arielle Noel Jalao100% (1)

- Chapter 3. The Accounting EquationDocument2 pagesChapter 3. The Accounting EquationKarysse Arielle Noel JalaoNo ratings yet

- The Accounting Equation: Current Assets Are Assets That Can BeDocument3 pagesThe Accounting Equation: Current Assets Are Assets That Can BeKarysse Arielle Noel JalaoNo ratings yet

- RTFDocument14 pagesRTFKarysse Arielle Noel JalaoNo ratings yet

- Chapter 2 - HandoutsDocument9 pagesChapter 2 - HandoutsKarysse Arielle Noel JalaoNo ratings yet

- Chapter 3. The Accounting EquationDocument2 pagesChapter 3. The Accounting EquationKarysse Arielle Noel JalaoNo ratings yet

- Tutorial Chapter 1 Hand OutDocument3 pagesTutorial Chapter 1 Hand OutKarysse Arielle Noel JalaoNo ratings yet

- Accounting Cycle GuideDocument18 pagesAccounting Cycle GuideKarysse Arielle Noel JalaoNo ratings yet

- Math ModDocument4 pagesMath ModKarysse Arielle Noel JalaoNo ratings yet

- IFRS 9 PIR - EFRAG Final Comment Letter - 28 January 2022Document38 pagesIFRS 9 PIR - EFRAG Final Comment Letter - 28 January 2022Mikel MinasNo ratings yet

- Case 1 Ultratech-Cement-Ltd-Shareholders-Dilemma-About-Inorganic-GrowthDocument15 pagesCase 1 Ultratech-Cement-Ltd-Shareholders-Dilemma-About-Inorganic-Growthchauhantanisha0110No ratings yet

- FIN 081 - P2 Quiz2Document55 pagesFIN 081 - P2 Quiz2Grazielle DiazNo ratings yet

- NPV IRR ExplainedDocument8 pagesNPV IRR ExplainedkumarnramNo ratings yet

- Reits in The Philippines: A Presentation To The Trading Participants of The Philippine Stock Exchange (PSE)Document27 pagesReits in The Philippines: A Presentation To The Trading Participants of The Philippine Stock Exchange (PSE)Ron FabiNo ratings yet

- Gencer Energy Financials Excel Sheet UpdateDocument26 pagesGencer Energy Financials Excel Sheet UpdateRAJNo ratings yet

- AStudyon Working Capital Management Efficiencyof TCSIndias Top 1 CompanyDocument13 pagesAStudyon Working Capital Management Efficiencyof TCSIndias Top 1 CompanySUNDAR PNo ratings yet

- Stock Statement Kunnel March-23Document5 pagesStock Statement Kunnel March-23Vinoop OkvNo ratings yet

- FBNBank Ghana Limited 3rd Quarter Financial Statement (2021)Document1 pageFBNBank Ghana Limited 3rd Quarter Financial Statement (2021)Fuaad DodooNo ratings yet

- Part 1 - Financial Statements AnalysisDocument38 pagesPart 1 - Financial Statements AnalysisAjmal KhanNo ratings yet

- Philip VerlegerDocument5 pagesPhilip VerlegerAlfredo Jalife RahmeNo ratings yet

- 2 4 RevaluationDocument29 pages2 4 RevaluationFe ValenciaNo ratings yet

- Lista Libri GannDocument14 pagesLista Libri Ganndavetrader50% (2)

- Cash Flow StatementDocument18 pagesCash Flow StatementSriram BastolaNo ratings yet

- Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDocument94 pagesPrepared by Coby Harmon University of California, Santa Barbara Westmont CollegeBertoniNo ratings yet

- Chapter 15 The Term Structure of Interest Rates A. Yield-To-MaturityDocument6 pagesChapter 15 The Term Structure of Interest Rates A. Yield-To-MaturityGauravNo ratings yet

- AMD AssignmentDocument4 pagesAMD Assignment234ss 567ppNo ratings yet

- Accounting Ratio - WPS OfficeDocument6 pagesAccounting Ratio - WPS OfficeRommel SalagubangNo ratings yet

- ACFN 631 Self - Test Question No 4 PDFDocument3 pagesACFN 631 Self - Test Question No 4 PDFEsubalew GinbarNo ratings yet

- Working Capital - Synopsis-2022-23Document19 pagesWorking Capital - Synopsis-2022-23archana bagal100% (1)

- DR1Document81 pagesDR1Rushabh BhandariNo ratings yet

- Dividend TheoriesDocument22 pagesDividend TheoriesRadhakrishna Mishra100% (1)

- CIB Derivative WhitePaper 293301Document4 pagesCIB Derivative WhitePaper 293301shih_kaichihNo ratings yet

- Working Capital ManagementDocument2 pagesWorking Capital ManagementNguyễn Trần Hoàng YếnNo ratings yet

- Case 8. The Company Provided The Following InformationDocument2 pagesCase 8. The Company Provided The Following InformationVannesaNo ratings yet

- SSRN Id4338175Document163 pagesSSRN Id4338175Kartik RatheeNo ratings yet

Download as docx, pdf, or txt

You might also like

- Magsino Hannah Florence Activity 5 Discounted Cash FlowsDocument36 pagesMagsino Hannah Florence Activity 5 Discounted Cash FlowsKathyrine Claire Edrolin100% (2)

- Keith J Cunningham - Financial LiteracyDocument5 pagesKeith J Cunningham - Financial Literacykoetjinsiong100% (4)

- Bharat Chemicals Ltd. SolnDocument4 pagesBharat Chemicals Ltd. SolnJayash KaushalNo ratings yet

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- Sep 27 - Practice Problems On ValuationDocument2 pagesSep 27 - Practice Problems On ValuationMost. Amina KhatunNo ratings yet

- Black BookDocument85 pagesBlack BookRamesh Yadav100% (1)

- Exercises FSDocument6 pagesExercises FSDIVINE GRACE ROSALESNo ratings yet

- Peoria COperation - Cash Flow StatementDocument8 pagesPeoria COperation - Cash Flow StatementcbarajNo ratings yet

- Analysis and Interpretation of FS-Part 1Document2 pagesAnalysis and Interpretation of FS-Part 1Rhea RamirezNo ratings yet

- Internal Test - 2 - FSA - QuestionDocument3 pagesInternal Test - 2 - FSA - QuestionSandeep Choudhary40% (5)

- Technical Analysis of Stocks Commodities 2018 No 07 PDFDocument64 pagesTechnical Analysis of Stocks Commodities 2018 No 07 PDFs9298100% (1)

- Fsa Questions and SolutionsDocument11 pagesFsa Questions and SolutionsAnjali Betala KothariNo ratings yet

- Comparative Income Statement of Star Company For 2016-2018 Star Company Comparative Income Statement December 31, 2016,2017 and 2018Document5 pagesComparative Income Statement of Star Company For 2016-2018 Star Company Comparative Income Statement December 31, 2016,2017 and 2018JonellNo ratings yet

- Top Down Ebit Tax Rate Nopat 6600: Net Sales 100,000Document2 pagesTop Down Ebit Tax Rate Nopat 6600: Net Sales 100,000Jayash KaushalNo ratings yet

- 201B 201A Peso Change % ChangeDocument4 pages201B 201A Peso Change % ChangeNin JahNo ratings yet

- Task Performance I. Horizontal AnalysisDocument3 pagesTask Performance I. Horizontal AnalysisarisuNo ratings yet

- Assignment N3Document12 pagesAssignment N3Maiko KopadzeNo ratings yet

- Homework N3Document24 pagesHomework N3Maiko KopadzeNo ratings yet

- Question No 1: A-Gross PayDocument6 pagesQuestion No 1: A-Gross PayArmaghan Ali MalikNo ratings yet

- Financial Statement: Balance SheetDocument2 pagesFinancial Statement: Balance SheetChara etangNo ratings yet

- Chapter Five Format and ExampleDocument8 pagesChapter Five Format and Examplechris mutungaNo ratings yet

- Inbound 578213835412696153Document2 pagesInbound 578213835412696153Joppel PrescoNo ratings yet

- 20201015012755Document57 pages20201015012755hasharawanNo ratings yet

- Assgnmnt 2 FIN658Document5 pagesAssgnmnt 2 FIN658markNo ratings yet

- Pricewell Single Entity Financial StatementsDocument6 pagesPricewell Single Entity Financial StatementsBig SmutNo ratings yet

- Cortez Exam in Business FinanceDocument4 pagesCortez Exam in Business FinanceFranchesca CortezNo ratings yet

- 8-9 Mecca Copy Budget Balance SheetDocument5 pages8-9 Mecca Copy Budget Balance SheetAli Hassan SukheraNo ratings yet

- 5110WA7 FinancialsDocument1 page5110WA7 FinancialsAhmed EzzNo ratings yet

- 5.ratio Analysis SumsDocument9 pages5.ratio Analysis Sumsvinay kumar nuwalNo ratings yet

- AFAR2 CH. 3 - Problem Quiz 1Document19 pagesAFAR2 CH. 3 - Problem Quiz 1Von Andrei MedinaNo ratings yet

- BTAXREV ACT 184 Week 3 Income Taxation - Tax ReturnsDocument21 pagesBTAXREV ACT 184 Week 3 Income Taxation - Tax ReturnsgatotkaNo ratings yet

- Intercompany Sale of PPE Problem 2: Requirement: January 1, 20x4Document31 pagesIntercompany Sale of PPE Problem 2: Requirement: January 1, 20x4Abegail LibreaNo ratings yet

- Model Scheme IS CFS Fcfe BS Irr Coc NPV/DCF Development ScheduleDocument11 pagesModel Scheme IS CFS Fcfe BS Irr Coc NPV/DCF Development ScheduleMilind VatsiNo ratings yet

- Horizontal and Vertical AnalysisDocument4 pagesHorizontal and Vertical AnalysisJasmine ActaNo ratings yet

- Quiz BusFinHVRJULIANA VILLANUEVA ABM201-1Document10 pagesQuiz BusFinHVRJULIANA VILLANUEVA ABM201-1Juliana Angela VillanuevaNo ratings yet

- Illustration For Financial Analysis Using RatioDocument2 pagesIllustration For Financial Analysis Using RatioamahaktNo ratings yet

- Financial Management Week 2 AssignmentDocument2 pagesFinancial Management Week 2 AssignmentAndrea Monique AlejagaNo ratings yet

- Cash Flow HomeworkDocument2 pagesCash Flow HomeworkMyron BrandwineNo ratings yet

- 5,655.00 Additional Investment Needed/financingDocument23 pages5,655.00 Additional Investment Needed/financingMPCINo ratings yet

- Analysis and Interpretation of Financial StatementsDocument24 pagesAnalysis and Interpretation of Financial StatementsMariel NatullaNo ratings yet

- P and L and BSDocument8 pagesP and L and BSgautam48128No ratings yet

- Võ Thành Thắng - 31211024016 - NFGDocument28 pagesVõ Thành Thắng - 31211024016 - NFGtungphan.31211023431No ratings yet

- Tut 8 - Management AccountingDocument29 pagesTut 8 - Management AccountingTao LoheNo ratings yet

- Bank A and B - Bank XDocument4 pagesBank A and B - Bank XSoleil SierraNo ratings yet

- Tugas 5 - InventoryDocument11 pagesTugas 5 - InventoryMuhammad RochimNo ratings yet

- Adam's Learning Centre, Lahore: Interpretation of Financial StatementsDocument10 pagesAdam's Learning Centre, Lahore: Interpretation of Financial StatementsMasood Ahmad AadamNo ratings yet

- Adam's Learning Centre, Lahore: Interpretation of Financial StatementsDocument10 pagesAdam's Learning Centre, Lahore: Interpretation of Financial StatementsMasood Ahmad AadamNo ratings yet

- Start-Up Costs Start-Up Assets: Emergency Funds MiscellaneousDocument4 pagesStart-Up Costs Start-Up Assets: Emergency Funds MiscellaneousJudith Atienza HugoNo ratings yet

- Financial Analysis LiquidityDocument22 pagesFinancial Analysis LiquidityRochelle ArpilledaNo ratings yet

- CONFRA2Document5 pagesCONFRA2Pia ChanNo ratings yet

- Far (Semestral Project)Document5 pagesFar (Semestral Project)Diana Rose RioNo ratings yet

- Activity-1 Unit 2 Financial Analysis 3BSA-1Document4 pagesActivity-1 Unit 2 Financial Analysis 3BSA-1JonellNo ratings yet

- Activity-1 Unit 2 Financial Analysis 3BSA-1Document4 pagesActivity-1 Unit 2 Financial Analysis 3BSA-1JonellNo ratings yet

- Assets 2018 2019 Forecast: Balance SheetDocument12 pagesAssets 2018 2019 Forecast: Balance SheetJosephAmparoNo ratings yet

- Horizonatal & Vertical Analysis and RatiosDocument6 pagesHorizonatal & Vertical Analysis and RatiosNicole AlexandraNo ratings yet

- Income Statement - Bells Manufacturing Year Ending December 31, 2015Document12 pagesIncome Statement - Bells Manufacturing Year Ending December 31, 2015Elif TuncaNo ratings yet

- Project PDA Conch Republic: Ebit 13,000,000 9,300,000Document4 pagesProject PDA Conch Republic: Ebit 13,000,000 9,300,000Harsya FitrioNo ratings yet

- Vertical Analysis SolutionsDocument5 pagesVertical Analysis SolutionsSamer IsmaelNo ratings yet

- DONE BA 118.3 Module 2 Quiz 1answer KeyDocument8 pagesDONE BA 118.3 Module 2 Quiz 1answer KeyRed Ashley De LeonNo ratings yet

- Comprehensive AccountingDocument5 pagesComprehensive AccountingAnn Kea GuillepaNo ratings yet

- Problem 1: P Company and Subsidiary Consolidated Working Paper Year Ended December 31, 2017Document6 pagesProblem 1: P Company and Subsidiary Consolidated Working Paper Year Ended December 31, 2017Vincent FrancoNo ratings yet

- Intl Business Machines Corp ComDocument6 pagesIntl Business Machines Corp Comluisa Fernanda PeñaNo ratings yet

- Intl Business Machines Corp ComDocument6 pagesIntl Business Machines Corp Comluisa Fernanda PeñaNo ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Micro (Scope Is On An Individual Level) and MacroDocument3 pagesMicro (Scope Is On An Individual Level) and MacroKarysse Arielle Noel JalaoNo ratings yet

- SW IV Answer Key PDFDocument4 pagesSW IV Answer Key PDFKarysse Arielle Noel JalaoNo ratings yet

- Managerial Econ LessonDocument14 pagesManagerial Econ LessonKarysse Arielle Noel JalaoNo ratings yet

- SD5 Financial Statement AnalysisDocument7 pagesSD5 Financial Statement AnalysisKarysse Arielle Noel JalaoNo ratings yet

- Reviewer PDFDocument9 pagesReviewer PDFKarysse Arielle Noel Jalao100% (1)

- Chapter 3. The Accounting EquationDocument2 pagesChapter 3. The Accounting EquationKarysse Arielle Noel JalaoNo ratings yet

- The Accounting Equation: Current Assets Are Assets That Can BeDocument3 pagesThe Accounting Equation: Current Assets Are Assets That Can BeKarysse Arielle Noel JalaoNo ratings yet

- RTFDocument14 pagesRTFKarysse Arielle Noel JalaoNo ratings yet

- Chapter 2 - HandoutsDocument9 pagesChapter 2 - HandoutsKarysse Arielle Noel JalaoNo ratings yet

- Chapter 3. The Accounting EquationDocument2 pagesChapter 3. The Accounting EquationKarysse Arielle Noel JalaoNo ratings yet

- Tutorial Chapter 1 Hand OutDocument3 pagesTutorial Chapter 1 Hand OutKarysse Arielle Noel JalaoNo ratings yet

- Accounting Cycle GuideDocument18 pagesAccounting Cycle GuideKarysse Arielle Noel JalaoNo ratings yet

- Math ModDocument4 pagesMath ModKarysse Arielle Noel JalaoNo ratings yet

- IFRS 9 PIR - EFRAG Final Comment Letter - 28 January 2022Document38 pagesIFRS 9 PIR - EFRAG Final Comment Letter - 28 January 2022Mikel MinasNo ratings yet

- Case 1 Ultratech-Cement-Ltd-Shareholders-Dilemma-About-Inorganic-GrowthDocument15 pagesCase 1 Ultratech-Cement-Ltd-Shareholders-Dilemma-About-Inorganic-Growthchauhantanisha0110No ratings yet

- FIN 081 - P2 Quiz2Document55 pagesFIN 081 - P2 Quiz2Grazielle DiazNo ratings yet

- NPV IRR ExplainedDocument8 pagesNPV IRR ExplainedkumarnramNo ratings yet

- Reits in The Philippines: A Presentation To The Trading Participants of The Philippine Stock Exchange (PSE)Document27 pagesReits in The Philippines: A Presentation To The Trading Participants of The Philippine Stock Exchange (PSE)Ron FabiNo ratings yet

- Gencer Energy Financials Excel Sheet UpdateDocument26 pagesGencer Energy Financials Excel Sheet UpdateRAJNo ratings yet

- AStudyon Working Capital Management Efficiencyof TCSIndias Top 1 CompanyDocument13 pagesAStudyon Working Capital Management Efficiencyof TCSIndias Top 1 CompanySUNDAR PNo ratings yet

- Stock Statement Kunnel March-23Document5 pagesStock Statement Kunnel March-23Vinoop OkvNo ratings yet

- FBNBank Ghana Limited 3rd Quarter Financial Statement (2021)Document1 pageFBNBank Ghana Limited 3rd Quarter Financial Statement (2021)Fuaad DodooNo ratings yet

- Part 1 - Financial Statements AnalysisDocument38 pagesPart 1 - Financial Statements AnalysisAjmal KhanNo ratings yet

- Philip VerlegerDocument5 pagesPhilip VerlegerAlfredo Jalife RahmeNo ratings yet

- 2 4 RevaluationDocument29 pages2 4 RevaluationFe ValenciaNo ratings yet

- Lista Libri GannDocument14 pagesLista Libri Ganndavetrader50% (2)

- Cash Flow StatementDocument18 pagesCash Flow StatementSriram BastolaNo ratings yet

- Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDocument94 pagesPrepared by Coby Harmon University of California, Santa Barbara Westmont CollegeBertoniNo ratings yet

- Chapter 15 The Term Structure of Interest Rates A. Yield-To-MaturityDocument6 pagesChapter 15 The Term Structure of Interest Rates A. Yield-To-MaturityGauravNo ratings yet

- AMD AssignmentDocument4 pagesAMD Assignment234ss 567ppNo ratings yet

- Accounting Ratio - WPS OfficeDocument6 pagesAccounting Ratio - WPS OfficeRommel SalagubangNo ratings yet

- ACFN 631 Self - Test Question No 4 PDFDocument3 pagesACFN 631 Self - Test Question No 4 PDFEsubalew GinbarNo ratings yet

- Working Capital - Synopsis-2022-23Document19 pagesWorking Capital - Synopsis-2022-23archana bagal100% (1)

- DR1Document81 pagesDR1Rushabh BhandariNo ratings yet

- Dividend TheoriesDocument22 pagesDividend TheoriesRadhakrishna Mishra100% (1)

- CIB Derivative WhitePaper 293301Document4 pagesCIB Derivative WhitePaper 293301shih_kaichihNo ratings yet

- Working Capital ManagementDocument2 pagesWorking Capital ManagementNguyễn Trần Hoàng YếnNo ratings yet

- Case 8. The Company Provided The Following InformationDocument2 pagesCase 8. The Company Provided The Following InformationVannesaNo ratings yet

- SSRN Id4338175Document163 pagesSSRN Id4338175Kartik RatheeNo ratings yet