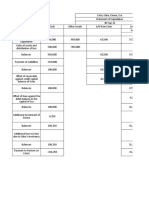

Instructions: Prepare A Statement of Partnership Liquidation

Instructions: Prepare A Statement of Partnership Liquidation

You might also like

- Chapter 7 - Assignment 2Document9 pagesChapter 7 - Assignment 2Gwen Stefani DaugdaugNo ratings yet

- Problem #1 Shares Issuance For Cash: Name: Section: ProfessorDocument14 pagesProblem #1 Shares Issuance For Cash: Name: Section: Professorkakao0% (3)

- SFM N21 Final QB - Atul AgarwalDocument449 pagesSFM N21 Final QB - Atul AgarwalSai VardhanNo ratings yet

- 2Document3 pages2Leinard AgcaoiliNo ratings yet

- Financial Accounting and ReportingDocument8 pagesFinancial Accounting and ReportingPauline Idra100% (1)

- Prelim AFAR 1Document6 pagesPrelim AFAR 1Chris Phil Dee75% (4)

- APC Ch6solDocument22 pagesAPC Ch6solAnonymous LusWvy100% (8)

- Exam Paper 2012 ZAB CommentariesDocument35 pagesExam Paper 2012 ZAB Commentariesamna666No ratings yet

- Partnership Liquidation - Lump-Sum Exercise 6-1Document23 pagesPartnership Liquidation - Lump-Sum Exercise 6-1Norleen Rose S. AguilarNo ratings yet

- MC 6 SolutionDocument16 pagesMC 6 SolutionkylaNo ratings yet

- Corporation Problems-1Document18 pagesCorporation Problems-1Avia Chelsy DeangNo ratings yet

- Win Ballada Parcor Chapter 4 ProblemDocument2 pagesWin Ballada Parcor Chapter 4 ProblemKrngyxNo ratings yet

- Requirement 1 Digos Trading Statement of Partnership Liquidation June 30, 20ADocument4 pagesRequirement 1 Digos Trading Statement of Partnership Liquidation June 30, 20AGvm Joy MagalingNo ratings yet

- Chapter 4Document5 pagesChapter 4Billy Vince AlquinoNo ratings yet

- Chapter 2Document27 pagesChapter 2Mary MarieNo ratings yet

- Miranda, Leon and EstoqueDocument1 pageMiranda, Leon and EstoqueHana0% (1)

- Part 2Document2 pagesPart 2PRETTYKONo ratings yet

- Liquidation 2Document3 pagesLiquidation 2Kenneth CuencaNo ratings yet

- Acp311 OperationDocument2 pagesAcp311 OperationAngeline Patac LumiguidNo ratings yet

- Henri Emanuel Reforba - Learning Task #2Document6 pagesHenri Emanuel Reforba - Learning Task #2Rhea BernabeNo ratings yet

- PARCOR - 2Nature-and-Formation-of-a-PartnershipDocument30 pagesPARCOR - 2Nature-and-Formation-of-a-PartnershipHarriane Mae GonzalesNo ratings yet

- Instructions: Compute The Amount of Ayesa's Capital Account at September 1, 2014Document10 pagesInstructions: Compute The Amount of Ayesa's Capital Account at September 1, 2014Nicole Fidelson0% (1)

- 1stLecture-Partnership LiquidationDocument25 pages1stLecture-Partnership LiquidationRechelle Dalusung100% (1)

- CHAPTER 16 - DIVIDENDS - Problem 3 - Computations - Page 597-599Document9 pagesCHAPTER 16 - DIVIDENDS - Problem 3 - Computations - Page 597-599Penelope PalconNo ratings yet

- CAlAMBA AND SANTIAGO - TUGOTDocument2 pagesCAlAMBA AND SANTIAGO - TUGOTAndrea Tugot100% (1)

- Quiz 2 For StudentsDocument4 pagesQuiz 2 For StudentsLorNo ratings yet

- Problem #9 Two Sole Proprietorship Form A PartnershipDocument3 pagesProblem #9 Two Sole Proprietorship Form A PartnershipNiño Rey LopezNo ratings yet

- MC With Answers Partnership Operation CorporationDocument19 pagesMC With Answers Partnership Operation CorporationASHLEY ROLAINE VICENTENo ratings yet

- MARVIN LISING Exercise 1 Installment Liquidation With Schedule of Safe PaymentsDocument5 pagesMARVIN LISING Exercise 1 Installment Liquidation With Schedule of Safe PaymentsMoon YoungheeNo ratings yet

- Parcor Proj (Version 1)Document45 pagesParcor Proj (Version 1)Jwhll MaeNo ratings yet

- Partnership Exercise 2Document5 pagesPartnership Exercise 2nikNo ratings yet

- Problem 20-23Document5 pagesProblem 20-23Teresa Pantallano DivinagraciaNo ratings yet

- Problem 6 1Document2 pagesProblem 6 1SerdenRoseNo ratings yet

- Chapter 7 Angel Ann E. Orola Bsba HR1 1Document90 pagesChapter 7 Angel Ann E. Orola Bsba HR1 1Gwen Stefani DaugdaugNo ratings yet

- Cfas ReviewerDocument7 pagesCfas ReviewerDarlene Angela IcasiamNo ratings yet

- Activity Partnership DissolutionDocument2 pagesActivity Partnership DissolutionKaren Joy Jacinto ElloNo ratings yet

- Solved Gloria Detoya and Esterlina Gevera Have Operated A Successful... - Course HeroDocument4 pagesSolved Gloria Detoya and Esterlina Gevera Have Operated A Successful... - Course HeroeannetiyabNo ratings yet

- Stephanie Calamba and Allan Brillantes SolutionDocument6 pagesStephanie Calamba and Allan Brillantes SolutionGerald RamiloNo ratings yet

- Parcor Chap 6 DoneDocument10 pagesParcor Chap 6 DoneJohn Carlo CastilloNo ratings yet

- ReviewerDocument15 pagesReviewerALMA MORENANo ratings yet

- ACCTG122 Homework On Partnership LiquidationDocument2 pagesACCTG122 Homework On Partnership LiquidationJoana TrinidadNo ratings yet

- P 2-1 (Cash and Net Assets Contributions)Document7 pagesP 2-1 (Cash and Net Assets Contributions)pjmerinNo ratings yet

- Accounting Midterm Exam (Partnership Up To Dissolution) : Answer: 103,500 346,500Document6 pagesAccounting Midterm Exam (Partnership Up To Dissolution) : Answer: 103,500 346,500JINKY MARIELLA VERGARA100% (1)

- Partnership Liquidation Exercises p.135Document6 pagesPartnership Liquidation Exercises p.135Kaye GomezNo ratings yet

- Incorrect: Discussion 7Document3 pagesIncorrect: Discussion 7Jasmine ActaNo ratings yet

- LiquidationDocument18 pagesLiquidationSamaica MontemayorNo ratings yet

- UntitledDocument4 pagesUntitledShevina Maghari shsnohsNo ratings yet

- CHAPTER 2 PartnershipDocument17 pagesCHAPTER 2 PartnershipLAZARO, Jaspher S.No ratings yet

- ParCor Chapter 5 - Hernandez - BSA 1-1 PDFDocument5 pagesParCor Chapter 5 - Hernandez - BSA 1-1 PDFBSA 1-1No ratings yet

- Accounting For PartnershipsDocument3 pagesAccounting For PartnershipsRixa Doreen Antoja50% (2)

- Chap 3 and 4 - ParcorDocument4 pagesChap 3 and 4 - ParcorAnne Gwynneth RadaNo ratings yet

- Par CorDocument27 pagesPar CorPam LlanetaNo ratings yet

- PROBLEMDocument3 pagesPROBLEMSam VNo ratings yet

- December 8 DiscussionDocument6 pagesDecember 8 DiscussionMark Domingo MendozaNo ratings yet

- Win Ballada Parcor Chapter 4 ProblemDocument2 pagesWin Ballada Parcor Chapter 4 ProblemKrngyxNo ratings yet

- Mara, Teri, and Rita Partnership Statement of Partnership Liquidation December 31, 2018Document6 pagesMara, Teri, and Rita Partnership Statement of Partnership Liquidation December 31, 2018Serenity CarlyeNo ratings yet

- MC6Document5 pagesMC6shudayeNo ratings yet

- Far QuizDocument7 pagesFar QuizMeldred EcatNo ratings yet

- Chapter 3 ParcorDocument6 pagesChapter 3 ParcorJwhll MaeNo ratings yet

- Parcor Proj (Version 1)Document33 pagesParcor Proj (Version 1)Jwhll MaeNo ratings yet

- APC Ch6solDocument25 pagesAPC Ch6solVaneza DayananNo ratings yet

- Partnership Liquidation - Lump-Sum Exercise 6-1Document23 pagesPartnership Liquidation - Lump-Sum Exercise 6-1ConnorNo ratings yet

- Partnership Liquidation Chap 6Document25 pagesPartnership Liquidation Chap 6Regine BaterisnaNo ratings yet

- Natural Obligations Study Guide I. DefinitionsDocument2 pagesNatural Obligations Study Guide I. DefinitionsLeinard AgcaoiliNo ratings yet

- Problem of The Week 1: AnswerDocument1 pageProblem of The Week 1: AnswerLeinard AgcaoiliNo ratings yet

- Takdang Gawain 4: Orihinal Na Akda: Boats in A StormDocument3 pagesTakdang Gawain 4: Orihinal Na Akda: Boats in A StormLeinard AgcaoiliNo ratings yet

- Chapter 4 (Section 2) Study Guide IDocument2 pagesChapter 4 (Section 2) Study Guide ILeinard AgcaoiliNo ratings yet

- Reflection PaperDocument2 pagesReflection PaperLeinard AgcaoiliNo ratings yet

- Chapter 4 (Section 1) Study Guide IDocument4 pagesChapter 4 (Section 1) Study Guide ILeinard AgcaoiliNo ratings yet

- Chapter 3 (Section 3) AGCAOILIDocument3 pagesChapter 3 (Section 3) AGCAOILILeinard AgcaoiliNo ratings yet

- Chapter 4 (Section 4) Study Guide IDocument2 pagesChapter 4 (Section 4) Study Guide ILeinard AgcaoiliNo ratings yet

- Chapter 3 (Section 1) Study Guide IDocument5 pagesChapter 3 (Section 1) Study Guide ILeinard AgcaoiliNo ratings yet

- Chapter 4 (Section 6) Study Guide IDocument2 pagesChapter 4 (Section 6) Study Guide ILeinard AgcaoiliNo ratings yet

- Chapter 4 (Section 3) Study Guide IDocument2 pagesChapter 4 (Section 3) Study Guide ILeinard AgcaoiliNo ratings yet

- Chapter 4 (Section 5) Study Guide IDocument2 pagesChapter 4 (Section 5) Study Guide ILeinard AgcaoiliNo ratings yet

- Study GuideDocument4 pagesStudy GuideLeinard AgcaoiliNo ratings yet

- ChapterDocument4 pagesChapterLeinard AgcaoiliNo ratings yet

- Contracts - Chapter 9Document2 pagesContracts - Chapter 9Leinard AgcaoiliNo ratings yet

- Chapter 2 (Section 2) Study Guide IDocument3 pagesChapter 2 (Section 2) Study Guide ILeinard AgcaoiliNo ratings yet

- Contracts - Chapter 2 (Section 3)Document2 pagesContracts - Chapter 2 (Section 3)Leinard AgcaoiliNo ratings yet

- Contracts - Chapter 8Document2 pagesContracts - Chapter 8Leinard AgcaoiliNo ratings yet

- Contracts - Chapter 3Document2 pagesContracts - Chapter 3Leinard AgcaoiliNo ratings yet

- Reflection Paper 2Document3 pagesReflection Paper 2Leinard AgcaoiliNo ratings yet

- Contracts - Chapter 7Document2 pagesContracts - Chapter 7Leinard AgcaoiliNo ratings yet

- Contracts - Chapter 2 (Section 1) AGCAOILIDocument3 pagesContracts - Chapter 2 (Section 1) AGCAOILILeinard AgcaoiliNo ratings yet

- Contracts - Chapter 2 (Section 2) AGCAOILIDocument2 pagesContracts - Chapter 2 (Section 2) AGCAOILILeinard AgcaoiliNo ratings yet

- Contracts - Chapter 1 AGCAOILIDocument2 pagesContracts - Chapter 1 AGCAOILILeinard Agcaoili100% (2)

- MFRS 1Document42 pagesMFRS 1hyraldNo ratings yet

- Branch Accounting ProblemDocument6 pagesBranch Accounting ProblemGONZALES, MICA ANGEL A.No ratings yet

- Case1 Big Bull CapitalDocument75 pagesCase1 Big Bull CapitalSakshi SharmaNo ratings yet

- RewiewerDocument34 pagesRewiewerMickaella VergaraNo ratings yet

- Business Administration Past PaperDocument23 pagesBusiness Administration Past PaperFahmeeda AhmedNo ratings yet

- WLCON 2022 17A Annual ReportDocument35 pagesWLCON 2022 17A Annual ReportJamaica AlejoNo ratings yet

- Cambridge Associates PE BenchmarksDocument11 pagesCambridge Associates PE BenchmarksDan Primack100% (1)

- Group 7: Country Report PresentationDocument51 pagesGroup 7: Country Report PresentationHà Anh NguyễnNo ratings yet

- UK Diabolo Manual-E05Document19 pagesUK Diabolo Manual-E05Eliott WalletNo ratings yet

- MIDTERM DRILL 1 TEST AnsweristsDocument6 pagesMIDTERM DRILL 1 TEST AnsweristsDan Andrei BongoNo ratings yet

- Chapter-4 Rectification of ErrorsDocument19 pagesChapter-4 Rectification of Errorslenovo lenovo100% (1)

- Does Shari'ah Screening Cause Abnormal Returns? Empirical Evidence From Islamic Equity IndicesDocument22 pagesDoes Shari'ah Screening Cause Abnormal Returns? Empirical Evidence From Islamic Equity IndicesJelena CientaNo ratings yet

- Keppel DC REIT - CircularDocument76 pagesKeppel DC REIT - Circulareuniceyl001No ratings yet

- FAR.3515_Cash_and_cash_equivalents_Document4 pagesFAR.3515_Cash_and_cash_equivalents_marlou mNo ratings yet

- Business and TechnologyDocument11 pagesBusiness and TechnologyBhaskar DasNo ratings yet

- Securities and Exchange Commission: Sec Form 17-A, As AmendedDocument4 pagesSecurities and Exchange Commission: Sec Form 17-A, As AmendedZinampan GarrijayNo ratings yet

- Adani Group - How The World's 3rd Richest Man Is Pulling The Largest Con in Corporate History - Hindenburg ResearchDocument147 pagesAdani Group - How The World's 3rd Richest Man Is Pulling The Largest Con in Corporate History - Hindenburg ResearchmanusolomonNo ratings yet

- Amity University Kolkata: Fundamentals of Financial ManagementDocument16 pagesAmity University Kolkata: Fundamentals of Financial ManagementSupratim RoychowdhuryNo ratings yet

- Mutual Funds ShivnadarDocument126 pagesMutual Funds ShivnadarKritika KoulNo ratings yet

- Balance Sheet of Maruti Suzuki IndiaDocument415 pagesBalance Sheet of Maruti Suzuki IndiaMahesh VaiShnavNo ratings yet

- Cash Flow Statement of AmulDocument6 pagesCash Flow Statement of AmulArav Sarin60% (5)

- CH 9. Working Capital and Tresury Mgt.Document5 pagesCH 9. Working Capital and Tresury Mgt.Tanvir PrantoNo ratings yet

- Reverse DCFDocument9 pagesReverse DCFjenkisanNo ratings yet

- Palepu - Chapter 5Document33 pagesPalepu - Chapter 5Dương Quốc TuấnNo ratings yet

- Concept Questions: Q.1. Payback Period and Net Present ValueDocument3 pagesConcept Questions: Q.1. Payback Period and Net Present Valuemiller jackNo ratings yet

- FAIS Assignment 1 - Mariam Jabbar PDFDocument4 pagesFAIS Assignment 1 - Mariam Jabbar PDFMariamNo ratings yet

Download as docx, pdf, or txt

You might also like

- Chapter 7 - Assignment 2Document9 pagesChapter 7 - Assignment 2Gwen Stefani DaugdaugNo ratings yet

- Problem #1 Shares Issuance For Cash: Name: Section: ProfessorDocument14 pagesProblem #1 Shares Issuance For Cash: Name: Section: Professorkakao0% (3)

- SFM N21 Final QB - Atul AgarwalDocument449 pagesSFM N21 Final QB - Atul AgarwalSai VardhanNo ratings yet

- 2Document3 pages2Leinard AgcaoiliNo ratings yet

- Financial Accounting and ReportingDocument8 pagesFinancial Accounting and ReportingPauline Idra100% (1)

- Prelim AFAR 1Document6 pagesPrelim AFAR 1Chris Phil Dee75% (4)

- APC Ch6solDocument22 pagesAPC Ch6solAnonymous LusWvy100% (8)

- Exam Paper 2012 ZAB CommentariesDocument35 pagesExam Paper 2012 ZAB Commentariesamna666No ratings yet

- Partnership Liquidation - Lump-Sum Exercise 6-1Document23 pagesPartnership Liquidation - Lump-Sum Exercise 6-1Norleen Rose S. AguilarNo ratings yet

- MC 6 SolutionDocument16 pagesMC 6 SolutionkylaNo ratings yet

- Corporation Problems-1Document18 pagesCorporation Problems-1Avia Chelsy DeangNo ratings yet

- Win Ballada Parcor Chapter 4 ProblemDocument2 pagesWin Ballada Parcor Chapter 4 ProblemKrngyxNo ratings yet

- Requirement 1 Digos Trading Statement of Partnership Liquidation June 30, 20ADocument4 pagesRequirement 1 Digos Trading Statement of Partnership Liquidation June 30, 20AGvm Joy MagalingNo ratings yet

- Chapter 4Document5 pagesChapter 4Billy Vince AlquinoNo ratings yet

- Chapter 2Document27 pagesChapter 2Mary MarieNo ratings yet

- Miranda, Leon and EstoqueDocument1 pageMiranda, Leon and EstoqueHana0% (1)

- Part 2Document2 pagesPart 2PRETTYKONo ratings yet

- Liquidation 2Document3 pagesLiquidation 2Kenneth CuencaNo ratings yet

- Acp311 OperationDocument2 pagesAcp311 OperationAngeline Patac LumiguidNo ratings yet

- Henri Emanuel Reforba - Learning Task #2Document6 pagesHenri Emanuel Reforba - Learning Task #2Rhea BernabeNo ratings yet

- PARCOR - 2Nature-and-Formation-of-a-PartnershipDocument30 pagesPARCOR - 2Nature-and-Formation-of-a-PartnershipHarriane Mae GonzalesNo ratings yet

- Instructions: Compute The Amount of Ayesa's Capital Account at September 1, 2014Document10 pagesInstructions: Compute The Amount of Ayesa's Capital Account at September 1, 2014Nicole Fidelson0% (1)

- 1stLecture-Partnership LiquidationDocument25 pages1stLecture-Partnership LiquidationRechelle Dalusung100% (1)

- CHAPTER 16 - DIVIDENDS - Problem 3 - Computations - Page 597-599Document9 pagesCHAPTER 16 - DIVIDENDS - Problem 3 - Computations - Page 597-599Penelope PalconNo ratings yet

- CAlAMBA AND SANTIAGO - TUGOTDocument2 pagesCAlAMBA AND SANTIAGO - TUGOTAndrea Tugot100% (1)

- Quiz 2 For StudentsDocument4 pagesQuiz 2 For StudentsLorNo ratings yet

- Problem #9 Two Sole Proprietorship Form A PartnershipDocument3 pagesProblem #9 Two Sole Proprietorship Form A PartnershipNiño Rey LopezNo ratings yet

- MC With Answers Partnership Operation CorporationDocument19 pagesMC With Answers Partnership Operation CorporationASHLEY ROLAINE VICENTENo ratings yet

- MARVIN LISING Exercise 1 Installment Liquidation With Schedule of Safe PaymentsDocument5 pagesMARVIN LISING Exercise 1 Installment Liquidation With Schedule of Safe PaymentsMoon YoungheeNo ratings yet

- Parcor Proj (Version 1)Document45 pagesParcor Proj (Version 1)Jwhll MaeNo ratings yet

- Partnership Exercise 2Document5 pagesPartnership Exercise 2nikNo ratings yet

- Problem 20-23Document5 pagesProblem 20-23Teresa Pantallano DivinagraciaNo ratings yet

- Problem 6 1Document2 pagesProblem 6 1SerdenRoseNo ratings yet

- Chapter 7 Angel Ann E. Orola Bsba HR1 1Document90 pagesChapter 7 Angel Ann E. Orola Bsba HR1 1Gwen Stefani DaugdaugNo ratings yet

- Cfas ReviewerDocument7 pagesCfas ReviewerDarlene Angela IcasiamNo ratings yet

- Activity Partnership DissolutionDocument2 pagesActivity Partnership DissolutionKaren Joy Jacinto ElloNo ratings yet

- Solved Gloria Detoya and Esterlina Gevera Have Operated A Successful... - Course HeroDocument4 pagesSolved Gloria Detoya and Esterlina Gevera Have Operated A Successful... - Course HeroeannetiyabNo ratings yet

- Stephanie Calamba and Allan Brillantes SolutionDocument6 pagesStephanie Calamba and Allan Brillantes SolutionGerald RamiloNo ratings yet

- Parcor Chap 6 DoneDocument10 pagesParcor Chap 6 DoneJohn Carlo CastilloNo ratings yet

- ReviewerDocument15 pagesReviewerALMA MORENANo ratings yet

- ACCTG122 Homework On Partnership LiquidationDocument2 pagesACCTG122 Homework On Partnership LiquidationJoana TrinidadNo ratings yet

- P 2-1 (Cash and Net Assets Contributions)Document7 pagesP 2-1 (Cash and Net Assets Contributions)pjmerinNo ratings yet

- Accounting Midterm Exam (Partnership Up To Dissolution) : Answer: 103,500 346,500Document6 pagesAccounting Midterm Exam (Partnership Up To Dissolution) : Answer: 103,500 346,500JINKY MARIELLA VERGARA100% (1)

- Partnership Liquidation Exercises p.135Document6 pagesPartnership Liquidation Exercises p.135Kaye GomezNo ratings yet

- Incorrect: Discussion 7Document3 pagesIncorrect: Discussion 7Jasmine ActaNo ratings yet

- LiquidationDocument18 pagesLiquidationSamaica MontemayorNo ratings yet

- UntitledDocument4 pagesUntitledShevina Maghari shsnohsNo ratings yet

- CHAPTER 2 PartnershipDocument17 pagesCHAPTER 2 PartnershipLAZARO, Jaspher S.No ratings yet

- ParCor Chapter 5 - Hernandez - BSA 1-1 PDFDocument5 pagesParCor Chapter 5 - Hernandez - BSA 1-1 PDFBSA 1-1No ratings yet

- Accounting For PartnershipsDocument3 pagesAccounting For PartnershipsRixa Doreen Antoja50% (2)

- Chap 3 and 4 - ParcorDocument4 pagesChap 3 and 4 - ParcorAnne Gwynneth RadaNo ratings yet

- Par CorDocument27 pagesPar CorPam LlanetaNo ratings yet

- PROBLEMDocument3 pagesPROBLEMSam VNo ratings yet

- December 8 DiscussionDocument6 pagesDecember 8 DiscussionMark Domingo MendozaNo ratings yet

- Win Ballada Parcor Chapter 4 ProblemDocument2 pagesWin Ballada Parcor Chapter 4 ProblemKrngyxNo ratings yet

- Mara, Teri, and Rita Partnership Statement of Partnership Liquidation December 31, 2018Document6 pagesMara, Teri, and Rita Partnership Statement of Partnership Liquidation December 31, 2018Serenity CarlyeNo ratings yet

- MC6Document5 pagesMC6shudayeNo ratings yet

- Far QuizDocument7 pagesFar QuizMeldred EcatNo ratings yet

- Chapter 3 ParcorDocument6 pagesChapter 3 ParcorJwhll MaeNo ratings yet

- Parcor Proj (Version 1)Document33 pagesParcor Proj (Version 1)Jwhll MaeNo ratings yet

- APC Ch6solDocument25 pagesAPC Ch6solVaneza DayananNo ratings yet

- Partnership Liquidation - Lump-Sum Exercise 6-1Document23 pagesPartnership Liquidation - Lump-Sum Exercise 6-1ConnorNo ratings yet

- Partnership Liquidation Chap 6Document25 pagesPartnership Liquidation Chap 6Regine BaterisnaNo ratings yet

- Natural Obligations Study Guide I. DefinitionsDocument2 pagesNatural Obligations Study Guide I. DefinitionsLeinard AgcaoiliNo ratings yet

- Problem of The Week 1: AnswerDocument1 pageProblem of The Week 1: AnswerLeinard AgcaoiliNo ratings yet

- Takdang Gawain 4: Orihinal Na Akda: Boats in A StormDocument3 pagesTakdang Gawain 4: Orihinal Na Akda: Boats in A StormLeinard AgcaoiliNo ratings yet

- Chapter 4 (Section 2) Study Guide IDocument2 pagesChapter 4 (Section 2) Study Guide ILeinard AgcaoiliNo ratings yet

- Reflection PaperDocument2 pagesReflection PaperLeinard AgcaoiliNo ratings yet

- Chapter 4 (Section 1) Study Guide IDocument4 pagesChapter 4 (Section 1) Study Guide ILeinard AgcaoiliNo ratings yet

- Chapter 3 (Section 3) AGCAOILIDocument3 pagesChapter 3 (Section 3) AGCAOILILeinard AgcaoiliNo ratings yet

- Chapter 4 (Section 4) Study Guide IDocument2 pagesChapter 4 (Section 4) Study Guide ILeinard AgcaoiliNo ratings yet

- Chapter 3 (Section 1) Study Guide IDocument5 pagesChapter 3 (Section 1) Study Guide ILeinard AgcaoiliNo ratings yet

- Chapter 4 (Section 6) Study Guide IDocument2 pagesChapter 4 (Section 6) Study Guide ILeinard AgcaoiliNo ratings yet

- Chapter 4 (Section 3) Study Guide IDocument2 pagesChapter 4 (Section 3) Study Guide ILeinard AgcaoiliNo ratings yet

- Chapter 4 (Section 5) Study Guide IDocument2 pagesChapter 4 (Section 5) Study Guide ILeinard AgcaoiliNo ratings yet

- Study GuideDocument4 pagesStudy GuideLeinard AgcaoiliNo ratings yet

- ChapterDocument4 pagesChapterLeinard AgcaoiliNo ratings yet

- Contracts - Chapter 9Document2 pagesContracts - Chapter 9Leinard AgcaoiliNo ratings yet

- Chapter 2 (Section 2) Study Guide IDocument3 pagesChapter 2 (Section 2) Study Guide ILeinard AgcaoiliNo ratings yet

- Contracts - Chapter 2 (Section 3)Document2 pagesContracts - Chapter 2 (Section 3)Leinard AgcaoiliNo ratings yet

- Contracts - Chapter 8Document2 pagesContracts - Chapter 8Leinard AgcaoiliNo ratings yet

- Contracts - Chapter 3Document2 pagesContracts - Chapter 3Leinard AgcaoiliNo ratings yet

- Reflection Paper 2Document3 pagesReflection Paper 2Leinard AgcaoiliNo ratings yet

- Contracts - Chapter 7Document2 pagesContracts - Chapter 7Leinard AgcaoiliNo ratings yet

- Contracts - Chapter 2 (Section 1) AGCAOILIDocument3 pagesContracts - Chapter 2 (Section 1) AGCAOILILeinard AgcaoiliNo ratings yet

- Contracts - Chapter 2 (Section 2) AGCAOILIDocument2 pagesContracts - Chapter 2 (Section 2) AGCAOILILeinard AgcaoiliNo ratings yet

- Contracts - Chapter 1 AGCAOILIDocument2 pagesContracts - Chapter 1 AGCAOILILeinard Agcaoili100% (2)

- MFRS 1Document42 pagesMFRS 1hyraldNo ratings yet

- Branch Accounting ProblemDocument6 pagesBranch Accounting ProblemGONZALES, MICA ANGEL A.No ratings yet

- Case1 Big Bull CapitalDocument75 pagesCase1 Big Bull CapitalSakshi SharmaNo ratings yet

- RewiewerDocument34 pagesRewiewerMickaella VergaraNo ratings yet

- Business Administration Past PaperDocument23 pagesBusiness Administration Past PaperFahmeeda AhmedNo ratings yet

- WLCON 2022 17A Annual ReportDocument35 pagesWLCON 2022 17A Annual ReportJamaica AlejoNo ratings yet

- Cambridge Associates PE BenchmarksDocument11 pagesCambridge Associates PE BenchmarksDan Primack100% (1)

- Group 7: Country Report PresentationDocument51 pagesGroup 7: Country Report PresentationHà Anh NguyễnNo ratings yet

- UK Diabolo Manual-E05Document19 pagesUK Diabolo Manual-E05Eliott WalletNo ratings yet

- MIDTERM DRILL 1 TEST AnsweristsDocument6 pagesMIDTERM DRILL 1 TEST AnsweristsDan Andrei BongoNo ratings yet

- Chapter-4 Rectification of ErrorsDocument19 pagesChapter-4 Rectification of Errorslenovo lenovo100% (1)

- Does Shari'ah Screening Cause Abnormal Returns? Empirical Evidence From Islamic Equity IndicesDocument22 pagesDoes Shari'ah Screening Cause Abnormal Returns? Empirical Evidence From Islamic Equity IndicesJelena CientaNo ratings yet

- Keppel DC REIT - CircularDocument76 pagesKeppel DC REIT - Circulareuniceyl001No ratings yet

- FAR.3515_Cash_and_cash_equivalents_Document4 pagesFAR.3515_Cash_and_cash_equivalents_marlou mNo ratings yet

- Business and TechnologyDocument11 pagesBusiness and TechnologyBhaskar DasNo ratings yet

- Securities and Exchange Commission: Sec Form 17-A, As AmendedDocument4 pagesSecurities and Exchange Commission: Sec Form 17-A, As AmendedZinampan GarrijayNo ratings yet

- Adani Group - How The World's 3rd Richest Man Is Pulling The Largest Con in Corporate History - Hindenburg ResearchDocument147 pagesAdani Group - How The World's 3rd Richest Man Is Pulling The Largest Con in Corporate History - Hindenburg ResearchmanusolomonNo ratings yet

- Amity University Kolkata: Fundamentals of Financial ManagementDocument16 pagesAmity University Kolkata: Fundamentals of Financial ManagementSupratim RoychowdhuryNo ratings yet

- Mutual Funds ShivnadarDocument126 pagesMutual Funds ShivnadarKritika KoulNo ratings yet

- Balance Sheet of Maruti Suzuki IndiaDocument415 pagesBalance Sheet of Maruti Suzuki IndiaMahesh VaiShnavNo ratings yet

- Cash Flow Statement of AmulDocument6 pagesCash Flow Statement of AmulArav Sarin60% (5)

- CH 9. Working Capital and Tresury Mgt.Document5 pagesCH 9. Working Capital and Tresury Mgt.Tanvir PrantoNo ratings yet

- Reverse DCFDocument9 pagesReverse DCFjenkisanNo ratings yet

- Palepu - Chapter 5Document33 pagesPalepu - Chapter 5Dương Quốc TuấnNo ratings yet

- Concept Questions: Q.1. Payback Period and Net Present ValueDocument3 pagesConcept Questions: Q.1. Payback Period and Net Present Valuemiller jackNo ratings yet

- FAIS Assignment 1 - Mariam Jabbar PDFDocument4 pagesFAIS Assignment 1 - Mariam Jabbar PDFMariamNo ratings yet