Download as pdf or txt

You might also like

- Digital Communications A Discrete-Time Approach Rice M. 2009 Solution ManualDocument539 pagesDigital Communications A Discrete-Time Approach Rice M. 2009 Solution ManualPeter Smith57% (7)

- Advanced Level Pure Mathematics TranterDocument473 pagesAdvanced Level Pure Mathematics TranterDilan Harindra100% (3)

- Two Coupled PendulumsDocument10 pagesTwo Coupled PendulumsBilal HaiderNo ratings yet

- Graphing Rational Functions Ws - Docx 2Document4 pagesGraphing Rational Functions Ws - Docx 2محمد أحمد عبدالوهاب محمدNo ratings yet

- Lesson Plan Inverse ProportionDocument1 pageLesson Plan Inverse ProportionJonathan Robinson100% (5)

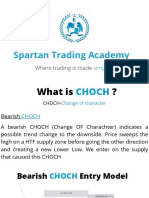

- What Is Choch - Spartan Trading AcademyDocument12 pagesWhat Is Choch - Spartan Trading AcademyabimalainNo ratings yet

- Finite Element Method For Structural Dynamic and Stability AnalysesDocument45 pagesFinite Element Method For Structural Dynamic and Stability AnalysesabimalainNo ratings yet

- The Newmark Method: T T U T U T TDocument6 pagesThe Newmark Method: T T U T U T TanirbanNo ratings yet

- Solution of Equilibrium Equations in Dynamic AnalysisDocument56 pagesSolution of Equilibrium Equations in Dynamic AnalysisUlul AzmyNo ratings yet

- Module 3 PDFDocument39 pagesModule 3 PDFSruti SuhasariaNo ratings yet

- Boyce de 10e PPT Ch03 6 FinalDocument9 pagesBoyce de 10e PPT Ch03 6 FinalphakphumNo ratings yet

- 24.3.6 - Variation of Parameters Second OrderDocument11 pages24.3.6 - Variation of Parameters Second Orderanon_422073337No ratings yet

- Autocorrelation: y X U S Euu SDocument15 pagesAutocorrelation: y X U S Euu SRawad JumaaNo ratings yet

- Moment Generating FunctionsDocument10 pagesMoment Generating FunctionsupamaharikrishnanNo ratings yet

- State Transition MatrixDocument26 pagesState Transition MatrixmemotetoNo ratings yet

- Applied Mathematics and Computation: Guihua Zhao, Minghui Song, Zhanwen YangDocument12 pagesApplied Mathematics and Computation: Guihua Zhao, Minghui Song, Zhanwen YangJese MadridNo ratings yet

- Finite Element Method For Structural Dynamic and Stability AnalysesDocument48 pagesFinite Element Method For Structural Dynamic and Stability AnalysesabimalainNo ratings yet

- EVEN11Document37 pagesEVEN11David GMNo ratings yet

- Dougherty C12G06 2016 05 22Document31 pagesDougherty C12G06 2016 05 22rachmanmustafaNo ratings yet

- Ma GMM: Review Exercises For Chapter 11Document9 pagesMa GMM: Review Exercises For Chapter 11tadeitobelloNo ratings yet

- Hopf Bifurcation in A Partial Dependent Predator-Prey System With Delay Q Huitao Zhao 2009Document5 pagesHopf Bifurcation in A Partial Dependent Predator-Prey System With Delay Q Huitao Zhao 2009MeMu MeMuNo ratings yet

- Module 1 PDFDocument37 pagesModule 1 PDFSruti SuhasariaNo ratings yet

- A B C T Ut T C T C T Ut T C T X X XDocument6 pagesA B C T Ut T C T C T Ut T C T X X Xariella2mansfieldNo ratings yet

- E T P E T P T: T T T T TDocument130 pagesE T P E T P T: T T T T TAbdul RehmanNo ratings yet

- MIT2 092F09 Sol Exam2Document4 pagesMIT2 092F09 Sol Exam2RedRobynNo ratings yet

- Laplace TransformDocument7 pagesLaplace TransformiamheretohelpNo ratings yet

- Chapter 2 - Fourier TransformDocument31 pagesChapter 2 - Fourier TransformOgunyemi VictorNo ratings yet

- Homework EconometricsDocument7 pagesHomework EconometricstnthuyoanhNo ratings yet

- Chapter 3-2Document44 pagesChapter 3-2rawadNo ratings yet

- (Cdxd3.Com) Cong Thuc XSTKDocument9 pages(Cdxd3.Com) Cong Thuc XSTKYNo ratings yet

- Autocorrelation (Lec 12) : 1 Nguyen Thu Hang, BMNV, FTU CS2Document52 pagesAutocorrelation (Lec 12) : 1 Nguyen Thu Hang, BMNV, FTU CS2HATNo ratings yet

- Handout Time Series For Sem II 2020 PDFDocument24 pagesHandout Time Series For Sem II 2020 PDFAkanksha DeyNo ratings yet

- Tutorial 4Document5 pagesTutorial 4Nornis DalinaNo ratings yet

- Signals and Systems: CE/EE301Document9 pagesSignals and Systems: CE/EE301Abdelrhman MahfouzNo ratings yet

- Lecture 14Document5 pagesLecture 14Yamaneko ShinNo ratings yet

- Tutorial 2Document2 pagesTutorial 2Nornis DalinaNo ratings yet

- Stochastic Diff Eq PDFDocument44 pagesStochastic Diff Eq PDFAntoni Torrents OdinNo ratings yet

- Dom Q2Document18 pagesDom Q2Arjun Giri NairNo ratings yet

- Time Integration Fundamentals For ClassDocument50 pagesTime Integration Fundamentals For ClasscucrasNo ratings yet

- CochraneDocument10 pagesCochraneMounica ToletiNo ratings yet

- Cluster ExpansionsDocument38 pagesCluster ExpansionsgrossogrossoNo ratings yet

- KNNL Ch12Document10 pagesKNNL Ch12Artur GiesteiraNo ratings yet

- Numerical Analysis SolutionDocument14 pagesNumerical Analysis SolutionDr Olayinka Okeola50% (2)

- Articulo de Pendulo DobleDocument6 pagesArticulo de Pendulo DobleamaflabNo ratings yet

- 2.super Position of Periodic MotionsDocument47 pages2.super Position of Periodic Motionsvsnmurthy1No ratings yet

- Curves in SpaceDocument10 pagesCurves in SpaceJohn ManciaNo ratings yet

- Bode, Polar & Nyquist Plot NotesDocument47 pagesBode, Polar & Nyquist Plot NotesMitul YadavNo ratings yet

- Discrete Random Variables and Probability DistributionsDocument36 pagesDiscrete Random Variables and Probability DistributionsBeverly PamanNo ratings yet

- Nonlinear Optics Lecture 6Document16 pagesNonlinear Optics Lecture 6t8enedNo ratings yet

- 278 Assignment 3Document10 pages278 Assignment 3NiharNo ratings yet

- Analyzing Insertion Sort As A Recursive AlgorithmDocument10 pagesAnalyzing Insertion Sort As A Recursive AlgorithmHehe 'Heny' CaemNo ratings yet

- Ss TheoryDocument5 pagesSs TheoryKIRAN LOKHANDENo ratings yet

- 3.1 Time-Domain Analysis of Control Systems: Unit-IiiDocument23 pages3.1 Time-Domain Analysis of Control Systems: Unit-IiiRajasekhar AtlaNo ratings yet

- Lecture 05 Analysis (I) Time Response and State Transition MatrixDocument33 pagesLecture 05 Analysis (I) Time Response and State Transition MatrixSanjana VijayakumarNo ratings yet

- Com Solutions ManualDocument966 pagesCom Solutions ManualbrooksNo ratings yet

- GT-17 KeyDocument18 pagesGT-17 KeyRubini SureshNo ratings yet

- Linear Independence and The Wronskian: F and G Are Multiples of Each OtherDocument27 pagesLinear Independence and The Wronskian: F and G Are Multiples of Each OtherDimuthu DharshanaNo ratings yet

- MAT351T WR2 2014A MemoDocument3 pagesMAT351T WR2 2014A MemoMduduzi Magiva MahlanguNo ratings yet

- 1C09-08 Design For Seismic and Climate ChangesDocument31 pages1C09-08 Design For Seismic and Climate ChangesSanketWadgaonkarNo ratings yet

- Ece 232 Discrete-Time Signals and Systems Solved Problems I: DT e T X T C and e C T XDocument4 pagesEce 232 Discrete-Time Signals and Systems Solved Problems I: DT e T X T C and e C T XistegNo ratings yet

- 2011 III Examen II Algebra LinealDocument7 pages2011 III Examen II Algebra LinealWalter VelásquezNo ratings yet

- Part - A: Ext X Extxt RDocument22 pagesPart - A: Ext X Extxt RSneghaa PNo ratings yet

- HW10, Hooman KargarDocument12 pagesHW10, Hooman KargarabimalainNo ratings yet

- Nag 1610190805Document8 pagesNag 1610190805abimalainNo ratings yet

- X X X X A X: Onlinear OscillationsDocument1 pageX X X X A X: Onlinear OscillationsabimalainNo ratings yet

- ProgSpec-H2A1 H2A2 H2A3 H2U5-2021-22Document16 pagesProgSpec-H2A1 H2A2 H2A3 H2U5-2021-22abimalainNo ratings yet

- Sample DamDocument48 pagesSample DamabimalainNo ratings yet

- Sample Dam BDocument66 pagesSample Dam BabimalainNo ratings yet

- Lesson 06 2015Document52 pagesLesson 06 2015abimalainNo ratings yet

- Sample Dam BDocument67 pagesSample Dam BabimalainNo ratings yet

- Lesson 07 2015Document69 pagesLesson 07 2015abimalainNo ratings yet

- Lesson 10 2015Document102 pagesLesson 10 2015abimalainNo ratings yet

- Lesson 09 2015Document44 pagesLesson 09 2015abimalainNo ratings yet

- Lecture Notes On Non Linear VibrationsDocument154 pagesLecture Notes On Non Linear VibrationsabimalainNo ratings yet

- Stability Chapter 03Document14 pagesStability Chapter 03abimalainNo ratings yet

- Assignment 2 2016Document2 pagesAssignment 2 2016abimalainNo ratings yet

- 2015 Lesson07 Example 1Document70 pages2015 Lesson07 Example 1abimalainNo ratings yet

- Lesson 03 2015Document48 pagesLesson 03 2015abimalainNo ratings yet

- CEE 9571 - Advanced Concrete TechnologyDocument3 pagesCEE 9571 - Advanced Concrete TechnologyabimalainNo ratings yet

- Stability Chapter 05Document8 pagesStability Chapter 05abimalainNo ratings yet

- 2015 Lesson06 Example1Document7 pages2015 Lesson06 Example1abimalainNo ratings yet

- 2015 Lesson06 Example4Document37 pages2015 Lesson06 Example4abimalainNo ratings yet

- Imbalance Vs Balanced Price Action by SpartantradingacademyDocument11 pagesImbalance Vs Balanced Price Action by SpartantradingacademyabimalainNo ratings yet

- 3 Important ORDER BLOCK Rules SpartantradingacademyDocument9 pages3 Important ORDER BLOCK Rules SpartantradingacademyabimalainNo ratings yet

- Applsci 11 03213 v2Document17 pagesApplsci 11 03213 v2abimalainNo ratings yet

- Session 15-WTC PPT (Apr 15, 2019)Document27 pagesSession 15-WTC PPT (Apr 15, 2019)abimalainNo ratings yet

- Session 13-WTC PPT (Apr 01, 2019)Document30 pagesSession 13-WTC PPT (Apr 01, 2019)abimalainNo ratings yet

- Recursive Algorithms and Recurrence EquationsDocument5 pagesRecursive Algorithms and Recurrence EquationsAmogh VaishnavNo ratings yet

- 7th Math WorkbookDocument234 pages7th Math WorkbookAchin MmalhotraNo ratings yet

- DiBenedetto 2002 Real AnalysisDocument505 pagesDiBenedetto 2002 Real AnalysisLucas Venâncio da Silva SantosNo ratings yet

- Grade 7 Division Finals QuestionsDocument2 pagesGrade 7 Division Finals QuestionsJasmin And - Angie97% (35)

- G251ex1 (Fa05) Kinetics of The Persulfate-Iodine Clock ReactionDocument10 pagesG251ex1 (Fa05) Kinetics of The Persulfate-Iodine Clock ReactionhungNo ratings yet

- Conic Sections and CirclesDocument19 pagesConic Sections and Circlesapi-339611548No ratings yet

- Kelompok 2 SPLDV (English) (1) REVISIDocument41 pagesKelompok 2 SPLDV (English) (1) REVISIrafirudin CRNo ratings yet

- Algebra 2 Part 1 PresentationDocument101 pagesAlgebra 2 Part 1 PresentationLeo Jun G. AlcalaNo ratings yet

- Midterm 1ADocument5 pagesMidterm 1AMicki BuiNo ratings yet

- Gradient, Divergence, and CurlDocument24 pagesGradient, Divergence, and CurlPekan Ilmiah MatematikaNo ratings yet

- Department of Education: Punta Integrated SchoolDocument4 pagesDepartment of Education: Punta Integrated SchoolRobelyn ManuelNo ratings yet

- Percentage DPP 03 (English)Document4 pagesPercentage DPP 03 (English)Jaya VatsNo ratings yet

- Digital Signal Processing - U4Document82 pagesDigital Signal Processing - U4Ashok BattulaNo ratings yet

- PDE 2nd Sem QPDocument14 pagesPDE 2nd Sem QPOprudhNo ratings yet

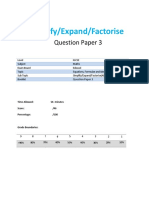

- Simplify/Expand/Factorise: Question Paper 3Document9 pagesSimplify/Expand/Factorise: Question Paper 3Robin WongNo ratings yet

- Unit 3B Radical Expressions and Rational ExponentsDocument25 pagesUnit 3B Radical Expressions and Rational ExponentsJimmy Mandapat100% (1)

- Cheena Francesca Luciano - WORKSHEET Q2 WK 2Document4 pagesCheena Francesca Luciano - WORKSHEET Q2 WK 2Cheena Francesca LucianoNo ratings yet

- Math9 q1 Mod1of8 Illustrations-Of-Quadratic-Equations v2Document24 pagesMath9 q1 Mod1of8 Illustrations-Of-Quadratic-Equations v2Cotejo, Jasmin Erika C.0% (1)

- EC400 Revision Notes AllDocument94 pagesEC400 Revision Notes AllArjun VarmaNo ratings yet

- Number System Imp Question Paper 1Document1 pageNumber System Imp Question Paper 1vmehrotra301045No ratings yet

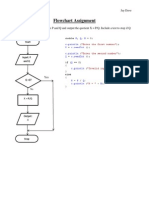

- Jay Dave Flowchart AssignmentDocument5 pagesJay Dave Flowchart Assignmentapi-225496804No ratings yet

- Lecture Notes On Cryptographic Boolean Functions: Anne CanteautDocument48 pagesLecture Notes On Cryptographic Boolean Functions: Anne CanteautJose Fabian Beltran JoyaNo ratings yet

- Solving by Graphing Systems of EquationsDocument6 pagesSolving by Graphing Systems of EquationsNilam Doctor100% (1)

- Copulas and Their AlternativesDocument9 pagesCopulas and Their AlternativesGary VenterNo ratings yet

- MA21/MAT201: RamaiahDocument3 pagesMA21/MAT201: RamaiahTsukasa EishiNo ratings yet

- 8 2 Polar GraphsDocument3 pages8 2 Polar GraphsRaisa RashidNo ratings yet

- Unit 3 Crit B QuestionsDocument11 pagesUnit 3 Crit B QuestionsNaani RajaNo ratings yet